Please see below, an article from Tatton Investment Management, analysing the key factors currently affecting global investment markets and an outlook for 2026. Received this morning – 15/12/2025

Powell offers some liquid cheer

Stocks were mostly solid last week but tech was weak, culminating in a mild US sell off late on Friday. Oracle revealed ostensibly very strong numbers, but this wasn’t enough to beat analysts’ stretched forecasts. With the debt expansion outstripping sales growth, the cloud computing giant’s shares initially slumped 10% and ended 15% lower on the week. Broadcom then also disappointed on Friday, proving how difficult it is for anyone other than the ‘Magnificent Seven’ to keep investors happy.

Substantially higher prices for all manner of computer chips are also impacting sentiment about big tech’s capex splurge. Tech/AI optimism is not unwarranted, but reality checks are limiting its extent.

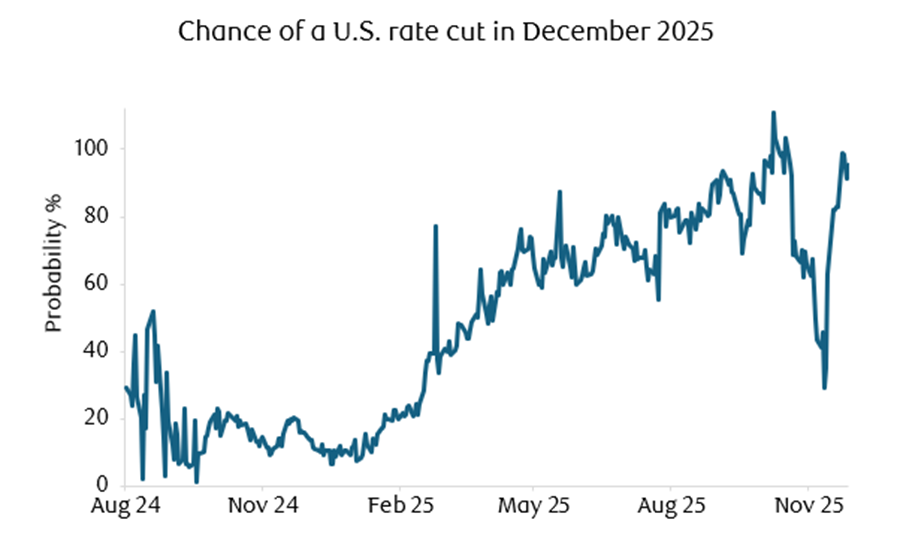

Before that, the Fed’s expected rate cut, and liquidity adjustment pushed US stocks up across the board. The Fed’s new $240bn bond buying isn’t quite quantitative easing: it’s time limited (QE was open ended) and focussed on short-term bonds, and there is no intention to drive down risk premia. But it will improve market liquidity nonetheless. Markets now see the Fed as less hawkish than expected, benefitting small and midcap stocks, while lowering bond yields and the dollar. Notably, cryptocurrencies didn’t benefit as some thought they might.

The US is now clearly disengaging from Europe and focussing on Latin America, which has boosted European defence stocks and forced European leaders into more urgency on stranded Russian assets to help finance their Ukraine support. European stocks are doing better in general, buoyed by joint-enterprise fiscal spending. European bond yields have shifted up while US yields have fallen, and the euro is on a better trajectory.

UK budget talk has thankfully subsided and domestic investors are putting money back into risk assets.

Read on for a condensed version of Tatton’s 2026 outlook.

The outlook for 2026 – overview

Based on the aggregate global earnings outlook, investment returns should be positive in 2026 but we expect significant change and rotation. The positive case is based on interest rate cuts, fiscal stimulus and a wave of AI capex – boosting corporate earnings in the first in H1 2026 at least. The risks are mainly geopolitical (Russia-Ukraine, China-Taiwan – but US-Venezuela is unlikely to move markets) or policy-related (tariffs).

Global trade growth will continue to be curtailed by the Trumpian backlash to globalisation. But the world’s biggest economies are investing to build infrastructure and domestic demand, so aggregate growth will still be supported. There is a strong investment drive coming from individual countries (European defence spending, Chinese stimulus and US fiscal support) and from private AI capex. Rapid geopolitical and technological change raises risks, but the investment drive should keep profits ticking. The big tech firms are expected to win out from the AI race, but we don’t know whether future profits will live up to expectation.

The investment drive underlies our rotation thesis: previously unloved parts of the market improving while previous outperformers struggle to maintain their advantage. The infrastructure buildout requires capital, which requires central banks staying accommodative. If they turn restrictive, capital could get dragged away from ‘growth’ assets, meaning less liquidity and more volatility. That’s a constructive environment for active investment managers.

H2 2026 is less clear. Growth could disappoint and AI capex run out of steam, or it could be so effective that inflation resurges and the Fed turns hawkish – causing markets to tighten up. There’s also a risk price controls in reaction to the US consumer unaffordability disquiet. Unaffordability is why many feel gloomy about the economy while investments look a lot more optimistic. Hopefully next year’s changes rectify some of that gap.

2026 Outlook by region

US stocks will be supported by rates cuts, a fiscal boost and AI capex in H1 2026. The so-called ‘K-shaped economy’ (growth driven by AI asset returns, while the old economy and those without assets struggle) makes it difficult to assess growth. Companies aren’t firing much, but they aren’t hiring either, which is why the Fed’s dovish stance will continue. Trump’s appointments to the Fed will increase the dovish tilt too – pushing down short-term bond yields. Trump is also likely to boost fiscal policy ahead of the midterm elections, pushing up long-term yields, meaning a steeper yield curve.

This could overheat the economy in H2, causing the Fed to tighten and possibly spook investors. The dollar could keep weakening, as Trump attempts to address external trade imbalances. As that correction goes on, the US is a less attractive place to invest. It still has the biggest companies with the strongest profit growth, so we shouldn’t be too negative – but the K-shaped narrative makes things murkier.

UK assets are decently placed for 2026, but a strong year in 2025 might dull future returns. Britons’ negative perceptions of the recent budget don’t match up with the view from international investors: stocks gained, bond yields fell and sterling strengthened. The low rate of domestic ownership means international sentiment is more important for UK assets, and we expect that to remain in 2026. The Bank of England will cut rates this week and likely further next year, as inflation slows from sterling’s strength and less pressure on regulated prices. The global capital shift away from the US could also benefit the UK.

Europe has promise but, as usual, division could get in the way. Defence spending will boost growth but markets have already front run much of the benefit. Stock valuations have room to catch up with the US, but earnings growth momentum would have to catch up too. Financials have done well this year and will likely buyback their own shares – but this alone can’t power outperformance. The best thing for European assets would be a single financial market, which we hoped Chancellor Merz would push for but the jury is still out. German politicians are already talking about tightening belts, so Europe could be more fiscally prudent than the US. With no ECB rate cuts expected, that will flatten the yield curve. That is unless Russia becomes an even greater threat and Europe has to loosen the fiscal purse-strings.

Japan has strong long-term prospects, owing to corporate reforms and the cheapness of the yen. Prime Minister Takaichi isn’t taking advantage of the yen’s competitiveness, instead raising tensions with China and putting pressure on long-term bond yields. That’s why the yen will stay weak, despite the Bank of Japan likely raising rates. The flipside to persistent inflation is stronger growth and higher wages – which Japanese are now using to buy their own assets. That flow will support stocks in 2026.

China has a strong outlook, but restrictive economic policies could dampen returns. Beijing has been forcing the renminbi stronger, which isn’t good for the weak economy but is good for the renminbi’s international status. China is presenting itself as a reliable trade and finance partner to emerging markets in particular and they seem to agree. Beijing is also avoiding getting dragged into fights with the West, which is why it probably won’t invade Taiwan for the time being.

Emerging Markets have varied prospects for next year. Commodity exporters (particularly metals) will benefit from a surge of AI-fuelled infrastructure building, and Asian EMs stand to gain from China’s increasingly important regional economic hub. India’s service sector will be challenged by AI replacement. The reverse correlation between Indian and Chinese equity will likely continue.

2026 outlook by asset class

Bond and money markets will vary by region. Fed cuts will push down short-term US bond yields, while resurgent growth and potentially higher inflation will push up long-term yields – a steepening of the curve, which would extend the funding pressures for smaller companies. European yield curves will likely flatten, as the ECB holds short rates steady and fiscal policy looks less expansive than expected this year (unless Russia gets more aggressive and Europe has to fund even greater defence spending). UK bond yields depend on the government’s stability, but investors like Britain’s higher yields and strong currency. On corporate credit, default rates will likely rise amid a capital rotation, with more capital required in the real economy to build infrastructure. That healthy churn doesn’t mean systemic credit risk, though.

Equities are well supported for H1 2026, but the demand for capital to build infrastructure could mean rotation into previously unloved stocks. Rate cuts, fiscal spending and AI capex will boost earnings growth. Profit growth disproves that an ‘AI bubble’ is about to burst, but it will be difficult for big tech to outperform, given high equity valuations and the demand for capital. The wave of AI-related and state-led investment will create new opportunities. That’s healthy, but excess liquidity being soaked up by infrastructure investment means less liquidity in markets – making the risks feel riskier.

Commodities and cryptocurrencies: Industrial metals will be supported by infrastructure investment. Gold and cryptocurrencies are challenged by the fact that China’s renminbi has emerged as another alternative to the dollar, though gold should still be supported by central bank buying. Leveraged cryptocurrency traders have often been marginal equity buyers too, so crypto volatility matters for stocks.

Please continue to check our blog content for the latest advice and planning issues from leading investment management firms.

Marcus Blenkinsop

15th December 2025