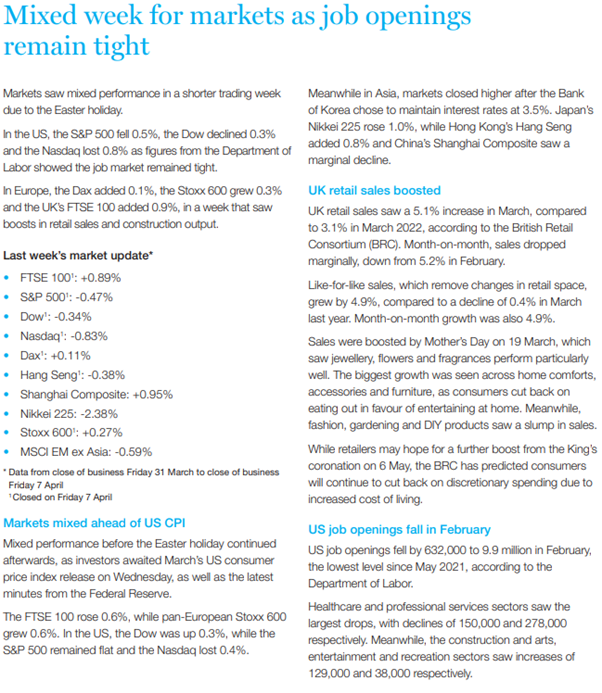

Please see the below article from Tatton Investment Management, providing a brief analysis of the key stories from global markets and economies over the past week. Received this morning – 17/04/2023

The return of calm bodes well for Spring

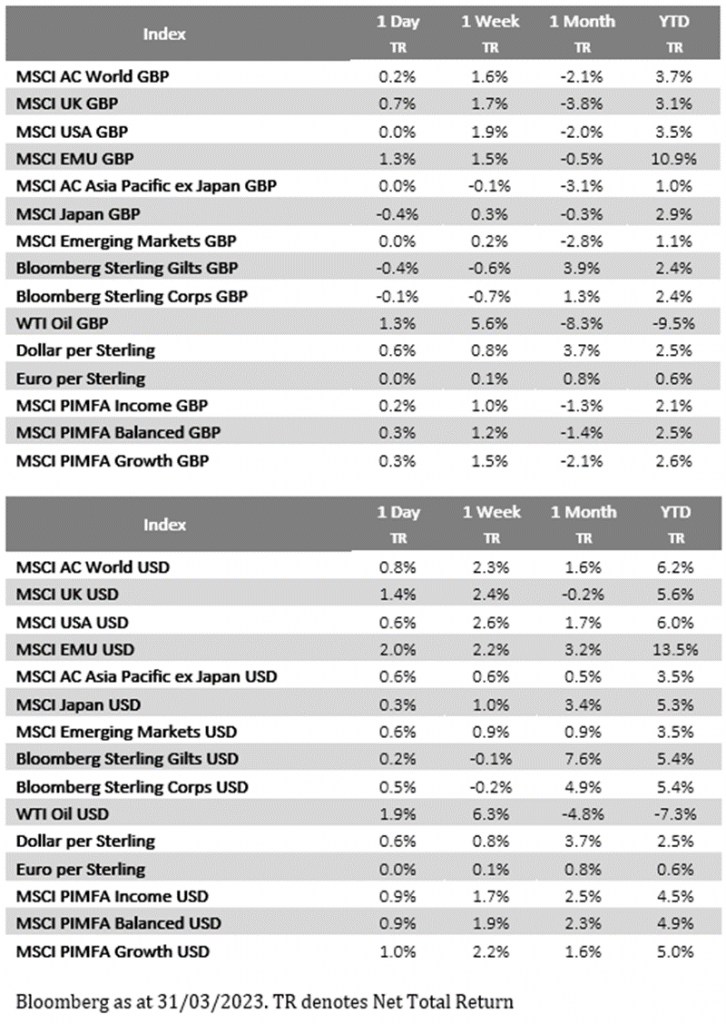

Considering how unnerving the first three months of the year were, UK investors in globally-diversified multi-asset portfolios (akin to the ones we manage) have not fared too badly. Mildly positive returns across the risk spectrum tell the story of another storm having passed without sinking global capital markets. Of course, predicting a less turbulent lead-in to summer may be foolish. While most global regions appear to be on a gentle economic upswing (and China’s upswing looks increasingly robust) US weekly employment data has been weakening noticeably and, by our measure, is close to becoming a signal of recession. Meanwhile, UK employment has also weakened. Across the Western world, small companies continue to be stressed by high short-term lending costs, if they can even get loans. Some have no longer access to loans at all. In the US, the profitless tech companies are still finding access to equity cash difficult to come by.

This suggests that until central banks are comfortable headline inflation no longer poses a threat, destabilising bankruptcies remain a strong possibility. Last week, we had mixed messages from central bankers, with either warnings about rate rises or statements about “wait-and-see”. We are still yet to hear anyone proposing that cuts should be made. The all-too-predictable danger is that rate cuts are only discussed after economies have started falling. But to give central bankers their due, they have yet to induce recession despite the talk for the past year. The renewed calm in markets is a positive for the prospects of a soft landing. But the outlook feels delicately balanced. Yes, we have lower volatility and progress to towards smaller ‘waves’ in markets and the economy. At the same time, the inflation genie is slowly being squeezed back into the proverbial bottle. This all bodes well – for now.

Mixed risk signals abound

The US dollar has been notably weaker this year. Of course, as the world’s reserve currency, dollar moves are affected by much more than economic fundamentals. Dollar assets, like US Treasury bills, are regarded as safe havens by investors. As such, the dollar tends to strengthen when markets fear weak global growth – one of the defining narratives of last year. By the same token, the dollar tends to weaken when markets are hopeful for the global economy, as other riskier assets become more attractive relative to those US safe havens. Economists therefore sometimes interpret dollar weakness as a sign of risk appetite.

A risk-on move makes some sense in the current environment. Now that economic weakness is clearly coming through, investors are increasingly looking ahead to the next growth cycle. Indeed, US Federal Reserve officials have even started hinting that interest rates might loosen in the near future. The problem is that this rationale does not fit with the wider market moves experienced. The US stock market has traded basically flat over the last two weeks, and shown little sign of a sustained up-turn.

Moreover, gold – the historical safe-haven asset – has rallied strongly over the last month. And to make matters more confusing, so too have the – decidedly less safe – cryptocurrencies. Both Bitcoin and Ethereum have had overwhelmingly positive returns this year, the latter up 55% in dollar terms and the former climbing an eye-watering 75%. What to make of these mixed signals? Looking at the current state of capital markets and the global economy, it is impossible to say for sure, but we have some doubt that dollar weakness and crypto strength should be interpreted solely as signs of general optimism, and other factors are at play, including a dramatic pick-up in Chinese liquidity. In the meantime, the lower dollar is good news for those countries whose currencies have gained, given their input prices from global trade in dollars have fallen, thereby reducing inflation pressures and also improving their relative price competitiveness.

China’s rebound accelerates, while Beijing postpones political agenda

The Chinese government has wholeheartedly shifted to a pro-growth policy set-up this year, abandoning its zero-Covid policy and loosening commercial lending restrictions. As a result, things are undeniably looking better in the world’s second-largest economy. We knew Beijing would provide plenty of fuel for growth, in the form of liquidity injections and easier lending conditions, and signs are clear that this is now having a strong impact. The most recent business sentiment indicators published at the end of March showed a remarkable pick-up coming in the services sector, with the non-manufacturing purchasing managers’ index (PMI) at 58.2 last month, the highest recorded figure since early 2011. China’s manufacturing sector is a little less buoyant, with March’s figure at 51.9, down from 52.6 in February. This suggests an uneven recovery, propelled by consumer spending over industrial activity.

Financial conditions have also eased markedly over the last couple of months, with big increases in overall money supply and the much-watched total social financing numbers. With little inflationary pressure, a desire for domestic growth and muted external support, the People’s Bank of China cut its reserve requirement ratio by another 25 basis points to 10.75% in March. This should encourage banks to lend more, and comes on top of vast liquidity support handed out to struggling property developers last year. Officials are clearly not complacent in supporting growth, as evidenced by the Finance Vice Minister’s plea for more fiscal support and tax cuts for small companies.

While policy conditions are extremely pro-growth, the Chinese government is fully aware that the recovery is fragile. This is likely one of the reasons behind Beijing’s recent détente with western leaders. French President Macron and European Commission President Ursula von der Leyen held a joint summit with President Xi Jinping last week, amid China’s increased military activity in the Strait of Taiwan. Despite the harsh rhetoric between Chinese, US and European officials over recent weeks, Beijing is clearly showing a desire to engage rather than pull out of difficult talks.

One of the most important things to understand about Chinese politics is that issues of national sovereignty – including Taiwan, Hong Kong and Xinjiang – are treated as non-negotiable by the Communist Party, and are therefore ringfenced from economic considerations. What this means is that even if Beijing engages in sabre-rattling around Taiwan, we should still expect conciliatory tones in other areas, in large part because the Chinese economy still needs all the support it can get. And while western consumers struggle, the last thing China will want to do is erect further barriers to trade. Growth is set on an expansion path in China, both now and for the near future. President Xi will not want to crush the green shoots of a recovery. We should therefore expect pragmatism going forward.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Alex Kitteringham

17th April 2023