Please see the below article from Invesco detailing their thoughts on the latest bout of market volatility. This article is from their Multi Asset team on the reasoning behind the ‘global sell off’:

Global stocks have fallen sharply from their all-time highs in the last few weeks.

It appears we are on the brink of that next broad-based 10% decline as the economy weakens, the Federal Reserve passed on lowering interest rates at the July meeting and investors continue to lighten their holdings in expensive tech stocks.

It is hard to say with precision how long this bout of volatility will last for, and even though market participants appear to have quickly moved from pricing an overly rosy picture to an overly negative one, we think that at this stage, investors shouldn’t necessarily throw in the towel.

The current state of play of financial markets

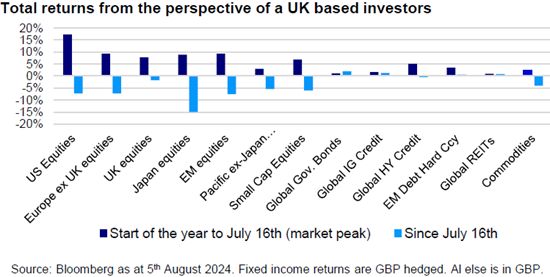

Risk assets performed strongly since the start of the year, driven by hopes for a goldilocks economic scenario and a rush into US tech stocks fuelled by enthusiasm for artificial intelligence technology. At their peak on July 16th, global equites were up 14% in GBP terms.

In the last few weeks however, sentiment started to shift, with global equities giving back half of their year-to-date gains. Bonds on the other hand have offered multi-asset investors some reassurance as this more classical growth-driven sell-off has seen government bonds cushion part of the blow in equities by moving in the opposite direction.

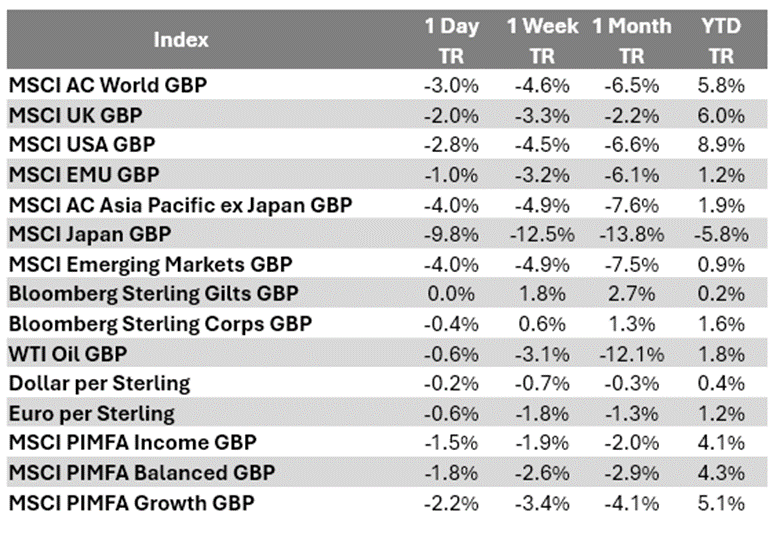

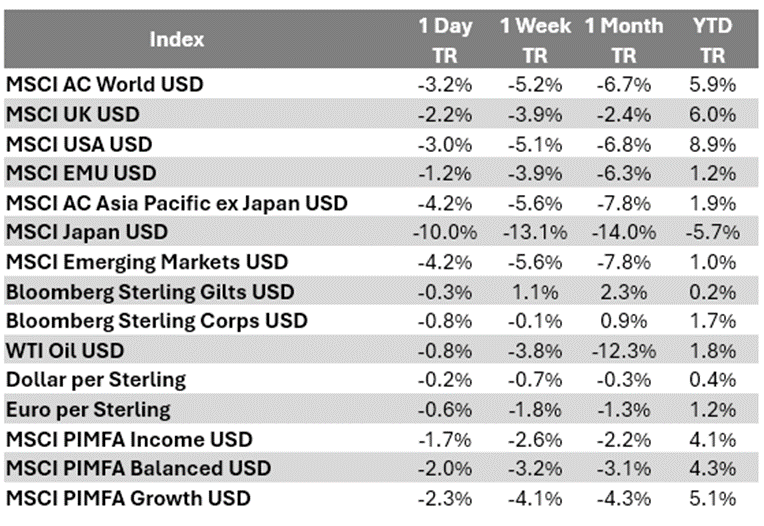

Notwithstanding the alarming moves, investors should note that most markets are still up for the year as shown below.

What has triggered the sell-off?

It’s hard to pin this on any single event. Below we list what we think are some of the key culprits.

1. Recession fears?

After several months of stability, economic data around the world has started to soften with the most noticeable decline being in the US – evidenced by last Friday’s unexpected 114k new jobs added (lower than the 215k average of the last year) and the unemployment rate jumping to 4.3%, the highest since October of 2021. Although that’s not in and of itself an unhealthy unemployment rate, its sudden march higher has raised concerns for a potential recession.

2. Fed too slow to act?

Post the 2022 pull-back, equity markets have been unstoppable, buoyed by falling inflation and growing expectations of rate cuts, particularly from the US Fed. But during last week’s meeting, the Fed didn’t cut rates as many had hoped triggering fears that the Fed may be too late to act before a slow in hiring turns into rampant layoffs.

3. AI trade losing steam?

After benefitting from stellar returns, investors started to unwind big positions in the likes of Apple, Nvidia, Microsoft, Meta, Amazon, Alphabet and other tech stocks. Warren Buffet, Berkshire Hathaway’s CEO for instance recently sold half of Berkshire’s stake in Apple, which many see as a troubling sign for the health of the tech sector. Because these companies make up an enormous chunk of the overall value of the S&P 500, when investors sell off tech stocks, that has a massive detrimental effect on the broader market.

4. Unwinding of the Japanese yen carry trade

While less structural in nature, the mayhem that swept across world markets was amplified by a market strategy known as the “carry trade.” Japan’s benchmark Nikkei 225 plunged 12.4% on Monday and markets in Europe and North America suffered outsized losses as traders sold stocks to help cover rising risks from investments made using cheaply financed funds borrowed mostly in Japanese yen. Markets recovered much of their losses on Tuesday. But the damage lingers.

More common than you think

Drawdowns (a decline of less than 10%), are always coming. Since the early 1980s, there has been a greater than 5% drawdown in the S&P 500 Index in every year but two (1995 and 2017). Even in this year, which had felt relatively benevolent until the past few weeks, the S&P 500 Index experienced a 5% drawdown in April before climbing to an all-time high in the middle of July.

On the other hand, corrections (declines of greater than 10%) happen less frequently. Corrections typically don’t just emerge out of nowhere. Often, they’re the result of policy uncertainty and/or surprising weakness in economic activity. The market has currently gone since Nov. 2, 2023, without an official correction, representing a 188-day period of a resilient economy and declining inflation.

Reasons to remain constructive as the dust settles

We appear to potentially now be on the brink of that next 10% decline as the economy weakens, the Federal Reserve passed on lowering interest rates at the July meeting and investors continue to lighten their holdings in expensive tech stocks.

It is hard to say with precision how long this bout of volatility will last for, and even though market participants appear to have quickly moved from pricing an overly rosy picture to an overly negative one, we think that at this stage, investors shouldn’t necessarily throw in the towel.

Growth slowdown is not the same as recession

In our opinion, this macro backdrop is consistent with an incoming deceleration but not indicative of imminent recession risks given:

- Ongoing resilience in consumer and corporate balance sheets

- The labour market is cooling, but not falling off a cliff

- Banks do not appear to be tightening lending standards significantly

- There does not appear to be significant excess in the economy

As of today, growth is solidly in positive territory on a global basis, with developed markets growing between 1-2% and consensus expectations signalling similar growth rates over the next two years.

The Fed should join the rate cut party soon

Last week, the Fed kept its main interest rate between 5.25 per cent and 5.5 per cent. However, the combination of a slowing jobs market, cooling inflation and the negative market reaction should lead the central bank to finally act. Historically, markets tended to perform well in easing cycles that were not associated with recessions. All eyes are therefore set on the Fed’s next meetings scheduled for September, November and December.

Tech stocks may be falling out of favour, but we don’t think this is their end

Tech stocks are still trading at lofty valuations, and while this may temper future upside potential, we don’t think investors will completely shy away from the sector. To evaluate the sustainability of their performance, investors should eschew reliance on charts of share price performance and focus instead on business fundamentals and valuations. While not unassailable these companies have large moats, very strong balance sheets, and many have revenue streams that are far less cyclical than tech companies of the past.

Please continue to check our blog content for advice, planning issues, and the latest investment, market and economic updates from leading investment houses.

Andrew Lloyd

08/08/2024