Please see below Brooks Macdonald article received this morning, which provides a market update and refers to Ukraine’s successful counter-offensive strategies in their ongoing war with Russia.

What has happened

Despite a lack of new news on the central bank front, markets have been increasingly preparing themselves for another hawkish rebuke from the Federal Reserve that could lead to a leg higher in interest rate hike expectations. As a possible portent of things to come, Sweden’s Riksbank surprised investors with a 100bp rate hike, which was above expectations.

Federal Reserve

7pm UK time will see the release of the latest Fed decision with markets expecting a 75bp increase in interest rates alongside some aggressively hawkish language. The mood coming into this meeting is a far cry from August when bond markets were hoping for a sign of a Fed pivot towards a more balanced outlook that weighed inflation and recessionary risks. Earlier in the summer we saw a leak when market pricing was significantly different to what the Fed was intending on unveiling, a lack of a similar briefing for this meeting suggests the Fed is comfortable with 75bps. Arguably the key question therefore is how the fresh economic projections from the central bank paint the inflation and growth picture and whether the bank prepares the market for a further 75bp hike in November. Whilst the Fed meeting is the most important of the week, the market is pricing a 50:50 chance between the Bank of England hiking by 50 or 75bps tomorrow.

Ukraine war

Yesterday Russia announced that it would be holding referenda in the four Russian-controlled regions of Ukraine. Such a move has been widely condemned and appears to be part of a strategy to quickly lay territorial claim to parts of Ukraine so as to claim that further incursions into that territory are an invasion of Russia itself. The recent, successful, counter-offensive by Ukraine appears to have raised concerns within the Russian government that further land could be lost, prompting these referenda and also a partial mobilisation of Russian forces. The mobilisation was announced earlier this morning and reservists will now be called up to assist in the invasion of Ukraine.

What does Brooks Macdonald think

The announcement of a partial mobilisation has led to a rise in oil prices but so far is yet to feed into broader equity markets, although it should be noted that an escalation in Ukraine War rhetoric, alongside the US CPI release last week, has already been weighing on risk appetite in recent days.

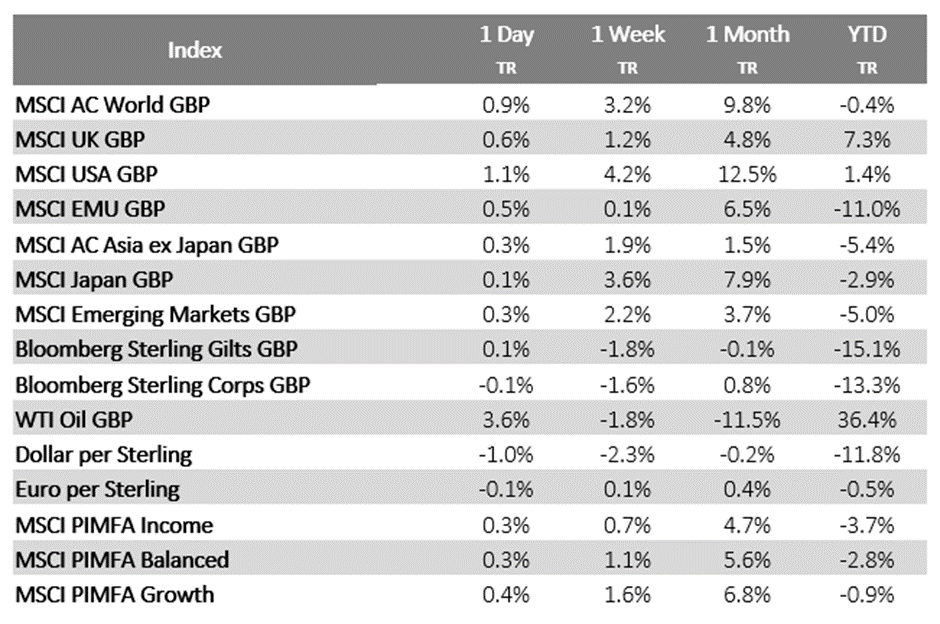

| Index | 1 Day | 1 Week | 1 Month | YTD | |

| TR | TR | TR | TR | ||

| MSCI AC World GBP | -0.5% | -1.4% | -4.4% | -5.1% | |

| MSCI UK GBP | -0.5% | -2.5% | -4.5% | 2.7% | |

| MSCI USA GBP | -0.9% | -0.8% | -5.1% | -4.2% | |

| MSCI EMU GBP | -1.3% | -2.8% | -4.3% | -15.3% | |

| MSCI AC Asia ex Japan GBP | 1.2% | -2.4% | -1.8% | -6.8% | |

| MSCI Japan GBP | 0.4% | -0.6% | -3.7% | -6.8% | |

| MSCI Emerging Markets GBP | 1.1% | -2.2% | -1.7% | -6.5% | |

| Bloomberg Sterling Gilts GBP | -1.2% | -1.3% | -8.4% | -23.3% | |

| Bloomberg Sterling Corps GBP | -0.9% | -0.9% | -6.2% | -19.4% | |

| WTI Oil GBP | -1.2% | -2.1% | -3.4% | 33.5% | |

| Dollar per Sterling | -0.4% | -1.0% | -3.8% | -15.9% | |

| Euro per Sterling | 0.1% | -1.0% | -3.1% | -4.0% | |

| MSCI PIMFA Income | -0.8% | -1.4% | -4.7% | -8.3% | |

| MSCI PIMFA Balanced | -0.8% | -1.5% | -4.9% | -7.6% | |

| MSCI PIMFA Growth | -0.9% | -1.7% | -4.7% | -5.4% | |

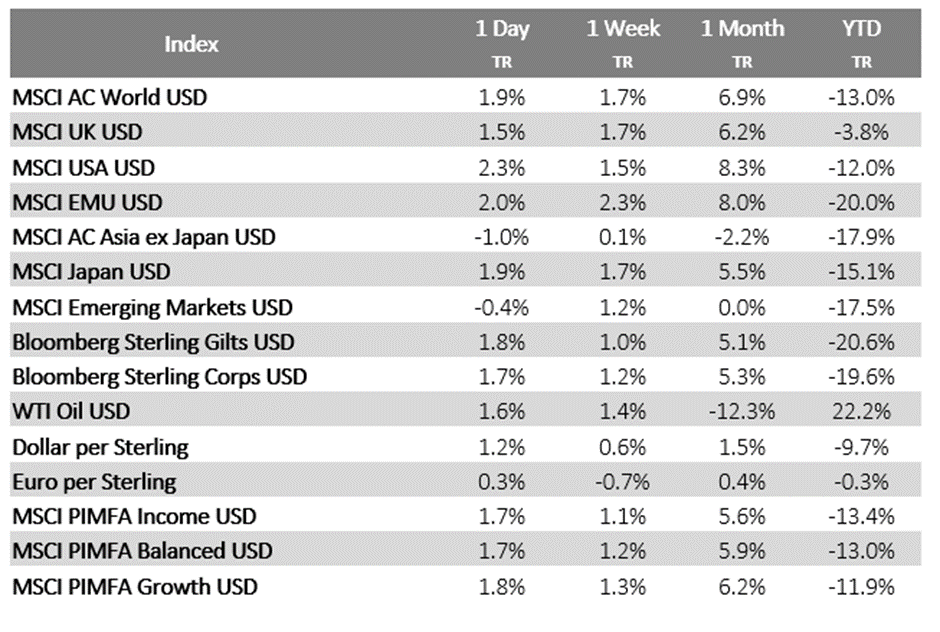

| Index | 1 Day | 1 Week | 1 Month | YTD | |

| TR | TR | TR | TR | ||

| MSCI AC World USD | -0.8% | -2.6% | -7.9% | -20.2% | |

| MSCI UK USD | -0.6% | -3.7% | -8.1% | -13.7% | |

| MSCI USA USD | -1.2% | -2.0% | -8.7% | -19.4% | |

| MSCI EMU USD | -1.6% | -4.0% | -7.8% | -28.8% | |

| MSCI AC Asia ex Japan USD | 0.9% | -3.6% | -5.5% | -21.6% | |

| MSCI Japan USD | 0.1% | -1.8% | -7.3% | -21.6% | |

| MSCI Emerging Markets USD | 0.8% | -3.4% | -5.3% | -21.4% | |

| Bloomberg Sterling Gilts USD | -1.4% | -2.4% | -11.5% | -35.3% | |

| Bloomberg Sterling Corps USD | -1.0% | -2.0% | -9.3% | -32.1% | |

| WTI Oil USD | -1.5% | -3.3% | -7.0% | 12.3% | |

| Dollar per Sterling | -0.4% | -1.0% | -3.8% | -15.9% | |

| Euro per Sterling | 0.1% | -1.0% | -3.1% | -4.0% | |

| MSCI PIMFA Income USD | -1.1% | -2.6% | -8.3% | -22.9% | |

| MSCI PIMFA Balanced USD | -1.1% | -2.7% | -8.5% | -22.3% | |

| MSCI PIMFA Growth USD | -1.1% | -2.9% | -8.2% | -20.5% |

Bloomberg as at 21/09/2022. TR denotes Net Total Return

Please check in again with us shortly for further news and relevant content.

Chloe

21/09/2022