Please see the below an article from Tatton Investment Management which was received this morning (14/11/2022) and details their thoughts on last week’s events and their impact on markets:

Overview: signs of ‘peak’ inflation emboldens markets

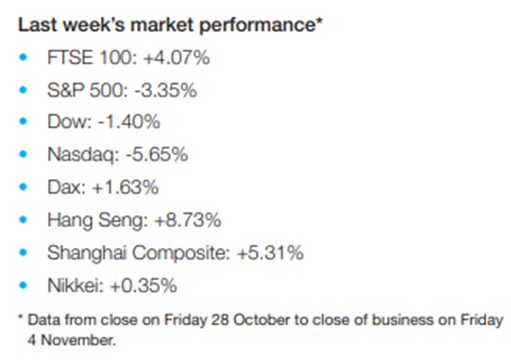

There were three big stories in capital markets last week: the US midterm elections, the latest crash in the surreal world of crypto currencies, and the release of US inflation data for October. By Friday, it was the lower-than-expected inflation data that took precedence. Thursday’s report from the Bureau of Labor Statistics revealed annual consumer price index (CPI) inflation slowed to 7.7% in October, below the 8% expected by most economists, and the lowest level since January. So, for the first time this year it appeared that current rising inflation may be over for the US. While it is still too early to assume the Federal Reserve (Fed) will pivot away from its monetary tightening policy, the market euphoria following the data release was quite something. We may not have reached the actual turning point in terms of shifting economic tides, but perhaps this week’s activity confirms our suspicion of the shared belief among market participants that the current economic downturn is more likely to be shorter and shallower than some scaremongers (including the Governor of the Bank of England) suggest.

Last week also saw FTX, the second-largest crypto exchange, become a casualty of both crypto’s defining feature (lack of regulation) and the less forgiving market environment. It turns out that diehard cryptocurrency traders still prefer the stability of the money created by central banks. For us, what is most interesting about this episode is the likely impact on general credit spreads – the proverbial canary in the coalmine of capital markets during economic downturns. While FTX’s demise and bankruptcy filing is still in its early stages, talk of FTX as a “mini-Lehman” will depend on which financial institutions report large exposures (if any). This may change this week when the impact of FTX’s related hedge fund, Alameda Research, on prime brokers and other hedge funds emerges.

As we head towards the close of the year, when asset managers have a tendency to shut down exposures, last week’s positive upturn certainly felt encouraging. However, investors should not expect 2022’s market pressures to end here. The Fed’s December meeting may well cause yet another turn in market sentiment and the underlying corporate profit development, coupled with thinning seasonal liquidity from institutional investors, leaves us bracing for more potential volatility before the year ends.

Republican ‘red wave’ fizzles out

Last week’s midterm elections in the US had been labelled as the most important midterms in recent memory, with democracy itself on the ballot. But while Republicans went as far as to predict a ‘red wave’, the weekend brought news that the Democrats had retained Senate control at least, with the House of Representatives still up for grabs. The Republican party’s underperformance was an unwelcome surprise for capital markets last week, mostly because investors crave stability, which means a preference for the status quo and even political gridlock.

For markets, the real test lies in judging what fiscal policy will emerge after all the votes have been counted. The Democrats have shown a desire to increase the overall tax base in line with spending proposals – coming out at fiscally neutral – and control of the Senate could them make progress with this agenda. What the future holds for the Republican party after this ballot box set back is much less clear, and could come down to whoever gains the Republican presidential nomination in 2024. Trump is expected to announce his candidacy this week and, were he to be successful, some fear a return to fiscal indiscipline, especially in the face of slower growth. On the other hand, the unexpectedly poor performance of Republicans – particularly those linked to Trump himself – suggests the party may field someone else. That someone would almost certainly be Florida Governor Ron DeSantis. His successful re-election campaign was built around promises of sales-tax cuts targeted on everyday items, which would benefit the less well-paid. It is yet to be seen how the lower tax revenues will impact Florida’s provision of public services. It would be difficult to achieve a similar policy at the federal government level, as sales tax is levied by the states, so the equivalent would be lower income tax.

Meanwhile, Biden and the Democrats gained a fillip from the electorate, and will be poring over the voter data and surveys to divine what were the key positives. Recapturing the Senate gives Biden some ammunition to counter critics who believe his age and frailty should render him a one-term-only president. The Democrats have no obvious centre-ground alternative candidate themselves, but Trump’s early entry into the nomination race means they may wait to see how things pan out, especially if the Republican fight gets messy. With Trump involved, it almost certainly will.

To PE or not to PE? That is the question

This year, private equity (PE) has protected some of the world’s largest investors from the misery in publicly-traded securities. On average, PE firms recorded 1.6% of gains in the first quarter of 2022, and only some mild falls since then. Publicly-traded global equities by contrast are down 22% over the same timeframe. Lower volatility does not seem to come at the cost of growth either. The industry has grown exponentially in the last decade and a half and, while it was thought rising interest rates would make things much harder, PE firms predict a bright future. According to BlackRock analysts, returns from US private equity are expected to eclipse other asset classes over the next decade.

Of course, when something seems too good to be true, it usually is, especially when you remember that private fund managers set those fund valuations themselves. Private equity funds hold their assets for a long period, so at any given time it is difficult to work out what the market value for those assets should be. And on other measures, the private equity market looks much less rosy. Carlyle Group, for example, has lost more than half of its stock value this year – despite flat or even positive reported returns in its underlying assets.

PE funds also recently struggled to attract capital in similar amounts as in recent years. That much should be expected, given the tightening of global financial conditions. But this is being compounded by the so-called ‘denominator effect’. PE funds work by setting up a closed-end fund for certain acquisitions, then drawing in ‘limited partners’ (LPs) to foot the bill. These funds are then managed by PE firms like KKR or Carlyle – which take a healthy chunk of the profits – but the risks are borne by the LPs. The problem comes from the fact that the LPs are often large institutional investors like pension funds, which have strict regulatory requirements on where they can put their money. These rules often dictate that only a certain percentage of an overall portfolio can be put into private assets, usually in the 20-30% range. If those PE funds outperform other parts of the portfolio by a significant margin – as seen this year – the ratio gets out of kilter. PE backers therefore have to pull out some funding as a regulatory requirement.

Many have taken to calling on existing LPs for more capital. Large pension funds and the like should have enough cash to do so, but smaller investors may be forced to sell some assets to meet these payments. Given how large PE exposure has become over the last decade and a half, this could have serious knock-on effects in publicly-traded markets. Moreover, if PE funding continues to dry up and firms keep having to make capital calls, we could see a similar liquidity crunch

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Carl Mitchell – Dip PFS

Independent Financial Adviser

14/11/2022