Please see the below message from Tatton Investment Management, detailing their new Multifactor Authentication system. Received late this morning – 18/07/2022

We are continually striving to improve the security measures on the Tatton Portal to protect you and ourselves. We recognise that Multifactor Authentication (MFA) is an important tool to help prevent malicious actors from gaining unauthorised access to your account. We are currently in the process of integrating MFA into the Portal, so while there is nothing for you to do now, there are some important changes that will be implemented in the coming weeks.

What is Multifactor Authentication?

When you sign in to your online accounts – a process we call “authentication” – you’re proving to the service that you are who you say you are. Traditionally that’s been done with a username and a password. Unfortunately, that’s not a very good way to do it. Usernames are often easy to discover; sometimes they’re just your email address. Since passwords can be hard to remember, people tend to pick simple ones or use the same password at many different sites.

That’s why almost all online services – banks, social media, shopping – have added a way for your accounts to be more secure. You may hear it called “Two-Step Verification” or “Multifactor Authentication” but the good ones all operate off the same principle. When you sign into the account for the first time on a new device or app (like a web browser) you need more than just the username and password. You need a second thing – what we call “a second factor” – to prove who you are.

How will this work with the portal?

You will continue to log in to the Portal as usual, using your username and password. There will be certain circumstances where you will need to provide “a second factor”. We will provide further detailed information on how this works in the coming weeks.

What do you need to do?

For now, there is nothing you need to do. MFA will go live in August 2022, if you choose not to setup MFA for your Tatton Portal account then you will be unable to access the Portal from that point onwards. MFA is crucial to the security and protection of you and Tatton so please keep an eye out for further communications, including the detailed instructions on how to get started with MFA.

Please continue to check our blog content for advice and planning issues from ourselves and leading investment houses.

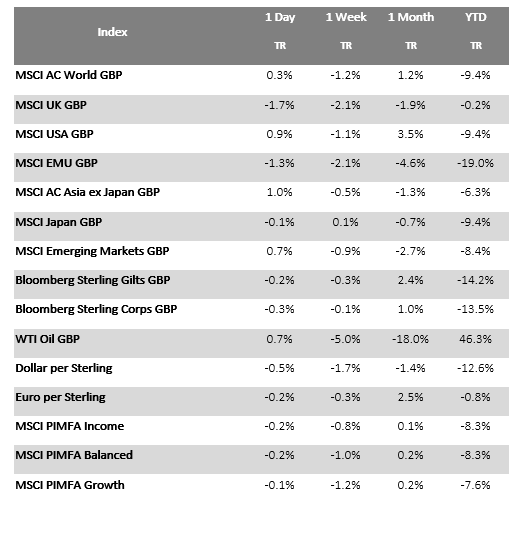

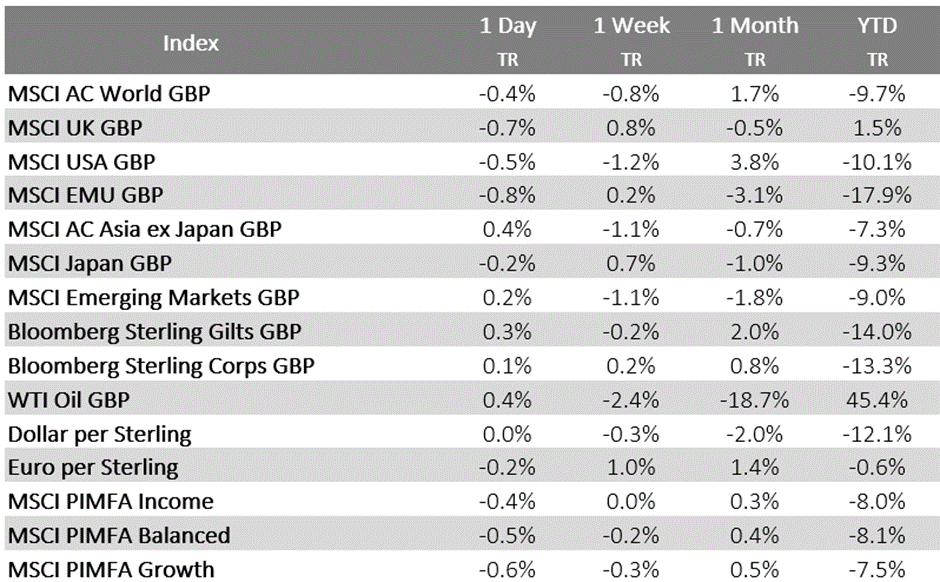

Please find below, a Daily Investment Bulletin received from Brooks Macdonald, this morning – 15/07/2022

What has happened

Risk appetite remained supressed yesterday as bank earnings and recessionary fears combined into another poor day for equity markets. JPMorgan yesterday missed expectations and Morgan Stanley saw investment banking revenue halve compared to the previous year. Q2 earnings will be a key determinant of whether the market concludes that the year-to-date falls adequately compensate for the expected deterioration of margins over the short to medium term.

Federal Reserve

With the US CPI report causing investors to reappraise the near term path for US interest rates, ‘Fed speak’ is being scrutinised to gauge the chances of a 100bp hike. The Fed will enter their communication blackout window on Saturday so yesterday’s comments are one of the last tests of Governor sentiment that the bond market has to work with. Governor Waller yesterday said that the CPI beat earlier in the week justified another 75bp rate hike however he was open to a larger hike if economic data was stronger than expected. President Bullard meanwhile also supported a 75bp hike, with the result that markets reduced their expectations for a 100bp hike. The 2-year US Treasury yield gave back some of its recent rise, trading at 3.11% at the time of writing. US technology stocks were a particular beneficiary of this reduction in rate expectations, managing to secure a small gain yesterday even as the broader US market sold off.

Italy

European political risk returned to the fore yesterday as Prime Minister Mario Draghi attempted to resign after the Five Star Movement refused to back his government in a confidence vote. Draghi said that ‘The loyalty agreement that was the foundation of my government has gone missing.’ With President Mattarella declining the resignation, the Italian political backdrop is uncertain with a fresh round of elections possible. Italy has been facing a large number of economic and political challenges since COVID, as reflected in the spread between German bond yields and Italian yields. Yesterday saw that spread widen to its largest level in over a month.

What does Brooks Macdonald think?

Adding to the concerns of a global slowdown, overnight China released their Q2 GDP data which showed that the economy contracted on a quarter-on-quarter basis. China continues to struggle in applying the zero COVID policy to the latest Omicron led surge and this slowdown may well prompt Beijing to provide further economic support to ensure that the economy does not stall over the summer.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

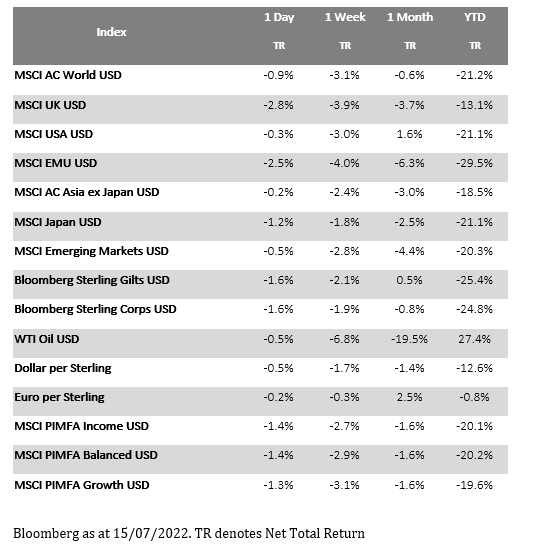

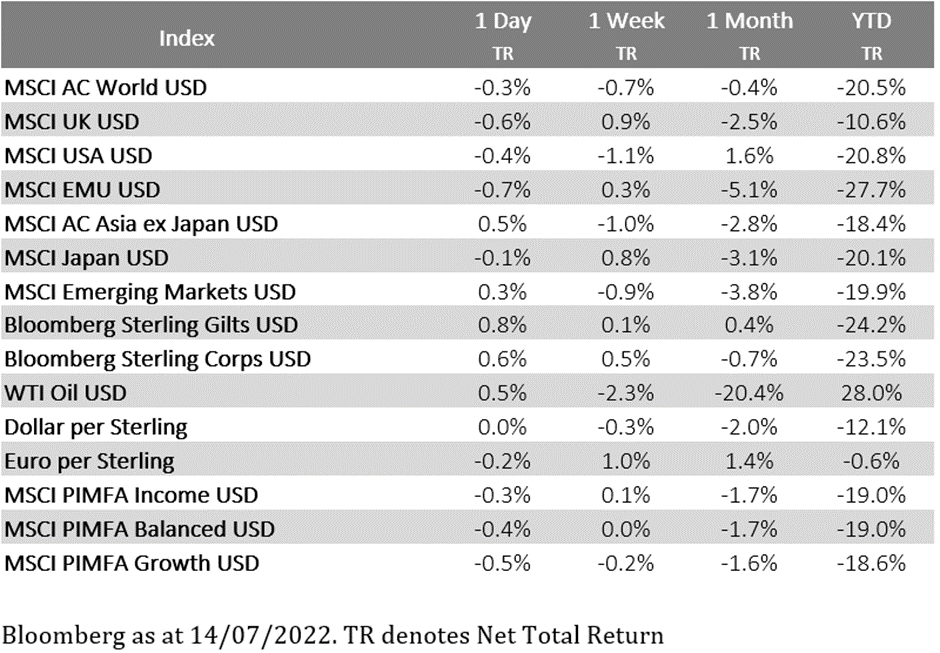

Please see below the latest daily investment bulletin from Brooks Macdonald, which was published and received this morning (14/07/2022):

What has happened?

US equity futures dipped sharply after the release of the June CPI print, however the market staged somewhat of a comeback to end the day only mildly in the red. The bond market was less sanguine however, with a surge higher in the US 2-year bond yield as investors priced in more aggressive Fed rate hikes.

US CPI

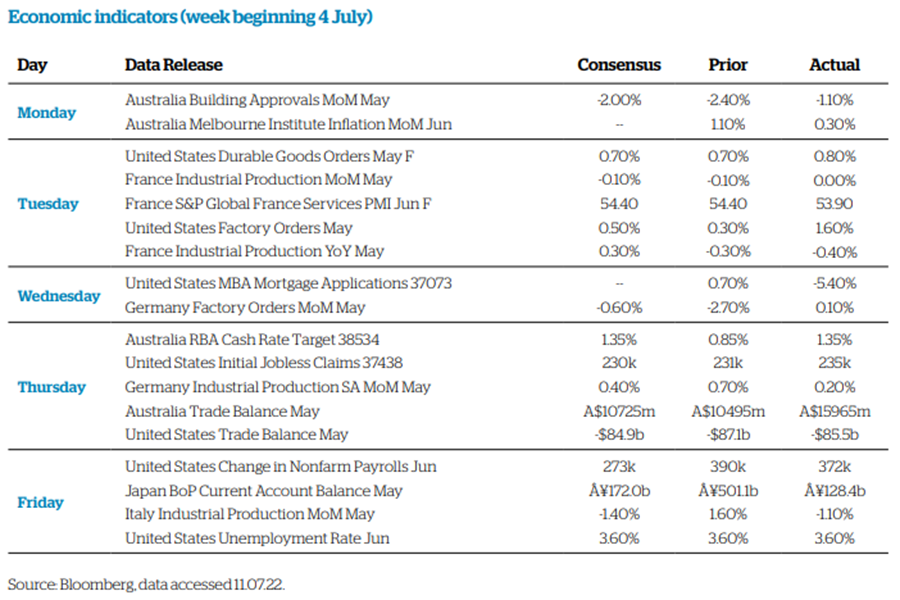

Both the headline and core CPI readings came in higher than the market was expecting. The month-on-month figures saw a dramatic 1.3% increase in the headline and 0.7% in the core reading. Both of these 20bps more than the market was expecting. The market took little comfort from the components of the CPI surge, with a broad showing of inflationary pressure amongst the basket as the year-on-year headline CPI figure crept above 9%. The sharp moves in bond markets mean that investors are pricing in around 90bps of rate hikes at the July meeting, effectively meaning that investors feel a 1% hike is more likely than a 75bp hike. Adding to this grim mood within bond markets, Cleveland Fed President Mester provided a suitable summary of the report as ‘uniformly bad – there was no good news in that report at all’.

Bond Market moves

In March of this year we were debating the impact of a slight intraday inversion of the 2s10s yield curve, as I write the 2-year yield sits at 3.22% and the 10-year yield at 2.97% – a pretty clear statement from the bond market that they believe the Fed will raise rates in the short term but need to cut them in 2023. For context, this is the largest inversion of the yield curve that we have seen since 2000. This surge in US bond yields was enough to finally lead the Euro to fall below parity with the US dollar however the Euro recovered a small amount of ground by the end of the day and remains hovering around 1 Euro to the dollar.

What does Brooks Macdonald think

June’s CPI number was always going to be messy given the moves that were taking place in commodity markets during the month. Whilst yesterday’s report wasn’t particularly enjoyable reading, the broader context is that commodity prices have fallen quite substantially. Compared to three months ago, oil is down over 10%, copper almost 30% down and wheat down 25%. It will take some time for these falls to feed into the consumer inflation basket but should the commodity sell-off continue, better inflation reports will lie ahead.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below this week’s Markets in a Minute article from Brewin Dolphin received late yesterday afternoon – 12/07/2022

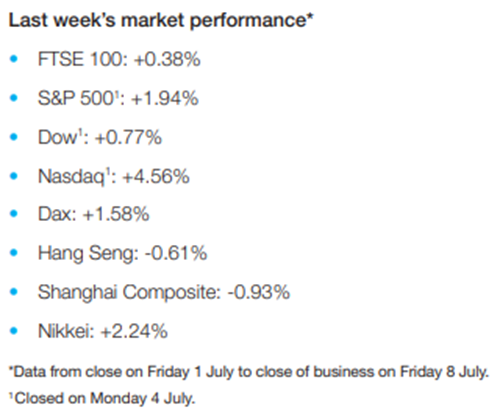

Stock markets were mixed last week as coronavirus cases rose in China, and the US Federal Reserve vowed to tackle inflation.

The Shanghai Composite fell 0.9% as cities across China reimposed restrictions designed to stem the spread of Covid-19. A senior health official said Shanghai, which recently ended a two-month lockdown, faces a “relatively high” risk of further community transmission of the virus.

The UK’s FTSE 100 edged up 0.4% as prime minister Boris Johnson announced his intention to resign, after more than 50 ministers and several Cabinet members stepped down. Johnson will remain as caretaker prime minister until a new leader of the Conservative Party has been chosen.

In the US, the S&P 500 ended its holiday-shortened trading week up 1.9%, lifting it out of bear market territory. Friday’s payrolls report from the Labor Department showed employers added 372,000 non-farm jobs in June, well above expectations of around 270,000.

Shares in Europe also advanced, with the STOXX 600 and Germany’s Dax up 2.5% and 1.6%, respectively.

Russia halts gas flows to Germany

Stocks started this week in the red amid concerns that a temporary halting of Russian natural gas supplies to Germany could become permanent. Gas supplies via the Baltic Sea pipeline Nord Stream 1 were halted for ten days from Monday for annual maintenance work. However, there are fears the shutdown could be extended and exacerbate Europe’s gas crisis.

Germany’s Dax fell 1.4% on Monday (11 July) while the STOXX 600 declined 0.5%. Hong Kong’s Hang Seng tumbled nearly 3% after Beijing regulators issued fines to several technology firms for non-compliance with anti-monopoly disclosure rules. US stocks were also weaker ahead of the release of the latest inflation data.

The FTSE 100 was down 0.4% at the start of trading on Tuesday following a weak session in Asia overnight.

Federal Reserve pledges to fight inflation

Last week saw the release of the Federal Reserve’s June policy meeting minutes, in which officials emphasised the need to fight inflation through further interest rate hikes. Members of the Federal Open Market Committee said the July meeting would likely see a further increase in rates of 50 or 75 basis points (bps), following a 75- bps hike in June. Members said the June increase was necessary to control inflation, which is at its highest level since 1981.

“Participants concurred that the economic outlook warranted moving to a restrictive stance of policy, and they recognised the possibility that an even more restrictive stance could be appropriate if elevated inflation pressures were to persist,” the minutes said.

Members acknowledged that raising interest rates could slow the pace of economic growth but said returning inflation to 2% was “critical to achieving maximum employment on a sustained basis”. Fed officials expect US gross domestic product to rise by just 1.7% this year, down from the March estimate of 2.8%.

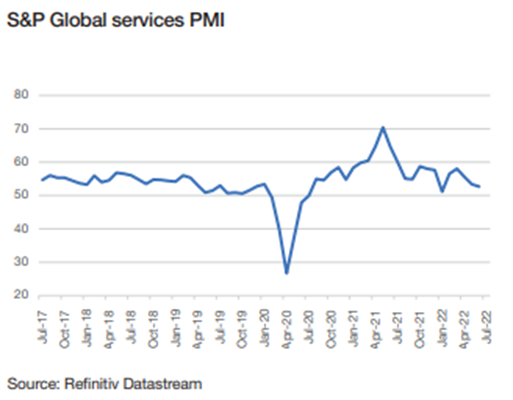

Demand for services slowing

There was evidence of a slowing US economy in the latest S&P Global services purchasing managers’ index (PMI). The business activity index dropped for the third month running from 53.4 in May to 52.7 in June. Although business activity remained above the 50-point mark that separates growth from contraction, it was the weakest rise in activity since January.

New orders fell for the first time in nearly two years as sustained price pressures and economic uncertainty hit demand. Confidence about the year ahead also dropped to a 21-month low, while the rate of input cost inflation slowed from May’s survey but was still among the fastest since the series began in October 2009.

Meanwhile, the US manufacturing PMI fell from 57.0 in May to 52.7 in June, the lowest for almost two years, led by a near-stagnation of factory output and the first fall in new orders since May 2020.

Euro area retail sales miss forecasts

The volume of retail sales in the euro area rose by a seasonally adjusted 0.2% month-on-month in May, missing economists’ forecasts of 0.5% growth, according to data from Eurostat. This followed a 1.4% drop in April, which was revised down from initial estimates of a 1.3% drop.

While sales volumes of non-food products rose by 1.2%, automotive fuel sales fell by 0.2% and sales of food, drinks and tobacco declined by 0.3%. On an annual basis, sales of food, drinks and tobacco dropped by 3.6%.

UK house prices hit record high

The UK housing market defied expectations of a slowdown in June with average property prices rising by 1.8%, the biggest monthly increase since early 2007, according to Halifax. On an annual basis, prices rose by 13% and pushed the typical UK house price to another record high of £294,845.

Russell Galley, managing director at Halifax, said the supply-demand imbalance continued to be the reason behind the sharp increase in house prices. “Demand is still strong – though activity levels have slowed to be in line with pre-Covid averages – while the stock of available properties for sale remains extremely low,” he said.

Galley added that while a slowing of house price growth may come later than previously anticipated, it should still be expected in the months ahead as increased pressure on household budgets and higher interest rates impact affordability.

Please continue to check back for our latest blog posts and updates.

Please see below article received from Brooks Macdonald yesterday afternoon, which provides a global market update following Boris Johnson’s resignation and further rises in energy costs.

Economic data last week painted a better picture of near-term economic momentum

Last week saw a better run of economic data with bond yields and equities rising ahead of the key earnings season. After Boris Johnson’s resignation, a leadership race has begun within the UK’s Conservative party with the field expected to be whittled down this week.

Energy security concerns in Europe led to a surge in European energy costs

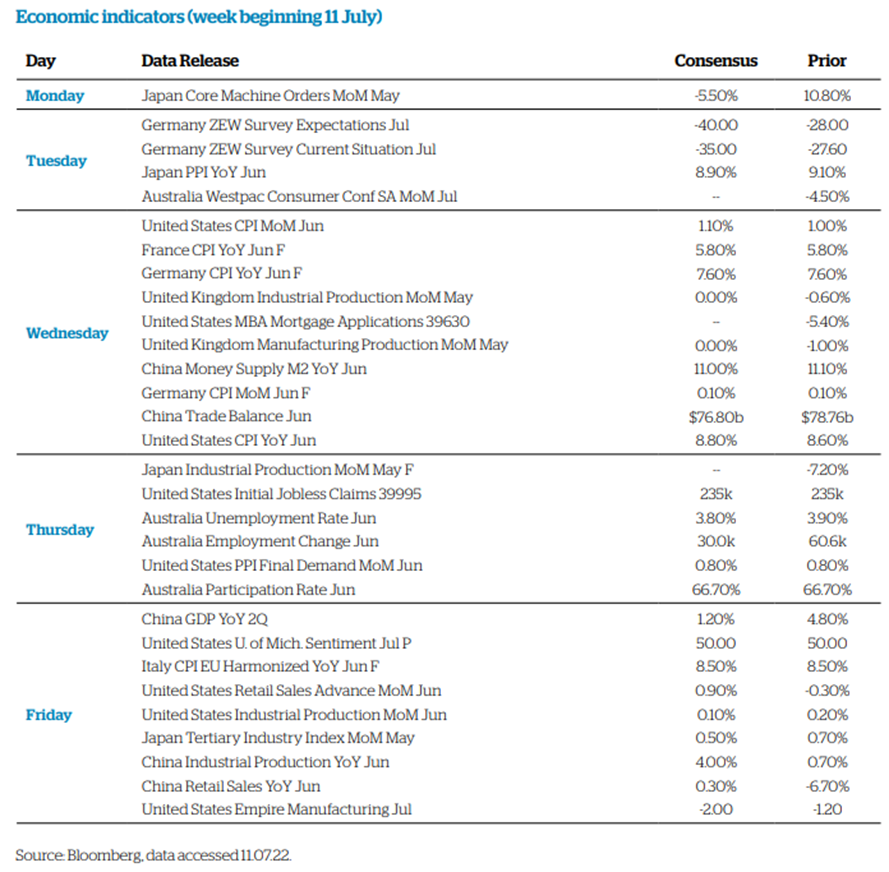

While European energy prices have seen sharp moves higher, the US’s energy security has kept US energy prices relatively subdued with US natural gas prices well off the peak set in early June. With US energy prices falling in June, this means this week’s US CPI print will be of particular interest. The first half of the month saw elevated prices whilst the latter part saw substantial declines. As it takes some time for these prices to feed into the consumer price basket, inflation is likely to remain elevated in June’s reading however the core CPI rate is expected to continue its decline on a year-onyear basis due to base effects.

US CPI to be in focus this week with June a month of two halves

Today sees the beginning of the scheduled closure of the Nord Stream 1 pipeline for maintenance with the key pipeline for continental European gas remaining closed until 21st July.

Geopolitical tensions between Russia and the EU remain fraught, there has therefore been some concern that the closure period may be extended by Russia in order to apply economic pressure on European capitals. The planned strikes in Norway would have also impacted gas exports however that has been averted, allowing energy prices to retreat slightly on Friday but remaining considerably higher for the week. The US enjoyed better economic data last week, allowing the US 2-year yield to rise by 27.2bps1, pricing in almost one additional Federal Reserve (Fed) rate hike. By contrast 2-year German bund yields were effectively unmoved as bond markets price in the energy supply fears and investors wagered that this would ensure the European Central Bank (ECB) retained a more cautious stance.

Differences in short dated yields are an important driver of currency returns and have been the dominant force in setting currency leadership this year. The growing gap between US and European 2-year yields led to further underperformance from the Euro versus the US dollar, meaning parity between the two currencies is now a near-term possibility.

Please check in again with us soon for further relevant news and market updates.

Please see below the Tatton Monday Digest, analysing key news stories impacting markets and economies around the world. Received this morning – 11/07/2022

Overview: Markets not yet reflecting broader public fears

The murder of past Japanese Prime Minister Abe is a reminder of how much we should value our public servants and politicians. We should be grateful that they are prepared to do a job we need so much. Whether they are exercising high office or merely representing us, they are invested with great expectation, much responsibility but little immediate power to meet those expectations.

The sad news from Japan compounded what was a politically turbulent week, both here in the UK and internationally. However, against this background, markets were benign. In the UK, it felt like market moves were linked to ructions in the Cabinet. However, sterling fared better through the week than the euro. Fears for Europe continue to worsen, driven by the current awful situation surrounding European energy prices. Two weeks ago, we pointed out how Europe’s gas and electricity prices had surged, especially for contracts covering this coming winter. Last week, the price situation worsened, which led to both French and German governments stepping in to save energy distributors. The German energy distributor-generator Uniper will be rescued with a government package, probably of around €8-9 billion. The rescue will potentially involve the German government taking an equity stake but also lending the company most of the proceeds (in the same manner as happened for Lufthansa during the pandemic – the government got its equity stake at a discount to the market price at the time).

It may not solve the problem in terms of generating enough electricity. Russia is constraining gas supplies, but France’s problems revolve around the lack of rainfall in the Alps and poor maintenance over many years. The drought has brought river levels to very low levels and those rivers are used as the cooling water supply for EDF’s old nuclear reactors. Output is the lowest in 30 years. Elsewhere, Bloomberg reported on 2 July that “Italy is set to spend almost 40 billion euros subsidising energy bills for consumers, while the UK put down some £37 billion to ease the impact on consumers. The nationalisation of Bulb alone will cost consumers about £2.2 billion”. For markets however, the issue is whether businesses, especially manufacturers will be immunised. Most are currently forced to pay market rates. As we mentioned last week, manufacturers average energy proportion of overall costs in 2019 was about 12%. This winter, electricity will be around four times that price. So, even if consumers are not hit directly by electricity price rises, they will face further inflation in goods. Businesses will likely see sales volumes decline. That would mean a Europe-wide recession, an outcome now clearly being priced by markets.

However, there is some good news coming from markets. The fall in bond yields (both fixed and ‘real’) is not surprising given the context, but provides some respite. More surprising perhaps is that general credit spreads are finishing the week broadly unchanged after spiking higher midweek. They’re still signalling a recession, but the government actions are giving hope that a pandemic-like response for businesses is in the offing. Meanwhile, the declines in industrial metal and agricultural commodity prices are alleviating some inflationary concerns. Risk assets in the US are stabilising as well following the sharp downswing in longer-dated bond yields. While the move came about because of growth concerns, it also seems a number of investors have bought back into bonds after being considerably underweight for a long period. Credit spreads also came down quite sharply, about 0.1% in yield falls for investment-grade credits. Also on a positive note, China is stepping up its fiscal push into the autumn with about $220 billion of new credit being raised by local governments. The swing-round in growth in China following the lockdowns has been as strong as could possibly been expected, and is set to go further. At this rate China may well reach the 5.5% yearly growth target for 2022 despite running at a near 10% annualised decline for the second quarter.

Market sentiment will depend greatly on the outturn for Europe. The Nord Stream pipeline annual maintenance shutdown finishes on 21 July and investors will be hoping Gazprom will resume a full supply after the unscheduled reductions that began in June. However, this week, French and German government willingness to step in to bail out the energy companies and protect consumers and businesses has certainly helped. As long as investors (and perhaps the European Central Bank) are willing to fund the increase in debt, Europe may be able to see this through without devastating economic damage.

UK government staggers on – but markets only shrug

As the working week starts, Boris Johnson is still Prime Minister in name if not in substance. The slow-motion collapse of the Conservative Party has become a psychodrama of the highest degree. A paralysed government is clearly a serious issue at any time. When inflation is rampant and real economic growth has deteriorated, one might expect it to be the worst possible time. And yet, capital markets barely registered the move.

A simple rationalisation might be that Johnson’s demise has long been telegraphed, and so former allies finally gathering for his execution is not big news. Last month’s narrow win in the vote of no confidence never really felt like a victory, and the writing has not so much been on the wall as all over the national news. While markets once evaluated Britain’s prospects by the relative hardness of its Brexit and its likely impacts, there is a sense now that the damage has already been done. The UK has the highest inflation rate in the G7 and one of the worst growth outlooks. Although energy and commodity price rises are not the fault of the UK severing ties with the European Union (EU), frictions with our largest trading partner have exacerbated the global supply chain issues.

Last week, the Bank of England (BoE) issued yet another dire warning on economic prospects. According to Governor Andrew Bailey, “Since the last financial stability report, the global economic outlook has deteriorated markedly”. Deterioration now seems to be a trend in BoE guidance, with recession either looming or already underway. So, there is a sense that change of government either will not or cannot change much about the near-term situation. Whoever ends up in charge of the Treasury come Autumn will likely want to bring in further tax cuts – but the space to do so has arguably already been exhausted by Sunak. Beyond which, any new measures will likely have minimal impact. While a full-scale loosening of fiscal policy anytime soon is unlikely, it is by no means out of the question – particularly given the uncertainty over who might end up at Number 10. That would force the BoE into more short-term interest rate hikes than currently priced (the market now expects another 0.75% over the next three meetings). While the sum of the fiscal easing and monetary tightening may end up being neutral for the UK economy, retail banks are tightening up loans against worsening balance sheets, and this would probably not help.

For almost all of the last century the UK benefitted from a positive flow of investment income. Our stock of overseas assets brought in more than we paid out on our liabilities. Now, in addition to a buying more goods and services than we sell abroad, we have to pay out interest and dividends. This introduces a huge risk to financial stability, as a sudden flight of capital would leave the system exposed. More inflation and a widening government deficit could trigger such an exodus. Moving “beyond Brexit” is critical to the UK’s prospects, but few think a new Conservative leader can. That is why are keeping an eye on the incoming government’s fiscal policy. We do not expect it to materially affect the UK’s position, but there is a tail risk that cannot be ignored. For sterling, this is balanced against the short-term upward pressure it could bring from a more aggressive BoE. All in all, the risks are finely balanced, if a little uncomfortable. The muted currency market response to this week’s chaos is therefore perhaps fitting.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

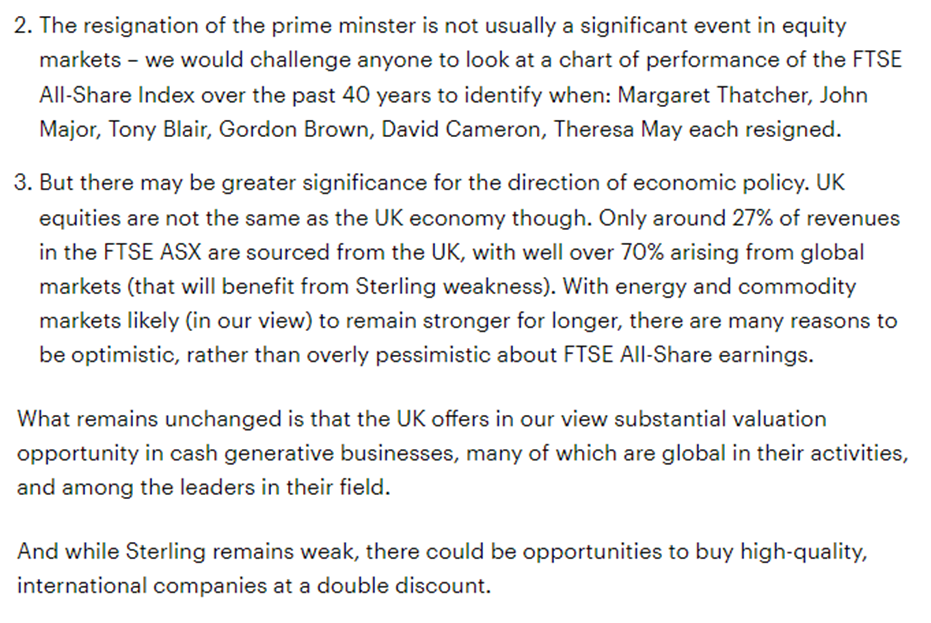

Please see below for some interesting insights from Invesco regarding the departure of Boris Johnson and its impact on the UK Economy. This was published yesterday, 07/07/2022:

Although replacing the Conservative party leader is unlikely to impact equities, the delay in implementing any further fiscal policies may adversely impact the UK Economy. The hope is that the decision won’t take too long.

Check back for further updates on this and other relevant content.

Please see below the Quarter 2 analysis from Brewin Dolphin which was released yesterday:

Geopolitical upheaval limiting supplies and exacerbating inflation has been the theme of Q2 and looks to continue into Q3. Brewin Dolphin do hint here that inflation may have reached its peak. This means the volatility we have seen lately may be with us a little longer.

The message is still to focus on long-term investment goals and remain invested while markets recover. Hopefully Q3 will bring more positive news.

Please check back with us soon for further updates.

Please find below, a Daily Investment Bulletin received from Brooks Macdonald this morning – 07/07/2022

What has happened

Despite fairly dire economic sentiment, equities made gains yesterday with European equities outperforming as they caught up on the late US rally on Tuesday night. Below the surface, investors continue to rachet up their probabilities of a recession with commodity prices falling and the US 10-year Treasury yield remaining below the 2-year yield, a historical precursor to recessions.

Boris Johnson

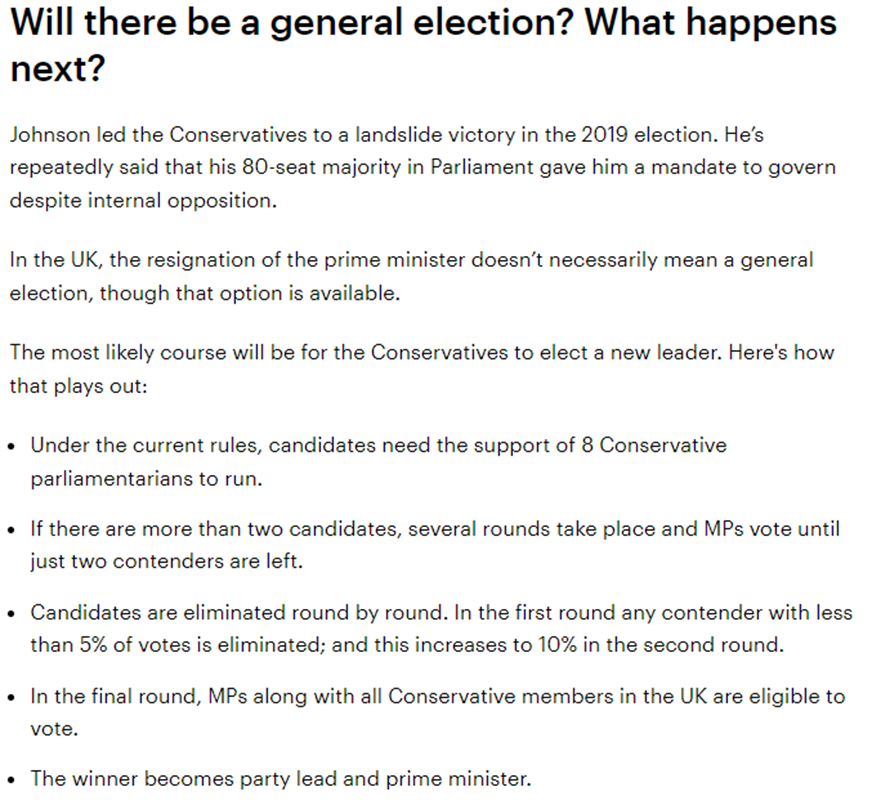

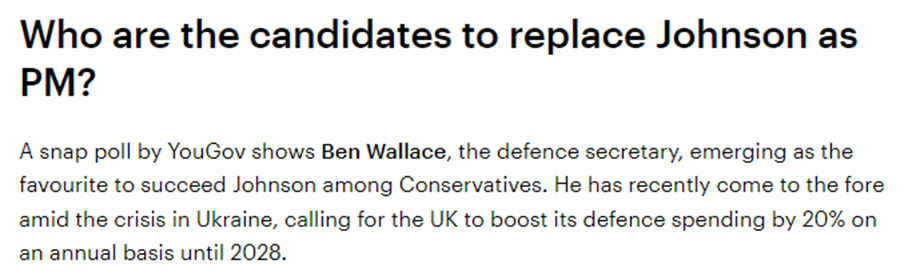

This paragraph has needed to be rewritten several times in the last hour but with the announcement that Boris Johnson will step down as Conservative leader, the scene is set for a leadership contest, the winner of which will become Prime Minister. Yesterday saw some fairly extraordinary scenes with a large number of ministers resigning but Boris Johnson remaining resolute that he retained a political mandate to govern after the large majority at the last general election. This morning, Downing Street officials briefed that Boris Johnson would resign as Conservative leader later today whilst remaining caretaker Prime Minister until the election process is concluded in the autumn.

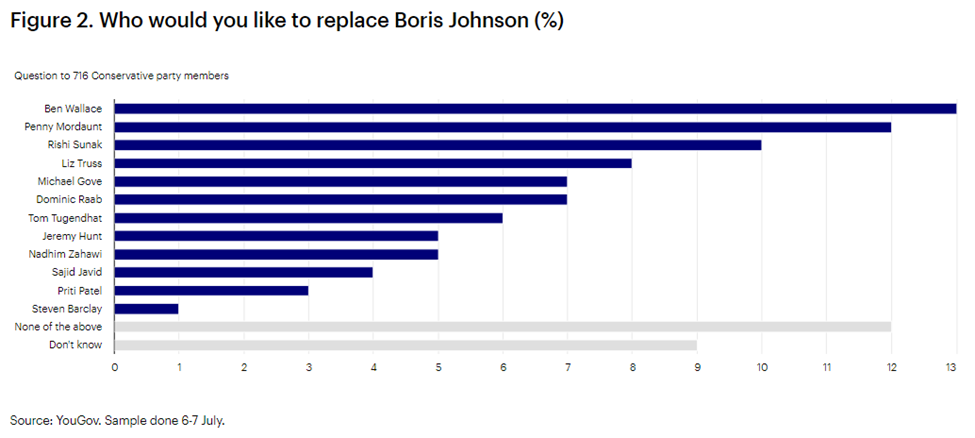

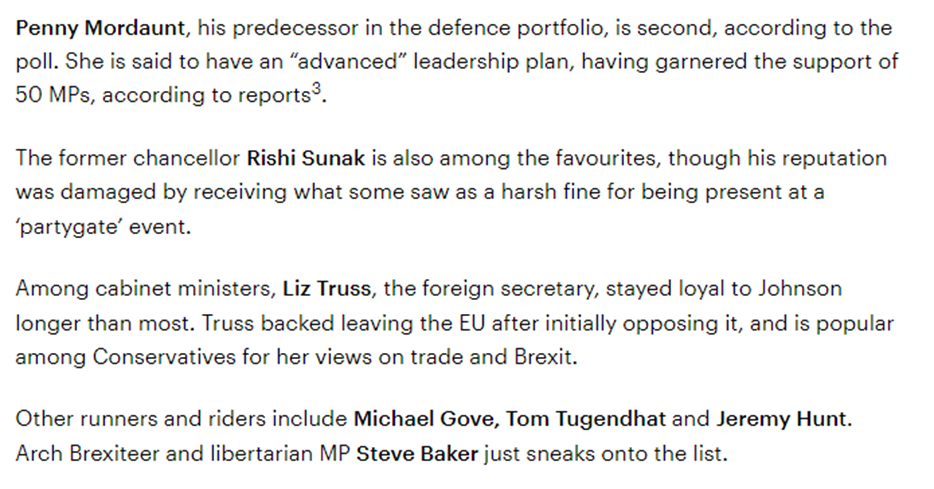

What next

Sterling has seen a small bounce this morning versus the major currency pairs however until a clear leader emerges from the pack of contenders, the true economic and political impact of the change in leader will be hard to price in. At this stage we probably shouldn’t read too much into the bookmakers odds however Penny Mordaunt is leading. Mordaunt has distanced herself from the Prime Minister for several months, which could prove a factor amongst MPs as well as the Conservative membership, and pairs pro-Brexit leanings with liberal Conservatism – potentially appealing to both wings of Tory MPs. Conservative MPs will debate the benefits of each candidate, voting until two candidates remain, with the ultimate winner chosen by Conservative party members.

What does Brooks Macdonald think?

Back in 2019, sterling’s price was closely correlated with the perceived probability of a softer or harder Brexit. In recent weeks, with global central banks opting for differing levels of aggression in tackling inflation, currency pairs have largely been determined by expected differences in interest rate policy. This leadership contest however will undoubtedly draw the attention of currency markets given a) the new leader would have up to 2 years until the next general election b) EU/UK relations remain highly uncertain and c) the cost of living crisis makes fiscal policy even more important.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

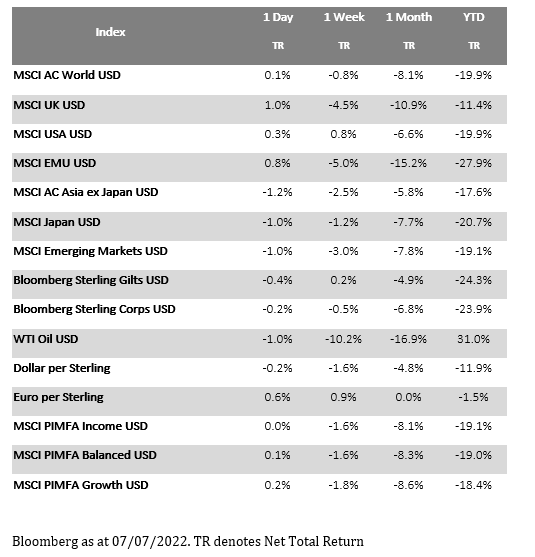

Please see this weeks Markets in a Minute update from Brewin Dolphin received late yesterday:

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.