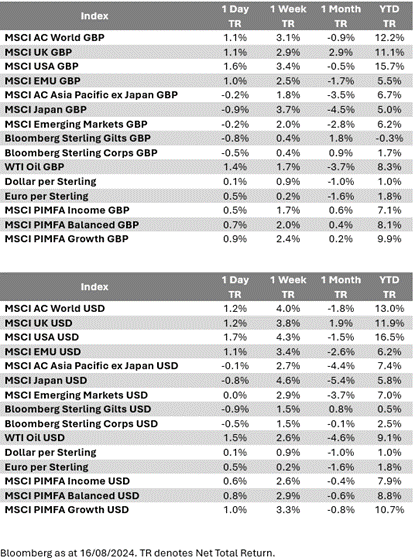

Please see the below article from Brewin Dolphin, providing a brief analysis of the latest movements in global investment markets. Received last night – 20/08/2024

Japanese political drama

A lot of economic data and a few key earnings reports were expected last week. What was unexpected, although not entirely surprising, was the announcement from Japanese Prime Minister Fumio Kishida that he won’t take part in the race to become party leader in September, effectively resigning the premiership.

Kishida has been dogged by scandal this year, but still had a relatively long tenure of nearly three years; his predecessor served just over a year as prime minister, which is not unusual in Japan.

Kishida’s replacement will be important. Currently, the most popular of his potential replacements is former Defence Minister Shigeru Ishiba. He has expressed a desire to see Japanese monetary policy normalised, which seems the most pronounced threat to the Japanese economic status quo.

At the time, only Takayuki Kobayashi, the Minister of Economic Security, had declared his candidacy and he has yet to comment on Japanese monetary policy. There’s still plenty of time for other candidates to join the race.

Yields rose and the yen rallied upon Kishida’s announcement, possibly because of Ishiba’s stance. Nevertheless, the week saw strong performance from risk assets and Japanese equities. That could be because last week saw information that could support or refute the case against the U.S. economy. Is it plunging into recession, or is the consumer just taking a breather?

Overall, the data was reassuring. This meant less pressure for sharp interest rate cuts in the UK and it may even have rekindled the carry trade.

U.S. inflation

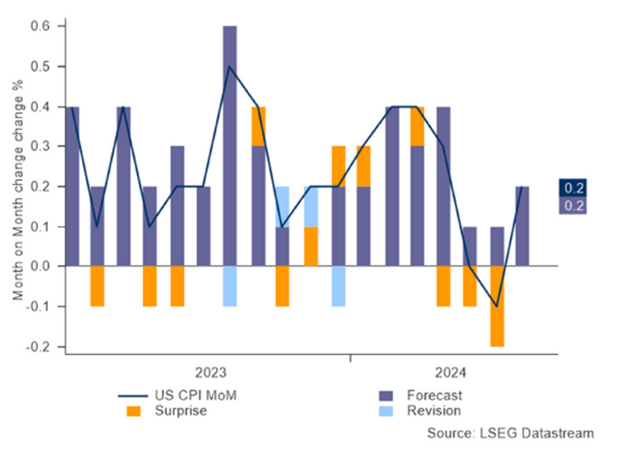

The U.S. consumer price index (CPI) was the most important monthly data for a long time, as inflation remained the main source of angst for investors. But weak price growth in May and June seemed to help investors channel their neuroses elsewhere.

Inflation’s certainly not the demon it was. Prices rose at 2.9% over the last 12 months, which is still too high, but well down on the 9% rate reached in June 2022.

Although headline inflation hasn’t dropped much in the last year, one of the bright spots about this month’s report was that it dropped below 3% for first time since June 2022. Since then, inflation has been stubborn and is unlikely to fall much faster over the coming months.

An alternative perspective

Investors, however, have learnt to look beyond the headline CPI rate. The Federal Reserve’s (the “Fed”) preferred inflation gauge is the personal consumption expenditure price index (PCE), but CPI gets the headlines because it’s released earlier in the month.

In terms of the differences between the two, CPI is increasingly reflecting increases in rental costs. For example, rent makes up 38% of the CPI basket and contributed 1.8% of the 2.9% rate.

Rental costs accelerated this month, which was very disappointing, but it’s not something to be worried about. We can say with enormous confidence that they’ll fall in the coming months, as the CPI basket, which measures one sixth of the rent revisions of the overall inflation basket, lags the timelier All Tenants Regressed Rent Index. The latter has been slowing rapidly and implies that the path of rental CPI normalisation has further to run.

To reflect the part of the economy that can actually be influenced by monetary policy, the Fed has placed more emphasis on a measure called ‘core services excluding rent’. This seems the most important number to take away from CPI, as it will influence how the Fed considers changing interest rates. When core services excluding rent declined in May and June, it suggested that inflationary pressures had finally been tamed. But having stripped out many of the volatile prices, what’s left really ought to be quite a stable number, so two months of declines seemed unsustainable.

This month, these prices rose by 0.21%, which would be consistent with a 2.5% annual rate. 2.5% CPI is only just above the equivalent 2% rate for PCE, so things are definitely moving in the right direction. These CPI numbers would not dissuade the Fed from cutting interest rates in September.

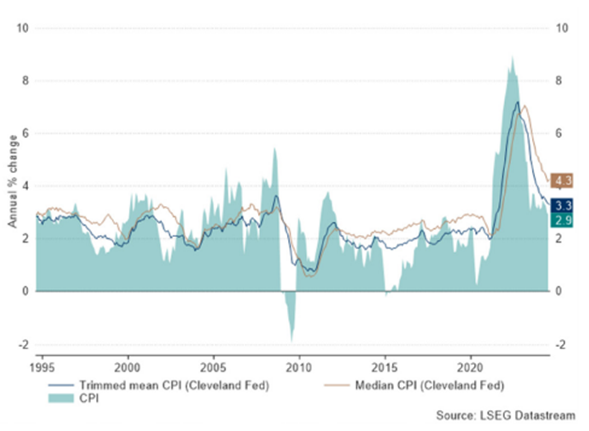

The only warning sign for policymakers here would be the persistence of alternative measures of CPI. Measuring price increases without the most volatile elements can be done by excluding food and energy (to give ‘core’ CPI), or it can be done by literally excluding the most volatile elements, no matter what they are (the ‘trimmed mean’ CPI) or by only measuring the median price increase each month.

These approaches show that inflation is slowing, but remains above the headline rate of inflation, and the most recent month actually saw prices increase. And that belies the true message of last week’s CPI report: that inflation remains above target, but not far enough above target to prevent the Fed from cutting interest rates when it meets in September.

The Fed believes rates are currently restrictive and can see a change in consumer behaviour, so it has become very concerned about the economy being too weak, and less concerned about inflation being too hot. Expectations that rates might be cut twice look wide of the mark though.

The UK economic recovery continues We also had the UK inflation report last week. It was biased by some volatile numbers, but again, the alternate measures of CPI, for example the median CPI, show that inflation hasn’t normalised yet.

In the UK, of course, interest rates have already been reduced. There’s also less evidence of the economy slowing.

Earlier in the week, it did seem as if there was a reducing number of job vacancies, but an apparent reduction in payrolled employees a few months ago has turned out to be a misestimate, which has been corrected by revisions.

The employment data are acknowledged as being unreliable due to low response rates to surveys. Fundamentally, it seems unlikely the labour market is particularly weak, because the economy has been picking up speed. Retail sales announced Friday morning reflected this, and the slowdown in inflation the UK has experienced so far, coupled with increases to the National Living Wage and the cut in National Insurance, have been wind in consumers’ sails.

What do U.S. retail sales tell us?

Flipping back to U.S. retail sales, and these were more upbeat than anticipated. We’ve heard a downbeat story from many retailers during earnings season, and this broadly continued with Home Depot confirming customers have spent more on wares to spruce their homes up over those required to perform major renovations.

Walmart saw similar focus on value from customers. It’s difficult to square with the official retail sales numbers. Perhaps the message that some retailers have seen things pick up a little at the start of August is the most telling.

What’s next?

The Democratic National Convention kicked off on Monday and will continue until Thursday. The conference began with President Joe Biden and former secretary of state Hillary Clinton endorsing Vice President Kamala Harris in November’s presidential race. While it’s unusual to see policy surprises at the convention, the change in nominee means the Democratic agenda is still being put together. If that does lead to any policy announcements, they’ll come later in the week.

Tim Walz, the current Governor of Minnesota and somewhat surprising vice-presidential nominee, will speak on Wednesday, while current Vice President and presidential nominee Kamala Harris will speak on Thursday.

This week will also see the publication of meeting minutes from the European Central Bank (ECB) and the Fed, as well as provisional purchasing managers indices for August.

Fed Chair Jay Powell and Governor of the Bank of England Andrew Bailey will both speak at the Kansas City Fed’s Jackson Hole Economic Symposium, which takes place between 22 and 24 August. The symposium features keynote speeches from prominent economists and policymakers. These speeches often provide insight into the Fed’s monetary policy thinking. They can also move financial markets and offer an opportunity to hear from some of the world’s most prominent central bankers.

Bank of Japan Governor Kazuo Ueda has a prior engagement and will instead attend a special session at Japan’s parliament to discuss the 31 July rate hike. This took the market by surprise and was seen as a significant contributor to the sharp sell-off in Japanese equities that took place thereafter. It will be a busy week for him.

Please continue to check our blog content for the latest advice and planning issues from leading investment firms.

Alex Kitteringham

21st August 2024