Please see below an article from Brewin Dolphin detailing their views on recent market data and events which was published yesterday (09/07/2024) and received this morning:

Janet Mui, Head of Market Analysis, discusses how markets digested the news of Labour’s landslide election win, France’s hung parliament, and the latest U.S. economic data.

It was politics that occupied the news headlines last week. And while it’s had some impact on markets, the UK general election was met with market apathy given that the result had been expected – that’s despite a historic seat gain for Sir Keir Starmer’s Labour Party.

This result is popular with the markets, as Labour is seen as a more functional governing party compared to the years of infighting, division and leadership contests under the Conservative Party.

A strong majority for Labour means an endorsement of the party’s leader and policy agenda. In Labour’s case, its commitment to avoid a repeat of Liz Truss’s infamous brush with fiscal mortality means a likely period of economic orthodoxy is welcome.

In France, by contrast, a majority for Marine Le Pen’s National Rally Party over the weekend would’ve been a concern for markets because her policy agenda seems fiscally cavalier. However, last week, it seemed increasingly likely that National Rally wouldn’t achieve a majority, causing French assets to perform relatively well. Indeed, National Rally came third in the second round of voting on Sunday. Left-wing alliance New Popular Front won 188 seats while President Emmanuel Macron’s liberal coalition Ensemble came in second with 161 seats.

The strength of Labour’s performance stands in contrast to a general tide of increased preference for more socially conservative policies. UK voters don’t necessarily have a different perspective on what’s important, but they do have a different political system, and this victory for Labour had more to do with the fracturing of the rightwing vote than a triumph of the left.

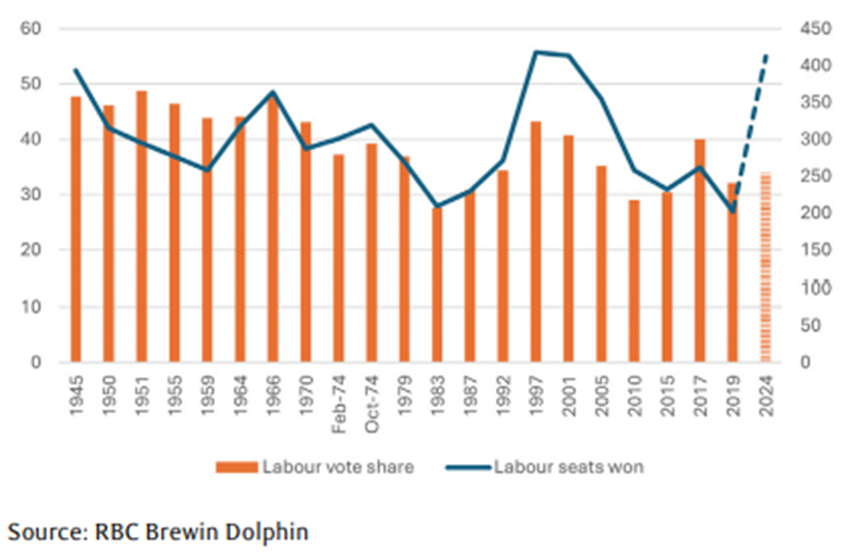

This was Labour’s third highest seat haul, but its sixth lowest share of the popular vote, since 1945. Its vote share was up less than 2% on the 2019 election, in which Jeremy Corbyn’s Labour was trounced by Boris Johnson.

The splitting of the right-wing vote across the Conservatives and Reform UK was instrumental in delivering huge seat gains for Labour and the Liberal Democrats. Also contributing towards Labour’s success was the decline in the Scottish National Party’s vote share.

With a Labour majority always seeming the most likely result, the market was apathetic, with no discernible movement in bonds or currency markets.

Within the FTSE 100, the housebuilders were amongst the leaders. They are perceived to benefit from Labour’s plan for a blitz of planning reform, which will enable more housebuilding. The policy will doubtless be unpopular with many existing constituents, but a large majority helps quell any stirrings of rebellion.

Is a change on the cards for the Democrats?

The biggest political headlines were drawn by U.S. President Joe Biden, as he has been fighting to retain his position as the presumptive Democratic nominee to contest the presidential election this November.

A few Democrats have finally started to break cover and call for Biden to stand down. By convention, a sitting president is not challenged when seeking re-election, but Biden’s advanced years have caused many to question the wisdom of him standing.

The issue has been that nobody else has been seen to stand a better chance of beating Trump than Biden, but that seems to be changing with head-to-head polling suggesting that Vice President Kamala Harris may have a better chance than Biden. She would be the easiest replacement candidate for the party as she was already Biden’s stated running mate. Prediction markets and betting odds seem to suggest that Harris may even be considered more likely to face the voters.

Bond markets would likely look fondly on a change in Democratic candidate now that Biden’s chances have diminished so much. They perceive Trump as a malign inflationary influence.

However, in reality, the economic consequences of a Trump presidency are more complex than that, depending on whether his party would also control the Senate and House of Representatives (all of which are quite possible).

Is economic momentum slowing?

It’s easy to get distracted by the politics but, of course, the more tangible factor affecting markets is economics. Last week’s business surveys from across the globe painted an ambiguous picture of the economic outlook.

Manufacturing activity remains muted although the low level of inventories should reassure us that downside is limited. Services sector activity continues to expand but does so at a slower rate than in May. There were confusing irregularities in the data, making it difficult to see a distinct trend.

In general, the economy looks to have lost some momentum compared to the first quarter. What’s consistent is evidence that price growth is slowing.

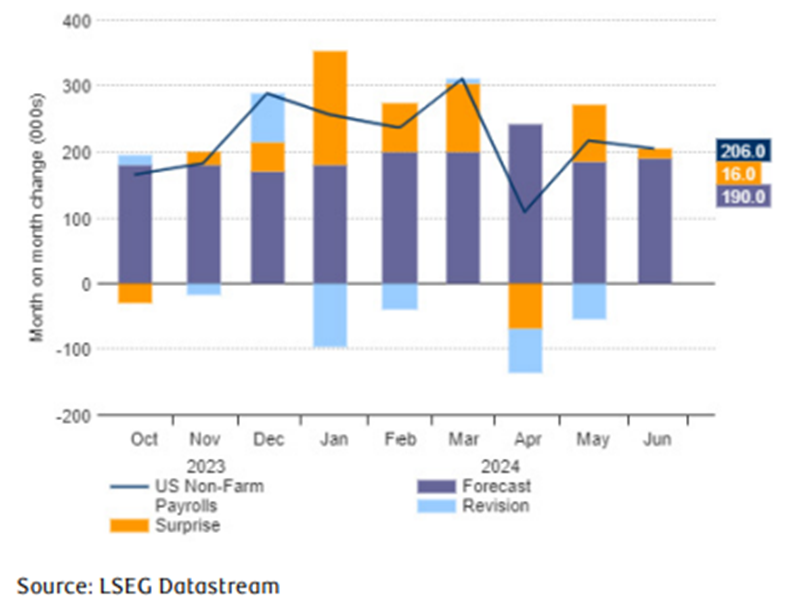

The book end to last week was Friday’s U.S. employment report. Headline employment growth was slightly ahead of expectations, but there were plenty of caveats to threaten the positive headline.

The unexpected jobs growth came from government hiring, with the private sector slower than expected. The unemployment rate ticked up and this has been moving higher in a way that could be consistent with a recession. However, the moves have been about increasing labour supply, rather than job losses or a slowdown in hiring. April and May’s jobs growth was also revised down to a more modest pace.

Finally, wage growth slowed on an annual basis. Taken as a whole, this was a labour market report that will help the Federal Reserve to build the case for rate cuts. If services sector inflation (excluding housing) is reasonable in June, the case for a September rate cut will have become very compelling.

Please continue to check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Carl Mitchell – DipPFS

10/07/2024