Please see below the latest daily investment bulletin from Brooks Macdonald, which was published and received this morning (14/07/2022):

What has happened?

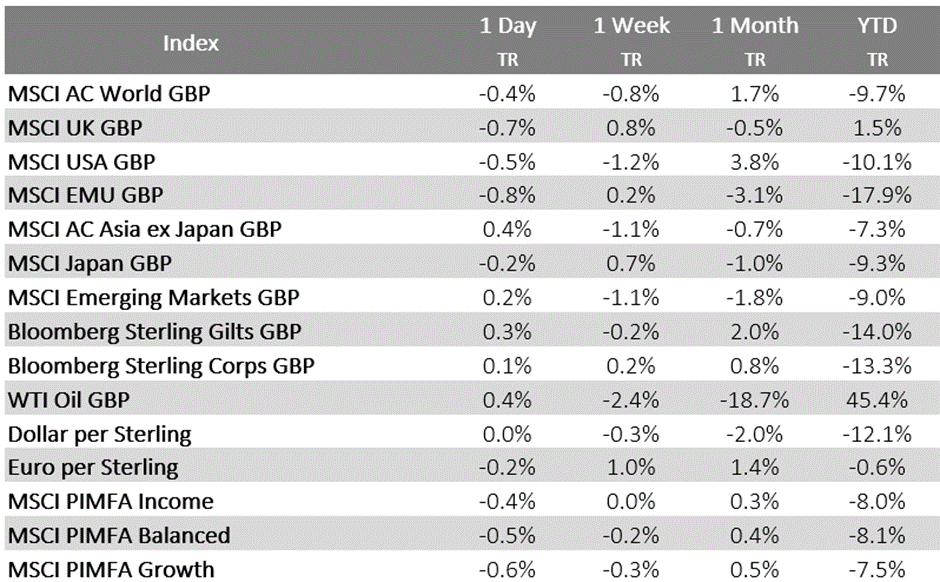

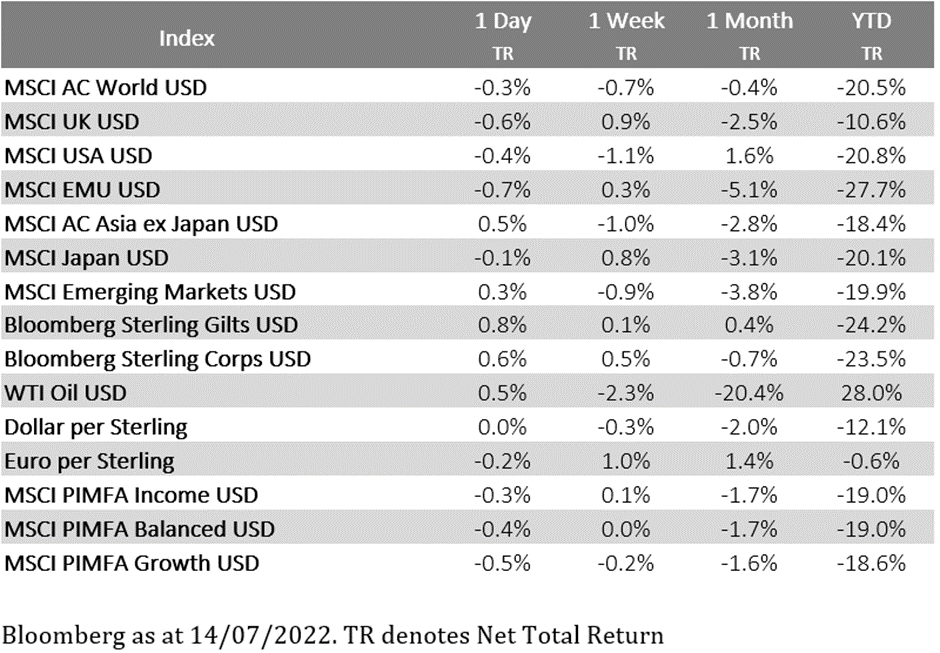

US equity futures dipped sharply after the release of the June CPI print, however the market staged somewhat of a comeback to end the day only mildly in the red. The bond market was less sanguine however, with a surge higher in the US 2-year bond yield as investors priced in more aggressive Fed rate hikes.

US CPI

Both the headline and core CPI readings came in higher than the market was expecting. The month-on-month figures saw a dramatic 1.3% increase in the headline and 0.7% in the core reading. Both of these 20bps more than the market was expecting. The market took little comfort from the components of the CPI surge, with a broad showing of inflationary pressure amongst the basket as the year-on-year headline CPI figure crept above 9%. The sharp moves in bond markets mean that investors are pricing in around 90bps of rate hikes at the July meeting, effectively meaning that investors feel a 1% hike is more likely than a 75bp hike. Adding to this grim mood within bond markets, Cleveland Fed President Mester provided a suitable summary of the report as ‘uniformly bad – there was no good news in that report at all’.

Bond Market moves

In March of this year we were debating the impact of a slight intraday inversion of the 2s10s yield curve, as I write the 2-year yield sits at 3.22% and the 10-year yield at 2.97% – a pretty clear statement from the bond market that they believe the Fed will raise rates in the short term but need to cut them in 2023. For context, this is the largest inversion of the yield curve that we have seen since 2000. This surge in US bond yields was enough to finally lead the Euro to fall below parity with the US dollar however the Euro recovered a small amount of ground by the end of the day and remains hovering around 1 Euro to the dollar.

What does Brooks Macdonald think

June’s CPI number was always going to be messy given the moves that were taking place in commodity markets during the month. Whilst yesterday’s report wasn’t particularly enjoyable reading, the broader context is that commodity prices have fallen quite substantially. Compared to three months ago, oil is down over 10%, copper almost 30% down and wheat down 25%. It will take some time for these falls to feed into the consumer inflation basket but should the commodity sell-off continue, better inflation reports will lie ahead.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Carl Mitchell – Dip PFS

Independent Financial Adviser

14/07/2022