AJ Bell Budget Update – How Budget changes might impact your money

Please see below, AJ Bell’s Technical Analysis of yesterday’s Autumn Budget, with a comment from us at the end:

Among a raft of changes, chancellor Rachel Reeves announced reforms to salary sacrifice as well as increases to income tax on savings and dividends as she attempts to bridge the gap between spending and revenue in the UK’s finances.

The protracted leadup to the Budget included rumours around gifting limits and a hike in employee income tax. However, these were not introduced. Instead, tax rises are centred on dividends, interest on savings, and additional council tax for high-value properties. Tax threshold freezes will also continue, and the rules around salary sacrifice are set to change so that contributions over £2,000 will be subject to national insurance.

The subscription allowance for Cash ISAs has also been reduced to £12,000 each year for those under age 65. Stocks and shares ISAs remain at the £20,000 limit.

Here’s a breakdown of the main policy changes in the Budget, when they come into play, and how they could affect your finances:

Limit on salary sacrifice

Beginning in April 2029, salary sacrifice will have a £2,000 limit on pension contributions each year that are not subject to national insurance. After this point, both employees and employers will face national insurance on their contributions. Salary sacrifice currently helps workers save up to 8% in employee national insurance on the cost of their pension contributions. The below table shows the impact on employee’s pay packets per year, assuming the employee has agreed to exchange 6% of their notional salary for a pension contribution, with a 6% matched contribution from their employer.

Despite the new national insurance cap, pension contributions will still be exempt from income tax and workers can continue to enjoy pension tax relief up to their marginal rate of tax. Plus, making pension contributions to schemes like SIPPs will still reduce a taxpayer’s ‘adjusted net income’, pulling them out of higher rate tax while also boosting their retirement savings.

Rather than making a formal arrangement to keep their salary below a certain level, workers will need to work out what extra contributions they need to make to reduce their ‘adjusted net income’. This will involve a little bit of extra admin but will still be well worth it when you consider the potential tax savings on offer.

Lifetime ISA scrapped

The government will be making a new product available in early 2026 to replace the Lifetime ISA. It will attempt to create a simpler ISA product, focused on helping first-time home buyers. The Budget does not mention if the refreshed vehicle will encompass the other main purpose of Lifetime ISAs, which is as a means of building a retirement pot.

In the 2024/2025 tax year, 87,250 individuals took money out of their Lifetime ISA to purchase a home and about 960,000 people subscribed to a Lifetime ISA, according to the Office for National Statistics. These wrappers currently allow for subscriptions of up to £4,000 each year with a 25% government top up.

Withdrawals can be used to buy a first home with a value of £450,000 or less or for an income in retirement after the age of 60. Withdrawals for any other reason are subject to a penalty charge except in a few exceptional circumstances.

Reduction of Cash ISA allowance

While Stocks and shares ISAs will maintain their £20,000 annual subscription allowance, Cash ISAs will have a £12,000 subscription limit each year beginning in April 2027. This limit will not apply to those over the age of 65.

For those searching for cash alternatives following the policy change, there are ways to create cash-like holdings within a Stocks and shares ISA. These include money market funds, treasury bills, or low-risk, multi-asset instruments which have large cash holdings.

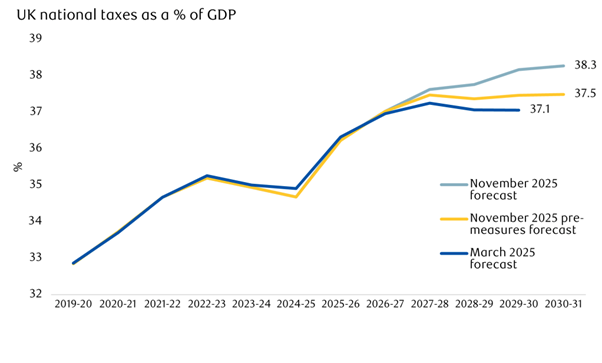

Tax threshold freezes

Tax threshold freezes have been extended for another three years until 2031, meaning income bands will be on track to stay the same for the best part of a decade. The cumulative effect of the freeze means people are seeing their tax bills rise dramatically when compared to a scenario in which thresholds had increased in line with inflation each year. Extending the freeze until 2031 will cost individuals up to £1,293 in extra tax over the next three years, according to AJ Bell’s calculations.

The extent of the tax hit is dictated by how much you earn, with an extra tax bill of £683 over the three years for someone on £45,000 or £1,293 for someone on £70,000.

More than 8.3 million people are now paying higher or additional rate tax, up by 45% since 2021, and extending the freeze will push even more working people and pensioners into higher tax bands.

If there had been no freeze, the OBR estimates that the personal allowance would have been £17,470 by 2030/31 and the higher rate threshold would have been a whopping £20,100 higher – standing at £70,370.

If you take Reeves’ extension to the freeze alone, the personal allowance would have stood at just over £13,353 by the 2030/31 tax year – instead it will remain stuck stubbornly at £12,570.

Increased tax on dividends

Both basic and higher rate taxpayers will face an increase of two percentage points in the amount they pay on dividend income starting in April 2026. This means that basic rate taxpayers will now face a 10.75% tax while higher rate taxpayers face a 35.75% tax. There is no tax increase for additional rate taxpayers from their current 39.35% rate.

If dividend-paying investments are held in an ISA or pension, there will be no dividend levy to pay. Outside of these wrappers, investors will have a £500 tax-free dividend allowance before they begin to be taxed at the above rates.

For example, if a basic rate taxpayer was earning a 4% yield on a £100,000 portfolio, their tax bill would increase from £306.25 at the current 8.75% rate to £376.25 at the new rate (10.75% of £3,500).

Increased tax on savings income

Savings income will also see a 2% tax increase for all levels of taxpayer beginning in April 2027. Basic rate taxpayers will pay 22%, while those in the higher and additional rate brackets pay 42% and 47% respectively.

Thanks to the extended freeze on income tax bands, more people will be pushed into a higher tax band, resulting in a cut to or loss of their tax-free savings allowance. Basic rate taxpayers have a tax-free savings allowance of £1,000, but it decreases to £500 for higher rate taxpayers and there is no allowance for additional rate taxpayers.

For someone with £5,000 of savings interest above their personal savings allowance, the tax increase will cost them an extra £100 a year in tax.

Over 10 years, a higher rate taxpayer with a £50,000 savings pot earning 4% interest (£2,000) will face £380 of additional tax thanks to the increase. A basic rate taxpayer will face £135 in extra tax across the same period.

Additional tax for high value properties

Starting in April 2028, owners of properties valued at more than £2 million will be subject to an additional yearly charge on top of their existing council tax bill in a so-called ‘mansion tax’.

The surcharge will begin at £2,500 and scale in bands to £7,500 for those with properties valued at £5 million or more. These levies will increase over time on an annual basis in line with consumer price inflation.

OBR estimates that this tax will be factored into the price of properties over time and result in price bunching below each band on the scale.

Stamp duty waived for new shares

In a rare bright spot for investors, the Budget introduced an exemption of stamp duty for newly listed stocks in the UK for the first three years. Investors currently pay stamp duty of 0.5% on share purchases. The waiver aims to boost demand for new additions to the market and thereby increase the appeal of London to businesses considering a stock market listing.

Our Comment

From my point of view this Budget did not focus enough on growing our economy here in the UK. Unfortunately, the factions within the Labour party appear to be constraining any real focus on business growth.

The impact of this Budget over the next few years is that we are all going to be paying more taxes. This includes the core Labour voters. As a result, domestic consumption could be impaired.

Businesses and individuals will need to plan to alleviate the impact of some of the Budget measures. It is more important than ever that we use the allowances and reliefs available to us while we have them.

I’m hoping for more output focused on economic growth, we will see. This morning I’ll be listening to a technical review of the Budget. We will keep you posted.

Steve Speed

27/11/2025