Please find below, an update on how politics are affecting global markets, received from Tatton, this morning – 24/10/2022

Overview: markets look on as Westminster psychodrama continues

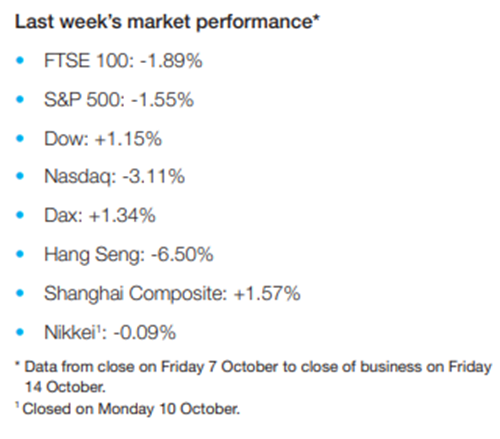

Given the volatility in UK politics last week, broader capital markets felt like a sea of calm in comparison. Markets had already priced in the upside on sterling, believing unfunded Tory tax cuts were no longer on the agenda, but not another leadership hiatus or even the possibility of an early general election. This perhaps explains that after initial cheers, sterling settled at where it had been already against the US dollar before Liz Truss tendered her resignation. Gilts have experienced a rollercoaster of wild and outsized movements during her short but turbulent reign and so the relief rally that followed her departure is understandable.

However, as noted before, the ill-advised fiscal event that triggered Truss’s political death spiral unhelpfully boosted an uptrend in bond yields that had been well underway since the beginning of the year. How yields and yield differences will fare from here will (hopefully) now only partially depend on the further political developments in the UK, but much more on where the rate of inflation is heading and with it, economic activity levels. On the so-called ‘loss of trust’ of international capital markets in the reliability of the UK and its institutions, the past week has demonstrated that while the UK is most certainly not immune from political mistakes, the system deals swiftly and reliably with failure.

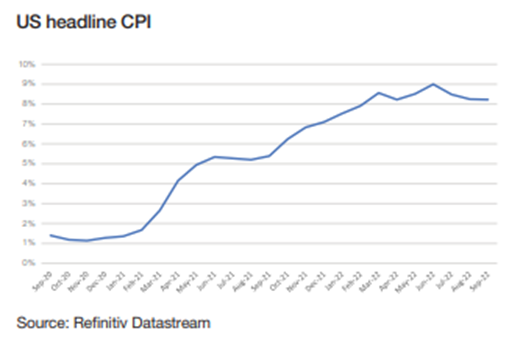

UK inflation (as measured by the Consumer Prices Index) was interesting last week, with food and insurance leading the core (non-energy prices) back up to 10.1%. Both may be seeing lagged impacts from previous energy price rises – but also the shortage of available labour. Our food has become much more energy-intensive in recent years. Indeed, the lagged impacts of energy are still evident across the board. Overall, and compared to previous weeks, the market has been cheered by a lessening of the sense of crisis around Europe and the UK, even if the backward-looking economic data reports still look concerning.

Europe’s energy struggles may be easing

Regarding price pressures on consumers, last week offered some good news for Europe, including the UK. Gas and electricity prices for near-term delivery (over the winter) have come down, as gas storage reserves have filled to higher levels and earlier than anticipated, while industrial demand has fallen much more quickly than thought possible. There was further good news on the electricity front as Germany’s Chancellor Scholz spoke a ‘Machtwort’ (meaning word of authority) and more or less forced his coalition partners to agree a temporary extension of the life of the three remaining German nuclear reactors over the winter.

This altogether lower temperature from the demand and the supply side in pan-European energy markets has led to a sense that the probability and extent of downside scenarios have lessened. This in turn is taking fiscal support pressure off politicians, and leaves markets anticipating less bad times ahead. Despite government-imposed price caps, there had been heightened fear of bankruptcies – which remains elevated, but the immediate danger is clearly receding, as we note from falling European high yield credit rates for those firms with the lowest credit ratings.

Increasingly, scenario assessments like the recent one from Bloomberg’s energy analysts are raising the possibility that Europe could find itself with a gas surplus should the coming winter prove not to be particularly cold one. This would certainly be very good news for hard-pressed consumers, even though the boost to demand from the release of energy earmarked savings could fan broader inflation once again and force the hand of central banks to follow the US Federal Reserve’s push for rates that are anticipated to reach 5% at the end of Q1 next year.

How much isolation can President Xi’s China afford?

Attention has been on Beijing over the last few days, as the Chinese Communist Party hosted its 20th national congress. Held every five years, the congress decides key party posts – which in turn decide state, military and commercial appointments – and sets the policy agenda for the next half a decade. The biggest but least surprising announcement was the inevitable reappointment of Xi Jinping as leader, with party rivals purged (including the very public ‘retirement’ of Xi’s predecessor Li Keqiang) and loyalists installed in his new leadership team. Without question, this is now Xi’s China.

It is somewhat disheartening, then, to hear Xi’s priorities are more political than economic. The biggest brake on growth is Beijing’s strict zero-COVID policy. China is still cycling through regional lockdowns every few months, while its housing market is still ailing from the slow-motion collapse of property developers such as Evergrande. Meanwhile, slowing developed world demand makes it difficult for China to export its way out of trouble. Growth was slowing even before the pandemic, thanks to Beijing’s deleveraging efforts and crackdown on the shadow banking sector. But that was at least an admirable goal – removing excessive debt and improving economic or financial stability. However, harsh crackdowns at home (both COVID- related and on corporates) and tough rhetoric against major trading partners – in the face of an economic slowdown – are a different matter.

It was easy to see why Chinese officials delayed the release of GDP data last week: people may not like what they see. Economists predict annual growth has slowed to 3.3%, the second-lowest figure in the last three decades (after 2020’s initial lockdown year). This is deeply worrying for the party. Just last week, the US announced a de facto embargo on selling high-end technology to China, pushing the rivalry between the world’s pre-eminent powers into something approaching a cold war. This hit tech stocks in the US, but had a broader impact on Chinese stocks. If sustained, the effective ban on technology intellectual property transfer could have a severely limiting effect on long-term growth.

Indeed, the longer-term picture is clouded by China’s ageing population and its increasingly isolated position. Some analysts suggest we are moving into a structurally weaker period for China, where growth may average around 3% per year instead of the incredible 7% or 8% we have grown accustomed to. Even if true, base effects would mean that growth opportunities would still be very significant. China’s estimated 2022 GDP is $18.3 trillion, meaning that 3% growth would add over $500 billion to the global economy – that is still more than China’s total growth in 2016. Zero-COVID is still the biggest hurdle, but if we see signs of that policy loosening early next year – which may well happen if vaccinations of the elderly continue and economic growth falters – then global investors could in the short term become very positive on China.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

David Purcell

24th October 2022