Please see below, an article from Tatton Investment Management, analysing the key factors currently affecting global investment markets. Received this morning – 09/02/2026

Flipping the narrative

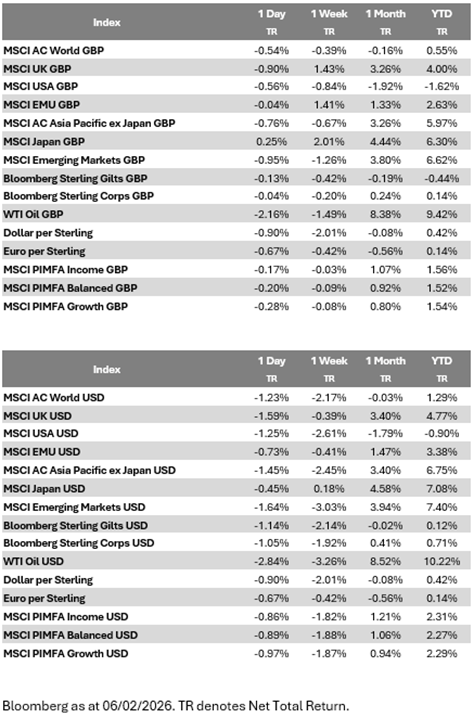

Global stocks marked time overall last week but US equities were a notable underperformer again despite a late Friday rally. AI is at the centre of the narrative but, this time, it’s not a positive. Other regions held up better: Japanese stocks soared ahead of an expected Takaichi’s election win (now a confirmed landslide victory). UK equity weathered political turmoil (helped by a more dovish Bank of England) and European stocks benefitted from the ECB also recognizing a benign inflation outlook.

Kevin Warsh’s nomination as the next Federal Reserve chair calmed markets to a degree, although some fear he might prove less positive for equities. He’s a strong-willed, orthodox and surprisingly hawkish pick – but his hawkish streak is more on reducing the Fed’s bond holdings. He’s said recently that AI productivity will suppress inflation and allow for lower rates (Trump wouldn’t have picked him otherwise) but he wants to reduce the Fed’s liquidity provision – returning it to the true lender of last resort. It’s a worthy aim but will likely mean more market volatility and valuation gains will be more difficult. On the plus side, his arrival will likely mean banking deregulation. Banks can and should pick up the liquidity slack over time.

The AI sell-off started with software companies but spread to the likes of Nvidia and Oracle when it became clear that layoffs are a growth risk – compounded by weak US jobs data. The US economy is sensitive to its stock market. The strongest effect is felt when businesses react to a fall in their share prices by switching from expansion to cost-cutting. If stocks keep falling, the labour market could deteriorate further. Recent growth data has held up well, but markets are already directly impacting economic confidence.

Falling bond yields are providing an offset – both for investors and by lowering borrowing costs. US businesses will likely start borrowing again when if rates and yields fall, benefitting sectors outside of tech and further fuelling the small cap rotation. The AI macro risk is more pronounced in the US than elsewhere, exemplified by the relative outperformance of UK and European equity.

We shouldn’t lose sight of the fact that productivity growth is the ultimate driver of growth and investment returns. Disruption brings risks, but creates its own balancing forces.

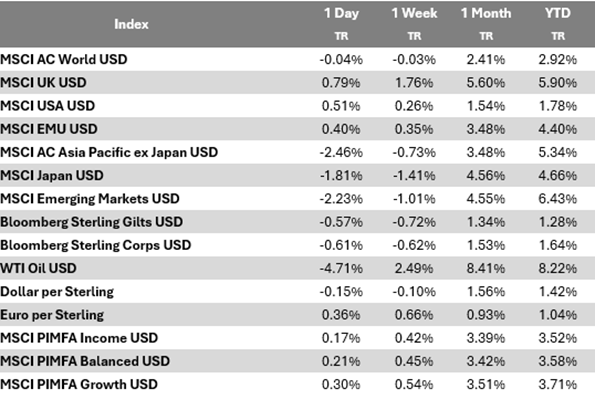

January Asset Returns Review

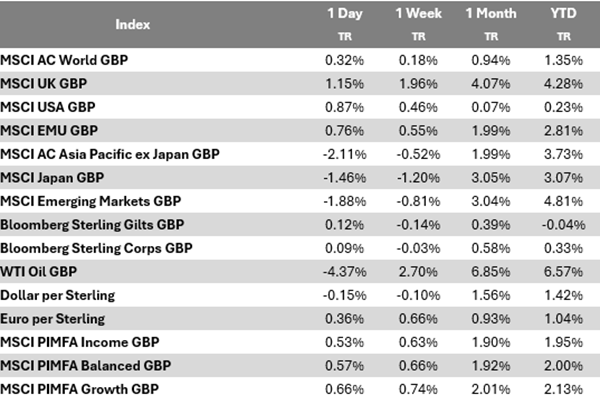

Stocks edged up 0.9% in sterling terms in January, while bonds gained 0.2%, but with significant variation. Trump’s tariff threats over Greenland had only a mild impact on equities, and his threat on Fed independence pushed up US bond yields. Bond markets were soothed by the appointment of Kevin Warsh as the next Fed chair, but that wasn’t enough to revive the dollar. US stocks lost 0.6% due to currency weakness and concerns over big tech. Microsoft’s disappointing earnings sent its shares down 12% in the space of a few hours – though Meta’s jumped after strong earnings. Meanwhile, stronger US economic data pushed up 2026 growth estimates, helping small-cap stocks.

Regional rotation continued: European stocks gained 2.2% and UK 3%, thanks to more attractive valuations (and despite still weaker earnings growth than the US). Japanese stocks jumped 4.5%, with improving corporate profitability now backed up by global cyclical trends. But Japan’s bonds sold off sharply and the yen sank. The bond market has structural problems (similar to the UK’s ‘Liz Truss moment’) but the current discount looks attractive. The global growth narrative also pushed emerging markets up 6.7%, with high-tech Korea a standout once more.

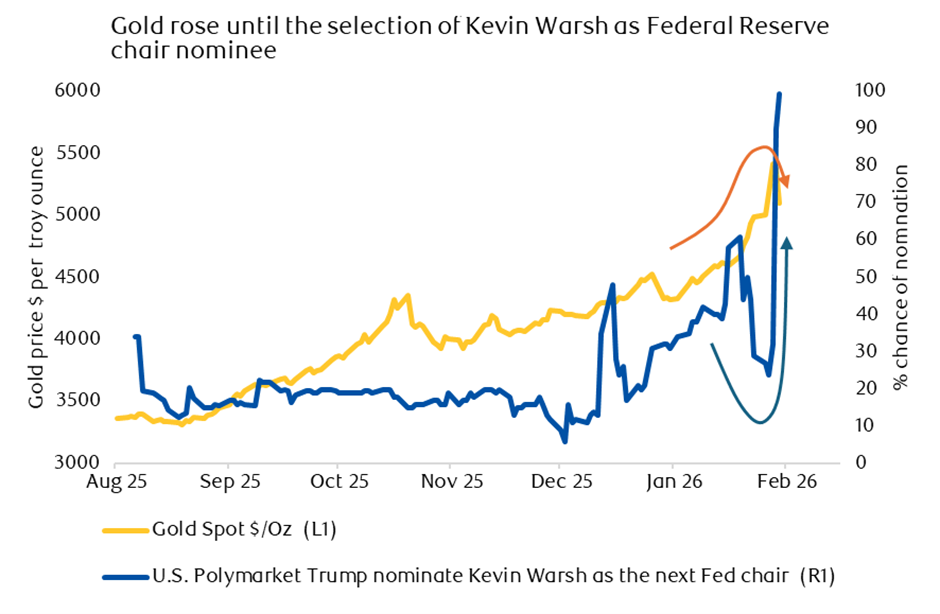

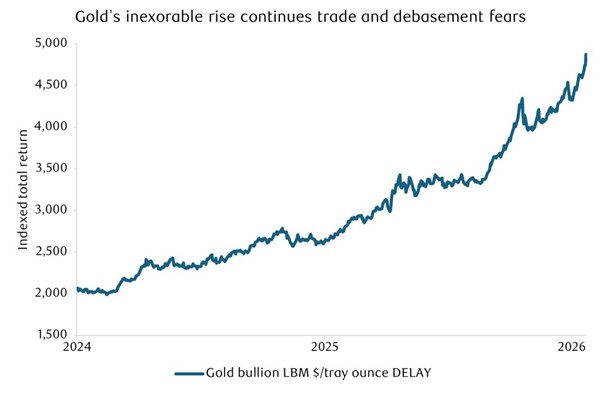

Gold’s price spike was remarkable, but it was more driven by speculation and illiquidity than its usual long-term supports (central bank purchases, private Chinese demand and retail momentum trading). Silver prices gained too, but cryptocurrencies – a similarly speculative, liquidity-driven asset – sank. That sends mixed signals about investor risk appetite. Other commodities sent mixed signals too: oil prices have been weak over the last three months (despite gaining in January) but industrial metals gained. The former points to weaker growth, and the latter suggests strength.

AI losers emerge

The AI trade started eating itself, after Anthropic’s new Claude Cowork tools threatened to replace workers and entire industries. Anthropic CEO Dario Amodei has been vocal about this, publishing an essay last month that predicted “unusually painful” job losses, as AI cuts across all industries simultaneously. We already see stories about AI-related layoffs at the likes of Amazon, Expedia and Dow Jones, and we think it’s a significant factor behind the lack of hiring in developed economies. Last week, the fear of AI displacement forced a sell-off across legal services, analytics and software sectors.

A recent IFS working paper suggests AI innovations increase output, investment wages and employment over the long-term – as productivity gains and job creation outweigh job displacement over the long-term. But rapid transitions are painful in the medium term: the UK’s transition from manufacturing caused a long and deep recession in the early 1980s. And manufacturing accounted for just 30% of UK GDP in 1979, whereas services today account for 81%. The fear of job replacement alone can cause a recession too, as workers save more and consume less, hitting business revenues and causing layoffs.

We aren’t saying this will happen, but it has become a clear and present macroeconomic risk. Where investors used to only see upside in AI, now they see a growth risk. This is different to the ‘AI bubble’ narrative. It’s not that investors are worried inflated valuations or unsustainable profits for AI companies; it’s that the pain could outweigh the gain in the short or medium-term. Even Nvidia and Oracle – two of the biggest AI winners, whose share prices dropped last week – need customers who can afford to buy. This also doesn’t negate the positivity about long-term productivity. But the losers are now clearly in focus – which could reinforce the capital market rotation we have seen recently.

Please continue to check our blog content for the latest advice and planning issues from leading investment management firms.

Marcus Blenkinsop

9th February 2026