Please see this week’s Markets in a Minute update below from Brewin Dolphin, received yesterday afternoon – 07/04/2026.

Markets steady as Iran deadline approaches

As another President Trump deadline approaches, markets remain calm despite dwindling energy reserves.

Key highlights

- Oil supply crisis deepens: An extended closure would push energy prices to levels where demand destruction begins, weighing on growth alongside demand for aluminium and other industrial metals.

- Market volatility driven by contradictory White House messaging: Claims of deals and “two week” wind-downs drives volatility as conflict continues.

- 6 April deadline forces market risk reduction: Iran’s response to a peace plan fell over Easter weekend, forcing risk reduction ahead of the break, particularly in European markets.

Markets remain distracted by a world in conflict

Gas and oil product prices have soared outside the U.S. since the conflict began

Source: Bloomberg

Markets return from the Easter break facing another key deadline in the U.S.–Iran war. President Trump’s original deadline for reopening the Strait of Hormuz passed over the weekend and was extended to today at 8pm local time (1am tomorrow in the UK) after which he’d promised to target desalination and power plants (the emphasis seems to have shifted to bridges and power plants).

The threat of further military escalation is real, and equity and bond markets have made and held small gains over the last week. Markets are dispassionate and consider only economic consequences rather than political or humanitarian ones.

Even so, it might seem surprising that markets have remained calm, despite depleting energy reserves and system redundancy tightening the market further. From an economic perspective, an escalating conflict and a deadlocked one have largely the same implications. In both scenarios, the Strait of Hormuz (the Strait) is already largely closed with only a few vessels passing through on Iranian terms.

An escalation of the conflict, therefore, wouldn’t necessarily impede transit any more than the current situation already does. What matters is whether it moves the situation closer to, or further away from, an open Strait. With or without escalation, the Strait can reopen shortly after the end of hostilities, which can occur whenever the U.S., as the dominant military power in the region, chooses.

With the original aims of the action having been quite loosely defined, a form of regime change has occurred, as has a form of disarmament, though the recovery of enriched uranium seems like a far harder hurdle to clear. If the U.S. were to cease hostilities, Iran might continue disrupting shipping briefly as a deterrent against future action, but would ultimately benefit more from allowing normal service to resume.

So, as long as the economic impact of the war doesn’t worsen and the economy keeps moving, maintaining hedges and short positions becomes increasingly costly, allowing markets to gradually stabilise. Most equity markets have recovered from their lows, indicating that technical support is kicking in, with last week’s sharp mid-week rally driven more by deeply oversold positioning than by any substantive change in the conflict’s trajectory.

The more consequential risk remains the Strait. An extended closure would push energy prices to levels where demand destruction begins, weighing on growth alongside demand for aluminium and other industrial metals. Brent crude traded above $115 per barrel last week, and investors are now attempting to price in the growth implications.

The oil supply picture remains precarious. Research suggests that beyond mid-April, once de-sanctioned Russian and Iranian floating crude and strategic reserve stocks are drawn down, the oil deficit could rise from 4.5/5 million barrels per day to approximately 9/9.5 million barrels per day.

On prediction markets, roughly 50% of participants expect more than 20 ships to transit the Strait by the end of April, with only about 40% expecting 30 or more – well below the pre-war average of approximately 100 ships per day. Even 30 ships per day, combined with activated pipelines in Saudi Arabia, the UAE, and Iraq, wouldn’t restore pre-war supply levels. This implies oil prices would need to remain significantly elevated to balance the market.

Elsewhere, the Houthis’ entry into the broader conflict last week – threatening Saudi oil infrastructure – prompted retaliatory strikes on two of the world’s largest aluminium smelters in the region. The producer stated it had sustained significant damage and it would take “considerable time” to bring capacity back online. For context, the Middle East accounts for approximately 9% of global aluminium production, and the two affected smelters produce around 3.2 million tonnes per year.

Gas prices have returned to levels last seen at their January peak, though they remain well below the 2022/23 extremes. The feed-through to consumer prices will take time but is now a clear risk to the inflation outlook.

European markets must now wait until tomorrow’s 1am deadline to see how the next phase of the conflict develops.

Market performance over the last quarter

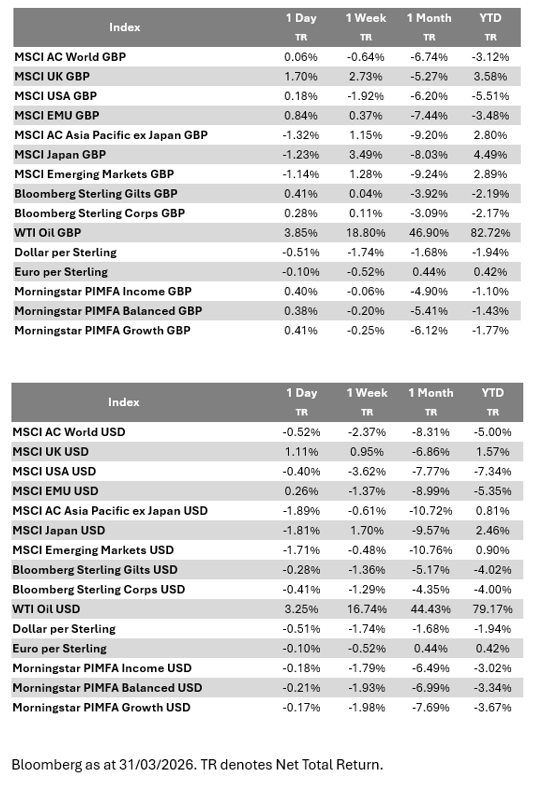

Major market performance during quarter ending 31 March 2026

Source: LSEG

- Quarterly performance (to 31 March): Emerging markets were the best-performing major region over the quarter, while the U.S. was the weakest. Currency effects were material – the S&P 500 underperformed in local currency terms over the final month but outperformed in sterling total return terms due to dollar strength.

- UK motor finance: The FCA announced motor finance payouts of approximately £7.5 billion, nearly £2 billion below original estimates, with 12.1 million loans eligible for compensation of up to £829 each. This should benefit domestically focussed banks and lenders that had provisioned for higher figures.

Please continue to check our blog content for advice, planning issues and the latest investment market and economic updates from leading investment houses.

Charlotte Clarke

08/04/2026