Please see today’s Daily Investment Bulletin from Brooks Macdonald which provides a brief analysis of the key factors currently affecting global markets:

What has happened

The US equity market managed a small gain yesterday, setting another all-time high as Europe played catch up, recording a larger gain. The smaller cap US equity market outperformed the Magnificent Seven yesterday helping to close some of the considerable year to date performance gap between the two. With the Federal Reserve in communication blackout, there was relative calm within the US Treasury market with 10-year US Treasury yields stable around 4.1%.

Bank of Japan

Overnight the Bank of Japan, the first major central bank to have its meeting ahead of a packed fortnight, kept its monetary policy unchanged. The bank revised its core inflation forecast, expecting inflation to be lower in the upcoming fiscal year. Maintaining interest rates, and monetary policy more broadly, at ultra-accommodative levels meant that 10-year Japanese government bond yields fell slightly.

Chinese assets

Hong Kong listed Chinese equities received a boost this morning after reports circulated that Chinese authorities were considering a 2 trillion yuan stimulus measure. The package is designed to provide momentum within the stock market which has had a very tough 2024 so far. The news helped Hong Kong equities more than mainland China itself which has seen more muted gains. The market has largely shrugged off previous attempts at stimulus, fearing that the regulatory backdrop still remains hawkish towards industries targeted in 2021 and 2022 such as real estate and educational technology.

What does Brooks Macdonald think

Looking ahead to today, the ECB’s Bank Lending Survey will be released for Q4 2023. The report will help investors understand the appetite for debt in the Euro Area as well as the availability of debt supply. The Q3 report suggested that banks expected a far more buoyant Q4, investors will be looking closely to see whether this has materialised.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see the below Tatton Investment Management Monday Digest article received this morning – 22/01/2024:

Overview: ‘Lower, slower’ replaces ‘Higher for longer’

Positive sentiment, driven by expectations of an imminent and significant onset of rate cuts, began to wane last week, and global capital markets resumed their volatile path of last year. The combination of a distinct slowing in the downward trajectory of inflation, paired with increasing confirmation that economic conditions are more on the up than down (at least in the US), have made it even less probable that rates will be cut soon and fast. As a result, some investors are facing up to the very distinct possibility that rates may only begin to be cut later and then more slowly. In other words ‘lower, slower’ seems to be replacing last October’s ‘higher for longer’ narrative.

Consequentially, bond yields rose again last week, led by more rises in the US Treasury market. In the US, mega-caps were notable performers and the Nasdaq Composite regained the 15,000 level. However, equities overall generally drifted downwards with smaller caps under pressure. Non-US markets also declined.

Global companies are reporting lacklustre results for the last quarter of 2023 and givingsimilarly tepid forward guidance. It’s still the early stages of the reporting cycle, with just 6% of S&P 500, companies having reported, mostly banks, consumer and industrials. Bank results have been mixed, while consumer names are seeing less US spending power as households’ cash savings decrease. Revenue ‘beats’ may be not as positive as hoped, but broadly speaking, expectations for US companies’ earnings growth are still strong, driven mostly by US domestic demand.

Last week’s return of seemingly indecisive markets suggests a creeping realisation that the inherent impatience of markets has once again led to unrealistic expectations over the potential rates ‘reward’ on falling inflation. Does that mean market sentiment has reversed and investors are no longer optimistic? No, not at all from what we can see. A dose of realism into how long it may actually take for economic and market fortunes to be sustainably positive again may well offer up some short term investment opportunities, particularly while markets have re-entered range-bound terrain.

Just how sustainable are European and US deficits?

At the moment, fiscal deficits are high by historical standards and rising over the long-term. This is not the short-term funding gap we saw in the pandemic, but a sustained push toward looser fiscal policy, and it is happening across virtually all major economies. With bonds currently in limbo, understanding countries’ fiscal positions – and whether they might lead to instability – is key. Even though rising deficits can be seen across the world, the outlook varies by region – most consequentially between the US and Europe.

In the US, deficit spending has continued and grown under President Biden. Some of this is a hangover from pandemic-era policies, but even after those have faded there has been a substantial increase in the gap between federal tax receipts and spending. The US government is running a cumulative deficit of $509 billion for the 2024 fiscal year so far,$94 billion more than in the same period in the prior fiscal year. Tax receipts are growing, thanks to the enduring strength of the underlying economy, but outlays are growing faster. Sustained fiscal expansion is one of the main reasons why US growth remained surprisingly strong last year. It is almost inevitable that this impetus will reverse but a sharp change in outlays could make things extremely difficult. Some analysts have argued on this basis that the US economy will struggle in 2024. The flipside of this, though, is that the Federal Reserve (Fed) has made clear its intention to cut rates, bringing down short-term yields and lowering immediate borrowing costs. That would constitute a substantial relief in terms of interest expense for the Treasury, since it has done a lot of its borrowing through short-term markets.

Heading into election season, the fiscal deficit will likely be an avenue of attack against Biden. This will probably happen regardless of which Republican candidate ends up on the ballot, even though Trump’s own fiscal record is clearly questionable. Fiscally conservative rhetoric will be heard – even perhaps from the more centrist Democrats – but that does not guarantee fiscally conservative policy.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below, Brooks Macdonald’s ‘Daily Investment Bulletin’ which provides a brief analysis of the key factors currently affecting global markets. Received this morning – 19/01/2024

What has happened?

Equities saw a rebound yesterday as technology shares rallied in light of a positive 2024 outlook from chipmaker heavyweight, TSMC. The American Depository Receipts, which seek to track the share price of foreign listed companies, of TSMC rose by almost 10% yesterday. European equities also participated in this rally, rising over half a percentage point. This stock specific news helped buoy equity markets but the overall tone in bond markets remained downbeat as the interest rate cut narrative wilted in the face of further strong US economic data.

US economic data

The weekly initial jobless claims, which continue to help drive week-by-week sentiment, were stronger than expected with just 187k unemployment filings, versus the 205k expected. The 4-week average, which smooths out some of the larger moves, fell to the lowest level since February 2023 so it appears that labour market tightness is still a feature of the economy. After this data, the US 10-year Treasury yield continued to rise, hitting a one-month high of 4.14%. Longer dated bonds also moved in sympathy with the US 30-year Treasury up to 4.37%, the highest level in 6 weeks. Europe was not immune, with 10-year bund yields also rising on the day.

ECB

With the next ECB meeting less than a week away, the market has been focusing on the path of European interest rates. Yesterday saw the release of the December minutes which echoed the recent concern from ECB speakers that the de facto loosening of conditions caused by market interest rate cut expectations, is premature. The minutes that said ‘concern was expressed that the sharp market repricing threatened to loosen financial conditions excessively, which could derail the disinflationary process.’ The ECB appear to be committed to seeing disinflation embedded before endorsing the market’s pivot.

What does Brooks Macdonald think?

US political risk will start coming into the frame as the year continues and the US Presidential race hots up. Yesterday saw the US government avoid a partial government shutdown after a stopgap bill was approved. The can has been kicked down the road until March in order to allow lawmakers to agree to a politically contentious long term funding bill. Congressional leaders will be hoping to avoid several short-term bills as it increases the risk of a long-term bill being negotiated during the Q3 where the political pressure will be greatly heightened.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see the below article from Evelyn Partners detailing their thoughts on this morning’s UK inflation announcement for December 2023. Received yesterday.

What happened?

UK annual headline CPI inflation for December was reported at 4.0% (consensus: 3.8%), which was marginally higher than November’s reading of 3.9%. In monthly terms, CPI was up 0.4% (consensus: +0.2%), compared to a decrease of 0.2% in November.

Core inflation (excluding food, energy, alcohol, and tobacco) was 5.1% (consensus: 4.9%), which was consistent with the prior reading.

What does it mean?

UK CPI in December came in hotter than expected, marking a blip in inflation’s downward trajectory. The biggest concern right now is the services category, which was up 6.4% vs the expectation of 6.1%. The Bank of England will want to see some deceleration in this category before they can be confident in easing policy.

But looking forward, we expect CPI to continue to decelerate for two main reasons. First, the base effects look favourable in the coming months. Second, energy prices are likely to fall — Cornwall Insights, an energy research firm, forecast that the Ofgem price cap will fall by 14% in April.

The largest upward contribution to the monthly change in the December CPI annual rate came from alcohol and tobacco division, with prices rising by 12.8% in the year to December 2023. This increase was largely due to an increase in tobacco duty, after the government announced higher taxes in their autumn statement.

The largest downward contribution came from food and non-alcoholic beverages. Meanwhile, the gas and electricity category also continued to pull down the headline figure following the October change to the Ofgem energy price cap.

Traders now expect around five interest rates cuts in 2024, with the first coming in May. Although they have rowed back on their expectations at the start of the year when they priced in six cuts for the year.

Sterling rallied on the data release, and we could see some pressure on front-end gilts when the bond market opens this morning.

Bottom Line

This was a disappointing inflation print for the Bank of England, but it likely marks a bump in the road to lower inflation. With energy prices set to continue falling, it’s looking like inflation could be back at the 2% target by the middle of 2024, giving the Bank room to cut interest rates.

Please check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Please see below this weeks markets in a minute article from Brewin Dolphin, received late yesterday afternoon 16/01/2024.

Guy Foster, Chief Strategist, discusses the risks of escalating tensions in the Red Sea, while Janet Mui, Head of Market Analysis, analyses the latest US inflation figures.

As the second week of the year drew to a close, the contrast with 2023 remained tangible. The market seems to continue to see the glass half full, and even when confronted by some challenging technical and seasonal trends, the January blues are looking quite short-lived.

After losses in the first week, markets generally rallied in the second, and there was little in the way of news flow to point to as the drivers. At the end of the first week, US jobs growth was strong but with stronger wage growth than had been expected. So, the main theme of economic data at the beginning of 2024 was that recession risks were low, but with hints that inflationary pressures remain.

And that message continued into the second week. Again, it was a relatively quiet one from a news perspective, but the data continue to support the idea of an economy that is doing well with some lingering inflationary pressure.

Inflation persists

What were these data? The main news of last week was the US consumer price index (CPI) report and, jumping to the punchline, even though the report was stronger than expected, the markets showed little evidence of anxiety over the inflationary or interest rate outlook.

The headline rate of inflation was higher than expected but headline inflation tends to be dominated by food and energy prices. Energy prices have been weak but because they are volatile, it can be difficult to determine the extent to which movements in headline commodity prices translate into higher consumer prices from one month to the next. Furthermore, a rising oil price does not necessarily reflect robust domestic economic demand, and therefore would not necessarily prompt a response from the central bank (such as an increase in interest rates). So, attention naturally shifts to the core CPI measure, which strips food and energy prices out.

Core CPI was in line with expectations with prices rising 0.3% over the month. The bad news is that continued monthly increases at that pace would be exceeding the Federal Reserve’s inflation target, whereas increases of 0.2% would be consistent with that target. Fortunately, we can also assume that core CPI will come down in the future. Shelter is a large part of the index and rental inflation has been slowing. This strongly suggests that in the future, the rent of the shelter category will slow too.

This time it’s personal

In a sense it doesn’t matter, because the Fed does not base its policy decisions upon the CPI rate of inflation. Instead, it prefers the Personal Consumption Expenditure (PCE) Price Index. This number gets far less coverage than CPI, mainly because it comes out much later in the month, but what it lacks in timeliness it makes up for in relevance. With a lower weighting to rent and without the distortions of energy prices, and with a lower weighting to used vehicles, which were another temporary anomaly from the current month’s report, the core PCE is considered more accurate. Both are suggesting very similar annual rates of inflation at the moment, but the six-month annualised rate of core PCE price increases will likely drop to the Fed’s target of 2% when the data is eventually reported at the end of the month.

Were that to happen, the economy would enjoy the fabled Goldilocks scenario, which would be in play for the short term at least, as growth still seems ok. The weekly jobless claims data stubbornly refuse to rise, and the CPI data that we have just discussed gives an opportunity to estimate current consumer spending, which is the biggest driver of economic growth.

With the increase in employment, the increase in wages and notwithstanding the decline in hours worked, aggregate US consumer incomes increased by 7.8% over the last year – that is the fastest since January last year. This makes four months of consecutive improvement. Adjusting for inflation, real aggregate income growth has been 4.4%, so if employment remains robust and aggregate income expands faster than inflation, that should support economic growth and company earnings.

Earnings season We’ll find out over the coming days how companies faired during the last quarter as the US Q4 results season began in earnest on Friday. There will be plenty of headlines and statistics about the earnings season but in reality, it is difficult to draw many conclusions from the numbers posted in company results. Instead, it is what they say about the future that has more value. For instance, it seems likely that around 80% of companies will beat estimates, which sounds impressive until you realise this happens almost every earnings seasons. Typically, sell-side analysts at banks will forecast earnings and be overly optimistic. Over the course of a year, they will gradually reduce their estimates such that by the time the company reports, it beats reduced estimates.

Over most years, the aggregate market will see earnings undershoot estimates by around 6%. But that doesn’t necessarily matter as there have been plenty of years in which earnings have been poor in absolute terms, and disappointing relative to estimates (a year ahead). Investors have rightly been more focused on the future flow of potential profits from the company than any single year.

Banks got earnings season up and running on Friday. JP Morgan seems to have impressed while Citigroup and Bank of America underwhelmed.

Takeaways from management were encouraging. The Bank of America CFO said the bank thinks the soft landing is playing out. Jamie Dimon at JP Morgan was a little more circumspect, acknowledging that the economy continues to be resilient, and that consumers are still spending. He noted that markets are expecting a soft landing. But he highlights the size of the fiscal deficit and the pent-up impact of previous stimulus as reasons not to be too confident over current economic performance.

Rather than a Goldilocks scenario, Dimon emphasised that supply chains, the green transition, and healthcare would require higher levels of spending in the future, which could lead to higher inflation and interest rates. On the growth side, he warns of some of the uncertainties we noted in our annual preview; the economy is primed for recession with limited spare capacity but could easily avoid it with a fair wind. The problem would come if the economy was subject to economic shocks such as a spike in oil prices or disrupted supply chains.

On the Red Sea

On that note, of course, the other main news of last week saw an expansion of hostilities in the Red Sea. On Thursday, the US and UK intervened, with non-operational support from other Western nations, in military actions against Houthi rebels in Yemen. This is intended to prevent them from haranguing shipping en route to the Suez Canal. In advance of the attacks, the rebels warned there would be a response to them.

Since the attacks, they have continued targeting Israeli vessels. Iran has meanwhile condemned the attacks by the US and UK, and Saudi Arabia (which has been in conflict with the Houthis for almost a decade) expressed concern and pleaded for restraint. Oil and gold rose sharply on news of the intervention by the US and UK, although oil was sinking later in the session.

Traffic is still flowing through the Red Sea but at hugely inflated rates, reflecting the added risk to shippers. Meanwhile, many larger shippers have diverted around Southern Africa, which adds a further ten days and the requisite costs to the journey. These additional costs will be reflected in consumer prices at some stage, albeit goods prices are not the most influential category.

Please check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Please see below article received from Brooks Macdonald this morning, which provides a global market update with reference to political and economical developments in the US.

Despite an upside beat to US CPI last week, US bond markets became more confident that the Federal Reserve would cut interest rates in Q1 2024. Against this backdrop the US equity market rose almost 2%, with the index now less than half a percentage point away from its all-time high. Today will see a slow start to the new week with the US on holiday for Martin Luther King Day.

Despite US markets being closed, there will be some US headlines later today after the Iowa Caucus which will be a test of Republican appetite for a Trump nomination. Recent polls have pointed to a significant lead for Trump however commentators will be waiting to see if he can achieve 50% of the vote which would lock out any contenders regardless of vote switching as rivals drop out. Taiwanese politics will also be in focus after the presidential election which saw the incumbent Democratic Progressive Party (DPP) win with just over 40% of the vote. The DPP’s leader, William Lai Ching-te has previously been labelled a separatist by Beijing therefore markets are wary of any escalatory rhetoric in the aftermath of this win. So far neither Beijing nor the DPP have said anything to stir tensions, but this remains one to watch.

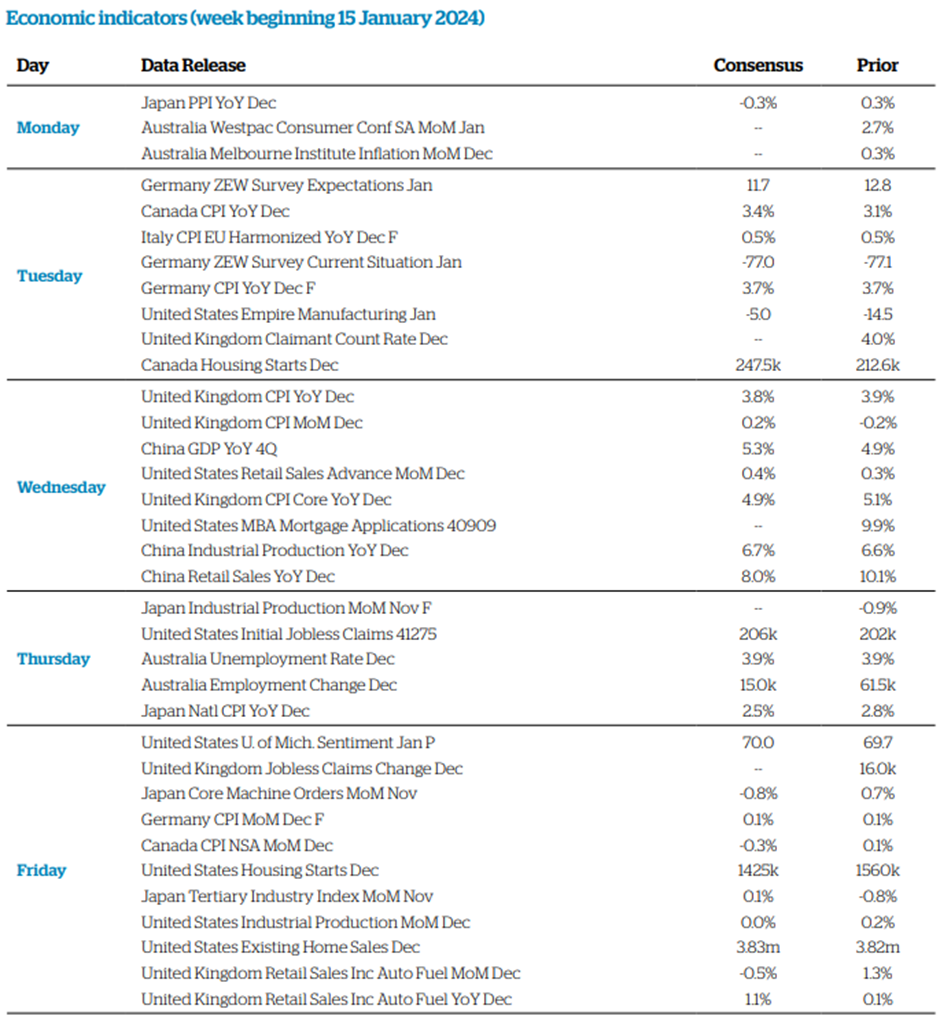

Alongside a busy week for the US earnings season, we will receive the latest US retail sales numbers for December. Given the importance of the month for sales, this will give an insight into consumer momentum as we continue through 2024. Housing data and the latest University of Michigan consumer survey will also be worth noting. In the UK, we have a large set of important data points including labour market measures on Tuesday and retail sales on Friday. The most important release will be the UK CPI report, on Wednesday, with the Bank of England hoping for continued signs of disinflation.

The Bank of England is eager to tilt towards a more balanced, or even accommodative, monetary policy. UK economic data has broadly flatlined in recent quarters, suggesting a stagnating economy. The Bank of England faces a very different backdrop to the US where economic momentum continues to feed the demand side of the inflation story. If UK CPI continues to come down the market could find the UK central bank changing its tune quite rapidly.

Please check in again with us soon for further relevant content and market news.

Please see this week’s Tatton Monday Digest update received this morning: Overview: a bumpy upwards path ahead

The equity market’s New Year malaise lasted no longer than usual. Last week, European equities recovered the previous week’s losses while US indices moved ahead smartly. However, softness in global banks hit the FTSE 100, as did a continued pullback in energy and materials sectors (that is, the more commodity-related companies). The standout performer was Japan, where investors appear convinced a corner has been turned. The Nikkei 225 broke the 35,000 level for the first time since 1990. Meanwhile, although issuance of new corporate bonds has slowed a little, corporate bonds as an asset class overall appeared to get a big infusion of investor capital. One can conclude from this that fears about a near-term recession have not just ebbed, they have effectively disappeared.

Against this backdrop of positivity, the risk for asset prices is unlikely to be about current earnings or their future growth. Nevertheless, in terms of upside, as we enter earnings season, companies will need to report lots of surprisingly positive Q4 earnings and solid outlooks in order for equity prices to rise substantially from here. Across the world, valuations (such as price-to-earnings ratios, even when using analyst expectations which include next year’s anticipated growth) are slightly expensive within the historical ranges, and they are expensive in the US.

The last few months point to rising investor confidence. Household/consumer and business confidence is showing early signs of turning upwards, and this positive combination augurs well for risk assets. The key question though, is whether positive growth will be gentle enough to keep prices stable and allow central banks to cut interest rates before the summer as markets have thus far anticipated. The next round of central bank meetings begins with the European Central Bank on Thursday 25 January, with the US Federal Reserve and Bank of England meetings scheduled for the following week. Given how much market fortunes have been tied to interest rate and yield levels over the past two years, yet again it is the central banks, and not so much the underlying economy, that will determine the direction of market travel over the coming quarter. Central bank watchers will be very busy over the next two weeks.

Has the disinflation trend come to an end?

Inflation expectations are key to the investment outlook for 2024. But there are already suggestions that markets may have gotten overexcited about the likelihood that inflation continues to decline at last year’s pace. Last week’s release of December’s consumer price index (CPI) numbers from both the US and Eurozone were higher than economist expectations. Eurozone inflation rose to 2.9% in December. However, inflation pressures were more apparent in the US, where the year-on-year overall CPI rate ticked up from 3.1% to 3.4% in December.

While we are sounding alarms about “transitory” dis-inflation, the further course of inflation is certainly something we will watch closely as we start the year. The early winter rally – and market excitement about disinflation – has set the scene for disappointment in at least some assets. Judging which ones is crucial for the year’s investment outlook. We can say two things with confidence. First, the recent valuation driven equity rally certainly makes stocks vulnerable to a short-term correction if there are inflationary signs. These might not come – and we have argued that China’s disinflationary impulse is a huge but often-ignored factor. But if they do, current valuations look vulnerable in the short-term – even if they are fair for the longer-term picture.

Second, the answer varies dramatically by region. The US market has been investors’ darling for years, and the Fed led the way in signalling rates easing this year. Europe, by contrast, has much lower equity valuations, even after recent outperformance. Core service inflation in Europe has also been surprisingly weak – particularly compared to the US. This side of the Atlantic, services look much more likely to pick up the disinflation slack.

India’s stalling reform progress

India is something of a fan favourite for UK investors, for multiple reasons. The world’s fifth-largest country economy is growing faster than any of those above it. It has strong economic and financial ties with developed nations – a particular draw for UK investors – but its financial and corporate structures still have plenty of room to improve. More recently, India’s stock market also benefitted from Emerging Market (EM) investors dramatically reallocating their capital away from the disappointing China. This led to a 20% jump in the Nifty 50, India’s headline equity index, in 2023. The index has doubled since the start of 2019.

India’s path in the last two decades has been remarkably similar to China’s between the 1990s and 2010s – a strengthening of corporate governance, opening up of asset markets and closer alignment with western-style international trade rules. This reform agenda has been at the heart of Prime Minister Narendra Modi’s two terms in office. Modi’s second term is set to end in a few months, with Indians going to the polls in the April-May general election. Even though his Bharatiya Janata party (BJP) is overwhelmingly expected to win, it would be hard, though not impossible, for the BJP to repeat or better their landslide 2019 performance. Modi remains popular even after nearly a decade in charge and some highly unpopular policies (like the initial reaction to demonetisation) – in large part thanks to improving economic conditions. But extending political gains this far into an administration is always a challenge. And for all the talk about Modi’s reform agenda (his allies promised a slew of labour law changes and privatisations within months of his second victory) his second term has been underwhelming. If the BJP loses seats, reforms will be harder to implement. On the reform basis alone, then, foreign investors have little to get excited about in 2024.

But India’s equity market success is also propelled by economic optimism – which is likely to carry on for the time being. Moreover, Indian assets are supported by production reallocation from China, whose risks are still very apparent. Whether those flows will continue later through the year is debatable. As we head into the election and beyond, investors might well re-evaluate their enthusiasm for India.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below, Brooks Macdonald’s ‘Daily Investment Bulletin’ providing a brief analysis of the key factors currently affecting global markets. Received this morning – 12/01/2024

What has happened?

Overnight the news that the US and UK have launched air strikes on Houthi rebels in Yemen is the main geopolitical story, however yesterday’s trading session was dominated by the US CPI release. US equity markets initially suffered after CPI came in above market expectations, however those losses were ultimately erased for the index to close only a few basis points lower.

Houthi air strikes

President Biden announced the strikes overnight saying that he would ‘not hesitate to direct further measures to protect our people and the free flow of international commerce as necessary.’ Oil prices rose as a result of this action and the market will also keep a close eye on container freight costs which will have inflationary impacts if they remain elevated.

US CPI

Starting with CPI, the monthly and annual headline CPI figures both surprised to the upside by 0.1%, meaning that the monthly figure expanded by 0.3%. For core CPI, the month-on-month expansion was also 0.3%, but that was in line with market expectations, although the year-on-year number fell less than hoped. The CPI readings were not disastrous for the soft landing narrative but continue to suggest that it will prove difficult to shift some of the stickier CPI subcomponents. In terms of those components, shelter is still running at 0.46% month-on-month which is important given its weight in the CPI basket. Interestingly, the PCE inflation measure, which the Fed officially targets, has a lower proportion allocated to shelter so may see less stickiness from this driver.

What does Brooks Macdonald think?

One of the logics behind the market rally later in the session was the realisation that if PCE continues to fall, despite CPI remaining sticky, this could give the US Federal Reserve the justification to cut interest rates should it want to. A surprising outcome from the day was the market’s expectations around a Fed interest rate cut by March which actually increased above a three-quarter percentage point probability. This occurred despite Fed speakers continuing to push back against such a certainty, with President Mester saying ‘I think March is probably too early in my estimate for a rate decline because I think we need to see some more evidence.’

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see the below article from Evelyn Partners detailing their thoughts on the US CPI inflation announcement for December 2023. Received this afternoon 11/01/2024.

What happened?

US December annual headline CPI inflation rose at 3.4% (consensus +3.2%) and compares with +3.1% in November. On a monthly basis, CPI rose 0.3% (consensus +0.2%), compared to an increase of 0.1% in November.

Turning our attention to the core figure, which excludes volatile food and energy prices, the annual number came in at 3.9% (consensus 3.8%), compared to 4.0% in November. In monthly terms, core CPI increased 0.3% (consensus 0.3%), which compares to 0.3% in November.

What does it mean?

December’s inflation report came in slightly above forecasters expectations with headline CPI re-accelerating slightly to 3.4%. However, core inflation continued to ease, falling below 4% for the first time since May 2024 with today’s figure of 3.9%.

The index for shelter continued its recent trend upwards rising by 0.5% on the month, shelter accounted for over half of the overall monthly inflation figure. However, on an annual basis shelter inflation has slowed to 6.2% from its peak of 8.2% in March 2023. Having decelerated dramatically during October and November the index for energy increased by 0.4% for the month of December, as increases in electricity and gasoline were large enough to offset the decrease from natural gas.

The faster than expected deceleration of inflation seen during the final quarter of 2023 has prompted money markets to start to anticipate rate cuts as early as March 2024. This change in market sentiment was provided some credibility by dovish communication from the Federal Open Market Committee (FOMC). Despite holding the base interest rate unchanged at 5.25-5.5% during their December meeting, the committee changed its forward guidance to signal it now expects to cut rates three times during 2024. This marks a considerable change in tone from the September meeting, when the committee did not expect to cut interest rates at all this year.

Despite Non-farm payrolls beating consensus estimates in December and the unemployment rate remaining low at 3.7%, wage growth appears to be normalising to levels consistent with 2% inflation over time. At the start of November, Federal Reserve (Fed) chair Powell stated that wage increases have come down significantly and are now “substantially closer to that level that would be consistent with 2% inflation over time”. On top of this, US productivity has been improving, with annualised Q3 productivity growth at 5.2%. So, despite annual wage growth remaining elevated at 4.1%, companies are still being rewarded by higher levels of output per unit labour cost. This should mitigate some of the inflationary pressures typically expected from heightened wage growth.

Immediately following the report bond yields rose with the US 10-year treasury note gaining ~7bps

Bottom Line

Despite today’s report showing in aggregate, limited new disinflationary progress, over recent months there have been three key macro trends that, in our view, have reduced the likelihood of a US economic hard landing. First, the labour market has started to soften without a notable step up in the unemployment rate. Second, wage growth is starting to moderate towards levels that would be consistent with the Fed’s 2% inflation target. Third, inflation has been decelerating faster than many forecasters had expected.

Money markets are currently pricing in rate cuts as early as March, in our view, that may be too soon, but if the labour market and inflation data softens further over the coming months, then we think US interest rates are likely to begin falling as we get towards the summer.

Please check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Please see below the latest ‘Markets in Minute’ update from Brewin Dolphin, which covers their views on recent events in markets and was received late yesterday (09/01/2024) afternoon:

At the end of 2023, everything rallied – and at the start of 2024, everything has sold off. This has not been an enormous shock. The fabled Santa Rally means that the S&P500 has risen in 15 out of the last 20 years. The flipside of this is that only ten of the last 20 Januarys have provided gains. When taking into account the currency exposure a UK investor suffers, this drops to eight out of the last 20 Januarys. The UK equity market is even more stark. 17 of the last 20 Decembers have seen gains, and only seven of the last 20 Januarys.

Seasonal trends do not form the bedrock of a reliable investment strategy. On average, January has been the worst month for the UK equity market but last January, stocks jumped 4.4%. As the influential investor Howard Marks remarked, “Never forget the six-foot tall man who drowned crossing the stream that was five feet deep on average.”

So, while the odds are generally slightly more favourable for December than January, this particular December saw a rally so strong and so broad that it pushed a number of stocks into overbought territory (when companies have rallied particularly sharply, they are overbought and often need to slow down or even reverse their gains).

Markets also seemed to suffer from a form of selective blindness, in which they took great cheer from the dovish central bank and were less concerned by signs of inflation persevering.

All of this meant that the early days of January were likely to see profit taking, as seems to have been the case

Middle Eastern escalation

Another issue the markets have been comfortable overlooking is the rise of geopolitical risk. The 7 October attacks on Israel saw a sharp rise in the oil price, reflecting the risk that the attacks could begin a cycle of escalation that might eventually disrupt energy supply. In the final months of the year, though, this risk was overwhelmed by the greater risk that the Organization of the Petroleum Exporting Countries (OPEC) might be oversupplying energy to the global economy, and that it might struggle to restrict supply in the face of price falls. During 2023, Saudi Arabia restricted its own supply to support prices for OPEC as a whole, but continuing to do so indefinitely would undermine the point of the OPEC operating as a cartel.

So, oil was weak at the end of last year, contributing to the increasing hopes of a soft landing for the global economy. But it picked up over the last week as the threat of escalation in the Middle East has returned. Prior to last week, we already understood that Houthi rebels, who have been fighting a civil war in Yemen for the last decade, had begun harassing shipping navigating the Red Sea through missile and drone attacks and attempted boardings. Over the New Year’s weekend, the US Navy intervened to defend shipping, was fired upon, and ended up sinking Houthi vessels. However, this action has not deterred Houthi attacks.

As discussed, the risk to oil is that a broader Middle Eastern conflict emerges from the current proxy wars involving Iranian-backed groups operating throughout the region. Over the course of last week, aside from activity in Yemen, the US struck Iran-backed militia in Baghdad with a drone strike and two bombs were detonated in Iran.

Fretting over freight rates

There are, however, more direct consequences of the Houthi harassment of shipping. The Red Sea is the gateway to the Suez Canal, which forms a well-travelled shipping artery between Asia and Europe. 12% of global trade travels this route each year and disruptions (as occurred when the vessel Ever Given blocked the canal in 2021) have serious repercussions for supply chains. It can mean that shipping either has to travel a further ten days around the southern cape of Africa, or for urgent transit, shippers will redemand higher transit fees to compensate them for the heightened risk of navigating the Red Sea.

Freight rates have risen sharply, despite the good fortune that these attacks began as the peak season was drawing to a close. Demand will, however, pick up, particularly ahead of Chinese New Year in mid-February. Unfortunately, they also come at a time when the water level in the Panama Canal is unusually low, restricting its use for pan-American transit. Anecdotal reports have suggested that freight rates have risen to multiples of the rates being charged a few weeks ago.

Should this trend continue, those costs will be reflected in consumer goods prices. Consumer goods have been an important source of disinflation over the last few months despite services costs seeming to remain persistently high. As a rule, goods prices in developed economies will likely reflect some combination raw material, transport and currency costs (recent weakness of the dollar will push up imported goods costs). Beyond this, goods may be over or under supplied, and after the surge of pandemic demand, consumer goods production outstripped demand, leading to a need for destocking, a process which seems to be coming to an end.

By contrast, a lot of services prices reflect wages. These have moderated in some regions (the US) more than others (the UK and Europe). But services prices have been slower to decline.

January’s jobs report

The US labour market was the main source of economic news last week. An ideal scenario would be one in which the inflationary pressures (slowing wage inflation) ease whilst employment levels remain high enough to keep the economy going. Early last week, we learnt that the number of job openings continued to decrease (albeit marginally), consistent with the idea of a loosening jobs market and a gradual decline in wage pressures. Last Thursday’s jobless claims data suggested that very few people were losing their jobs. This was all in keeping with the case for soft economic landing.

Friday saw more employment data which muddied the waters a little. Jobs growth was strong and should be good for growth, as long as it isn’t inflationary. But in December, wages did rise faster than expected and the unemployment rate stayed low at 3.7%. The labour force participation rate fell to its lowest in almost a year. These data will give the Federal Reserve some reason to fret over how fast inflation will decline in the future.

So, it has been a rough start to the New Year, but that would be expected given the strong finish to last year. Looking ahead, investors will be looking for evidence that tensions de-escalate in the Middle East. At home, they will want reassurance that the US labour market is not too hot to drive to prompt inflation, whilst also not being too cold so it provokes a recession.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.