Please see below, Brooks Macdonald’s Daily Investment Bulletin received this morning – 09/11/2023.

What has happened

US equities managed to deliver a small gain yesterday, marking the 8th consecutive day of gains, as the bond rally continued. Further falls in the oil price also helped support the view that inflation would come down quickly, with Brent Crude closing below $80 per barrel for the first time since July. In terms of the bond rally, the US 10-year Treasury yield fell below 4.5% after the bond market absorbed a fresh $40bn 10-year Treasury auction, raising hopes that the current level of supply would not destabilise the rally.

Bond market rally

The recent fall in bond yields is already following through to US mortgage pricing with the average 30-year mortgage rate down 0.25% over the last week alone. The overall rate remains above 7.5% however so we are by no means back to ‘cheap’ borrowing even if the path of travel is to be welcomed. Mortgage applications rose as a result but remain subdued versus recent history. Fed Chair Powell will today speak at a panel at the IMF conference so he may shine some additional light on current Fed thinking post the last week’s moves. Over in Europe, sovereign bonds also rallied despite prominent ECB bankers stressing that it was ‘far too early’ to be talking about cutting Euro Area interest rates.

Inflation

The fall in energy prices yesterday helped lower market expectations for inflation with medium term Euro Area inflation expectations falling to one of their lowest levels in six months. The energy moves were not limited to just the oil price with European natural gas prices falling. Reflecting concerns about the resilience of global demand, the highly economically sensitive copper price also fell yesterday.

What does Brooks Macdonald think

While the market has been quick to price in an improving inflation backdrop within Europe, consumer surveys still point to higher expectations. The ECB’s Consumer Expectations Survey is published with a significant lag, so reflects thinking in September but at that point, 1 year inflation expectations increased by 0.5% month-on-month to 4%. Falling energy prices should start to filter through to expectations over the coming months however the ECB will need to see a shift in consumer mindset in order to entertain any thoughts of a rate cut in 2024.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below article received from Brewin Dolphin yesterday afternoon, which provides a positive global market update.

Global equities rallied last week on expectations that interest rates may have finally reached their peak.

The S&P 500 rose 4.6%, its strongest weekly gain in almost a year, after the Federal Reserve indicated that the recent increase in long-term Treasury yields could mean that a further rate hike is not required. The Dow added 3.4% and the Nasdaq surged 5.4%.

In Europe, the Stoxx 600 and Germany’s Dax both added around three percentage points after eurozone inflation fell to its lowest level since July 2021. The FTSE 100 gained 1.2% as the Bank of England voted to keep interest rates unchanged.

The positive sentiment carried over to Asia, where Japan’s Nikkei 225 advanced 4.1% and China’s Shanghai Composite rose 0.3% despite concerns about China’s economy.

Eurozone business activity contracts further

European stock markets slipped into the red on Monday (6 November) as investors took profits after five-consecutive days of gains and data painted a gloomy picture of the eurozone economy. The latest HCOB eurozone purchasing managers’ index (PMI) showed the rate of decrease in business activity accelerated in October. The index fell to a 35-month low of 46.5 in October, down from 47.2 in September. New orders for goods and services fell at the quickest pace since May 2020. Over in Asia, South Korea’s Kospi surged 5.7% on Monday after the country re-imposed a ban on short selling.

UK and European indices were flat at the start of trading on Tuesday as investors analysed weaker-than-expected economic data from Germany and China. German industrial production slumped 1.4% in September, driven by a 5% decline in automotive industry production. Chinese exports dropped 6.4% year-on-year in October, much worse than the 3.5% decline expected by analysts. Imports unexpectedly rose by 3.0% over the same period.

Fed delivers dovish policy statement

Last week saw the US Federal Reserve vote to leave interest rates unchanged, as widely expected. The November meeting did not contain any new economic projections, which meant that all eyes were on the postmeeting press conference.

During the conference, Federal Reserve chair Jerome Powell noted that the recent surge in long-term US bond yields and mortgage rates had done some of the Fed’s job for it. He said Fed officials will be watching the effects of higher yields as they consider whether to hike rates again. Powell also said the Fed has come far in terms of its tightening campaign and that it takes time for higher interest rates to impact the real economy.

The comments were interpreted to mean that interest rates may have reached their peak, which drove steep declines in bond yields across different maturities.

US labour market cools

The drop in bond yields was further fuelled by a weakerthan-expected nonfarm payrolls report, released on Friday. Nonfarm payrolls increased by just 150,000 in October, while job growth in August and September was revised down by 101,000. Manufacturing was a notable area of weakness, with the sector experiencing net job losses of 35,000 last month. The Bureau of Labor Statistics said this reflected a decline of 33,000 in motor vehicles and parts that was largely due to strike activity. Average hourly earnings increased by 0.2% month-on-month, the lowest reading since February 2022, and the unemployment rate ticked up to 3.9%.

Although the data suggests the economy is slowing, markets reacted positively because it added to the conviction that the Fed will abandon its plan of one more rate hike in December.

BoE holds base rate at 5.25%

Here in the UK, the Bank of England (BoE) chose to leave interest rates unchanged for the second time in a row at 5.25%. The vote was 6-3, with three of the nine Monetary Policy Committee members favouring another 25-basis point increase.

While the BoE’s hiking campaign might have come to an end, the Bank went out of its way to flag that monetary policy will remain restrictive for some time as inflation and wage growth remain elevated. BoE governor Andrew Bailey said it was “much too early to be thinking about rate cuts”, adding: “We will keep interest rates high enough for long enough to make sure we get inflation all the way back to the 2% target.”

The most recent year-on-year inflation figure was 6.7%. The BoE expects inflation to fall sharply in the coming months, remain at around 3% next year, and drop below the 2% target at the end of 2025 – later than previously forecast. It also expects the UK economy to grow by 0.1% for the rest of this year and remain flat in 2024.

Japan approves stimulus package

Over in Asia, the Japanese government approved a $113bn stimulus package that aims to boost growth and help households cope with the rising cost of living. According to Reuters, the package includes temporary cuts to income and residential taxes, payouts to lowincome households, and subsidies to curb petrol and utility bills. The government estimates that the plan will boost Japan’s gross domestic product (GDP) by around 1.2% on average over the next three years.

Last week also saw the Bank of Japan (BoJ) announce a further relaxation of its yield curve control policy. The BoJ said the 1.0% ceiling for ten-year Japanese government bond yields will now be regarded as a reference rather than a strict cap on rates.

Please check in again with us soon for further relevant content and news.

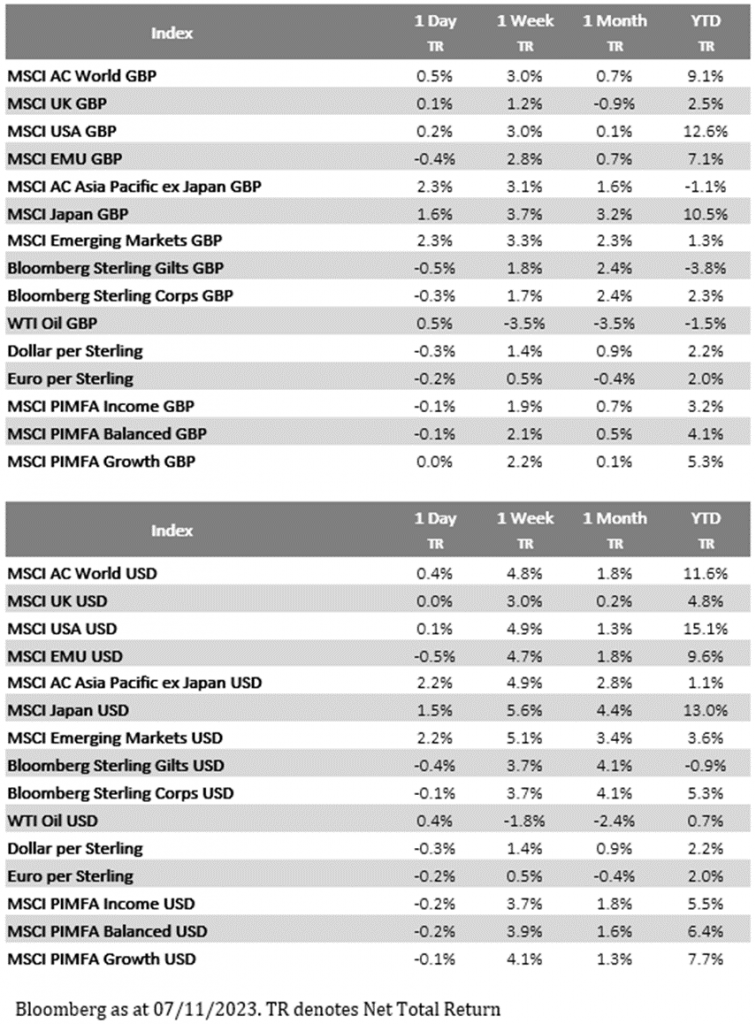

Please see below, Brooks Macdonald’s Daily Investment Bulletin which outlines the key factors currently affecting global markets. Received this morning – 07/11/2023

What has happened?

There was a bit of pushback against last week’s hopes of peak US interest rates and imminent cuts yesterday. The bond pressure was particularly acute in shorter dated bonds with the 2-year US Treasury yield rising by almost 10bps. Despite these moves, the US equity market managed to stay in positive territory for the day however below the surface, the US small cap index suffered under the weight of rising yields.

Central banks

Market expectations for a Fed interest rate hike rose slightly yesterday as did expectations of the central bank’s rate at the end of 2024. One of the drivers behind this was commentary from the Minneapolis Fed’s Kashkari who is one of the more hawkish members of the central bank. Kashkari said that ‘we need to let the data keep coming to us to see if we really have got the inflation genie back in the bottle’. A warning against declaring victory too early. On that note, the Reserve Bank of Australia lifted its cash rate yesterday in response to a slower-than-expected decline in inflation.

Lending conditions

The Senior Loan Officer Opinion Survey (SLOOS) from the Federal Reserve also captured the market’s attention. The survey is an important barometer of lending standards and therefore by extension the difficulty, or ease, of obtaining credit in the US economy. The survey showed some improvement in US banks’ willingness to lend however mortgage availability remained poor with the lending standards actually tightening for that component. While there was some improvement within the survey, the tight standards are still at levels previously associated with a recession.

What does Brooks Macdonald think?

The improved SLOOS data yesterday helps support an improving economic narrative however the standards, in aggregate, act as a break on the US economy. Should this tightness continue, it raises the risk of a hard economic landing. Until these lending standards ease, companies that have significant walls of upcoming bond or loan maturities, and therefore need to refinance, will find themselves at a material disadvantage to those who have secured longer term financing.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see the below Tatton Investment Management Monday Digest article received this morning – 06/11/2023.

Overview: Central bank dovishness proves contagious

Last week, we noted how negative sentiment in stock markets can become a self-perpetuating destructive force for an entire economy as the investing public feels the heat of feeling poorer (at least on paper). But seven days later, we look back at an impressive stock market recovery that proved far more substantial and persistent than anyone would have dared to suggest possible. So, what has fundamentally changed? Well, not the economic data, where there has been no significant changes from the previous ‘not as bad as expected’ string of releases. What did change though was that – contrary to expectation – the US Federal Reserve (Fed) seemed to adopt a similarly somewhat dovish tone to the European Central Bank (ECB) of the previous week.

Few were expecting any interest rate move from the Federal Open Markets Committee (FOMC) this month, but a majority of commentators thought another 0.25% move in December likely given next month’s meeting has more research inputs. But after Wednesday’s meeting, Fed Chair Jerome Powell gave the strong impression the FOMC is becoming convinced their work is done; that the employment market is becoming less heated, wage growth is calming, and inflation is set to come back towards target. It felt like the opposite of the Fed’s September message and the market reacted accordingly.

In comparison, the Bank of England (BoE) is still in more of a bind. Its Thursday meeting concluded with the same ‘no rate rise’ decision as their US and European counterparts, while the BoE’s statement acknowledged the stress in the UK economy, with interest rates hurting many. Nearer-term measures of inflation in the UK also are helpful at the margin but the BoE’s biggest worry remains and differs in that measures of wage inflation are still uncomfortably high.

Indeed, overall the mix of monetary and fiscal policy globally has already begun to shift to accommodation. The fiscal supports from China announced last week, and Japan this week, are substantial and added to investor perceptions that the investment environment may be about to become friendlier. Of course, much depends on the US. We’ve repeatedly seen that bouts of equity market positivity have supported households and businesses with already strong savings balances. The tight US financial conditions leading up to the FOMC meeting have been loosened in only two days. Following relatively weak US employment figures today, FOMC members have to believe the easing in the US labour market is more than seasonal if they are to hold on to their new-found dovishness.

What last week’s market moves also suggest is that institutional investors have been short of risk assets, both in equity and bond markets, while private households have been diverting money into their savings rather than investment accounts. This type of rebalancing flow may be ‘short-term’ but it can still go on for some time. Nevertheless, this past week’s market action informs us that the ‘higher for longer’ rates perception that only just sunk in over October may have already reached its expiry date given central bankers’ unexpected dovish tones.

Does Emerging Markets growth always mean returns?

Why would you invest in Emerging Markets (EM)? In a word, growth. As the name suggests, developing economies generally have high potential to develop, and foreign investors are keen to get in on the action. It does not always work out, of course, but that is just part of the game: high risk comes with high reward. We have written a lot about emerging markets in recent months, from the obvious China – whose ‘emerging’ status perhaps stretches the definition somewhat – to India, Brazil and Argentina. The risk-reward profile of EM investment means that for every India or Brazil success story, there are plenty of Argentina-style cautionary tales.

This simple mantra goes some way to explaining why EM assets are generally considered risk-on, doing well when global investors (primarily concentrated in wealthy developed nations) feel confident and vice versa. But in reality, things are a little more complicated. EM assets – certainly those in the benchmark MSCI EM index – have arguably been more affected by weakness in China (whose assets make up around 30% of the index’s total market capitalisation) than monetary tightening in the US and Europe this year. On the other hand, as we noted in recent months, Brazil and India have fared surprisingly well, despite weak global growth and tight financial conditions.

One obvious yet often overlooked complication for EM investors is that there is a world of difference between EM growth and returns on EM assets. China is the clearest example of this. Chinese gross domestic product (GDP) expanded from just over $11 trillion in 2015 to nearly $18 trillion in 2022 – meaning 62.4% growth, according to the World Bank. In that time its benchmark CSI 300 stock index grew just 10%, with plenty of volatility along the way. In contrast, the US economy grew just under 40% in the same period, but delivered 86% equity growth. Chinese stocks have sunk 8% this year, while US companies have added 10% to their share values. This reflects the fact that Chinese companies have faced huge problems – prompting an exodus of western capital. And yet, despite undeniable growth disappointment in the world’s second largest economy, the absolute level of growth has held up okay – certainly compared to the dire performance of Chinese equities.

When making the case for EM investment – either in a specific region or in EMs more generally – economists and analysts often point to growth-supportive factors, like weakness in the US dollar or supportive trade conditions. But those factors do not always weigh in favour of EM assets themselves. Indeed, they can often suggest foreign companies with EM exposure. Other asset classes – like corporate or government bonds – can often provide more exposure to EM growth. Growth, on its own, is rarely enough.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below article received from EPIC Investment Partners this morning, which coversthe Bank of England’s stance on keeping the base rate at 5.25%.

As expected, the Bank of England followed the Fed, voting 6-3 in favour of keeping the base rate at 5.25%, with a warning that monetary policy will likely need to stay tight for an “extended period of time”. Andrew Bailey, the Governor of the central bank, warned that whilst progress had been made in the fight against inflation, it was still too high and there was “absolutely no room for complacency”.

“We will keep interest rates high enough for long enough to make sure we get inflation all the way back to the 2% target. We will be watching closely to see if further increases in interest rates are needed, but even if they are not needed, it is much too early to be thinking about rate cuts,” Bailey said, adding that the committee would rely on future data to balance the risks “between doing too little and doing too much”.

In its latest Monetary Policy Report released with the decision, the committee acknowledged that inflation has fallen below the earlier projections made in August. The bank’s revised outlook now sees the consumer price index (CPI) at around 4.75% in Q4 of 2023, followed by a fall to about 4.5% in Q1 of the next year and a further drop down to 3.75% in Q2.

As for the UK’s GDP, it is now expected to have stagnated in Q3 2023, which is a weaker performance compared to the MPC’s August forecasts. The GDP is now projected to exhibit only 0.1% growth in the fourth quarter, also falling short of the previous expectations from August.

This was the first MPC that former US Federal Reserve Chair Ben Bernanke attended, as part of his review into the Old Lady’s forecasts and communications. The BoE appointed Bernanke in July to examine the forecast process after heavy criticism from politicians and some economists for underestimating the threat inflation posed. His review is focused on the lessons to be learned for future forecasts “during times of significant uncertainty.” It will not pass judgment on past policy decisions.

Today sees the penultimate Nonfarm Payrolls numbers for 2023. The market is going for +180k lower than October’s bumper +336k with an unemployment rate of 3.8%, hourly earnings of 0.3% and a participation rate of 62.8%.

Lastly, how the mighty have fallen. “Crypto King” Sam Bankman-Fried had gone from being (a supposedly) multi-billionaire to a broke, convicted fraudster who faces decades behind bars. The 31-year-old former CEO of FTX was found guilty by a jury on all seven charges of fraud and conspiracy against him. The sentencing for these charges, which carry up to 115 years in prison, is scheduled for March 2024.

A jury took just over four hours yesterday, including dinner, to conclude that Bankman-Fried stole USD 8 billion in customer funds from his crypto exchange FTX to fund risky investments, political contributions, and luxury real estate.

Please check in again with us shortly for further relevant content and news.

Please see the below article from EPIC Investment Partners providing their commentary on the FOMC Hold Rates/The Old Lady’s Table Mountain. Received this morning 02/11/2023.

The FOMC held interest rates at the 22-year high for the second straight meeting, albeit with Fed Chair Powell keeping the door slightly ajar to the possibility of additional tightening. Overall, there were very few changes to the accompanying statement to that given in September. All in all, Powell continued to acknowledge the downshift in inflation, whilst warning it was not “yet definitive enough”, adding that while the labour market is “rebalancing” it remains tight. He also reiterated the strength in GDP growth, but also acknowledged that “many forecasters are forecasting it will be slow”.

In the Q&A after the release, Powell reiterated that the Fed remains on guard against inflation threats. However, he didn’t specifically suggest that a resumption of hiking is imminent. In response to a question about whether financial conditions are sufficiently restrictive to get inflation to 2%, Powell said: “We haven’t made any decisions about future meetings. We have not made a determination and we are not confident at this time we have reached such a stance. We are not confident that we haven’t or we have. That is the way we are going to be going into these future meetings, is to be, you know, determining the extent of additional further policy tightening that may be appropriate to return inflation to 2%.”

With regards to the tight labour market and wages, Powell noted: “What we have seen is a very positive rebalancing of supply and demand, partly through just much more supply coming online”. “If you look at the broad range of wages, wage increases have really come down significantly over the course of the last 18 months, to a level where they are substantially closer to that level that would be consistent with 2% inflation over time. We can proceed carefully at this time”, Powell added.

Eyes now turn to the Old Lady at midday as she looks set to hold rates on the “Table Mountain” strategy as evidence continues to mount that the economy, labour market and inflation are weakening. At the time of writing, money markets are pricing a less than 5% chance of the BoE hiking rates.

The Table Mountain term comes from BoE Chief Economist Huw Pill, speaking in Cape Town recently, where he stated he supports the idea of a lower peak for interest rates and holding them there for longer to contain inflation, hence the Table Mountain approach.

Please check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Please see below Brooks Macdonald’s Weekly Market Commentary received yesterday afternoon 30/10/2023

• US equity market enters correction territory after falling more than 10% from its July peak

• Eurozone CPI and GDP will be in focus this week ahead of Friday’s US employment report

• Central banks from Japan, the US and UK will all issue their latest guidance this week.

US equity market enters correction territory after falling more than 10% from its July peak

After the US equity index moved c. 0.5% lower on Friday, the index has officially entered correction territory, being now more than 10% lower than its end of July peak level. Of those losses, around half of them have taken place in the last fortnight alone. Friday’s losses occurred despite strong results from Amazon and Intel which were released after the market close on Thursday.

Eurozone CPI and GDP will be in focus this week ahead of Friday’s US employment report

Starting with Europe, this week sees the release of the preliminary CPI releases as well as the Q3 GDP numbers. In terms of GDP, economists expect for there to have been no growth across the Eurozone in Q3 with the year-on-year growth rate at just 0.15%. Both headline and core Eurozone CPI readings are expected to cool with the headline rate expected to lurch lower from 4.3% year-on-year to 3%. The main US datapoint this week will be the US employment report on Friday where consensus expects 189k jobs to have been created after a blockbuster September that saw 336k new jobs. Before we get to Friday we will see the ECI, JOLTS, ADP and initial jobless claims data which will all give their own insights into the labour market. Lastly, earnings season continues apace this week with Apple releasing on Thursday likely to be the highlight.

Central banks from Japan, the US and UK will all issue their latest guidance this week

This week sees the Bank of Japan, Federal Reserve and Bank of England issue their latest monetary policy guidance. The Bank of Japan concludes its meeting tomorrow with investors split on whether the central bank will abandon the yield curve control which effectively caps yields on government bonds through quantitative easing. The BoJ is likely to revise up its near-term inflation forecasts which will put the bank under pressure. Then on Wednesday we hear from the Federal Reserve which is expected to stay on hold, but investors will be looking for guidance on December’s meetings. A strong US economy makes the argument for a December interest rate hike but equally the recent run-up in Treasury yields is doing some of the Fed’s work for it already. Our last central bank this week will be the Bank of England on Thursday. The Bank of England is not expected to raise interest rates or change its guidance however there is likely to be some dissent amongst voting members. Several members are concerned by the still strong pace of wages, favouring additional hikes, though these individuals are likely to be outnumbered by those cautious around the strength of the UK economy.

Please check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses. Charlotte Clarke 31/10/2023

Please see below, the ‘Monday Digest’ from Tatton Investment Management providing a brief analysis of markets and the key news from global economies over the past week. Received this morning – 30/10/2023

The resilience narrative comes under pressure

In recent times, a fall in bond yields (and therefore a rise in bond prices) would go alongside rises in equity prices, particularly the mega-cap growth consumer-related techs like Amazon, Alphabet (Google), Microsoft and Apple. However, last Thursday, US Treasury long maturity bond yields started to retreat from highs but US stocks carried on lower. In the credit markets, despite the higher government bond prices, corporate bonds were flat to weaker, especially among the more indebted companies. If this new dynamic continues, it may signal a change in investor expectations about the resilience of US sales and earnings growth.

In particular, concerns are building that the US consumer is running out of steam. The third quarter corporate results at Alphabet, Amazon and Meta were seen as good as they will be for the foreseeable future. Investors are worried the digital ad market is slowing. Meta disappointed (shares dropped more than 4%) after its executives warned of softer advertising spending, Alphabet slumped 9.5% last Wednesday, and despite a healthy quarter, Amazon stock was still down on the week and -17.5% below its 13 September high for the year.

To us, this seems to indicate waning investor confidence in US consumption. As a consequence, the stock market leadership of just a handful of darlings is waning. This is not necessarily a bad thing, but the risk is that it leads to a more significant correction beyond those names. US consumers could suddenly feel a lot less well-off, slowing demand much too quickly. This would force central banks into slashing rates much earlier than anticipated. The European Central Bank (ECB) met on Thursday and left rates unchanged (more on this below). The other global rate setters of the Federal Open Markets Committee and the Bank of England (BoE) meet next week. The stalling of the oil price and other energy price rises also should allow the rate pause to continue. All ears will be on the respective statements and press conferences. We expect dovishness from the BoE given the slowing inflation environment, the easing of employment tightness and the weak house market.

The oil majors double down

October has seen two of the biggest acquisitions in the history of the oil and gas industry. Last Monday, Chevron announced it will purchase fossil fuel producer Hess for $53 billion, less than two weeks after rival ExxonMobil agreed a whopping $59.5 billion deal for Pioneer Natural Resources. The megadeals have naturally caused stirs in the industry, suggesting anyone that thinks the world will soon wean itself off fossil fuels is kidding themselves. Clearly, corporates do not commit tens of billions without a plan that can withstand shareholder scrutiny. But, megadeals are not always a sign of confidence; rather than expansion, Chevron and Exxon might be consolidating ahead of an uncertain future.

This defensive interpretation is backed up by the fact that stock valuation premiums for recent oil and gas deals have been extremely small by historical standards. Pioneer sold for 9% above its market share price, while Hess Corporation accepted a 10% premium. There is probably a combination of motivations for these megadeals – partly defensive and partly bullish. This mixture has a lot to do with the particular environment that US oil majors find themselves in, certainly compared to global rivals. In the post-pandemic world, amid intense wars in Europe and the Middle East, energy security has become one of the top political priorities for every nation.

Europe’s quest for energy independence is inescapably tilted towards renewables: it has lots of capacity for solar, wind and hydro power (and relatively smaller distances for electric grids to cover) but little capacity to mine its own fossil fuels. The US has plenty of oil and gas, and its consumers are hesitant to change, particularly if that comes with higher short-term costs. For the world, we can hope that European reasoning wins out. Or that at least fossil fuel rich countries don’t lose track of alternatives and CO2 neutralisation technology development in parallel.

Is the ECB turning dovish?

Economic ills have put pressure on the ECB to slow, stop or even reverse its aggressive monetary tightening. Like most developed world central banks, the ECB is very worried about tightness in the labour market and the potential of the dreaded wage-price-spiral leading to persistent inflation (wages, profits and prices all increasing in response to each other). Wage rises in particular have been far outpaced by inflation in the Eurozone over the last year, meaning a sharp deterioration in household spending power, along with higher borrowing costs and a general dwindling of economic prospects. Speaking after the meeting, ECB President Christine Lagarde said growth is “likely to remain weak over the remainder of the year”. Policymakers are reasonably confident that price increases are coming under control, but – as the recent shift up in commodity prices and outbreak of another Middle Eastern war have shown – they are wary that externalities could turn for the worse, providing yet another input cost shock. Lagarde specifically mentioned the Israel-Hamas war’s potential effects on energy.

Over the last few years, the ECB has also made clear its concern for inflationary profit expansion – the flipside of the wage-price spiral, often ignored in British and US discussion. That being said, Europe is clearly in a different place to the US, where growth, jobs and consumer sentiment have been incredibly resilient despite a barrage of global pressures. We wrote last week that this was largely down to Americans’ willingness to draw on excess savings built up during the pandemic (though these are arguably dwindling, perhaps supporting the Fed’s recent decision to keep rates on hold). In Europe – and the UK for that matter – wage growth is moderating and consumers are clearly not feeling too confident.

The monetary impetus for inflation in Europe has fallen away, and there is no real economic impetus to replace it. A similar dynamic is taking hold in the UK – even if the Bank of England still has its hawks and hence might yet raise rates again. The US is not seeing this yet but, as we wrote last week, this is likely to change the more that excess savings come down. This side of the Atlantic, however, central bankers have every reason to turn dovish, and the evidence from last week’s meeting is that the ECB already has.

Please continue to check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Please see below an article published by Invesco and received late yesterday (26/10/2023) afternoon, which provides a snapshot of the big headlines of Q3 2023:

Please check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.