Please see the below article from Tatton Investment Management providing a brief analysis of the key factors affecting global markets. Received this morning – 25/09/2023.

Overview: to yield or not to yield?

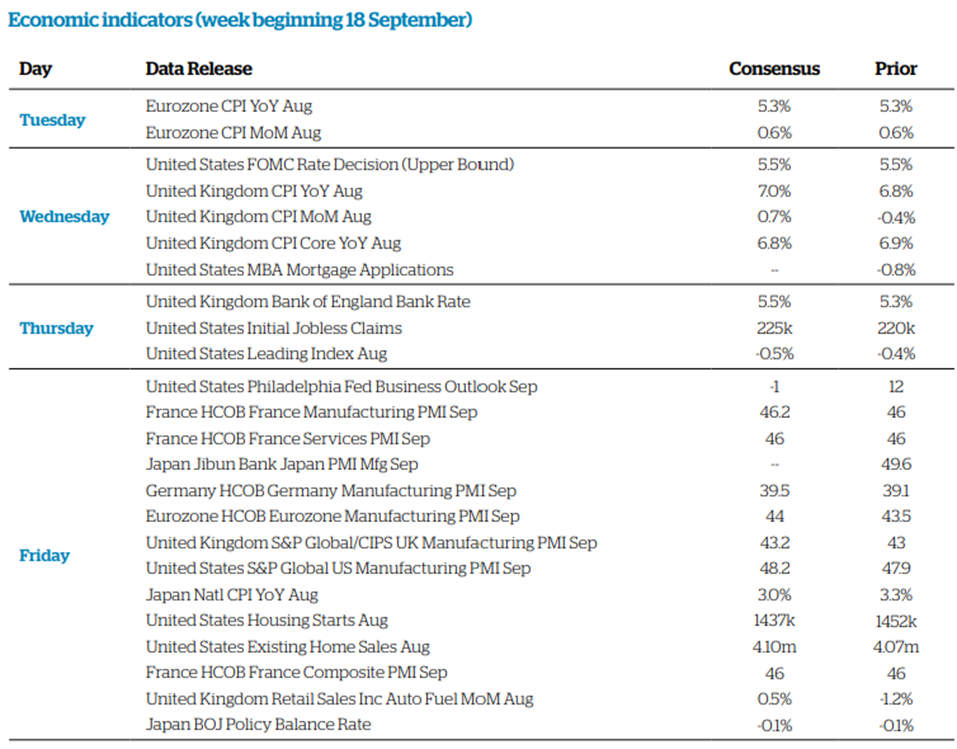

Last week, stocks and bonds ended up bruised following the ‘hawkish pause’. The US Federal Reserve (Fed) announced on Wednesday it would hold interest rates steady at 5.25-5.5%, but threw in some stern forward guidance to dispel doubts it might be easing off. Fed Chair Jay Powell’s talking points were much the same as they have been for the better part of two years: the US economy is still strong, inflation is too high, and consistently tighter monetary policy will be needed for the foreseeable future. The Fed backed up its words with a ‘dots plot’ projection that showed another rate rise this year, then holding steady in 2024. It was a reaffirmation of Powell’s commitment to keeping rates higher for longer.

Bond yields spiked on the back of the news. Ten-year US Treasury yields touched above 4.5% during early Friday trading – the highest level in 16 years. The move up in risk-free rates naturally makes equities look less attractive by comparison, sparking a sharp drop off in the S&P 500. There are concerns that equity valuations in terms of price-to-earnings multiples look vulnerable, especially after such strong stock performance without earnings growth for most of this year. Longer-term growth assets – typically more sensitive to interest rate moves – are therefore under threat again. With sluggish global growth all limiting the upside of company earnings and a ‘higher for longer’ monetary policy, investors are starting to wonder whether fixed income assets like bonds, with their now attractive yields, are better value than stocks. This ‘negative carry’ is a headwind to equities in the short term and re-establishes bonds as a value adding portfolio diversifier, however, long term investors know that only risk assets have historically been able to outperform inflation meaningfully.

Are oil price rises an inflation comeback or just a blip?

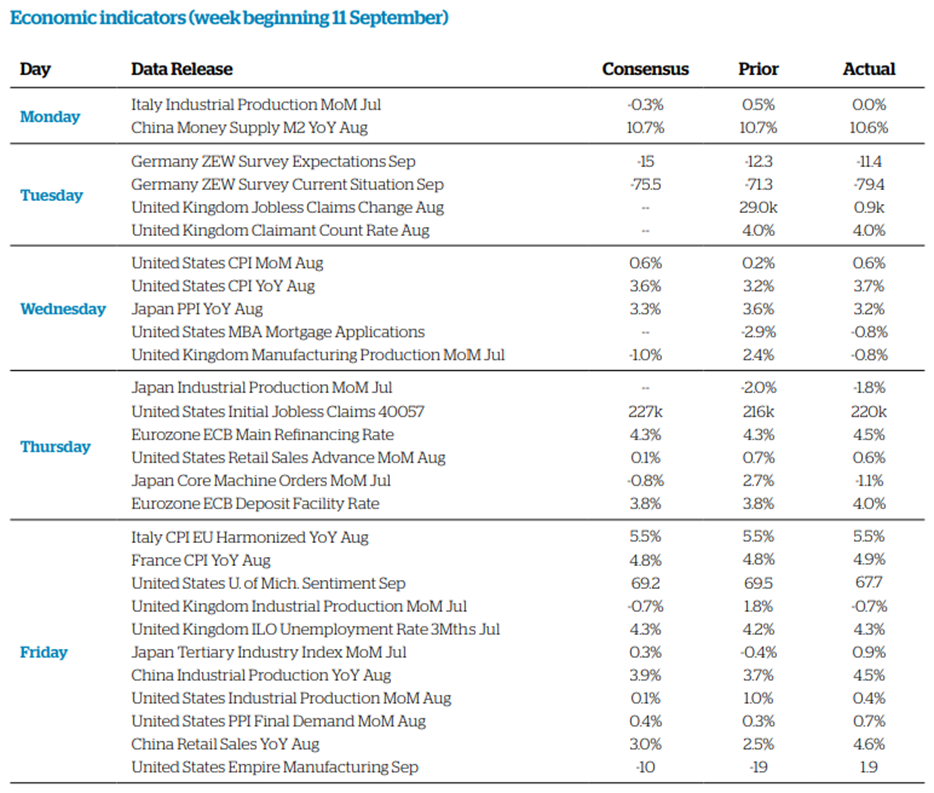

International oil benchmark Brent hit $94 per barrel (pb) during trading last Tuesday, the highest level since October last year, when markets and the world economy were still reeling from the Russian war. Higher oil prices can be tough at the best of times but are a major headache for central bankers fighting stubbornly high inflation – referenced by Christine Lagarde when the European Central Bank (ECB) raised interest rates recently. But higher oil prices are difficult for markets as well as policymakers, lifting headline inflation at a time when it is still uncomfortably high and acting as a tax on consumers and businesses unable to pass on costs. Morgan Stanley estimates the inflationary effect of a $20pb increase like the one seen since June would be a 0.5% addition to eurozone inflation. Not an astounding figure after the year we have had, but still an uncomfortable contribution.

With labour markets tight and inflation expectations (up to recently) high, consumers and businesses are now quick to react to higher price signals. Fuel prices are the most visible of these signals. Tight capacity – not just in oil and commodity markets but throughout the economy – means second-round inflation effects are now much more likely. As central bankers are keenly aware, the inflation genie is only just now getting back into the bottle, and hence higher oil prices are keenly noticed. On the other hand, should higher oil prices dampen consumer spending, this could lessen the Fed’s impetus to raise rates or keep them high. The Fed’s own research suggests an oil price increase of 10% takes 16 basis points (0.16%) off consumption and 14 from GDP. Compressing consumption and economic activity is the goal of rate rises, so in that sense higher oil prices may be doing the Fed’s job for it.

Again though, we should be cautious about jumping to conclusions. Core US inflation came in at 4.3% in August, which would still be well above the Fed’s 2% target if it translated directly into future inflation. While the trend is pointing down, the Fed will not want anything to disrupt this – as higher fuel prices surely could. The key point to watch is whether higher oil prices have a bigger effect on consumption and activity, or as a price signal for consumers. Markets nervously await the answer.

Trojan Horse tech

The artificial intelligence (AI) theme is hard to get a handle on from an investment perspective. Are these new technologies a revolution waiting to happen, or a bubble waiting to burst? We are not at dotcom levels of hype (yet), but ‘machine learning’ and ‘language models’ have reached corporate buzzword status. From a business perspective, the obvious benefits come from productivity growth. This has been one of the hardest things to find for more than a decade, low productivity being one of the key reasons behind the period of low growth following 2008’s Global Financial Crisis. Even in big tech, which has long been home to eye-watering stock valuations, there was a feeling some time ago that genuine innovation was lacking – particularly in stagnating markets like smartphones. The AI excitement changed all of that, even if productivity improvements take time to filter through.

Companies have been working on AI for decades and its potential was never exactly a secret, quite the opposite in fact, given that most of the building blocks are open source. Yet it took the release of ChatGPT with its generative language model to really kickstart the financial push in AI’s direction. What changed then was not the technology itself, but the perception of what it could do and how close we might be to world-altering changes.

Of course, entering a new market to fund a longer-term objective of changing the market altogether is a ‘Trojan Horse’-style strategy, and the fact that AI technologies will almost certainly create lots of new revenue streams in the future does not mean all the market valuations, especially on a stock level, are justified. To be sure, the words ‘generative AI’ are certainly good for certain share prices, but overall market appetite is fairly contained, historically speaking. This has surely something to do with the wider financial backdrop too. Interest rates have risen at the fastest pace in a generation, while global growth and near-term demand prospects look weak. In a way, perhaps this forces markets to make a longer-term evaluation.

The question, as ever, is how businesses will turn the current technologies into future earnings. And of course, knowing which companies might do so best would be nice too. Time will tell who the winners will be, and especially whether incumbents will reap the benefits, or whether newcomers can shake up the equity market. For now, though, having a ‘beacon of hope’ for what may generate real growth over the next decade is to be welcomed by investors.

Please check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Alex Clare

25/09/2023