Please see below, an article from Tatton Investment Management, analysing the key factors currently affecting global investment markets. Received this morning – 12/01/2026

Optimism prevails

Markets have started the year well, led by small and mid-cap stocks. US military action and threats barely moved markets – not even oil prices. Instead, investors are focused on reasonable growth data and its potential to improve.

According to JP Morgan’s nowcasts, US growth is estimated at to be running at an annualised 1.6%, while the UK is estimated to be expanding 1.5% although both economies did soften at the end of 2025, leading to gloomy commentary.

That slowing is likely to be a positive. It provokes monetary policy action; cooling inflation allows for beneficial interest rate cuts. It provokes government policy action; in the US, President Trump has promised more tax rebates and spending, which will add to the wave of AI investment coming through this year; in the UK, deregulation and a move back towards Europe.

Trump’s focus on interest rates has led to a likely criminal indictment for Jerome Powell and a decree that the housing agencies should buy $200bn of mortgage bonds. Markets seem to think Trump will have some success, that these actions may lower US government yields and mortgage rates in the near-term.

That doesn’t mean disruption isn’t a long-term problem, though. As we saw with Brexit, markets and even corporate profits can hold up decently after structural shocks, but they are felt over the long-term.

The upcoming wave of AI capex – raised by US tech firms last year and soon to be spent – is also soothing markets. We said in our 2026 outlook that the capex surge could cause the previously unloved parts of the market to do better, and we’ve seen that in recent weeks: value is outstripping growth, and small and midcap stocks are pushing ahead. It’s too early to call this a trend, though. Even if it becomes one, that doesn’t mean big tech stocks will do badly. More likely, it means tech stocks’ performance will depend on continued outperformance in profit growth, rather than valuations.

Strong global growth won’t necessarily mean another equity rally – since markets have already front-run strong 2026 growth. Stocks should be supported, but that also relies on inflation staying benign. Inflation has been subdued largely due to weak employment markets (perhaps a consequence of AI). At some point, though, the massive global infrastructure push will surely mean more employment, which could mean higher inflation and central banks turning hawkish. That’s a risk for the second half of 2026.

December Asset Returns Review

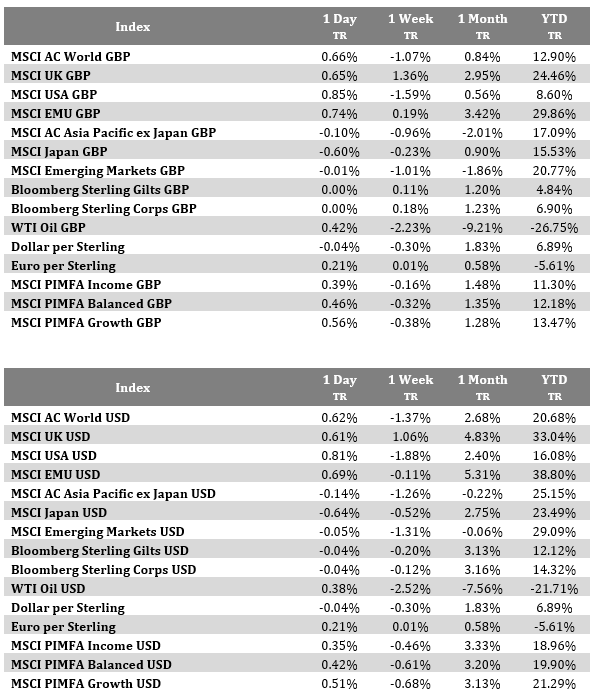

Global stocks dipped 0.5% in sterling terms in December, while bond prices dropped 0.2%. Rotation was the flavour of the month, with significant variation between regions and asset classes. US tech stocks dropped 2%, as the fears of an “AI bubble” finally took the wind out of their sails. We think the lack of share buybacks also played a role in US tech’s underperformance; tech companies have been spending big on AI infrastructure, sapping the cash available for buybacks. That made stretched valuations more vulnerable. AI infrastructure investment should benefit smaller US companies and older industries though, which is why small cap US outperformed large in December.

The growth-to-value rotation benefitted Europe’s market, which gained 2.4% as December’s (and 2025’s) standout performer. UK stocks were a close second, gaining 2.3% through the month, thanks to heavy weighting of relatively undervalued energy and financial stocks. The UK and Europe were helped by a weaker dollar.

The dollar was particularly weak against China’s renminbi. Beijing is pushing RMB stronger to boost its global status, but this doesn’t help its domestic economy – evidenced by Chinese stocks’ 2.2% fall last month. Broader emerging markets still did well (+1.5%), led by high-growth India and Latin America.

Commodities prices diverged sharply: oil fell 3.9% but metals gained significantly. Speculative metals trading pushed up prices, evidenced by the 31.5% surge in silver. Gold gained 2% through the month and an astonishing 53.6% in 2025, benefitting from the loss of faith in the dollar as a reliable long term store of value.

Even though there was no ‘Santa Rally’, 2025 was another strong year for investors overall. Some fear that, after three strong years, the good times must be over – but we don’t see any data to back that up. The investment outlook is positive for now.

Don’t count on housing

Residential property had a bad 2025: average UK prices barely moved and global house price inflation was just 2.2% year-on-year in December, according to Absolute Strategy Research. We thought that falling interest rates would support housing demand and construction, but a global lack of affordability meant prices declined in real (inflation-adjusted) terms. Property prices have been increasing faster than wages, without a major correction, for nearly two decades. They usually fall in a recession (banks repossess homes and offload them quickly) but we haven’t had a typical recession (the pandemic being very atypical) for years. Without recession, the only way for affordability to improve is for wages to slowly catch up with prices. That process started last year.

The UK, with its long-term housing supply problems, is a good example. RICS’ House Price Balance has been deeply negative since the summer, despite mortgage rates falling in 2025. Affordability, as a measure of wages to house prices, improved last year but is still historically high. UK housing supply actually expanded – with estate agents reporting a bump in properties on the market – but transactions are still falling, because few can afford to buy them.

One way to get the UK market moving would be easing planning regulation on existing homes, which still have historically high renovation costs. Regulation has already eased on new construction, but developers aren’t building because they are uncertain of demand.

Even if that happens, house prices are unlikely to rise significantly in 2026. Affordability is now a global political priority and policymakers are reluctant to see prices rise, even if they don’t want them to fall. We therefore see a dull outlook for house prices, and don’t consider property a great investment compared to equities or bonds. Hopefully that eases consumer costs and encourages equity investment. If so, a property lull wouldn’t be bad for the world economy.

Please continue to check our blog content for the latest advice and planning issues from leading investment management firms.

Marcus Blenkinsop

12th January 2026