Please see below this week’s Weekly Market Commentary from Brooks Macdonald, received yesterday afternoon – 08/01/2024

In summary

The US Equity Index posts its first weekly loss after nine weeks of consecutive gains

The headline US employment report pointed to a robust labour market backdrop

This week the market will focus on the US Consumer Price Index (CPI) report, released on Thursday

Markets began 2024 in a downbeat mood with equities suffering as bond investors pushed back their expectations for US interest rate cuts based on the US Federal Reserve (Fed) commentary and strong economic data. The highest profile of these strong data points was the headline US employment report on Friday. This week the main event will likely be the US CPI report which is released, unusually, on Thursday.

The headline number of new jobs created in the US was 216,000 versus market expectations of just 160,000. With that stronger number, the overall unemployment rate remained steady at 3.7% compared to the consensus expectation of a rise to 3.8%. Lastly, the average hourly earnings was expected to slow to 0.3% however it actually still expanded by 0.4% month-on-month. Within the data there were some signs of a slowdown including the household survey which showed a loss of 686,000 jobs, the highest since April 2020. Last month that same survey saw a gain of 586,000 so clearly volatile, but one to keep an eye on. Later in the day, the US Institute of Supply Management (ISM) services survey pointed to a significant weakening in job prospects with the employment subcomponent back to levels last seen in 2020. The combination of the ISM survey and non-farm payroll report shows a mixed picture. However, markets latched onto the headline number of new jobs created, creating a sombre mood even if the US Equity Index did manage to post a very small gain by the end of the day.

Thursday will see the US CPI report released for December, with market expectations pointing to a headline 0.2% month-on-month gain and a 3.2% year-on-year gain. For the core CPI figures, the consensus expects 0.25% month-on-month and 3.8% year-on-year. The year-on-year numbers continue to fall, however it is clear that the ‘last mile’ to bring the CPI numbers back to the Fed’s target are going to be difficult.

With the US equity market having had a negative week, after a very impressive nine consecutive weeks of gains, sentiment is clearly a little shaken ahead of the US CPI release. This week, alongside the CPI report are a series of Fed speakers, a number of Treasury auctions which will test appetite for US Treasuries at the current yield levels and also the latest New York Fed 1-year inflation expectations.

Please continue to check our blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see this week’s Tatton Monday Digest update received this morning:

Overview: After the party, the hangover

After the Christmas party, January perhaps started with a bit of a hangover. After an exceptional last two months of 2023, both equity and bond prices fell back last week as trading volumes normalised. UK and US yields were up quite sharply on the week, at 3.80% and 4.05%, respectively. Equities also responded in their usual way of falling back some 1%-2% through the course of the week, with some notable underperformance from tech-related stocks.

Professional investors, like us, seem to have looked at the lower yields on bonds and larger cap equities and decided to take the near-term profit. In part, this may well be because they are making space in portfolios for potential new investment positions. Companies are seeing the lower cost of capital as an opportunity to finally replenish funds with new bond issues, and equity issues in the form of initial public offerings (IPOs) and convertible bonds offering the appealing combination of bond-like downside protection with equity upside.

Such behaviour is born of optimism rather than pessimism. Companies want to raise capital because their business can generate a better return than the cost of that capital (even at these relatively higher rates than in the past few years) and investors believe in the new opportunities. It also suggests that capital markets are more in balance now than they were in December, when optimism rose but corporate treasurers wanted to wait until the new year.

The real news of the week was that the narrative of global policy rates being cut sometime in the second quarter took a hit. European inflation data was in line with – but not below – expectations while US December employment data was the same as November’s very surprising low of 3.7%. Indeed, the evidence suggests employment tightened at the end of the year, something that should bolster consumption but will do nothing to reduce robust wage growth. Low inflation data may help for this month, and possibly next, but rate cuts in March and April look as far-fetched as we thought they did at the tail end of last year.

US election: will a Trump candidacy shake markets?

When America votes, the world watches. Ever since Donald Trump announced his first presidential campaign in 2015, melodrama has given global audiences another reason to tune in. And with criminal charges piling up against the former president – but not even scratching his campaign for his party’s candidacy – the 2024 election is sure to be Trump’s most dramatic yet.

Strangely, though, that established truth does not usually extend to investors. Looking back, the 2020 election had little impact on the US stock market either before, during or after the fact. This was despite an extremely politically volatile campaign that ended in accusations of fraud and an attempted insurrection. Trump’s shock victory in 2016 initially knocked US equities, as investors feared the destabilising effects of a divisive political novice in the White House, but this downturn was recovered within days and markets later surged in what was wryly called the ‘Trump rally’.

The big question as we head into this election year is: can markets ignore US politics again? Judging by market reactions – or lack thereof – to Trump’s myriad legal troubles in 2023, it seems possible they can, but it is hard to analyse because of a lack of clarity about implications regarding market expectations. Many think that Trump gaining the Republican Party candidacy, and thereby featuring on national presidential ballots, is inevitable, but while Trump has a dominant lead over Republican rivals, his legal battles – in particular cases relating to his attempts to overturn the 2020 election result – could still sink his campaign.

That said, there is a growing feeling that, if Trump makes it onto the ballot, he will likely win in November. This is supported by his polling lead against President Biden, both nationally and in key swing states. Again, there are many unknowns here – including whether Biden himself will feature on the ballot, and whether economic improvements might rescue his dire popularity ratings before polling day. But a second term for Trump is certainly enough of a likelihood that investors and American citizens have to seriously consider it. For many Americans, the thought is extremely unpalatable, to put it mildly. There is a large group of liberal-leaning highly educated urban-dwelling citizens who think a second Trump presidency – combined with a radically conservative Supreme Court – could destroy the liberal democratic institutions that keep the republic running. That demographic tends to skew wealthier than rural less educated counterparts and, as such, makes up a much larger proportion of US domestic investors.

We have written much recently about the prolonged outperformance of the US, and whether it can continue now that its assets have become much more expensive compared to Europe and EMs. A change of market fortunes, as we argued before, needs a catalyst. Half the US fearing the death of democracy could be such an event.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below article received from Brewin Dolphin yesterday evening, which discusses the markets’ strong end to 2023.

The Santa rally continued broadly last week, albeit at a more moderate pace, after an ascent of over 15% on the MSCI World Index since late October.

The last trading day of the year was uneventful. The S&P 500 index fell 0.3% on the day, though miniscule compared to the +24.2% gain in 2023 and after nine consecutive weeks of gains. The Nasdaq 100 index had its best year since 1999 and the global bond market experienced its biggest twomonth gain on record.

It is a reminder that market volatility is normal, and that staying invested and strategically adding to investments during periods of market weakness can benefit portfolios over the long term.

To the markets. And as you can imagine, the festive period and the last trading week of the year is usually a quiet one. However, while western markets saw dull trading sessions, the Chinese stock market experienced some hefty moves in the positive direction.

Unpredictability continues in China

You may recall in our last Weekly Round-up, we wrote about how Chinese authorities were imposing strict regulations on the gaming industry that could challenge companies’ revenue models. This stance has since softened, which may have something to do with the $80 billion market rout led by Chinese tech companies like Tencent and Netease. Chinese authorities have now said they will listen to feedback from both companies and players on how to improve the new rules. But that wasn’t all. In what was seen as a further boost for the gaming industry, China also approved 105 domestic games.

Chinese stocks surged on the back of the change of tone. There was also a boost for investors hunting for bargains, as the mainland’s stock market is set for an unprecedented third consecutive year of declines.

So, are Chinese stocks sustainable in 2024?

We cannot rule out that Chinese stocks may go higher in the near term due to momentum and a reversal of extreme pessimism. And for those of us who are superstitious, 2024 is the year of the dragon, which is perceived to be a powerful and positive zodiac animal.

However, for long-term investors, the challenges that come with investing in China haven’t changed. Yes, the Chinese authorities may have sounded a bit more forgiving with the gaming sector, but that just shows the extreme and unpredictable nature of the policy setting. Policy risks and politics are making China borderline un-investible, with significant market volatility and high risk becoming the norm. The property market also remains a source of concern – especially the risk of a financial contagion.

China is not the only place sending mixed signals to investors though.

Japan – land of the rising rates?

Seen as the laggard of developed market central banks in terms of policy normalisation, the Bank of Japan (BOJ) has kept traders guessing on when it will exit the world’s last negative interest rates. It has been moving towards policy normalisation, notably with the near abandonment of yield curve control. With inflation in Japan at 2.8% and the official interest rate at -0.1%, higher rates seem justifiable; the BOJ just wants to be sure inflation is persistent.

The annual wage negotiations in spring will be crucial for the BOJ to gauge the inflation outlook, with speculation it will consider policy changes following the event. However, the BOJ’s governor, Kazuo Ueda, said this week they may not need to wait for the full results of the wage data, raising expectations that the BOJ may move before April. That said, the latest BOJ board minutes indicate that some members see no rush to exit its ultra-loose policy. The Japanese yen has reacted on these noises and Japanese stocks have displayed their usual negative correlation with the yen.

It is unlikely the BOJ will pre-commit or provide clearer guidance like the US Federal Reserve (the Fed). As a result, markets will have to live with confusing signals from the BOJ for the time being. For those of us choosing to ignore the more immediate market noises, the BOJ exiting negative interest rates is a matter of when, not if.

The Japanese bond markets have priced in a more than 50% chance of a rate hike by April 2024. If that happens, the BOJ will be tightening policy while other major central banks are cutting interest rates – potentially a key macro theme of policy divergence. This will have significant implications and present opportunities to market participants such as macro traders and asset allocators. One market dynamic will be via the yen and Japanese assets’ sensitivity to it. Another dynamic will be the cross-asset implications of higher Japanese government bond yields.

We watch Japanese policy developments closely because Japan is not only part of our regional exposure, but it has the potential to impact global markets. We have been paying particular attention to the possible knock-on impact of higher Japanese government bond yields on global bond yields. So far – and to our relief – the impact has been more on its currency rather global bond yields. This suggests the removal of the last anchor of low interest rates in Japan may not be an obstacle to the sustainability of a rally in global bonds in 2024.

2024 – the year of the soft landing?

At the end of the day, the elephant in the room for global assets remains the Fed. Like us, the Fed is watching the incoming data closely to decide on its next steps. In a week of limited economic data releases, we saw US data continue to broadly lean towards a soft landing. One notable data release was the personal consumption expenditure price indices, which are the Fed’s preferred measures of inflation. Both headline and core measures of the inflation gauge came in lower than expected in November. Notably, the headline Personal Consumption Expenditures Price Index has contracted by 0.1% month-on-month.

Meanwhile, US personal spending adjusted for inflation rose by 0.3% on the month, suggesting US consumers remain in spending mode going into the holiday season. US consumers have been supported by excess savings, resilient job market conditions and falling gasoline prices. For the labour market, the latest release of initial jobless claims figures hovered around the low 200,000s; a pace consistent with the low and stable unemployment rates seen in recent times. In summary, it is no surprise markets are feeling buoyant as we wave goodbye to sharp interest rate hikes (well, maybe not in Japan), expectations rise of the Fed pivoting to easier monetary policy in 2024, and US data points to a higher chance of a soft landing.

Please check in again with us soon for further relevant content and news.

Please see below, a short update from Copia:Capital which illustrates key recent figures from financial markets. Received this afternoon – 03/01/2024

Last Week:

Global stock markets recorded their strongest year since 2019 after markets rallied for the last two months of the year. The MSCI World Index, which is a measure of the world’s developed equity markets, finished up 22 per cent over the course of 2023. This was largely led by the S&P 500 index was up 24 per cent over the year and rose 14 per cent since October.

Asset managers launched the lower number of funds in the UK in 20 years. Morningstar reported that 397 funds were launched during 2023 which was down a quarter from the year before and much lower than the 899 launched at the peak in 2010. The drop in demand for funds came after investors shifted towards cash funds to avoid higher volatility.

There was record inflows into US money market funds in 2023 as investors were drawn to the high risk-free yields offered. Asset passed $6.3trn in US money market funds and US money market fund providers collectively earnt $7.6bn in fees over the year from these funds. The rates in money market funds have been much higher than previous years as a result of higher interest rates while the added volatility in equity markets have pushed more investors into money market funds.

Coming Up:

US Initial Jobless Claims data released, Thursday 4th January 2024 at 1:30pm.

EU December CPI data released, Friday 5th January at 10:00am.

Please continue to check our blog content for advice and planning issues from leading investment houses.

Happy new year to all! Please see the below article from AJ Bell providing their insight on the five themes to watch for investors in 2024. Received last week.

No adviser or client knows what is coming next, and whether inflation, stagflation or deflation will result from the combination of the interest rate pauses, Quantitative Tightening, pay increases, rising debt and elevated geopolitical tensions.

Basing investment strategies on just one scenario is probably not going to be good idea and portfolio construction may need to address range of outcomes, especially as we have elections to be fought (and electorates to be influenced) on both sides of the Atlantic in the next twelve months.

Carefully following five major investment themes may help advisers and clients sense which way the wind is blowing so they can try to obtain the best possible risk-adjusted returns for their portfolios, especially once they take the all-important issue of valuation into account.

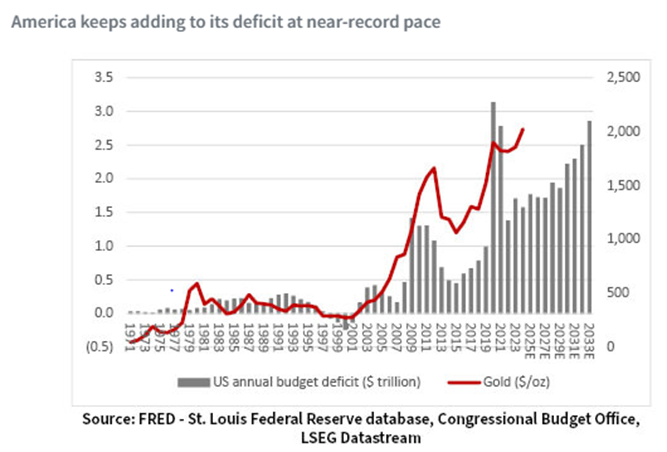

Debt

Debt-to-GDP is one barometer to watch, but according to the Bank of International Settlements it should be studied in conjunction with the percentage of tax income that is used to meet the interest costs. When that latter figure got to around 20% in 2007 (and was still rising), the financial markets buckled and nearly took the global economy with them.

FRED – St. Louis Federal Reserve database, Congressional Budget Office, LSEG Datastream

China and France are the two countries in this invidious position now, but the USA is catching up fast, as the Biden administration spends like fury on the CHIPS and Inflation Reduction Acts.

America’s latest annual fiscal deficit was $1.7 trillion, in the year to September 2023, the third-worst number on record, and the annualised interest bill has hit $1 trillion, or 20% of tax income. America cannot afford to keep interest rates where they are for long and there is a risk that the Fed has to cut rates to keep the burden manageable and take risks with inflation. This may be why gold (and Bitcoin, for that matter) are on a roll. Markets are pricing in five rate cuts from the Fed in 2024, but because inflation is cooling and growth benign, not because debt is a problem and interest costs are squeezing economic growth.

Wages

The 1970s’ inflationary outburst may have been prompted by loose monetary policy in the UK (and loose fiscal policy in the USA), followed by 1973’s oil price shock, but a vicious circle of higher pay demands, higher prices, higher pay demands, and higher prices then developed.

FRED – St. Louis Federal Reserve database, Office for National Statistics

Financial markets may therefore cheer a modest increase in unemployment, and central bankers accept it, as higher joblessness could help to put a lid on wages and inflation and thus provide scope for rate cuts. Equally, a sharp rise in the jobless rate could signal economic trouble, or at least more than is currently factored in by consensus earnings forecasts, so policymakers have a tricky balancing act here.

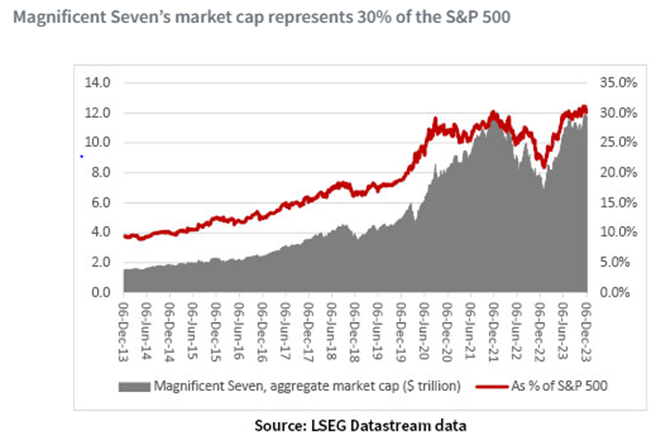

The Magnificent Seven

The stock

markets’ rally in 2023, and the return to favour of Alphabet, Amazon, Apple, Meta, Microsoft, NVIDIA and Tesla, suggests equities are pricing in an economic soft landing and a return to the low-growth, low-inflation and low-interest-rate environment of the 2010s that did so much to help the performance of long-duration assets like bonds and growth sectors, such as technology.

LSEG Datastream data

They might be right. But if they are wrong – and those five Fed rate cuts do not appear on schedule in 2024 – then the Magnificent Seven’s aggregate $11.8 trillion market cap could look exposed, for all of their dominant positions in their respective industries. Their share price and profit wobbles of 2022 showed they are not entirely immune to the economic cycle, so an unexpected recession could be one challenge. Sustained inflation could be another if it keeps rates higher than expected and boosts nominal growth from downtrodden cyclicals and value stocks. Again, only a perfect middle path may do.

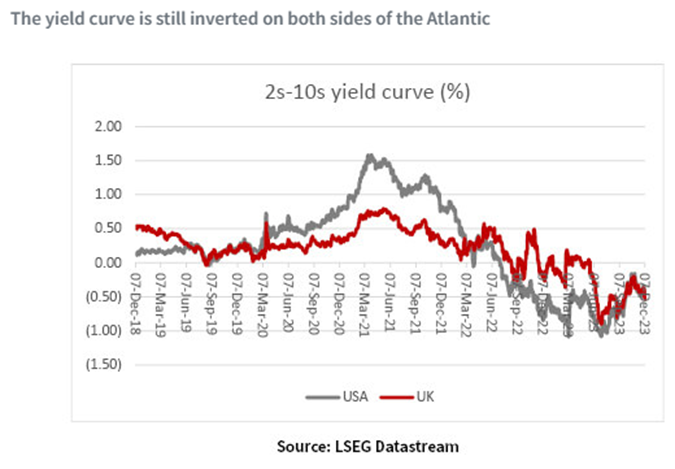

The yield curve

Bond yie

lds are falling again, but the yield curve remains inverted, whereby ten-year yields on Government bonds are lower than those on the two-year in the UK and USA. This is seen as a warning that a recession is on the way, as it means bond markets are factoring in interest rate cuts (the ten-year would usually have to offer a higher yield to compensate holders for the extra risk scope for things to go wrong over the longer lifespan of the debt).

LSEG Datastream data

It is not an infallible signal, but examples of soft economic landings are hard to find and stock markets are currently doing their best to ignore the bond market’s quite different message.

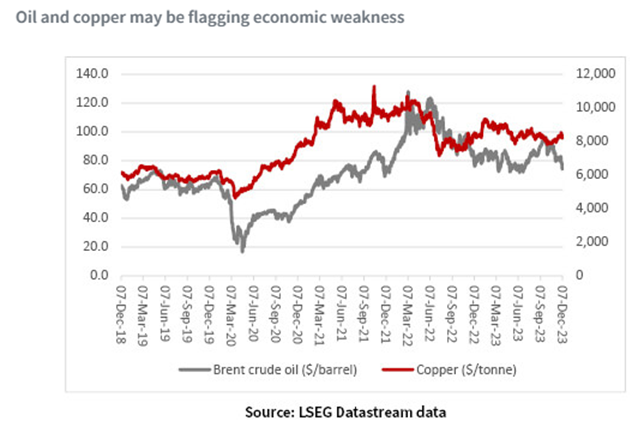

Oil and copper

If equities are pricing in a soft landing and fixed-income markets a harder one, commodity traders are even more confused. Oil’s renewed weakness may speak of recession. Copper, a reliable indicator of global economic health due to its many uses, is doing nothing. Gold looks to be fretting about debts and stagflation.

LSEG Datastream data

The messages from stocks, bonds and raw materials are therefore contradictory. But such are the globe’s debts that it seems likely central banks (and politicians) would rather play fast and loose and risk inflation or stagflation than recession and deflation. The experiences of 2007-09 and 2020-21 would suggest as much, anyway.

Past performance is not a guide to future performance and some investments need to be held for the long term.

Please check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

It has been another really interesting (probably too interesting?) year for us with markets, economies and invested assets being challenged again throughout 2023.

Although it has been a very bad year for conflicts globally and the ongoing human cost, this has not been the main focus for investors. Central bank’s policies globally has been the focus for investors. We continue to watch and interpret the data around inflation, interest rates, productivity and employment in particular. Keeping a close eye on wage inflation.

The good news is that central banks such as the Fed, the Bank of England and the European Central Bank (ECB), look like they may have stopped increasing interest rates. Interest rates may have plateaued. Markets are now looking at when interest rates might fall, and this could be as early as the second quarter of 2024 for the UK perhaps? And the second half of 2024 for the Fed and the ECB?

When interest rates do fall, we should see an improvement in investments. In J P Morgan’s view (Long Term Capital Markets Assumptions Report and webinar launch 30/10/2023), we are in a better position for investment returns than we have been for a few years, in a more normalised market.

J P Morgan state the need for a well diversified portfolio given the current outlook, with both ‘active’ and ‘tactical’ fund management.

This appears to be the broad consensus view, although as ever, we have both Bears and Bulls. A few fund managers are sitting on the fence and making provision for either outcome.

However, over the long term, history has proven that invested assets significantly outperform cash. You just need to remain invested and focus on your long-term objectives.

Business Update

We have had a busy year again here at P and B IFA. Our focus remains on servicing our existing clients and keeping them up to date with what is going on in our world and anything that might have an impact on our clients’ plans.

This year we have had significant legislative change for pensions in the Spring Budget with further clarification in the Autumn Statement and in the detail in the Autumn Finance Bill. These changes are generally good news for our clients but not without complexity.

However, from a tax point of view we continue to see reductions in allowances and stealth taxes as some allowances and tax thresholds remain frozen, and other thresholds lowered. This all results in a bigger tax take for the State.

Being tax efficient and using your allowances is more important than ever.

In addition regulatory change moves at a pace with the implementation of Consumer Duty regulations at the end of July. These changes are as ever about protecting our clients, this time they come with significant time cost to the business.

Thankfully, the use of digital technology for meetings, cutting out a lot of travel time, has allowed me to deal with the legislative and regulatory changes without working 24/7, although I don’t think I’ve ever worked harder.

We continue to work on the business and I’ve taken input from several external consultants over the year as we continually strive to offer a great service to our clients. This is to the benefit of our clients and our staff. I’ll keep you posted on any developments.

Consumer Duty regulations apply more broadly than to just IFAs like ourselves. The good news here is that we hope that the new regulations will help us receive a better service from providers, life offices and platforms etc. Now we spend too much time as the buffer working on behalf of our clients. This year we have had to educate the staff at life offices and platforms about the new pension legislation changes, so that they can understand our instructions on behalf of our clients.

It was worthwhile in the end. From a pension legislation point of view, we are in a better place than at the start of 2023.

Summary

It has been a busy year for all of us, but I think we are in a better place now. Things have moved on for economies, markets and invested assets and I feel like we are making progress, although risks remain, and volatility could continue for a while.

We have improved pension legislation too, that is good news and should help us keep our pension funding at the right level as for most of us it is extremely tax efficient.

Compared to this time last year, I’m feeling more positive about the new year. It won’t be straight forward, but I think we are starting to see improvements to the outlook.

Politically it will be an interesting year, hopefully with a normal democratic process, particularly in the US.

Wishing you and yours a healthy, happy and prosperous New Year. I’d love to see an outbreak of peace and goodwill globally.

Please see below an article published by Brooks Macdonald which was received yesterday afternoon and outlines their outlook for markets in 2024:

Glass half empty or full? Outlook 2024

As we near the end of 2023, we are at a crossroads for both economies and investments. During 2023 sentiment has oscillated between two different investment scenarios, the glass-half-full camp, and the glass-half-empty camp. The challenge is to construct portfolios while recognising that either scenario could occur. Given the uncertainty which prevails, we believe that maintaining a balance is key.

2023 has been a year in which investment markets have encountered cross winds. On the positive side, equity markets have benefited from a new age in technology, driven by generative artificial intelligence (AI). At the same time, geopolitical risks have heightened with Russia’s ongoing invasion of Ukraine alongside the conflict in the Middle East between Israel and Hamas. Furthermore, China-US relations remain fraught, despite recent efforts to improve them.

Inflation is the key focus for policy makers and with interest rates clearly in restrictive territory, the glass-half-empty camp is waiting for the full impact of higher interest rates on consumers and companies. At the same time, any worsening of the situation in the Middle East or tightening of supply by the OPEC+ members would lead to a rise in the oil price, causing further upward pressure on inflation.

The glass-half-full camp believe that given labour markets remain tight, wage growth will be robust. In the US, many consumers still have post-pandemic savings to spend and unlike in the UK, for example, have 30-year fixed rate mortgages meaning they are insulated from the recent rate rises.

The key question for both camps is whether consumers and companies will remain solvent while policy makers wait for inflation to fall back to the Central Banks’ targets.

How did we get here?

After a tough 2022 when both equities and bonds posted negative returns, 2023 has seen a recovery, at least in equity markets. At the time of writing, government bonds are still in negative territory, despite the fall in yields (and corresponding rise in prices) seen since the peak of mid-October. The MSCI All Country World Index is up 10.4% in total return, sterling terms. However, the same index adjusted on an equal-weight basis (where each stock has an equivalent weight in the index, removing the dominance of so-called ‘mega-cap’ stocks), is down -1.4%. This difference highlights the impressive performance of a small number of technology-related names which are perceived to be beneficiaries of AI.

The age of Generative AI

The new age of AI started with the launch of Chat GPT in November 2022. Chat GPT is what is known as a large language model-based chatbot developed by Open AI, enabling users to generate media (be it text, code, pictures and more). By January 2023 it had over 100 million users per month and was the fastest growing consumer software application in history. Investor attention turned to companies believed to be the enablers of AI, particularly those focused on designing the necessary

The picture in Euro Area and the UK is less robust, with the IMF forecasting growth of less than 1% in 2023 and an only modest recovery in 2024.

semiconductors: Nvidia, the US chip designer, has risen by comfortably more than 200% year to date. The key question is the size of the productivity gains across the broader economy. The US National Bureau of Economic Research looked at a staggered introduction of a generative AI-based conversational assistant using data from over five thousand customer support agents and found that access to the tool increased productivity, as measured by issues resolved per hour, by 14% on average. Clearly gains of this magnitude will help mitigate the effects of higher interest rates and wage costs.

Corporate earnings growth remains robust

After the boost from the post pandemic recovery, corporate earnings growth expectations are lower but still in positive territory. Data from Factset indicates that companies are delivering better than expected earnings-per-share numbers at an historically high rate. Looking ahead to 2024, current consensus estimates point to an expected annual US company earnings growth rate of over 11%. The operating environment is also becoming more favourable: post pandemic supply chain disruptions have ceased and trade volume growth of 3.3% in 2024 is expected, compared to 0.8% in 2023*.

Economic growth picture still mixed

Central Banks continue to face the challenge of bringing down inflation while avoiding a recession. They also must ensure financial stability and avoid a situation such as the failure of regional US banks in Q1 2023. The three main regional drivers of growth are the US, Europe (including UK) and China. The US reported annual real GDP growth of 4.9% in Q3 2023, well ahead of the Fed’s own estimate of long-term real GDP growth of 1.8%. Growth in China remains healthy, with the IMF forecasting China’s real GDP growth in 2024 of 4.6%.

However, the picture in Euro Area and the UK is less robust, with the IMF forecasting growth of less than 1% in 2023 and an only modest recovery in 2024. These differences illustrate the importance of using an asset allocation framework that can adjust for regional settings.

Investors face three outcomes for economic growth. First, a hard landing, which is a contraction in economic activity, sharply rising unemployment, and a collapse in consumer spending. Second, a soft landing, with a gradual slowing of growth, a recession avoided and a moderate rise in unemployment. Third, no landing, with economic growth continuing at the current rate. The first outcome would imply we should reduce equities and add to longer duration bonds, given the likelihood that interest rates would then be cut significantly. If the third were to materialise, we should add to equities and reduce more defensive assets such as fixed income. Over the course of the year, the soft landing outcome has become more likely but far from certain, so we aim to maintain a balance within portfolios for investors.

Bonds: income is back

Over the course of the past two years, the rise in bond yields has meant that bonds can once again provide a counterbalance to other asset classes within portfolios. This increase in yields available from longer dated bonds gave us the opportunity to increase slightly the duration within the bond portfolios, thereby locking in higher yields. We believe it is too soon to increase duration significantly though, given the risk that inflation may persist for longer. Within corporate bonds we continue to prefer higher quality investment grade bonds over the more speculative high yield, as we believe the additional yield available does not adequately compensate us for the additional risk of the latter.

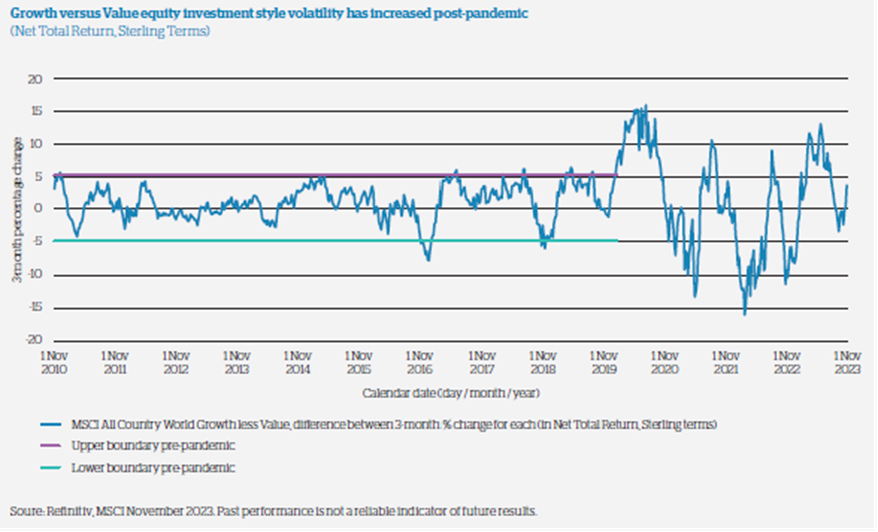

The equity barbell remains in place

The graph below shows how, since the pandemic, the style leadership of the equity market has changed more frequently and become more pronounced. For this reason, we have implemented a barbell approach in the equity portfolios, whereby we aim to achieve an equal weighting of both value and growth investment styles. Given the range of possible economic scenarios together with current heightened geo-political risks, the barbell approach remains. Despite this balance, we continue to take conviction views on a geographical basis, emphasising the different investment styles through our core equity and thematic exposures.

Conclusion

As we weigh up the investment outlook, the challenge for asset allocators is how to take a calculated position to keep exposure to more than one economic scenario materialising. There is currently insufficient visibility for us to back a single sustained outcome. Instead, staying invested but keeping balance continues to be our goal.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

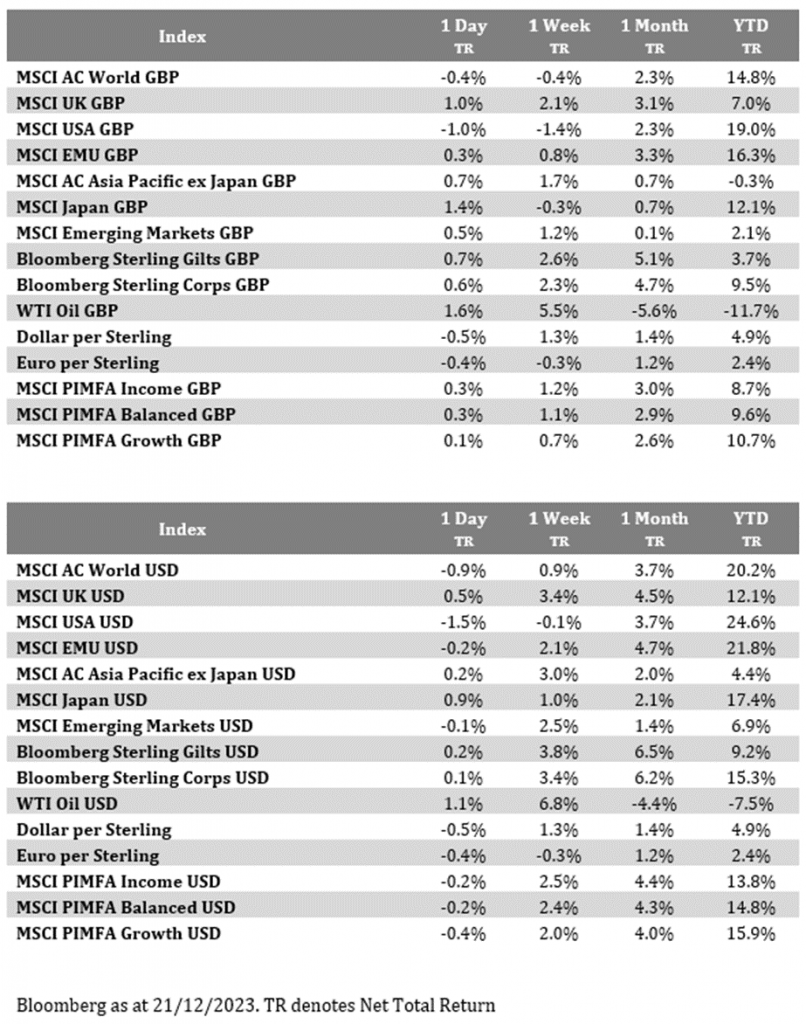

Please see below, Brooks Macdonald’s ‘Daily Investment Bulletin’ which provides a brief analysis of the key factors currently affecting global markets. Received this afternoon – 21/12/2023

What has happened?

The relentless march higher of US equity markets was interrupted late on Wednesday with the headline index off c. -1.5% on the day. The catalyst is not clear however after markets have traded solely in one direction for several weeks, regardless of central bank speakers or the incoming data, a snap back is arguably warranted.

Central banks

Despite the negative tone within equity markets, bond markets continued their rally with the US 10-year Treasury yield falling to 3.85% while the 2-year yield is now just 4.33%. Investors continued to ramp up their expectations of imminent interest rate cuts with bond markets now implying a 92% probability of a cut by March and 1.5% of cuts next year in totality. One of the factors that may have caused the sharp sell-off late yesterday is the growing gulf between the Fed’s dot plot of interest rate expectations and what is priced into the market.

Inflation

There was good news for the UK yesterday as headline CPI inflation fell more than the market was expecting to 3.9%. This was 0.4% below expectations but the Core CPI number, which excludes food and energy, saw an even more dramatic move lower, coming in at 5.1% versus 5.6% expected. Investors increased the number of interest rate cuts they are expecting from the Bank of England in 2024 and the gilt yield curve rallied. Over in Germany, the Producer Price Index inflation numbers showed significant deflation with the index contracting by -7.9% year-on-year compared to -7.5% expected. This helped European bond markets share in the rally seen in the US and UK.

What does Brooks Macdonald think?

On top of the positive inflation stories yesterday, the Conference Board’s US consumer confidence showed a resilient US consumer. Despite this, equities fell quite substantially at the end of the day which suggests a degree of investor fatigue around quite how quickly the market outlook has shifted from bleak at the end of October to unashamedly bullish by the end of the year.

Please continue to check our blog content for advice and planning updates from leading investment managers.

Please see below article received from Evelyn Partners this afternoon, which provides an economic update as we approach Christmas and the end of 2023.

What happened?

UK November annual headline CPI inflation was reported at 3.9% (consensus: 4.4%), its lowest pace in over two years, versus 4.6% in October. In monthly terms, CPI fell 0.2% (consensus: +0.1%), compared to remaining flat at 0% in October.

November annual core CPI (excluding food, energy, alcohol and tobacco) was 5.1% (consensus: 5.6%), versus 5.7% in October. In monthly terms, core CPI was -0.3% (consensus: +0.2%), versus 0.3% in October.

What does it mean?

Today’s encouraging inflation print confirms the continuation of the downward trend in inflation. Just over a year on from headline CPI peaking at 11.1% in October 2022, it has since decelerated by over 7% points, with much of that deceleration in the headline rate coming from lower energy prices in the transport (i.e. fuel) and housing and household services (i.e. gas and electricity) categories. What was even more promising was the downward movement in core inflation, which has decelerated to its lowest rate since January 2022.

As it stands, Brent crude oil prices are now down roughly 4% for the year despite heightened geopolitical risk in the Middle East and OPEC+ output cuts. This reduces the risk of upside in retail petrol and diesel fuel prices. This weakness in oil prices has been reflected in the CPI basket for transport which decelerated by 1.7% in November. On an annual basis this segment of the economy is now exhibiting deflation, with the 12-month inflation rate turning negative.

Looking elsewhere in the divisional breakdown, goods inflation has now decelerated to 2.0% on an annual basis. While services, although slowing, remains more resilient at 6.3% for the last 12 months.

Food and non-alcoholic beverages continue to put pressure on the wallets of households, with this segment exhibiting the highest monthly inflation rate for any category at 0.3% for November. On an annual basis, prices in this segment have risen by 9.2%.

Bottom Line

With both headline and core CPI inflation slowing at a faster rate than expected in November, this should reassure policy setters at the Bank of England that high interest rates are having the desired effect of materially decelerating inflation. The Monetary Policy Committee should now be able to focus on when to cut rates, rather than if additional tightening is required. Money markets are currently expecting these interest rate cuts to materialise in the second quarter of 2024.

Please check in again with us soon for further relevant content and market news.

Please see below article received from Brewin Dolphin yesterday afternoon, which comments on US inflation figures, interest rate decisions from the Federal Reserve and Bank of England, and Chinese economic data.

The glass is very much half full for the investment world at the moment, with good news being taken as such and bad news being shrugged off.

Continuing the theme of the last two months, gains have come from the anticipation of a more benign inflationary outlook. European inflation numbers have seemed to endorse that view, dropping quite sharply over the last few months. US inflation has been more nuanced; data released last week were broadly in line with expectations, but the underlying composition of inflation could give cause for concern.

US core inflation picked up during November to a pace that would be inconsistent with the Federal Reserve meeting its inflation target. It is well understood that core inflation is heavily influenced by shelter, and shelter inflation will reflect rents and changes in house prices with a lag, representing the time it takes for tenancy agreements to be renewed. That means there should be some disinflation to come from the housing slowdown that has already occurred. More recently, the impact of housing on the consumer price index (CPI) has become clouded. Demand for new housing seems depressed but house prices have been rising for the last few months. The recent sharp decline in bond yields means that US mortgage rates have been declining, which ought to offer further support for house prices and have some knock-on effect for shelter CPI.

Moreover, the Fed looks beyond core CPI these days to try and gauge underlying price pressures. While core inflation strips out volatile food and energy prices, so-called ‘supercore’ inflation comprises services inflation excluding energy and housing. This measure should reflect the general level of inflationary pressure driven by the balance of the labour market. It accelerated slightly this month and has been running ahead of the Fed’s implied inflation target for the last four months.

Interest rates

With this backdrop, the Federal Reserve announced its latest changes to monetary policy. Broadly, policy was left unchanged, as had been universally expected, but the press conference and statement surprised the market by being more dovish than anticipated. The Fed cut its inflation expectations and raised its growth expectations for what is left of 2023. More meaningfully, it also lowered the expected interest rate at the end of 2024 to a level that implies three interest rate cuts will take place over the year. This comes at a time when the Fed is also expecting inflation to remain above target (albeit only modestly). It is surprising the Fed would endorse rate cuts whilst seeming to tolerate above target inflation. For context, market-based interest rate expectations moved lower and now imply nearly six interest rate cuts over the next twelve months.

Labour markets are the key determinant of the inflationary environment but are often observed to be lagging indicators. By the time the unemployment rate has started rising, it has often developed a momentum that makes it difficult to stop. The fear of this, at a time when Fed chairman Jerome Powell believes policy is “well into restrictive territory”, will be the motivation for this dovish tilt.

One factor that has been helpful in curtailing inflation in the US is the relatively benign performance of wages. Wage growth peaked around the turn of last year in America but has not yet done so definitively in the UK or eurozone.

Europe

That discrepancy probably motivated the Bank of England (BoE) in its more hawkish tone. Three Monetary Policy Committee (MPC) members voted to raise interest rates again, believing there was evidence of persistent inflationary pressure. They were outvoted and policy was left on hold.

The MPC decision came after the release of quite weak monthly gross domestic product (GDP) data on Wednesday, on top of Tuesday’s relatively poor labour market data. BoE governor Andrew Bailey took a more predictable line, emphasising the battle to contain inflation was not yet won and the Bank would “take the decisions necessary to get inflation all the way back to 2%”.

All central banks become heavily motivated by the latest economic data at potential turning points in interest rate cycles. The data for the UK does seem quite weak, whereas there are tentative signs of the European economy recovering some momentum. This morning saw a slight setback in the purchasing managers indices for Germany and France. This was mirrored by the UK’s ailing manufacturing sector but bucked by the UK services sector, which expanded faster for a fourth consecutive month.

Meanwhile, in the east…

A lot of data was released last week detailing the Chinese economy. There are some signs of recovery, with annual growth numbers like the 10% expansion in retail sales seeming quite healthy. This is somewhat illusory though, as China was in lockdown this time last year. The thorn in the side of the Chinese economy remains the property market. Data released today showed the continued decline in new home prices. It comes after the conclusion of the Central Economic Work Conference (CEWC). The post-meeting communique signalled some measures would come in to try to bring relief to the Chinese economy. But the promise was vague and modest, suggesting perhaps a couple of interest rate cuts and a further easing of required reserves at banks (which would enable them to lend more to the economy).

China maintained its growth target of around 5%, which sounds ambitious given the weakness of the economy. But, again, this reflects the fact that last year, China was in lockdown, and so growing 5% from that depressed level should be neither taxing nor impressive.

Please check in with us again soon for further relevant content and market news.