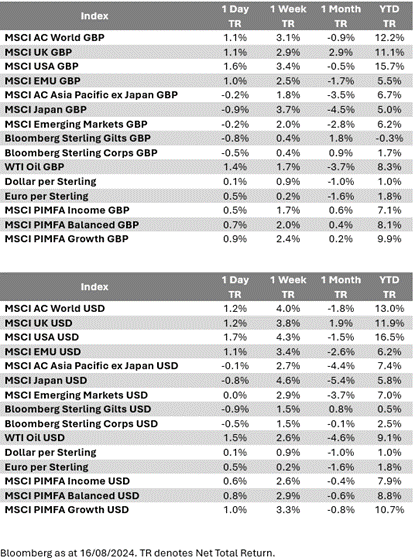

Please see Brooks Macdonald’s Daily Investment Bulletin covering their thoughts on global markets:

What has happened

Equity markets were in confident mood on Thursday. Buoying the economic outlook and pushing back on recession worries, yesterday’s US weekly initial jobless claims data was better than expected for the second week running. Initial claims fell by -7,000 in the week to Saturday 10th August, to 227,000 and below the Bloomberg consensus estimate of 235,000. The continuing claims number also fell. Reflecting the better news, the US S&P500 equity index ended yesterday up +1.61% in US$ terms. It is now up +8.28% above the intra-day low it reached last Monday (5th August) and is now only -2.19% below its record all-time high … a reminder for investors of the risks of trying to time short-term market exit and entry points. Within equity markets, as well as megacap US tech shares leading, smaller company share prices also outperformed with the US Russell 2000 equity index up +2.45% having its best day in four weeks. European equity markets also gained on Thursday, with the UK, French, and German equity markets all up on the day.

US recession positioning dealt a blow by better retail sales

Anyone still positioning for an impending US recession were dealt a blow by US retail sales yesterday. US retail sales month-on-month (MoM) saw their biggest gain since January 2023, up +1% MoM, and easily surpassing the consensus estimate of +0.3%. That the previous month saw a small downward revision didn’t seem to impact the positive market reaction. Adding to the resilient consumer picture, US retailer Walmart came out with better Q2 results yesterday and raised its sales and profit outlook for the full year as well. Walmart shares ended the day up +6.58% and notched up a new record closing high. Walmart CEO Doug McMillon summed up the view neatly, saying that “we aren’t experiencing a weaker consumer”. For completeness, it would be remiss not to mention that US industrial production numbers for July missed estimates yesterday, recording the first annual drop in three months – that said, the weakness was put down to the recent weather impact from Hurricane Beryl impacting factory certain factory activities.

China’s economic malaise continues

The economic malaise in China has continued into the calendar Q3, according to Chinese government data published yesterday. The standout was a surprise slowdown in fixed asset investment, to +3.6% for the first seven months of the year (versus the same period last year). It was below consensus estimates and is the fourth month in a row of declining growth rates. Industrial production growth was also weaker than expected and the third month in a row of falling growth rates. While retail sales looked better, it was thought to be largely down to a seasonal uptick and remains well below pre-pandemic levels of growth. Elsewhere, China’s arguably all-important housing market continues to be problematic: new home prices fell -4.9% year on year in July, the sharpest annual drop since June 2015, and deeper than the -4.5% slide in June.

What does Brooks Macdonald think

Economic performance doesn’t necessarily always correlate to equity market performance, but in China’s case this year, they are both suffering. So far in 2024, against the MSCI World (developed markets) equity index up +14.0% in US$ total return terms, China is lagging, up just +3.1%. And for context, China’s relative underperformance in FY 2023 was much worse. This has led to some to suggest China is worth looking at, if only on valuation grounds – but we continue to see China more of a value trap than a value opportunity. China’s policy makers are stuck between a rock and a hard place – desperate to deleverage the economy after decades of overbuilding in its property market in particular, this, more than anything else perhaps, explains why Beijing appears to be so reluctant to sign off on a large-scale fiscal stimulus to pump up growth rates.

Please continue to check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Andrew Lloyd DipPFS

16/08/2024