Please see this week’s Weekly Market Commentary from Brooks Macdonald which provides a brief analysis of the key factors currently affecting global investment markets:

The Santa Claus rally is underway after the Federal Reserve allows the market’s interest rate pivot to continue

Despite pushback from some Federal Reserve speakers, markets expect the first US cut during Q1 2024

Meanwhile, the Bank of Japan may only now exit its negative interest rate policy this week

After the Federal Reserve endorsed the market’s dovish pivot of US interest rate policy, risk appetite received a significant boost. By the end of the week, the US bond market implied 141bps of interest rate cuts by the end of 2024 and an over three-quarter chance that the first cut would take place by March. Bonds rallied against this backdrop with both the 2-year and 10-year yields down c. 0.3% on the week, this marks the best week for US Treasuries since the extreme market volatility of March 2020. Equities also performed strongly with the US leading the way with a 7th consecutive weekly advance.

Despite the Fed meeting sounding relatively dovish, Fed speakers on Friday were keen to push back against the growing consensus around a Q1 2024 first cut. President Williams said that the Fed ‘aren’t really talking about rate cuts’ yet and that March felt ‘premature.’ President Bostic struck a similar tone, saying that he wasn’t ‘really feeling that this is an imminent thing.’ Bostic suggested that the Fed may only start cutting interest rates from Q3, offering a counterweight to the strong bond market rally of last week. By the end of Friday the market had reduced the quantum of cuts expected in 2024 by 8bps.

The central bank focus will continue this week even as we approach the Christmas period. There has been much speculation as to whether the Bank of Japan’s negative interest rate policy would be ending at this meeting, with the market apportioning a rough 50:50 chance of that outcome. Reports have suggested that the Bank of Japan may hold off an announcement this week but strongly signal the move as ‘live’ for January’s meeting.

Whether the policy comes to an end at this meeting or next meeting is an aside to the remarkable fact that the US has gone through a full rate hiking cycle but that the disinflationary forces in Japan have been so powerful that only now is a positive interest rate on the cards.

Please continue to check our blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see the below Tatton Investment Management Monday Digest article received this morning – 18/12/2023.

Policy and politics set to play a pivotal role in 2024

Heading into 2024, capital markets are in a somewhat contradictory position. Global growth has been slow (and in some places negative) for some time, while central banks have raised interest rates at the fastest pace in a generation. But despite all those challenges, equities have had a good year overall. With inflation finally falling, central banks are now loosening their vice grips, and bond markets are predicting a slew of rate cuts from the major players starting as early as March. That has pushed risk valuations in favour of equities and, perhaps more importantly over the long term, has even bolstered growth expectations. How these expectations play out will be crucial for markets next year.

And yet, anxiety lingers. The rise in equity valuations has left stocks looking a little expensive, particularly in light of damp growth expectations in some regions. And despite the fact that no one seems to believe them, central bankers beyond the US are still toeing the official line that rates will have to stay higher for longer pretty much everywhere.

The consistent theme of this year has been that whenever markets look overexcited, monetary policymakers pour cold water over rate cut expectations. The policy outlook has become the dominant driver of markets, and ignoring what policymakers tell us has made for a volatile ride in investments all year. We expect this to continue for at least the early part of 2024. Ever since the financial crash of 2008, investors have been extremely sensitive to expected monetary policy, and 2023 was no different. This is historically unusual, but it could just be because – for most of that period – rates have been historically low. Rates staying lower for longer increases the sensitivity to rate changes because longer-duration assets gain in relative value and thus make up a larger share of the market (the so-called duration effect). Now that real interests (inflation-adjusted, i.e. what is left after inflation is subtracted) have moved higher, it is possible we will see fewer valuation effects and more focus on earnings stability and growth.

Growth prospects for the UK and Europe greatly deteriorated this year, while the US powered ahead thanks to the incredible resilience of the American consumer and considerable fiscal stimulus. Now, with inflation plummeting, interest rates will surely follow here and in Europe. Across the Atlantic, however, and regardless of the latest Fed acknowledgment that rates have peaked, market expectation remains that looser policy there might take some time. As we go through 2024, that could mean underperformance in the world’s largest economy – a reversal of what we have seen for years. If that happens, bond and equity dispersion will be joined by currency volatility. Such volatility makes firm predictions difficult. Looser monetary policy and (in the latter half of the year) an economic recovery in Europe are likely. Beyond that, unfortunately, we can only predict unpredictability.

Outlook for regions

US: The US was indisputably the standout performer this year, with US equities once again outperforming other markets. But the US economy might not be as strong as its global peers in 2024. Partly, this is about starting points; the US has grown more quickly than the rest but that growth did not spread outwards in 2023. Next year could see US demand providing more external support. That past strength is also likely to keep the Fed relatively less accommodative than other central banks (despite investors perceiving a dovish shift in the Fed’s policy following its December 2023 meeting). This could mean underperformance in US markets relative to Europe or even Emerging Markets. Currency volatility may result, perhaps continuing the recent trend of dollar weakness, which is again generally a growth positive for the global economy. There is also the small matter of a presidential election next year, which is likely to bring further spending promises and plenty of political instability. That being said, energy – especially natural gas and electricity – is much cheaper than in Europe and nowhere looks ready to match the depth and dynamism of the US economy.

The US might well become the victim of its own success in 2024. The liquidity from the pandemic period still is yet to be worked off. Meanwhile the lagged impacts from the pandemic-inspired loose fiscal stance are likely to keep the Fed from cutting rates as early as the European Central Bank (ECB) in Europe, even though growth is weakening. Markets seem to have a rosy view of Fed policy at the moment and so could end up disappointed. In our view, interest rates are likely to come down in Europe (and possibly even in the UK) before the US. These factors could bite in the second half of the year. At that point, Fed policy will have sucked up most of the excess liquidity while real disposable income growth may be slowing (possibly as wages growth slows and goods deflation lessens). We may even see the US flirt with recession. If so, currency volatility and, hence, wider market volatility, is likely.

UK: Monetary policy is perhaps the most important part of Britain’s outlook for 2024. Despite the perceived hawkishness of the Bank of England’s Monetary Policy Committee (MPC), we expect interest rates to come down, thanks to inflation finally falling back to target, and rate cuts should be underway by the summer. This will mean falling bond yields and a pick-up in equity valuations. UK equities are notably cheaper than global counterparts on a price-to-earnings basis, reflecting years of neglect by foreign investors. Valuations have plenty of room to climb and – since we expect positive bond market movements – Britain looks good value.

Next year will almost certainly see another General Election (though the latest possible date is January 2025, which is unlikely but cannot be fully ruled out) which, barring an historic turnaround, is likely to deliver a Labour government. Given Keir Starmer’s cautious approach, though, we do not expect this will dramatically change medium-term growth prospects or financial conditions. There are some hopes that trade negotiations with Europe might be improved by a structurally less antagonistic government, but any effect from this will likely be long in the future. Overall, it will likely be slow and steady for UK investors, but starting from a low base will help.

Eurozone: Economic weakness should mean supportive European monetary policy early in 2024. With any luck, and with the global economic tide potentially turning, this could translate into stronger growth in the second half of the year. These cyclical factors, combined with the relative cheapness of European equity versus the US, should mean market outperformance as of late, but risks remain. There is a risk that the European Central Bank (ECB) has overtightened already, throwing the fragile economy into deeper recession than needed. On the other hand, the continent is still recovering from its energy price shock and the fiscal deterioration it brought. We do not think these factors will disrupt what is ultimately a positive story, but we must stay wary.

We expect tight fiscal policy to be a feature of most major regions in 2024, but probably more so in Europe. That only increases the urgency of the ECB’s rate cuts, which are now a matter of when not if. Headline Eurozone inflation has been on a downward path for months. Markets have subsequently brought forward their rate cut expectations to as early as March. And even then, many commentators are suggesting the ECB is once again ‘behind the curve’ on inflation – only this time in reverse. With so much gloom around the Eurozone economy, growth optimism may seem strange. But looser monetary conditions and a recovery in global growth are sure to benefit the Eurozone. European equities are some of the most cyclical there are; the start of a new cycle should serve them well.

Emerging Markets: If our central scenario of a global cyclical recovery and weaker dollar plays out, Emerging Markets (EMs) stand to benefit in 2024. This would be helped by a Chinese economic recovery, particularly if consumers there felt confident again. With the inherent economic and financial risks surrounding the world’s second largest economy, EMs would do well to focus on securing their own prospects. Fortunately, this is already underway, particularly for regions like Brazil that sorted their inflation problems early.

For China, the main question is now not whether Beijing is willing to soften its deleveraging stance and promote growth, but whether it can. Private sector business confidence appears to have plummeted when one looks at market-based indicators. While government borrowing is now rising, private sector borrowing continues to decline. The recent spike in consumer default numbers, and the weak pricing power for goods exporters, suggests it might not be so easy. Even with central government support, we expect China to radiate disinflation for at least the early parts of 2024.

The green shoots of a global recovery, if and when they show, should boost sentiment around EM assets. But with the global economy in such a precarious position, 2024 will likely be another year where differentiating between EMs is key.

Outlook for asset classes

Bonds: In line with our expectations for government and central bank policies, we expect bond market dispersion in 2024. Despite ECB President Christine Lagarde indicating a continued bias towards tightening, a mild tightening in fiscal policy, softening wage rises, energy price falls and generally lower inflation should allow interest rates to fall sooner in Europe than in the US. That is likely to mean a widening of the gap between US and European yields in the early part of the year.

Shifts in the long-term risk premia – how long-term bonds are valued against short rates – have become more prominent in 2023. These have fallen sharply since October, dropping below historic averages. With inflation still lingering, we expect them to move higher in 2024 – primarily in the US. Relative risk valuations will impact credit spreads too, but these have thankfully been resilient. Even though growth is weak (and in some cases negative) investors do not seem to fear widespread bankruptcies or financial instability. That is good, since it will likely mean a ‘buy the dip’ mentality in corporate bond markets.

Equities: We expect global equities to be a tale of two halves, especially in the US. The heavily anticipated global recession – if it comes – will mean stagnant or falling corporate earnings, lowering the base attractiveness of stocks. On the other hand, a lot of that negativity is already priced into current equity values, after global stock markets saw heavy losses in 2022. Investors are tempted to look forward to the cycle after this one – when central banks will loosen policy and growth can start again. Optimists are hopeful about the next cycle, pessimists are still worried about this one, and everyone else is caught in the middle. Markets will likely go back and forth between these two modes until the underlying economic data makes it clear who is right.

The strength of the US equity market, much like its domestic economy, has been unparalleled in recent years. In particular, the outperformance of the US mega caps was stunning in 2023. Share prices for the so-called ‘Magnificent Seven’ – the most highly valued companies in the S&P 500 – increased by more than 70% in response to the generative AI investment craze, while the remaining stocks in the S&P gained just 10%. Whatever the justification for this outperformance, it means the US continues to be more expensive (on a price-to-earnings basis) than anywhere else.

Comparatively, British and European stocks are trading at cheap valuations. This is certainly true for the UK, whose attractiveness as an investment destination has been in decline since before Brexit. These, historically relatively cheap valuations are still a little pricey in absolute terms, at least for where interest rates are. But Europe’s rate cuts are effectively confirmed at this point, while we have argued elsewhere that the UK must follow suit. If global growth is stronger than expected, British and European equities stand to benefit.

The rest of the global equity picture is mixed for 2024. In Japan, improvements in corporate structures have gone under the radar in recent years, but it is clear that companies and shareholders are seeing the fruits of structural change. Margins are improving (from admittedly low levels) and Japanese workers are among the cheapest in the world for their skill levels. Any pick-up in exports (which can only come from a global cyclical rebound) will likely have second-round effects on wages and domestic demand, making Japanese stocks a worthwhile bet.

Currencies: Assuming our policy and economic outlook holds up, the US dollar should decline in 2024, but with bouts of volatility in currency markets. The dollar has become undeniably expensive over the last few years – thanks to impressive capital flows into the US – and this process has to stop at some point. There is every reason to think that point will come next year. Even a mild outperformance from outside of the US would likely cause some capital outflow, lowering the dollar’s value. The Japanese yen could be a particular beneficiary – considering its current cheapness on a purchasing power basis.

Commodities: Commodity prices – oil and gas in particular – will probably stay weak into the start of 2024. As the year goes on, though, global growth expectations should shift. Global growth usually means stronger commodity demand, so prices should be supported. But the amount of support depends on many factors, like where growth is expected to come from and in what form. Outside of oil and gas, metals have slowly lost ground – with the exception of iron and steel. This will not turn around until growth recovers, which is unlikely before the middle of 2024.

The biggest demand swing could come from China, whose government has made clear it prioritises consumer demand and building activity. If Beijing keeps revving the economy, prices for commodities in general will be well-supported. In this sense, we should keep an eye on commodity prices, as these could signal a wider recovery.

Property: There is potential for a property rebound in 2024, but whether it happens will depend on policy. The past year has been difficult for residential property, but activity has picked up across the world – even in China’s ailing building sector. This happened after the fall back in long-term bond yields, which suggests current rates are cheap enough to spark building activity.

Commercial real estate, on the other hand, is still in a clearing phase. The stable, post-pandemic level of demand for retail and office space is not yet clear, while input costs (including insurance) are also in flux. The end of 2023 has seen European real estate investment vehicles come under pressure – a trend that will likely be repeated across the world.

The biggest hope for property prices is government building policy. Next year will see nearly half the world’s population go through elections, and building is an easy sell for most politicians. In multiple regions, we have already seen suggestions of looser planning regulation. This has the potential to unlock substantial amount of growth for the wider economy. Prospective governments might see this as an easy win, considering that many building projects are at least partially funded by private groups, lowering the spending that appears on their balance sheets.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see the below article from Eveleyn Partners detailing their thoughts on today’s Bank of England MPC decision to continue to hold interest rates at 5.25%. Received this afternoon 14/12/2023.

What happened?

The Bank of England (BoE) held the base rate at 5.25% at their meeting today. This was the third consecutive meeting at which they have held rates at this level and was in line with market expectations.

The committee was split in its vote, as it was in November, 6-3, with the three external members of the committee continuing to prefer another 25bps increase.

What does it mean?

Today’s decision by the Bank of England will not come as a surprise to markets. What is of interest is the tone and rhetoric of the statement today. The Bank maintained its hawkish stance, that rates would need to be “sufficiently restrictive for sufficiently long” and leaving the door open for further tightening should inflationary pressures persist. That contrasted with yesterday’s FOMC statement which took a more dovish tone.

The economic backdrop to today’s meeting remains difficult. The economic data has been mixed since their November meeting, and the while progress on inflation has been made, uncertainty remains around the outlook. CPI inflation has fallen by 2.1% to 4.6%, undershooting the committee’s estimate of 4.8%. In terms of real GDP, October figures showed a 0.3% contraction, which leaves the economy set to undershoot the Banks 0.1% estimate for growth in Q4.

The fiscal backdrop has also changed, with the Chancellor easing policy in the Autumn statement and government suggesting there might be more to come in the Spring Budget, potentially adding inflationary pressure.

After the November MPC meeting, the first cut in interest rates had been priced in for August 2024. Since then, markets have grown increasingly optimistic about the timing of rate cuts – expected in May shortly before today’s meeting and remained little changed immediately after.

Bottom Line

We think the UK economy faces more inflationary challenges than some of its global peers, in particular the US, and would suggest the market for UK rates has been swept up recently in a wave of euphoria over interest cuts coming sooner than previously expected. Our view is that while the direction of travel is correct, there is risk that markets are disappointed when cuts do not come through as quickly as currently priced in.

Please check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Please see the below article from Evelyn Partners detailing their thoughts on the Fed’s decision to continue to hold interest rates at their present level. Received this morning 14/12/2023.

What happened?

The Federal Open Market Committee (FOMC) voted to keep rates on hold at 5.25-5.5% for the third meeting in a row. This marks the end of the US tightening cycle.

What does it mean?

Last night we received some good news from across the pond: the US Federal Reserve signalled that the tightening cycle is over, and it will pivot to easier monetary policy next year.

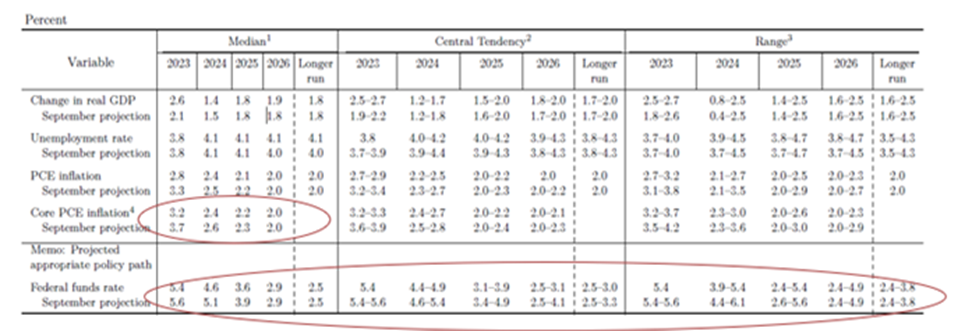

This signal came via three sources. First, the summary of economic projections, which collates the forecasts of committee members, showed that monetary policy is likely to be easier next year. The projections show that the median expectations for interest rates in 2024 were revised down from 5.1% to 4.6%—a notable move given that the previous forecasts were only submitted 3 months. This change was driven by a major downside surprise in the recent inflation data: the committee now expects core PCE inflation to be around 3.2% for 2023, instead of 3.7%.

Second, the dot plot – which maps the committee’s projections in more detail – also showed a notable decline in interest rates in the coming years.

In response, the Fed funds futures, which capture market-implied future interest rates, moved to price in 6 cuts next year, instead of the 4 expected before the meeting. The Fed isn’t expected to cut at its next meeting in January, but the market then anticipants three consecutive cuts from March to June, and it assigns a high probability of cuts in July and September.

Third, Chair Powell half-heartedly pushed back against the market’s dovish interpretation of this evidence. He noted that it was “too early to declare victory” but admitted that the committee had been talking about when to cut rates. He also said that the Fed would need to start cutting rates “way before” inflation reached its 2% target. These statements imply the next step will be to cut rates.

Unsurprisingly, markets rallied strongly on this news. The S&P 500 and Nasdaq gained ~+1.4%, while the US 10-year yield fell below 4% having topped 5% as recently as September.

Bottom Line

Last night the US Federal Reserve signalled that the tightening cycle is over, and it will pivot to easier monetary policy next year.

Unsurprisingly, markets rallied strongly on this news. The S&P 500 and Nasdaq gained ~+1.4%, while the US 10-year yield fell below 4% having topped 5% as recently as September.

Please check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Please see below the latest ‘Markets in Minute’ update from Brewin Dolphin, which covers their views on recent events in markets and was received late yesterday (12/12/2023) afternoon:

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below, Brooks Macdonald’s ‘Weekly Market Commentary’ which provides a brief analysis of the key factors currently affecting global investment markets. Received yesterday afternoon – 11/12/2023

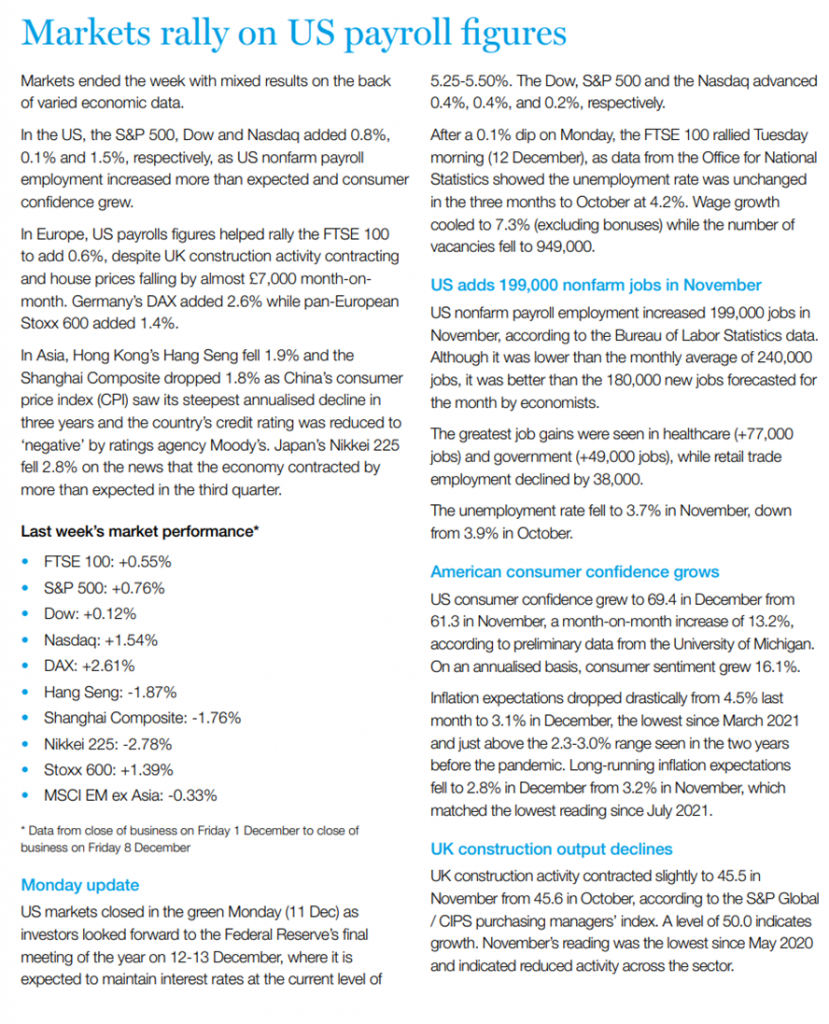

Despite the US equity market now posting its 6th consecutive weekly gain, there should be no complacency ahead of this week which sees a Fed meeting, an ECB meeting and perhaps most importantly, a US CPI print.

Before we move onto this week, we should acknowledge the US employment report which was slightly stronger than markets were expecting on a headline level and saw the US unemployment rate fall to 3.7% versus the 3.9% expected. Average hourly earnings were also slightly stronger than expectations. Taken as a whole, the US jobs report pushed back against the soft-landing narrative and expectations for a near immediate loosening of policy. There was some good news on Friday however as the University of Michigan survey showed 1 year inflation surprising to the downside, coming in at 3.1% versus the 4.3% that was expected.

The jobs report is likely to dissuade the Fed from sounding too dovish this week and markets also reduced the implied number of interest rate cuts in 2024 as a result. The key question for Wednesday’s Fed meeting statement will be whether the Fed explicitly rebukes the market’s pricing of around 4½ 25bp interest rate cuts in 2024. With the jobs report in recent memory, the Fed is likely to strike a more cautious tone, saying that while rate rises are likely finished, this does not mean rate cuts are imminent. The tone of the statement and press conference will be key, as will the dot plot of interest rate expectations. The ECB and Bank of England will report on Thursday, with expectations of a pause in interest rates from both central banks.

Before we get to the trio of central banks, markets will need to contend with the US CPI release on Tuesday. The consensus expects there to be no month-on-month inflation at a headline level and 0.3% growth for Core CPI. The major difference between these two readings is the gas price which is down -8% since October and is excluded from the Core CPI reading. The two-day Federal Reserve meeting will already be underway when the CPI report lands but it is undoubtedly going to feed into their thinking if we see an upside or downside surprise.

Please continue to check our blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below ‘Monday Digest’ article received from Tatton this morning, which provides a global market update as we approach Christmas.

After a gangbusters November for global capital markets, December is also currently on a positive track with trading volumes higher than November’s averages generally, suggesting quite a bit of capital is being put to work by investors.

Global bond yields have fallen yet again (meaning bond prices have risen), driven by fears of slowing global growth. Economic data has been mildly soft, while energy and commodities have been weak. European bonds outperformed following dovish noises from members of the European Central Bank (ECB).

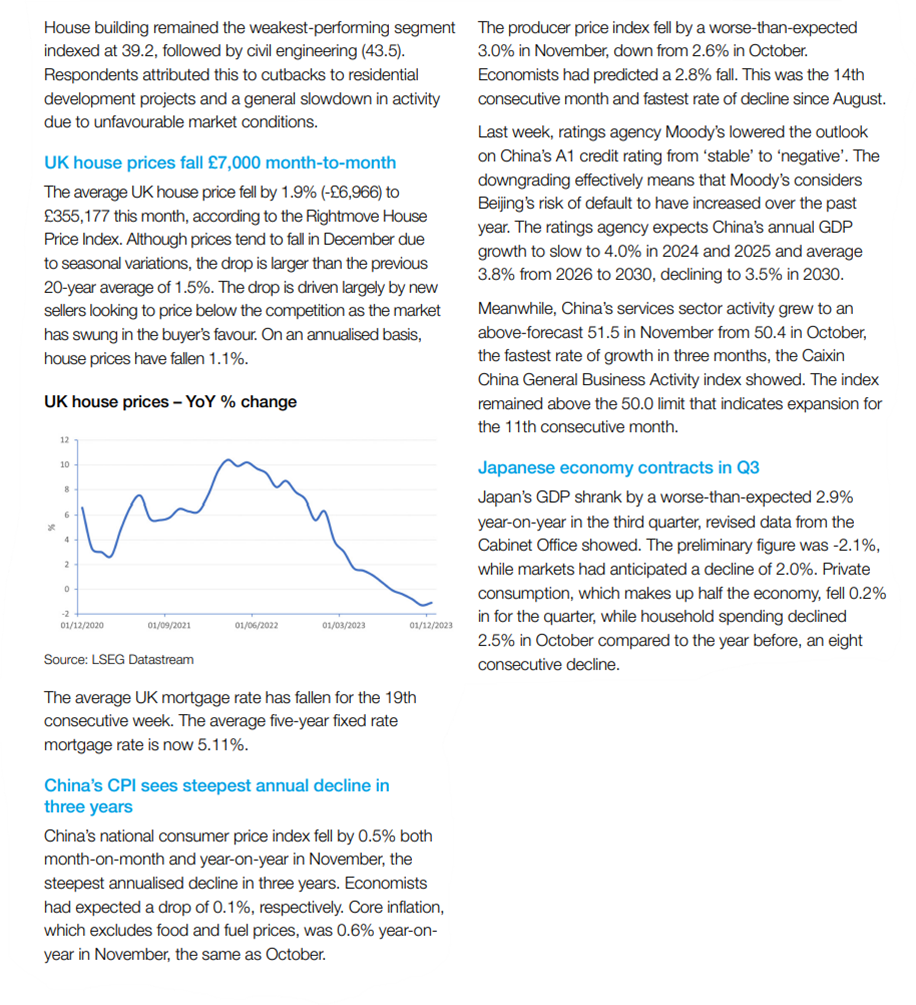

Economic data showed soft (but not awful) purchasing manager survey indices, offset somewhat by US mixed employment data. In the US, the job agency ADP’s November employment report weakened but Friday’s US employment report surprised economists by showing 199,000 jobs were added in November, a reasonable level of job creation paired with a very surprising fall in the unemployment rate, down to 3.7% from October’s 3.9%. Still, rate expectations have fallen because the policy setters at the US Federal Reserve (Fed) appear be more focused on inflation declines than worrying about what level of unemployment is too low for comfort. Nevertheless, bond investors had expected the US unemployment rate to worsen to 4% at least and November’s data does not support the case for any rate cuts without some other factor impinging.

But it seems bonds and equities are taking more of a cue from commodities and energy.

Equities ended the week back up to recent highs, with the US ‘Magnificent Seven’ bouncing back from fears about their exposure to softer consumer demand. Stocks had seen softness despite falling bond yields, as investors started to worry that earnings prospects may be challenged, with oil sending quite a weak growth signal.

Last week, we said how OPEC’s inability to act as bloc had led to ineffective supply cuts. Since then we have seen more oil price falls, and in addition, global industrial metals and agricultural prices moved down. They are less volatile than energy prices (mainly because energy stores are always relatively low compared to ongoing use) so the lesser decline is still significant. Commodity prices are still higher than they were 2021 but the decline from mid-2022 is clear. In the past 15 years, the biggest demand swing has emanated from China and there are all sorts of signals that the world’s second-largest economy is not providing the growth leadership that the largest economy in the world has given us.

With COP28 coming to a close at the weekend, the discussions have been neither a help nor a hindrance to asset and commodity prices, nor perhaps should they be, although COP28 president Sultan Al Jaber took the opportunity to swing the debate towards responsible fossil fuel policies. Ultimately, progress on dealing with emissions will be in the enactment of detailed policy, so perhaps this is good news. The conference also turned its attention to the loss of the natural world, which many think is a good refocusing.

Moody’s weighs in to add to the Chinese gloom November was the continuation of a miserable year in Chinese markets, where economic and policy disappointments have been the defining feature. At the time of writing, the CSI is down 12.5% year-to-date in renminbi terms, while the Hang Seng has dropped a painful 18.3%. Weaker-than-expected growth and trade – compared to admittedly high expectations – has been the root of China’s issues for some time. The government has repeatedly tried to counteract this with various support schemes or political pronouncements – to varying degrees of success.

Last week brought another headache for Beijing, after ratings agency Moody’s cut China’s credit outlook to negative. Moody’s pessimism extends to both government and private banking debt – both of which are feeling the pressure from an extended property market downturn. Moody’s has only changed its outlook on Chinese credit, and a slight downgrade is unlikely to affect China’s medium-term borrowing capacity in a big way. That said, the news is clearly not a good thing for the Communist Party government and financial stress has been worsened by the exodus of foreign investors from Chinese markets this year.

The Chinese Politburo met last week to avow a significant fiscal push next year. Among the policies being swung into action, the People’s Bank of China (PBOC) has introduced something that looks very much like quantitative easing (QE), or the buying of bonds. This policy can work in different ways but one of its possible implications is that financial market liquidity improves, which can then feed through into rises in risk asset prices. The lack of foreign equity buyers has generated much comment but the similar lack of domestic equity buyers has also been notable.

Chinese consumers are feeling pessimistic to, and for good reason: 8.5 million of them (around 1% of the total working-age population) have defaulted on debt payments since the start of the pandemic and been blacklisted by authorities. As well as severely constraining China’s domestic demand – a side of the economy Beijing avowedly wants to foster – struggling consumers cannot pay taxes, hence reducing the government’s funds and worsening its fiscal metrics. All of this puts the Party in a precarious position.

This weakness is surely one of the main reasons China has been so conciliatory toward the west in recent months. It is hard to see President Xi’s meeting with President Biden last month – his first visit to the US since early 2017 – as anything other than a big peace offering. Trade tensions between the world’s two largest economies may well continue, but they are likely to be pushed much more by Biden than Xi. For the global economy at least, conciliation is a positive. But for China, its underlying weakness seems worryingly hard to address.

Please check in again with us soon for further relevant content and news.

Please see below article received from Brewin Dolphin yesterday evening, which looks to the future as we near the end of 2023.

After a year of interest rate hikes and renewed geopolitical uncertainty, Guy Foster, our Chief Strategist, discusses what the next 12 months could have in store for investors.

This time last year, economists were talking about the near inevitability of a recession in 2023. In the event, the economy proved more resilient than many expected. Now, forecasts are improving for 2024 as well. If anything, the last year has reminded many forecasters that predicting recessions is a task that has eluded the best-resourced central banks for decades.

So, what can we say about the possibility of a recession hitting in 2024?

Some conditions for a recession are already fulfilled. Economists believe that most developed economies are operating beyond their capacity. This jargon refers to the fact that demand currently exceeds supply. There are, for example, shortages of some of the things economies need to grow – the most obvious being skilled labour.

Under such circumstances, central banks have been trying to bring demand and supply back into balance. One such way has sought to reduce the demand by raising interest rates. The question is whether they are able to do so with enough finesse that they do not discourage spending so heavily that they inadvertently plunge the economy into a recession.

Typically, this has proven to be a task at which policymakers fail more often than they succeed.

For them to succeed, we would need to see a more gradual realignment of demand and supply in such a way that doesn’t cause a sharp increase in unemployment. Investors call this ideal scenario a ‘soft landing’ for the economy, making it distinct from the ‘hard landing’ of a recession.

Will central banks achieve a soft landing?

With all the economic forecasting resources at their disposal, and plenty of practice, we might hope that central banks could achieve the fabled soft landing through carefully calibrated interest rate increases. The fact that inflation does seem to have peaked gives hope. But these interest rate increases do not take place in a vacuum. Often, it is the combination of the stress of higher interest rates and an external shock that tips the economy over the edge.

Examples of these shocks include the bankruptcy of Lehman Brothers and the collapse of a US housing bubble that prompted a global recession during 2008 and 2009; the collapse of the speculative bubble in technology stocks at the start of the millennium; and, in the early 1990s, the first Gulf War, which saw a sharp increase in oil prices.

So in terms of predicting whether the UK, the US or the world will enter a recession next year, we can say it is possible. In the end, however, it will likely depend upon whether the economy is subjected to some shocks which, by their nature, are unpredictable. It’s often appropriate to paraphrase former US defence secretary Donald Rumsfeld: “There are things we know we know, there are things we know we don’t know, and there are things we don’t know that we don’t know.” This is useful structure for considering the risk in economic forecasting.

What ‘we know we know’ is that the labour market is tight and interest rates have increased substantially, which raises the risk of a recession. However, the fact that inflation is falling and that recent declines in the oil price give households more flexibility over their discretionary spending makes the soft landing scenario more likely.

The things that ‘we know we don’t know’ would include whether tensions in the Middle East could disrupt oil supply and cause a price spike of the kind that has shocked the economy into recessions in the past.

But above all, there are the things ‘we don’t know that we don’t know’. As with every year, we have to acknowledge that things could happen that will not have been predicted in this or any other outlook piece. And it is that uncertainty which has historically made the forecasting of recessions a very challenging task.

Beyond the likelihood of a potential recession, we should also consider the potential severity of one. The recession taking place as Covid struck was by far the deepest in modern times (fortunately, it was also the briefest). Prior to that, the recession accompanying the financial crisis was the deepest since the early 1900s. The bubble in real estate was symptomatic of very high levels of consumer indebtedness, which ultimately caused such a severe recession. Households then spent the following decade reducing their reliance on debt and, in aggregate, are in relatively robust financial health.

What impact could upcoming elections have?

The main concern for the coming year is not consumer indebtedness, but government indebtedness – both in terms of the risk that it could cause a shock and because of the constraints that it places governments under.

For many years, there has been anxiety over the seemingly inexorable march upwards in government debt to gross domestic product (GDP) ratios. GDP is a measure of the money that gets earned within an economy and, as such, represents an upper limit on the amount that can be used to derive government revenues (what can be taxed).

The outlook for public finances will be a further ‘known unknown’ because there are a lot of elections taking place during 2024. The two obvious ones will be a probable election in the UK (which could theoretically be held any time until January 2025) and November’s election in the US.

The UK endured a brush with fiscal mortality following the mini-budget of September 2022. Even prior to that, there was widespread acceptance by both major political parties that fiscal policy should be constrained by a robust fiscal framework with independent verification of government financial projections (from the Office for Budget Responsibility). Whilst both parties will attempt to thread the needle between appearing not to be neglectful of public services and giving hope that the historically high tax burden can be reduced, it seems unlikely that either will offer particularly bold policies to do so. Labour (which currently enjoys a commanding lead in the polls) has adopted a more centrist approach after an unsuccessful lurch to the left between 2015 and 2020. The nuance upon which the election will be fought will not be revealed until a date is set, but is likely to focus on distributional and social rather than major economic differences.

In the US, it seems likely that November’s election will be contested between president Joe Biden and former president Donald Trump. Neither seems likely to strike an austere tone on the public finances, and it is possible that the bond market could react should it appear likely that Trump will win. This is because as the Republican candidate, he has a greater chance of controlling the two houses of Congress, which set budgets, than his likely opponent. Control of the Senate, where only a third of seats are contested each election, seems very difficult for the Democrats to retain. If Congress is divided, then financial policies tend to be restrained by partisanship.

What is the overall outlook for investments?

Whilst many will look to the coming election season with dread, the bright news from an investment perspective is that US election years have historically produced quite good returns. Brighter still are the relatively high yields on bonds, which now promise better returns in future years than they had done for a decade or more. These yields reflect current high interest rates, which bring the likelihood of interest rate cuts over the coming year, either to prevent a recession or at least reduce its seriousness. These are tailwinds for the equity markets.

Please check in again with us shortly for further relevant content and market news.

Please see todays daily update from Epic Investment Partners received this morning:

A few days ago, we learned that Israeli Prime Minister Benjamin Netanyahu had suspended a junior cabinet member from meetings “until further notice.” This action was taken in response to a comment that seemed to imply the individual would not object to nuclear weapons being used on Gaza. Israel’s far-right Heritage Minister, Amihay Eliyahu, also suggested that displaced refugees could “relocate to Ireland or deserts,” and that the “individuals in Gaza should find a solution on their own.”

In light of this suspension, we decided to investigate the number of nuclear weapons that Israel – and indeed the rest of the world – currently possess. We obtained our data from Google Bard. In ascending order, North Korea has 10 nuclear weapons, followed by Israel with 90. Pakistan and India have approximately 165 and 150 respectively. France has 290, while the UK has 225. China has 280, although a recent Pentagon report estimates that China now has around 500 operational warheads. However, even when combined, these figures represent only about 10% of the total number of nuclear weapons that the US and Russia possess. The US has 5,428 weapons, while Russia has 5,977.

On a positive note, the total number of nuclear weapons worldwide is estimated to be ‘only’ around 13,000. While still a large number, this is a significant decrease from the peak of over 70,000 during the Cold War.

Thankfully, we don’t have a narcissistic maniac or someone old enough to be many people’s great (great?) grandad with their fingers on the proverbial big red button!

Please continue to check our blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below, Brooks Macdonald’s ‘Daily Investment Bulletin’ received this morning – 07/12/2023.

What has happened

Yesterday’s European and US trading session saw the bond market rally continue apace however this exuberance was then curtailed by comments from the Bank of Japan suggesting an imminent change to their interest rate policy.

Bond market rally

Ahead of the Bank of Japan comments, European and US markets were becoming increasingly optimistic around the probability of a soft-landing in the US. The ADP report of private payrolls came in below expectations, supporting the view that the US labour market was cooling. Oil prices also dipped, falling to a 5-month low as weaker global economic demand was priced in. The transmission mechanism between changes in the oil price and headline inflation is rapid, particularly in the United States, so this is further good news for the market’s aggressive pricing of interest rate cuts in 2024.

Bank of Japan

Deputy Governor Himono disturbed the calm within bond markets however, observing that the negative interest rate policy of the central bank had impacted households and that a move to a positive rate would be helpful to improve household interest income. Himono said that he expected ‘there would be a sufficient possibility of achieving a positive outcome from the exit, since a wide range of households and firms would benefit from the virtuous cycle between wages and prices.’ Governor Ueda added that he saw policy management becoming ‘even more challenging from the year-end and heading into next year’, suggesting that changes were afoot. Expectations are growing that the Bank of Japan may therefore abandon its negative interest rate policy as soon as the 15th December central bank meeting. Japanese 10-year bond yields underperformed sharply as a result, leading the Japanese equity index lower in sympathy.

What does Brooks Macdonald think

The Bank of Japan is one of the last bastions of the pre 2022 ultra-low interest rate policy. The recent Tokyo CPI numbers suggested that there was less urgency to abandon the central bank’s negative interest rate policy which has been in place to disincentivise cash savings and drive consumption, in order to kickstart a moderate amount of inflation. If the Bank of Japan was to remove this policy, it would have global implications as the Yen remains one of the few markets globally where borrowing costs remain very low.

Bloomberg as at 07/12/2023. TR denotes Net Total Return

Please continue to check our blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.