Please see below article received from Evelyn Partners earlier this morning, which provides details on today’s UK December CPI inflation announcement.

What happened?

UK December annual headline CPI inflation was reported at 10.5% (consensus: 10.5%), down from 10.7% in November and a peak of 11.1% in October. The CPI monthly increase was 0.4% (consensus: 0.3%), compared to 0.4% in November.

What does it mean?

There is increasing evidence that UK headline CPI inflation has peaked and is being led down by lower energy prices. High frequency data show that this has further to go. Take wholesale one-month ahead natural gas prices. They have now fallen to below the pre-Russian invasion of Ukraine level and are down 19% so far in January. This should reduce the upward pressure in household energy bills. Petrol prices are also declining. The latest price of unleaded petrol on 17 January was £1.50, down from £1.52 at the end of 2022 and a peak of £1.92 last summer. Expect lower energy prices to exert downward pressure on inflation, at least in next month or two.

Looking beyond the near term, slowing economic growth, along with higher taxes and rising mortgage rates, are likely to be a drag on real household take-home pay in 2023. Lower discretionary incomes should prove to be a significant headwind against another upward acceleration in inflation from here. Moreover, high base effects from sharp price increases in 2022 will make it difficult to sustain high annual CPI inflation rates in 2023. Finally, the impact of supply chain disruption on prices in the goods market should begin to fade, while recent sterling appreciation will lower the cost of imported goods.

The Bank of England (BOE) expects headline CPI inflation to essentially halve to around 5% by the fourth quarter of 2023. Even so, core CPI inflation (excluding food, energy, alcohol and tobacco) remains fairly sticky. The risk to BOE’s inflation outlook is the potential secondary impact of workers demanding higher wages to keep up with the high cost of living. With the unemployment rate still near cyclical lows, there is a possibility that higher wage rates become entrenched in the economy, increasing the risk of a wage-inflation upward spiral.

Bottom Line

Given the current high rate of consumer price rises, the Bank of England will likely raise interest rates again at its next Monetary Policy Committee meeting on 2 February.

For investors, elevated inflation and likely negative GDP growth in 2023 are clear risks. However, the UK economy is not the equity market, and this probably explains why UK stocks gained nearly 17% more than the rest of the world in 2022, its biggest beat since 1990.

Moreover, UK-listed multinationals are largely linked to what goes on in the rest of the world. Looking forward, the reopening of the Chinese economy from Covid zero policy is a shot in the arm for externally focused UK companies. China seems to be willing to go for growth by relaxing restrictive policies applied to its all-important property sector. According to a Bloomberg report in early January, the Chinese authorities are set to raise lending caps for developers and extend the deadline for firms to meet debt limits. This could be a green light from the Chinese leadership to go for growth and should support overall UK EPS growth. Analysts are already starting to revise up 2024 UK EPS growth expectations in anticipation of global economic recovery. Given low valuations, UK stocks can perform this year.

Please check in again with us soon for further relevant content and market news.

Please see below, Brewin Dolphin’s ‘Markets in a Minute’ article summarising the key economic and markets news from the last week. Received late yesterday afternoon – 17/01/2023

Stocks rally on hopes of milder recession

Most major stock markets rose last week as better-than expected economic data helped to ease recession fears.

The FTSE 100 gained 1.9% after UK gross domestic product (GDP) unexpectedly grew in November, thanks to a boost from the men’s football World Cup. Germany’s Dax also rallied 3.3% as GDP data pointed to a milder economic slowdown over winter.

In the US, the S&P 500 and the Nasdaq surged 2.7% and 4.8%, respectively, helped by gains in large technology stocks such as Amazon and Microsoft. Signs of easing inflationary pressures also helped to boost investor sentiment.

In China, the Shanghai Composite added 1.2% on hopes that demand will rebound over the next few months following the scrapping of the country’s zero-Covid policy. Economists in a Reuters poll projected growth of 4.9% this year versus an estimated 2.8% in 2022.

BoJ monetary policy in the spotlight

Stock markets were generally quiet on Monday (16 January) as US indices were closed for Martin Luther King Day. In Asia, however, the Nikkei 225 fell 1.1% after data showed a higher-than-expected 10.2% increase in wholesale prices in December. This added to speculation that the Bank of Japan (BoJ) could phase out its monetary stimulus and start raising interest rates. It comes less than a month after the BoJ surprised the markets by widening its tolerance range for ten-year government bond yields, as part of its yield curve control policy.

The FTSE 100 started Tuesday’s trading session in the red after data showed UK wages grew at their fastest rate in more than 20 years in the three months to November. Regular pay excluding bonuses rose by 6.4% year-on-year, although they were down 2.6% after adjusting for inflation. The unemployment rate rose slightly from 3.5% to 3.7%.

UK economy grows 0.1% in November

Last week, figures released by the Office for National Statistics (ONS) raised hopes that the UK may have avoided sliding into a recession in 2022. GDP grew by 0.1% in November, beating analysts’ expectations of a 0.3% contraction. The services sector was the main driver of growth, expanding by 0.2% as football fans headed to bars and pubs to watch the World Cup.

A technical recession is defined as two consecutive quarters of falling economic output. GDP fell by 0.3% in the third quarter and economists were expecting a similar fall in the fourth quarter. However, Darren Morgan, ONS director of economic statistics, told BBC Radio 4’s Today Programme that for the UK to enter a recession in the fourth quarter, GDP in December would need to contract by 0.6%.

The figures could add to pressure on the Bank of England (BoE) to continue raising interest rates. Markets currently expect the BoE to increase the base interest rate by 0.5 percentage points to 4.0% at its February policy meeting.

German GDP surpasses pre-Covid level

GDP figures for Germany were also better than expected. Despite the war in Ukraine, high energy prices and supply Markets in a Minute 17 January 2023 chain bottlenecks, the economy managed to perform well in 2022, with the services sector benefitting from the lifting of lockdown restrictions.

GDP grew by 1.9% in 2022 and exceeded its prepandemic level of 2019 for the first time. The Federal Statistical Office said growth was likely to have stagnated in the fourth quarter, suggesting the economic slowdown over winter will be milder and shorter than previously thought.

It came after a German government economic adviser told Reuters that domestic inflation had probably peaked thanks to falling global energy prices.

US monthly inflation falls for first time since 2020

Over in the US, the highly anticipated consumer price index (CPI) report showed month-on-month inflation fell in December for the first time since May 2020. Headline inflation eased by 0.1%, bringing the year-on-year increase to 6.5%, the lowest since October 2021.

Please continue to check our Blog content for advice, planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see the Weekly Market Commentary from Brooks Macdonald received yesterday:

US inflation met market expectations, allowing US equities to rise during the week

Equity markets have continued their strong start to 2023, with the US Consumer Price Index (CPI) number coming in line with market expectations. This week sees the US earnings season start to ramp up despite a US holiday on Monday and Wednesday’s highlight will be the Bank of Japan meeting which may contain some policy tweaks.

The market now expects the US Federal Reserve (Fed) to raise interest rates by only 25bps on 1st February

With the CPI release matching market expectations, the bond market was quick to price in a smaller Fed rate hike when the committee meets in a few weeks’ time. The market now expects 27.2bps of rate hikes in February as of Friday’s close, suggesting investors are only assigning a very low probability to a larger 50bp rate hike. This week we have a number of Fed speakers who will update their monetary policy views in light of the latest CPI and wage numbers. Next weekend sees the beginning of the communication blackout ahead of the next Fed meeting so the rhetoric used this week will be of crucial importance to bond markets. Whilst there is no direct inflation data this week, Wednesday’s Retail sales number will be a good barometer for consumer demand. Retail sales are expected to have declined last month as weaker car sales combine with lower gasoline prices.

The Bank of Japan meets with Japanese inflation rising and Japan yet to raise interest rates this cycle

Japan remains a stark outlier amongst other global central banks, having not risen interest rates during this cycle. Even if we do not see a change to monetary policy this week, the bank’s inflation forecasts are likely to have risen, driving a debate around a future tightening of policy. Indeed, a day after the Bank of Japan meets, the countries’ inflation data will be releases with headline inflation expected to have risen by 4% year-on-year. With the annual wage negotiation cycle in Japan coming up, the level of national inflation will undoubtedly influence wage demands, a risk the Bank of Japan will be well aware of.

Last week’s US CPI release saw US equities post a strong week, outperforming European equities. One of the major drivers looking forward will be the Q4 earnings season where analysts are expecting a year-on-year decline in corporate earnings of almost 4%. This week sees large US banks report as well as some of the cyclical bellwethers in the US such as Alcoa, Kinder Morgan and Schlumberger. While the market has welcomed weaker economic data, such as the ISM services survey earlier this month, it will still be hoping for robust corporate numbers.

Please continue to check our Blog content for advice, planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see the below article from Tatton Investment Management with their thoughts on the likelihood of a recession in the UK in the near future. This article was received this morning, 16th Jan 2023:

Overview: Football fever helps stave off UK recession

The new year is proving to be a happy one for almost all asset classes and regions. Here in the UK, the FTSE 100 closed on Friday at 7,844 less than 60 points from its all-time high. The global financial press tells us markets are stronger because of fresh optimism of a likely easing in monetary policy because – as business leaders say – conditions are awful. And yet things are not that awful. On Friday, the Office for National Statistics (ONS) reported that UK gross domestic product (GDP) unexpectedly rose 0.1% in November. According to the ONS, the Qatar World Cup marginally helped consumer-facing businesses and the impact of strikes was not that severe. Unless December’s GDP figure falls more than 0.4%, the UK economy should avoid a technical recession in Q4 2022.

The Bank of England (BoE) had anticipated a recession was already underway in 2022’s second half, although its monetary policy views are more concerned with supply-side weakness, a problem it sees lasting into 2024. On Friday morning, Monetary Policy Committee (MPC) member Catherine Mann suggested the surveys showing still above-target UK household and business inflation expectations would mean larger rate rises were still on the cards. The European Central Bank (ECB) also seems firm in pushing ahead with rate rises, to the point of actively constraining economic activity. Even though it is lower than elsewhere, European core inflation is at its highest-ever level, and policymakers are still very worried about inflationary dynamics. Lagarde says these “are mainly related to fiscal measures and wage dynamics,” and the ECB still needs to tighten hard to counteract them.

Across the pond, members of the US Federal Open Markets Committee (the equivalent to the UK’s MPC) were also vocal that rates are still going up, although US bond investors believe the rate rises are nearly done. The slowing of wage rises is also apparent, as the average hourly earnings data showed in last week’s nonfarm payrolls. At the same time, few investors appear to believe a US recession is about to take hold. The bond market also tells us that fears of defaults in the credit market are declining – a stronger indicator of recession fear than the yield curve inversion.

Fears that the world was close some sort of economic precipice seem to have dwindled significantly. Investors may already be discounting a rosier picture, one where the nasty risks of 2022 seem to have ebbed quickly away. But the central bankers may need some convincing that a wage-price spiral is no longer a danger, given that as yet there is only the mildest of hints that the pressure has eased. We’ve had two weeks of ‘bad news is good news’ helping the markets. For markets to go higher in the long-term, let’s hope we have a run of ‘good news is good news’.

Commodities set to run hot once again

Last year was a strange one for commodity markets. Russia’s invasion of Ukraine wrought the biggest disruption to global energy supplies in a generation, causing oil and gas prices to soar over the first half of 2022. Sharply higher prices then destroyed demand and severely dampened the outlook for global growth. Oil and gas had a much weaker second half, as supply chains re-adjusted and demand fell significantly. Even European gas prices, which rose to eye-watering levels after President Putin turned off the tap, are substantially lower than their mid-year peak. Policymakers, analysts and capital markets predicted a harsh winter for Europe, with heat and energy rationing amid acute undersupply. However, this winter is predicted to be one of continent’s warmest on record, taking the edge off fuel prices.

This would appear to dampen the commodity outlook, but demand from China could reverse this dramatically. Beijing has now suddenly pivoted to an extremely pro-growth policy mix. The zero-Covid policy is ending, restrictions on the property sector are vanishing, and the People’s Bank of China is actively loosening monetary policy. There is likely to be a splurge of infrastructure building as we go through 2023, which will spark massive demand for raw materials. This is about as big a boost as the government could possible muster – making China’s domestic economy look like a coiled spring – and significantly improves the outlook for global commodities.

Chinese assets have rallied in the new year, and markets appear to be significantly frontrunning demand. Given Covid is still hampering activity, it could be some time before actual demand comes through. And given how much positivity is priced in, markets could be disappointed by Chinese growth. That said, China’s post-Covid bounce could well be even stronger than the one experienced in the western world. More than 1.4 billion people have been under some form of restrictions for more than three years, suppressing a great deal of their regular economic activity. There is a massive amount of pent-up consumer demand waiting to be released. On top of this, the Chinese government is easing other key policy areas like construction and finance. Not only will people want to go out and spend, but businesses will be eager to undertake projects put on hold for years – and they will have the capital needed to do so.

It is true, however, that we may have to wait before such strong demand comes through. Covid infections are extremely high and, even without government restrictions, this will inevitably hamper movement until cases come down. The Lunar New Year festival in February – usually a very active period – will likely be significantly busier than last year, but the virus will probably keep activity at relatively subdued levels , and it might not be until warmer weather comes in March that we see the turnaround become meaningful.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below the Evelyn Partners Update with a look into the US December CPI inflation data. Received yesterday afternoon – 12/01/2023

What happened?

US headline CPI inflation rose 6.5% year-on-year in December (consensus: 6.5%), compared to 7.1% in November. On a monthly basis CPI decreased -0.1% (consensus: -0.1%) compared to a 0.1% rise last month. The index for gasoline was by far the largest contributor to the monthly decrease, more than offsetting increases in shelter indexes.

Core CPI inflation, which excludes food and energy, came in at 5.7% (consensus: 5.7%) year-on-year, which compares to a 6% rise in November. On a monthly basis, core CPI rose 0.3% (consensus: 0.3%), versus 0.2% rise in November.

What does it mean?

With headline inflation continuing to decelerate, market attention will now turn to the all-important question: what does this mean for the Federal Reserve’s tightening cycle?

Taking the Fed at face value, one might expect to see more interest hikes than currently being priced by markets (25bps in Feb and 25bps in March). Federal Open Market Committee (FOMC) members have continued to sound hawkish, with the latest FOMC minutes highlighting their displeasure at the recent loosening in financial markets conditions, which they believe will damage their attempts to bring inflation back towards target.

Moreover, today’s inflation report provided a mixed picture with regards to the three inflation indicators that Jay Powell is following. Goods prices continued to fall but core services and housing inflation remained resilient. Core services excluding shelter gained 0.25% month-on-month (MoM), against 0.12% in November. Similarly, shelter shows no sign of abating and gained 0.8% MoM (vs 0.6%) in November.

But on the other hand, a series of papers have recently been published by the regional Fed banks which have adopted a more dovish tone. Most notably, analysis from the Federal Reserve Bank of Philadelphia found that in aggregate 10,500 net new jobs were added to the economy in Q2’22, instead of the 1,047,000 jobs estimated by the Bureau of Labor Statistics’ (BLS) Current Employment Statistics (CES). While the Cleveland Fed constructed a new, timelier, index to measure rental prices. The new measure was found to lead the BLS measure (used by the Fed) by four quarters and estimates that annual CPI rent inflation will peak in Q1/Q2’23. Given that rent is the largest CPI component, this has major implications for monetary policy. Could this new data provide some cover for the Fed to announce a pause in the first quarter?

Either way, in the near term we expect the Fed will continue to remain data-dependent given the challenges in accurately forecasting CPI. It’s unlikely they will telegraph ‘the pause’ in advance as they will want to avoid further loosening in financial conditions.

With inflation data consistent with expectations, markets continue to price the Fed funds rate to peak at ~5% in March 2023; US equity futures are rallying.

Bottom Line

Today’s report provided more evidence that US inflation is slowing, although components of core inflation continue to look ‘sticky’.

As the impact of interest rate hikes start feeding through into the real economy, we expect US economic activity to remain below trend next year. We favour adding defensive names to prepare for this.

Please continue to check our Blog content for advice, planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below today’s Daily Investment Bulletin from Brooks Macdonald, with a look ahead at Inflation data coming out of the US today. Received this morning – 12/01/2023:

What has happened

As markets eagerly await the US CPI release later today, there was growing optimism that inflation would quickly fade in 2023, buoying equity and bond markets. US 10-year Treasury yields fell with the benchmark yields sitting at 3.53% at the time of writing. Short-dated Treasury yields remained more robust with the Fed still expected to continue with tight monetary policy in the short term, even if we see a downside surprise to inflation today.

EU green subsidies

Risk appetite was also helped yesterday by reports suggesting that the German Chancellor was supportive of a fresh joint EU financing scheme which would provide a counter-balance to the US’s green subsidies which have been instigated by the recent blockbuster Biden bills. The optimism also extended to a broader hope that the EU was more likely to provide bloc wide measures looking forward, in good times and bad. The difference between Italian and German 10-year yields was a direct beneficiary of this with the spread narrowing by almost 0.3% since the start of the year, as investors imply that Germany would ultimately be warmer towards fiscal burden sharing.

US Inflation

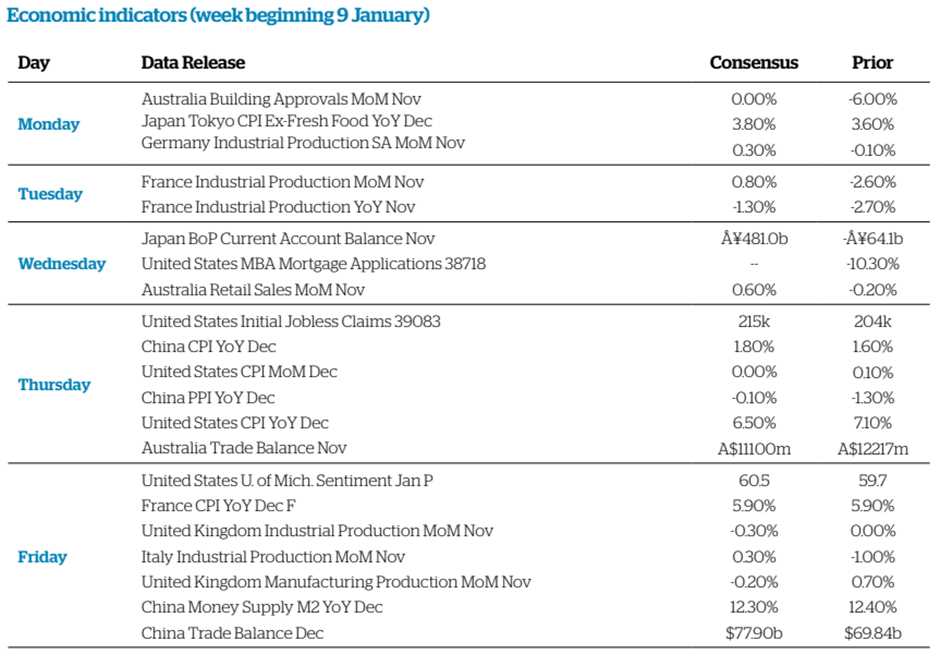

With the European inflation numbers pointing to a possible global retrenchment in inflation pressures, hopes have been riding high that we will see a third downside miss to the US CPI release today. Lower inflation now will open up far more options for global central banks to respond to the downturn in economic growth expected in 2023 therefore inflation remains critical to the outcome for US and European GDP this year. As a reminder, the economist consensus expects US headline CPI to fall to 6.5% and for the core figure, which excludes food and energy, to fall to 5.7%. While the initial reaction will be to these primary figures, bond markets will also be studying the sub-components to see if there are signs of slowing inflationary pressures amongst some of the stickier items in the CPI basket.

What does Brooks Macdonald think

As ever, it is hard to overstate the importance of today’s CPI figures. The current rally we have seen in risk assets, while moderate against the context of 2022’s falls, is predicated on an easing inflation backdrop. With inflation appearing to fall, markets are more confident that monetary policy can ease when economic growth recedes, avoiding a harsh recession. A large upside beat to the numbers today would call this into question making 13:30 today a vitally important time for markets.

Please continue to check our Blog content for advice, planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below ‘Markets in a Minute’ article received from Brewin Dolphin yesterday afternoon, which provides a positive global market update as we continue through the first month of 2023.

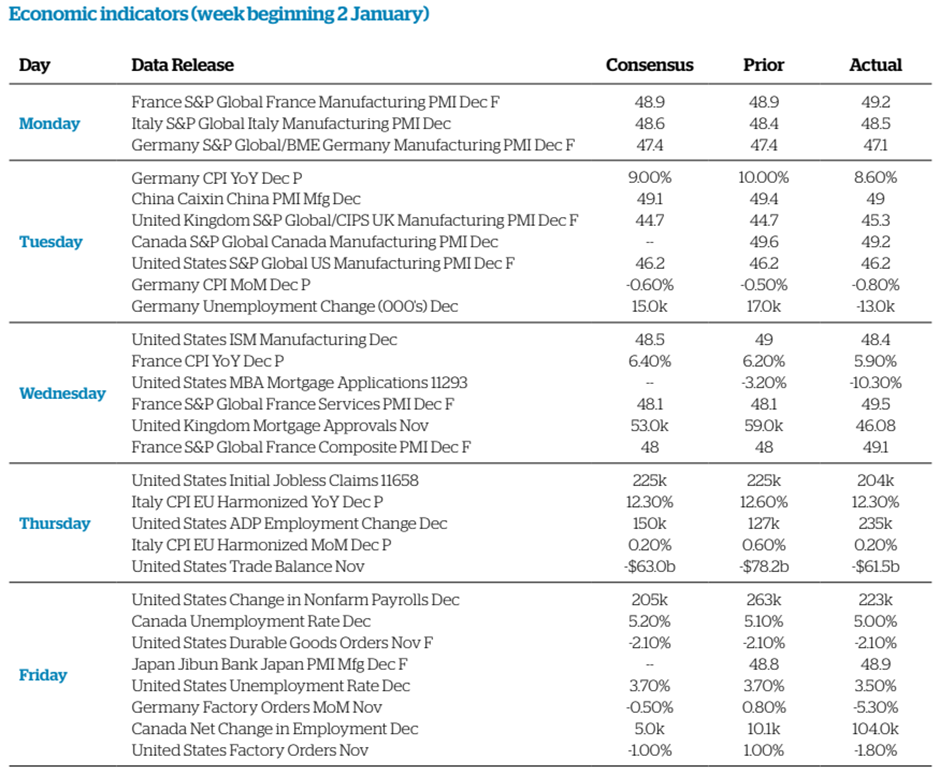

Most major stock markets finished their first week of 2023 in the green as data suggested inflation was cooling in both the US and Europe.

The S&P 500 and the Nasdaq ended their four-day trading week up 1.5% and 1.0%, respectively, after Friday’s nonfarm payroll report raised hopes the Federal Reserve could engineer a ‘soft landing’ for the US economy – i.e. slowing inflation without sparking a significant recession.

The pan-European STOXX 600 and Germany’s Dax surged 4.6% and 4.9%, respectively, as inflation in the eurozone fell below 10% for the first time in two months.

In Asia, the Hang Seng surged 6.1% and the Shanghai Composite added 2.2% on news that Hong Kong was considering reopening its border with mainland China after three years of coronavirus restrictions.

Stocks rally as Hong Kong-China border reopens

Stocks extended gains on Monday (9 January) after Hong Kong and China resumed quarantine-free travel over the weekend. It is hoped the reopening will provide a much-needed boost for Hong Kong’s economy, which is projected to have shrunk by 3.2% in 2022, according to reports in the Financial Times. The Hang Seng gained 1.9% on Monday while the Shanghai Composite added 0.6%. The positive sentiment spread to Europe, where the FTSE 100 climbed to its highest level since August 2018. In contrast, US indices slipped into the red as investors looked ahead to this week’s inflation data and earnings reports from major banks.

US jobs growth slows

The release of the official nonfarm payrolls report last Friday showed US jobs growth slowed for a fifth consecutive month in December. This fuelled optimism among some commentators that the Federal Reserve will be able to slow its pace of interest rates hikes and, in turn, avoid sparking a severe recession.

According to the Bureau of Labor Statistics, 223,000 jobs were added in the final month of 2022. This was above consensus expectations, but less than the 256,000 jobs added in November.

Average hourly earnings growth slowed to 0.3% month[1]on-month, and November’s wage growth was revised down from 0.6% to 0.4% month-on-month, easing concerns about wage inflation. Nevertheless, the average wage gain over the past two months has amounted to 0.35%, which is slightly higher than what would be considered consistent with the Federal Reserve hitting its 2% inflation target. The unemployment rate also dropped back to its cycle low of 3.5%, while the job openings to unemployed ratio remained very high.

Services and manufacturing activity fall

Separate data released on Friday showed services and manufacturing activity in the US fell in December, but so did price pressures. The Institute for Supply Management’s (ISM) services index dropped to 49.6, putting it into contraction territory (below 50.0) for the first time since May 2020. Excluding the Covid-19 pandemic slump, this was the weakest reading since late 2009. Prices paid continued to increase but at their slowest pace since January 2021.

Meanwhile, manufacturing activity contracted for the second month in a row, falling to 48.4 in December from 49.0 in November. Prices paid by manufacturers dropped sharply to their lowest level since February 2016, excluding the early pandemic plunge.

Eurozone inflation returns to single figures

Last week also brought encouraging signs of easing inflation in the eurozone. Lower energy prices helped the annual inflation rate fall to 9.2% in December from 10.1% in November, according to Eurostat’s flash index. However, core inflation, which excludes volatile food and energy prices, rose to a new high of 5.2% year-on-year, exceeding economists’ expectations.

It came after François Villeroy de Galhau, governor of the Banque de France and a European Central Bank (ECB) policymaker, said interest rates would need to rise further to reduce underlying price pressures. The ECB is expected to raise rates by 0.5 percentage points at both its February and March policy meetings.

UK mortgage approvals fall sharply

Here in the UK, data from the Bank of England showed mortgage approvals fell to their lowest level in two years in November as increased borrowing costs put off buyers. Approvals fell to 46,100, down from 57,900 the previous month and the lowest level since June 2020, when the pandemic brought the housing market to a standstill. The interest rate paid on new mortgages rose by 26 basis points to 3.35% in November, the highest since 2013.

Separate figures from Halifax showed the average house price fell by 1.5% in December from the previous month. Halifax said it expects house prices to fall by around 8% during 2023, which would see the cost of the average property returning to April 2021 prices.

Please check in again with us soon for further relevant content and news.

Please see below the latest Brooks Macdonald Weekly Market Commentary update, which was published and received today (10/01/2023):

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below, Evelyn Partners’ Investment Outlook providing a monthly round-up of global markets and trends. Received Friday afternoon – 06/01/2023

Playing the field for yield in 2023

2022 was a tumultuous year for financial markets. Both bond and equity prices fell sharply, a rare and unwelcome occurrence for multi-asset investors, as central banks moved abruptly to more aggressive monetary policy to address the highest inflation seen for 40 years.

Given the volatility seen in financial markets, in 2023 we expect investors to remain defensive and seek income-yielding securities backed by reliable cashflows to protect against potential further falls in markets. Excluding the pandemic, the good news is that the sell-off has led to the widest dispersion of dividend yield in global stocks for 13 years. In other words, dividend yields are high and there are more companies paying attractive yields. Assuming dividends are not cut, this is a time to play the field for yield and lock in the income they provide.

Our analysis finds the highest one-year forward dividend yields are in the energy sector at 4.1%. This is supported by elevated energy prices and capital expenditure discipline. Defensive areas of the equity market (e.g. consumer staples and utilities) and materials also score well on this front. This is in stark contrast to the low-yielding information technology, consumer discretionary and communications services sectors — which all pay dividend yields of less than 1.6%. There is an opportunity cost for sticking with such low-yielding stocks when short-term interest rates have risen and offer a higher return.

We see similarities in stock markets across different geographies. UK equities are expected to pay a dividend yield of 4.3%, the highest out of the major developed stock markets. This is supported by healthy company cashflows. The US, in contrast, is the lowest yielding market on 1.7%. Throughout 2023 we expect money to continue to flow into cashflow-backed income yielding assets, such as UK large-caps.

Once the US Federal Reserve (Fed) stops raising interest rates, possibly by the summer of 2023, it may provide a chance to acquire government bonds where yields are up from a year ago and economic growth is slowing. A Fed pause may also be a catalyst for Asian (ex-Japan) stocks should it weaken the US dollar, which would help encourage capital to flow back to the region. An improving situation in China, driven by the end of its zero-Covid policy, is another reason why Asian stocks could outperform global markets in 2023.

Balancing market headwinds and tailwinds

The stock market outlook still appears uncertain. Investors face plenty of headwinds, including lower global growth following interest-rate hikes and the cost-of-living crisis. Oxford Economics projects subdued global real GDP growth of 1.2% in 2023, well below the 2.9% estimated for Investment outlook Playing the field for yield in 2023 2022. For investors, slower growth implies a downside risk to the consensus estimate of 3% Earnings Per Share growth for the MSCI All Country World equity index.

There are also plenty of geopolitical concerns for investors to consider. For instance, Washington raised tensions with Beijing by imposing an effective ban on US tech companies exporting high-spec chip-manufacturing equipment to China on 7 October. Meanwhile, the Chinese military has held increasingly aggressive operations close to the borders of Taiwan. While there seems no sign of easing in Sino-US tensions, at least there are no scheduled presidential or general elections in G7 countries over the next year — the first time that has happened this century. This provides some stability and may help to ease political uncertainty.

In spite of choppy markets there are tailwinds to lift equities higher. Inflation is set to peak around the globe, giving central banks room to ease off from raising interest rates. Our analysis of the last six Fed hiking cycles shows that US stocks rose by 18%, on average, over the 12 months following a pause in rate increases.

Another tailwind would be if growth surprises on the upside. A lot depends on China. The Chinese authorities have largely scrapped their zero-Covid policies in response to the social unrest seen in many cities. With plenty of stimulus pumped into the economy already, Oxford Economics expects China’s real GDP growth to accelerate to 4.2% in 2023 from 3.1% in 2022.

And finally, US CPI inflation has come in below market expectations in the last two months, with the majority of economists anticipating a steady slowing throughout 2023. As inflation decelerates, real take-home pay (and spending) can be expected to recover. US household balance sheets are in decent shape following years of debt reduction since the Global Financial Crisis in 2008. Furthermore, consumers also have aggregate ‘excess’ personal savings built up since the pandemic of around $2 trillion (circa 10% of take-home pay), which can help to cushion the rise in the cost of living.

In our view, much of the bad news is now baked into global stock market valuations. The MSCI All Country World index trades at an undemanding price-to-earnings ratio of 15 times, well down from the cyclical peak of 20 times in September 2020. This creates a favourable platform for higher dividend-yielding stocks to perform in 2023. Nevertheless, expect plenty of market volatility as the global economy nurses its way through an inflationary hangover.

Market Highlights

Equities

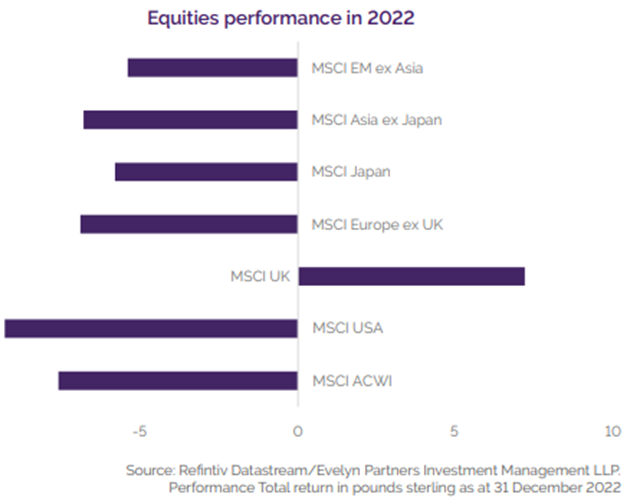

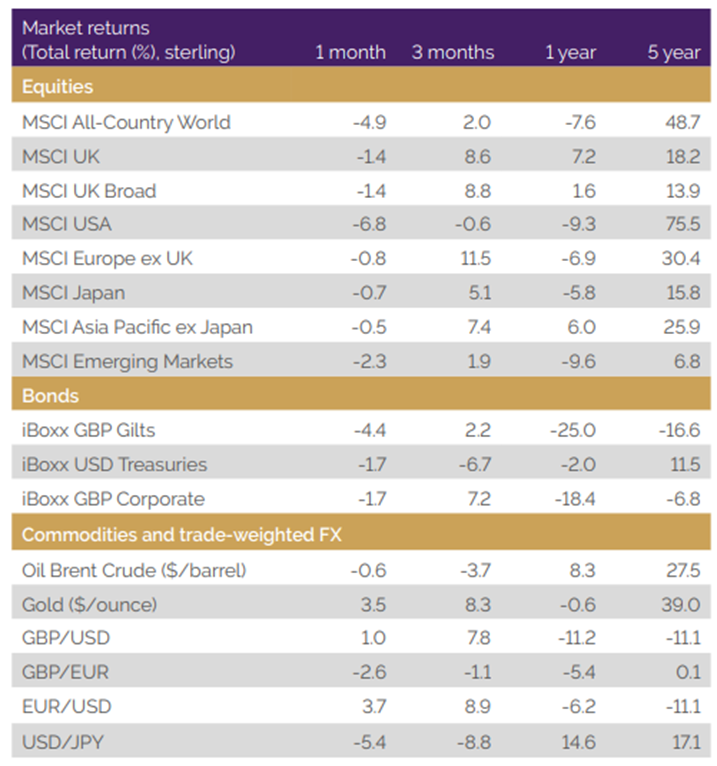

2022 was a year fraught with macro headwinds resulting in the worst performance of global equities since 2008. Rampant inflation prompted central banks to implement aggressive interest rate hikes that saw sensitive growthoriented stocks fall from the high valuations seen at the end of 2021. The US bore the brunt of this. MSCI USA fell 9.3, with the mega caps (Apple, Microsoft, Amazon, Tesla, Alphabet and Meta Platforms) falling, on average, by 42.2%. The war in Ukraine further compounded economic uncertainty and the resulting energy crisis contributed to Europe falling 6.9% over the year. Asian equities were not immune with China’s zero-Covid policy and the strong US dollar hampering growth in the region. Despite the troubling economic backdrop, the UK stock market returned 7.2%, substantially outperforming its peers. This was due to its bias towards defensive ‘value’ sectors such as healthcare, consumer staples and materials as well as a large exposure to the energy giants, BP and Shell.

Fixed income

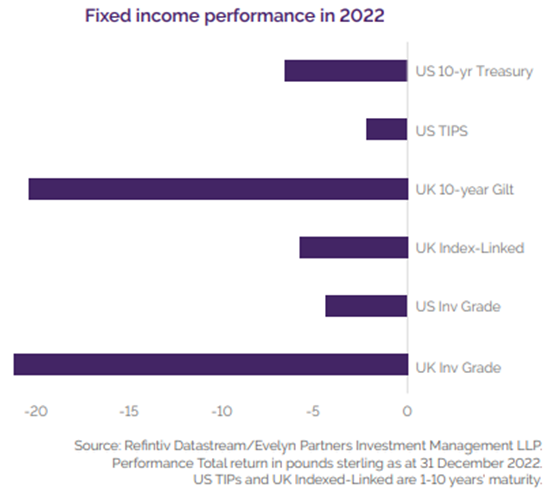

Government bonds did not offer protection during 2022 and posted one of the worst years on record. Rampant global inflation and accompanying interest rate hikes saw bond yields soar across both UK gilts and US treasuries. Longer duration assets performed poorly, with the US 10-year treasury falling 6.5% in sterling terms. The UK gilt market had a particularly turbulent year following Kwasi Kwarteng’s ‘mini-budget’. 10-year gilts were briefly down 24.4% and ended the year down 20.1%, their worst performance since 1974. Corporate bonds faced similarly poor performance, with US and UK investment grade bonds falling 4.3% and 20.9%, respectively in sterling terms. Both treasury inflation protected securities (TIPS) and inflation linked gilts failed to offer protection in the face of rising inflation, with rapid interest rate rises causing real interest yields to rise. US TIPS performed only slightly better down 3.0% in sterling terms, whilst UK index-linked fell 5.2%. The weak pound helped shield sterling investors from some of the negative returns in dollar denominated assets.

Currencies and commodities

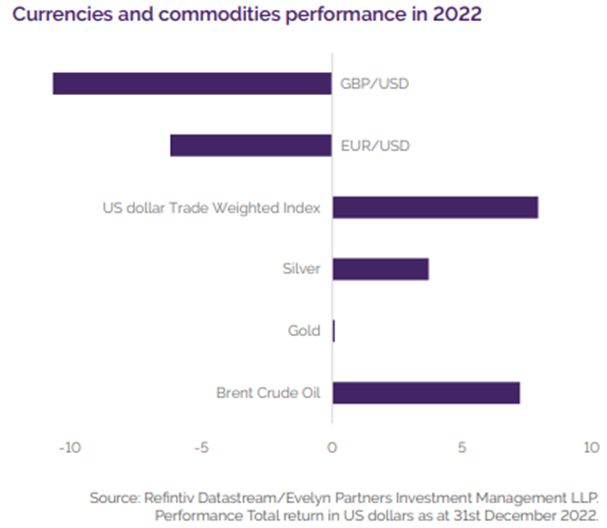

2022 was a volatile year for both currencies and commodities. Crude oil was up 37.4% by the end of first quarter, as Covid fears faded and western sanctions on Russia were imposed. However, Brent crude finished 2022 up 7.2% in US dollar terms as demand wilted under the threat of a global economic slowdown, despite OPEC+ announcing cuts to output. Gold remained largely flat in US dollar terms. Its initial strength, due to geopolitical uncertainty, was dampened by aggressive US Federal Reserve interest rate hikes. This resulted in the US dollar Trade-Weighted Index increasing 7.9% to a 20-year high as investors flocked to the greenback as a ‘safe-haven’ currency in the face of economic uncertainty. The euro found parity with the US dollar during 2022, before recovering slightly as the dollar’s strength eased. Sterling fell from $1.35 to $1.21 but found an all-time low of $1.037 following Kwasi Kwarteng’s ‘mini budget’.

Market commentary

Equities were down across the board to close out the last month of 2022 with MSCI All-Country World down 4.9% in sterling terms. December’s Federal Reserve meeting pointed to interest rates remaining higher for longer than the market had previously expected which weighed on the outlook. MSCI USA was the worst performer of the month, down 6.8%. Asia Pacific was the best performer. News of lockdown restrictions easing in China and a weakening US dollar were both positive catalysts for the region. Interest rate expectations moving up similarly weighed on fixed income with gilts down 4.4% and treasuries down 1.7% on the month, in sterling terms. Gold was up 3.5% for December and over the year fell by 0.6%, despite periods of rising interest rates traditionally favouring income producing assets. The US dollar continued to weaken through December with sterling and euro up 1% and 3.7% respectively.

Please continue to check our Blog content for advice, planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see todays Daily Investment Bulletin from Brooks Macdonald:

What has happened

Some of the early 2023 optimism faded yesterday as Fed officials pushed back against dovish bond market expectations and US data continued to point to strong demand. The US equity index moved back into negative year-to-date territory, underperforming European equities which were slightly down on the day.

US politics

The impasse within the US House of Representatives continued for a third day yesterday with Kevin McCarthy still unable to reach a majority of votes. There have now been 11 failed ballots, the first time this has happened since 1860. McCarthy has offered holdouts one of their demands, namely that any single member of the House can now call a motion to oust the Speaker. While this may improve McCarthy’s chances of reaching a majority, this could create legislative gridlock down the road when it comes to contentious legislation.

Jobs data

US jobs data continues to be a driving force behind the weaker US market sentiment, with the ADP report of private payrolls showing a stronger-than-expected gain in December whilst November’s number was also revised upwards. Initial jobless claims also hit a 3-month low in the last week of 2022, suggesting that the employment market remains robust. All of this, and the JOLTS report earlier this week, leads us into today’s US non-farm payroll report of US employment. The market expects the number of new jobs in December to have fallen from 263,000 in November to 200,000. This would leave the unemployment rate steady at 3.7%. Perhaps the more interesting measure will be the average hourly earnings figure which is expected to rise by 0.4%, less than November’s 0.6% but still a high number. For context, November’s 0.6% gain was the highest in 10 months. On a year-on-year basis average hourly earnings in the US are expected to have risen by 5%.

What does Brooks Macdonald think

With the jobs data continuing to point to a strong US labour market, Fed speakers have been eager to stress the bank’s focus on tighter monetary policy. President George said yesterday that the Fed should keep US interest rates above 5% into 2024 and President Bostic reiterated that inflation levels remained ‘way too high’. A slowdown in US economic activity during 2023 is the base case amongst economists however with the labour market remaining robust, there is a risk that the Fed overtightens in the short-term, possibly exacerbating the US downturn when it comes.

Please continue to check our Blog content for advice, planning issues and the latest investment, markets and economic updates from leading investment houses.