Please see below Brooks MacDonald Daily Investment Bulletin, received yesterday afternoon, 03/08/2022:

What has happened

Market movements closely tracked the take-off and landing of Speaker Pelosi’s plane as she travelled to Taiwan amidst strong condemnation from Beijing. With Pelosi’s plane safely landed, US Treasury yields ended sharply higher on the day, reversing Monday’s declines. Against this backdrop US equities struggled, posting modest losses on the day.

Taiwan

The safe landing of Pelosi’s aircraft led to a surge of optimism within bond markets however there are still some economic and political consequences to be fully priced in. China has announced a series of military drills over the coming days in what is seen as one of the strongest shows of force this century. China has also imposed targeted sanctions on Taiwan including exports of natural sand and food imports. The military exercises, and missile tests, are expected to keep both the US and China on edge over the coming days but markets took comfort from the relatively subdued Chinese response.

Corporate earnings

A series of strong earnings results helped market sentiment early on in the trading session yesterday. Uber and Lyft both saw strong earnings as did Maersk that is a beneficiary from the recent supply-chain disruption. Caterpillar, widely seen as a cyclical bellwether, produced downbeat forecasts, citing inflation and supply led constraints. Caterpillar does seem to have a bit of a reputation for downbeat economic forecasts however inflation and supply-side issues are undoubtedly weighing on industrial names. BP meanwhile raised its dividend and increased its buyback programme in response to strong earnings. These earnings have spurred another call for increased windfall taxes however until the Conservative leadership contest is settled, the windfall tax remains on hold.

What does Brooks Macdonald think

Amidst the earnings and geopolitical risks yesterday, a series of Fed speakers also threw cold water on expectations of an imminent pivot in Federal Reserve policy. The movements in both the bond and equity markets were quite remarkable in July given the lack of a clear change in policy from the US central bank. President Bullard said that the US economy could avoid a recession even if the Fed continues to raise rates and President Daly said that the Fed was ‘nowhere near’ complete on tackling inflation. Such words helped the rise in bond yields yesterday even if investors were mainly focused on tracking the path of Pelosi’s flight.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from us and leading investment houses.

Please find below, a market update received from Brewin Dolphin yesterday evening – 02/08/2022

Strong tech earnings boost investor sentiment

Equities rose last week as strong second quarter earnings from technology giants Amazon, Apple and Alphabet boosted investor sentiment.

US indices managed to shrug off news of a contraction in US gross domestic product (GDP) and another 75-basis point (bps) interest rate hike. The S&P 500 gained 4.3%, the Dow rose 3.0% and the Nasdaq surged 4.7%.

The pan-European STOXX 600 and the FTSE 100 advanced 3.0% and 2.0%, respectively, after data showed the eurozone economy expanded by more than expected in the second quarter.

In contrast, Japan’s Nikkei slipped 0.4% after the government downgraded its forecast for economic growth in the fiscal year ending March 2023 from 3.2% to 2.0%, citing slowing overseas demand and rising consumer inflation.

China’s Shanghai Composite eased 0.5% as a high-level meeting of the Communist Party omitted mention of its GDP growth goal and instead said China should “strive to achieve the best possible results”.

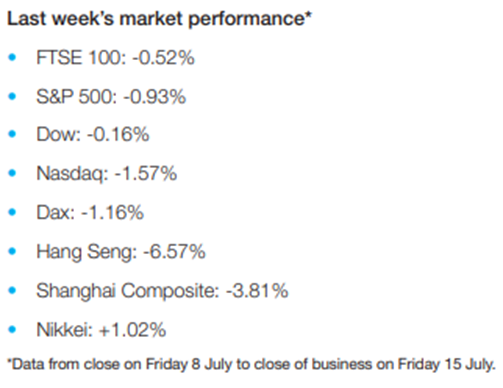

Last week’s market performance*

• FTSE 100: +2.02%

• S&P 500: +4.26%

• Dow: +2.97%

• Nasdaq: +4.70%

• Dax: +1.74%

• Hang Seng: -2.20%

• Shanghai Composite: -0.51%

• Nikkei: -0.40%

*Data from close on Friday 22 July to close of business on Friday 29 July.

US indices fall after best month since 2020

After July proved to be their best month since 2020, US indices fell on Monday (1 August) as investors feared US House speaker Nancy Pelosi’s potential visit to Taiwan could worsen tensions between China and the US. The S&P 500 slipped 0.3%, the Nasdaq lost 0.2% and the Dow shed 0.1%. Asian stocks suffered on Tuesday, with the Shanghai Composite and Hang Seng down 2.3% and 2.4%, respectively, after Beijing reportedly said it would retaliate with “forceful measures” if the trip goes ahead.

In economic news, data from S&P Global showed UK manufacturing output contracted for the first time in over two years in July because of reduced intakes of new work, weaker market demand, difficulties in sourcing components and transport delays.

The FTSE 100 was up 0.1% at the start of trading on Tuesday, while the Dax opened 0.6% lower.

US slips into a technical recession

Figures released last week showed the US economy shrank for a second consecutive quarter, meeting one of the most common criteria for a technical recession. GDP shrank by an annualised 0.9% in the second quarter, following a 1.6% contraction in the first quarter, according to the Commerce Department. Economists polled by Reuters had forecast GDP would rebound at a rate of 0.5% in the second quarter.

While back-to-back quarterly GDP contractions meet one definition of a recession, the National Bureau of Economic Research is responsible for making the official call on whether the economy is in a recession. One of the factors it looks at is employment, which remains strong.

Treasury secretary Janet Yellen stated last week: “Most economists and most Americans have a similar definition of recession: substantial job losses and mass lay-offs, businesses shutting down, private-sector activity slowing considerably, family budgets under immense strain. In sum, a broad-based weakening of our economy. That is not what we’re seeing right now.”

Fed hikes rates by another 75bps

The US Federal Reserve approved its second consecutive 75bps interest rate hike last week, taking its benchmark rate to a range of 2.25-2.5%. Investors were largely expecting the move and were cheered by relatively dovish comments by Fed chair Jerome Powell that future rate increases would depend on the data.

“As the stance of monetary policy tightens further, it likely will become appropriate to slow the pace of increases while we assess how our cumulative policy adjustments are affecting the economy and inflation,” he said.

Tourism boosts eurozone economy

In the eurozone, a surge in tourism helped the economy expand by more than expected in the second quarter. According to Eurostat’s preliminary flash estimate, GDP grew by 0.7% when compared with the previous quarter, much higher than the 0.1% growth forecast by economists. France, Italy and Spain all saw an expansion in GDP, whereas Germany’s economy stagnated.

Inflation in the eurozone is expected to hit a new high of 8.9% in July, up from 8.6% in June, driven by price rises in energy and food. There are concerns this could lead to interest rate rises and weigh on growth during the second half of the year. There are also fears that a reduction in gas flows through the Nord Stream 1 pipeline from Russia to Germany could spark a recession.

Elsewhere, the European Commission’s economic sentiment indicator for the euro area fell from 103.5 in June to 99.0 in July, below its long-term average. Industrial confidence fell by 3.5 points, while sentiment in the services sector declined by 3.4 points.

UK consumer borrowing doubles

Here in the UK, data from the Bank of England showed consumers borrowed a net £1.8bn in June, double the £0.9bn in May, most of which was on credit cards. The annual growth rate for consumer credit rose to 6.5%, the highest level since before the pandemic.

The figures have raised concerns that people are resorting to borrowing to fund the rising cost of living. Gas and electricity bills for some of the most vulnerable households could reach an average of £500 a month in January, according to BFY Group, an energy management consultancy.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see yesterdays Brooks Macdonald Daily Investment Bulletin received late yesterday:

What has happened

Risk appetite was hit yesterday by the upcoming visit by US House Speaker Pelosi to Taiwan as part of her tour of Asia.

Bond markets

With geopolitical tensions adding to fears over a global recession, bond yields fell yet again yesterday with the US 10-year Treasury yield now trading at 2.55%, almost 15bps lower than it was at the start of Monday. With economic growth risks still front and centre, the yield curve remains inverted with the 2-year yield around 30bps higher than the 10-year yield. European bond yields also saw declines yesterday as weaker German retail sales and Italian manufacturing PMIs worsened sentiment and caused investors to dial back their expectations of ECB tightening.

Commodities and Supply

With yesterday’s risk off tone, energy prices fell substantially, with the Brent international oil benchmark moving below $100 per barrel. These growth concerns were spurred not only by the recent weaker western data, but also Monday’s data releases from China. Few commodities were spared with industrial metals and agricultural goods both declining. There was some good news in the commodities arena as the first grain shipment from Ukraine since the war began departed a Ukrainian port amidst hopes that a partial return of Ukrainian exports will help boost global supply. Yesterday’s US ISM index contained some interesting reading, but perhaps of most importance to a market looking for signs of inflationary pressures easing, the prices paid measure fell dramatically from last month’s measure. This chimes with recent earnings results that suggested supply chain pressures were easing in certain areas. It may be too early for this to have filtered into the July CPI data released next week in the US but there are increasing signs that some of the post-pandemic distortions are being removed.

What does Brooks Macdonald think

Pelosi will be the highest-ranking US official to visit the island in 25 years and is likely to raise tensions between the US and China even with the US reassuring Beijing that the official US position remained one of strategic ambiguity. Recent rhetoric from Biden has suggested that the US would defend Taiwan in the event of an invasion though the White House has been at pains to stress that the official policy has not changed.

Please continue to check back for further updates.

Please see the below article from Church House Investment Management which was received this morning (02/08/2022) and provides an insight into market cycles, and the things to remember as a long-term investor.

Whether its shifting interest rates, soaring inflation, or heightened geopolitical tension, there’s a lot of short-term risk and uncertainty on the table right now.

The reality is, investors are quite right to be cautious – a look at the volatile performance of any major index since the beginning of this year alone can show you that.

With all this in mind, it’s hardly surprising that in May, Bank of America reported the average cash holding of a global asset allocator to be at its highest level since 9/11.

But should this really be the case?

A major part of any investment professional’s job should be to see the forest when the rest of the market sees the trees. As Warren Buffett, the Sage of Omaha himself, once said: “Be fearful when others are greedy and greedy when others are fearful”.

With so much value on the table in today’s period of economic retraction, there’s a strong argument to be made that right now is the time for investment professionals to be brave. Indeed, rather than hide in cash, these individuals must instead ask themselves a critical question: What can I do today that my clients will thank me for in five years’ time?

I suspect in this inflationary time, the answer won’t be, ‘sitting in cash.’

It’s difficult but rather than peering into the seemingly bottomless abyss of bad news, we should lift our heads, look across to the other side, and consider what opportunities we can exploit in the current volatility.

Don’t panic

The bottom line is, markets are cyclical.

That doesn’t mean they are easy to predict, but it does mean they tend to follow a sequence of stages over time. It’s the macro events that are unknown and that trigger the move from one stage to the next.

After a prolonged period of ultra-loose monetary policy and escalating equity valuations, a move from market “euphoria” into bearish territory was inevitable coming into 2022. However, it’s clear now that post-pandemic inflation, central bank tightening, and uncertainty around the Ukraine crisis were together enough to catalyse the beginning of this transition.

While the days of simply investing in something indiscriminately and watching its value rise may now be over, markets have made this transition time and time again throughout history, and every time, it has been possible to enhance returns by choosing the right investments while they were trading at a discount.

Spotting value

The idea that bottomed-out markets offer an opportunity to scoop up bargains to maximise upside potential is no doubt an attractive one although, in practice, this approach is by no means easy.

Increasingly short-term reporting requirements and a natural tendency to focus on the news headlines rather than individual stock fundamentals tend to make us blind to opportunities or shrink from making the bold call to invest.

Maybe it’s the memory of that saying from 2001 that a stock that’s fallen 90% is one that fell 80% and then halved. Whatever it is that deters us, being greedy when others are fearful isn’t easy but you wait, at some point after markets have recovered some smart aleck will tell you, “The easy money has been made”.

Making the best of it

There’s no question that the responsibility of managing someone’s money can be a daunting one at a time when everything seems to be collapsing in value. However, it’s important to keep perspective and take Warren Buffet’s advice – markets have recovered many times before and they will again, but you can’t partake in a market recovery if you’re invested in cash.

It’s critical to stick to the fundamental principles of investing and leverage today’s weakness as an opportunity, always asking oneself: What can I do today that my clients will thank me for in five years’ time?

Please continue to check our blog content for advice and planning issues from us and leading investment houses.

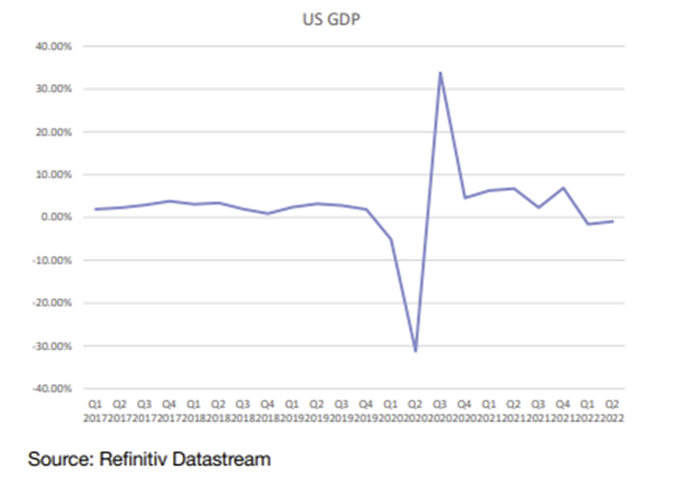

For a second consecutive quarter, the US economy shrank in real terms. Yet the US Federal Reserve (Fed) raised interest rates by another 0.75% last Wednesday because the US economy is too strong. Yet, despite all of the bearishness, markets put in a stonking performance last week. Pretty much all equity and bond markets ended with asset prices at higher levels. In particular, corporate bonds did well, even in Europe. Given that much of the fear in markets revolves around a potential credit crunch through Europe’s winter, many commentators have seen this as probably only a temporary respite.

Europe is currently facing a worse outlook than other areas and much of the news worsened last week. Eurozone inflation for June was higher (marginally) than expected at 8.9% year-on-year. It will be even worse next month because energy prices just keep rising. After Gazprom came up with an excuse to not deliver as much natural gas to Germany as was promised, gas prices went up to new records. We are undoubtedly in a ‘cold’ war again. Europe’s plan to cut gas use by 15% until 2023 is important. But as of now, no concrete plans have been proposed by any country. We only know energy caps will focus the reduction on industry, and that households will not face cuts, even if they are not shielded from price rises. Until we see how businesses can be protected for this winter, investors will stay worried about the potential for unbearable costs.

Investors have been both bearish and uncertain for a long time, even though valuations on many assets have become substantially cheaper. When investor sentiment is poor, it can be quite difficult for markets to fall further without the news getting much worse. So, while there were stories which worried us, much of it told us essentially what we already knew (like the inflation data and the US GDP data) or had good reason to expect (such as the slow Russia gas supply). On the positive side, Jerome Powell sounded less hawkish than expected after the US interest rate rise. Meanwhile China’s politburo pressed for more support for their economy. A bull market isn’t likely to set in anytime soon and, almost certainly, not until the energy price squeeze dissipates. Nevertheless, at least last week, it felt like it wasn’t getting worse.

Reasons to trust in the Fed’s tinkering

As mentioned, last Wednesday the Fed furthered its monetary tightening agenda, pushing interest rates up another 0.75%, following the 0.5% rise in May and the first 0.75% bump in June. Capital markets expected as much, but the big news came from the post-meeting press conference, where Fed chair Jay Powell hinted at a change of tack. As the Fed continues to tighten policy, “it will likely become appropriate to slow the pace of increases”, he said.

That comment buoyed markets. Short-term bonds rallied and the S&P 500 gained 2.6% in Wednesday trading. The Nasdaq – dominated by America’s big tech companies highly sensitive to interest rates – gained 4.1%. Judging from these moves, the market consensus seems to be that the Fed will reaching ‘peak’ interest rates soon and likely cut them in less than a year. The Fed has good reason to do so, judging by the latest economic data. Demand has clearly slowed, and US GDP contracted in inflation-adjusted (‘real’) terms in the first half of this year, which would meet some people’s definition of a recession. Admittedly, Powell pre-emptively noted that, even if the US economy had been in a technical recession for the first half of this year, it would not be a contraction in any normal sense of the word. Even so, the economy is clearly slowing down. The big question for the Fed, and indeed all of us, is what this means for inflation.

In normal circumstances, it would be a no-brainer that slowing growth – let alone potential recession – would translate into slower price rises. But the current global stagflation is no normal circumstance. Sharp supply shortages need to be met with equally sharp demand contractions for prices to stay stable. And, with unemployment still at historically low levels, the Fed is concerned with stopping the damaging wage-price spiral above all else.

Even here though, signs look good. Inventory data on US retailers and wholesalers show a significant uptick in inventories. While retailers have a bit to go before their stock levels match pre-pandemic levels, wholesalers have higher inventory levels relative to trend than at any point in the last 30 years. On the flipside, retail inventories are significantly lower – the latter having come down from high points earlier in the year. This suggests that final consumer demand has fallen more sharply than expected, causing retailers to reduce their orders and leaving wholesalers with unwanted supply. That is bad news for them, but it points to a sharp reversal of the supply-demand imbalance seen last year.

One of the biggest sources of US inflation over the past couple of years has been the housing market, particularly outside of the big cities. This drove a strong period for residential construction, adding to the 2021 growth spurt and driving up lumber prices (an indicator of housing construction). In the past couple of weeks, lumber prices have taken a downturn. This suggests slowing activity which, considering the construction sector is a huge employer, will likely have big knock-on effects for overall inflation. Mortgage providers have been upping their borrowing rates and tightening lending standards for fear of recession and the dearth of payments that might bring. This suggests lenders think house prices are unsustainable in the current environment. Mortgage rates have fallen quite sharply in the past month but are still well above 5%. Residential construction will likely struggle to rally from here, putting downward pressure on both growth and inflation.

The Fed’s actions have undoubtedly contributed to these trends and will continue to do so. The problem is that monetary policy works on a long lag. Further tightening from this point will not bring down growth and inflation in the next couple of months but rather next year and beyond. If the futures markets are right, inflation is already set to come down quite sharply to a much more normal level by then. Any extra tightening the Fed does in that time will likely bring down future growth more than it will tame short-term price rises. Powell and his team are aware of this, and this is probably one of the main reasons their rhetoric is now moderating. This is not to say the Fed is done with rate rises, but that its aggressive stance has likely peaked.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

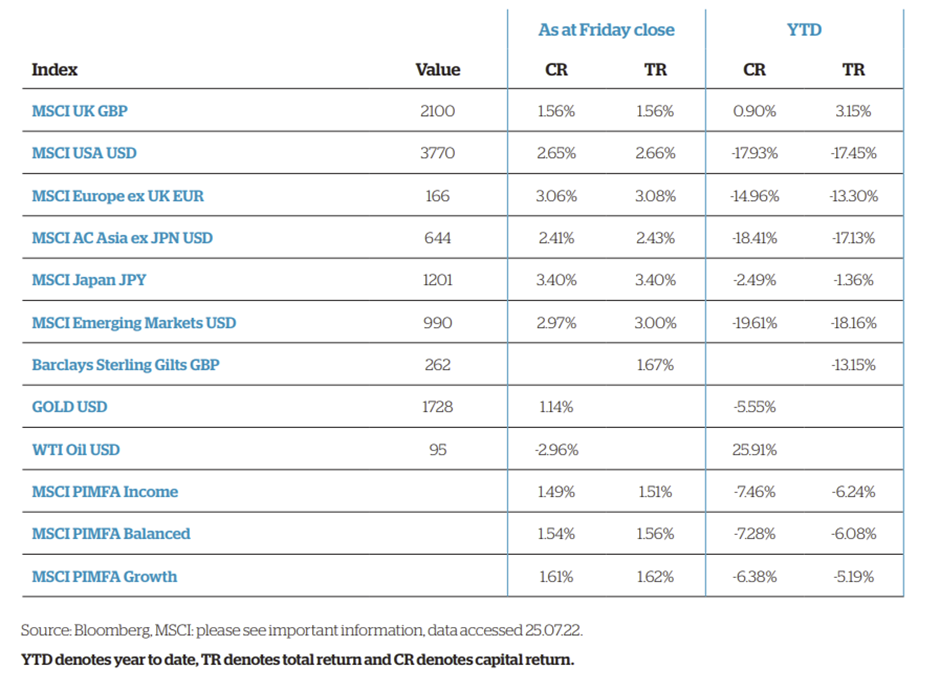

Please see below, a weekly market commentary received from Brooks Macdonald yesterday afternoon – 25/07/2022

Europe was in focus last week with Nord Stream 1’s reopening, Italian elections and the European Central Bank’s (ECB) hike all competing for attention

This week the US Federal Reserves’ (Fed) meeting and US Q2 Gross Domestic Product (GDP) will set the tone as we close out a volatile July

US and European earnings ramp up this week with the majority of companies beating expectations so far

Europe was in focus last week with Nord Stream1’s reopening, Italian elections and the ECB’s hike all competing for attention

Economic growth expectations remained a key driver of market moves last week with weaker data continuing to paint a picture of a slowdown in the US and the rest of the world. As a result bond yields fell, helping growth focused equities outperform already strong gains within the European and US stock markets.

Last week was dominated by European headlines, be those around the resignation of Italy’s Prime Minister, the restarting of the Nord Stream 1 pipeline or the ECB which scrapped its forward guidance in favour of a 50bp hike1 . This week the US will be in focus with the Federal Reserve concluding its rate setting meeting on Wednesday where it is widely expected to hike rates by 75bps2. Investors will be looking at how Fed Chair Powell balances the inflation risks with economic growth risks particularly given the weaker initial jobless claims of recent weeks which suggests a deterioration in the employment outlook. With the market now pricing in a change in tone at the Fed at the start of next year, with subsequent interest rate cuts, how the Fed addresses this elephant in the room is arguably more important than the size of Wednesday’s hike.

This week the US Fed’s meeting and US Q2 GDP will set the tone as we close out a volatile July

With recession fears remaining central to market moves, investors will also be watching the US GDP number on Thursday, which if negative means the US has entered a technical recession after contracting in Q1 of this year. It is worth stressing the technical nature of this recession, should it occur, given Q1 US GDP was driven lower by global factors rather than US factors. Equity markets are likely to look through such an outcome however it may have second order impacts on consumer demand should it solidify consumer negativity about future economic growth.

US and European earnings ramp up this week with the majority of companies beating expectations so far

All of this alongside a bumper week for US and European earnings means that the week will be a fitting end to a volatile July. So far in the earnings season, around 20% of US companies have reported with the majority beating earnings expectations. Many companies have painted a more cautious picture of 2023 however this largely chimes with the market’s broader macroeconomic thinking and therefore has been accepted by investors without too much concern.

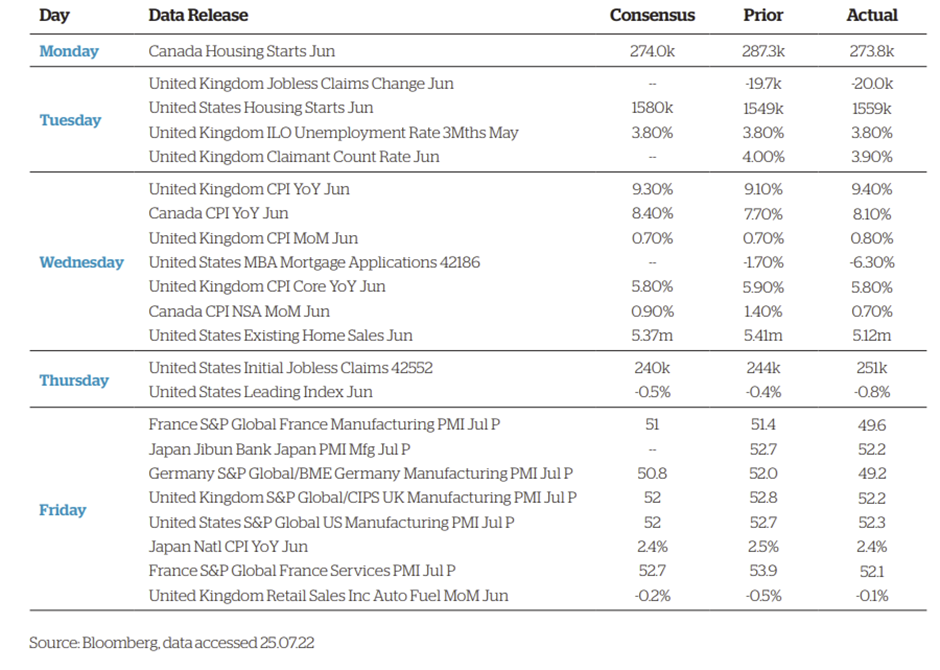

Economic indicators (week beginning 18 July)

Economic indicators (week beginning 25 July)

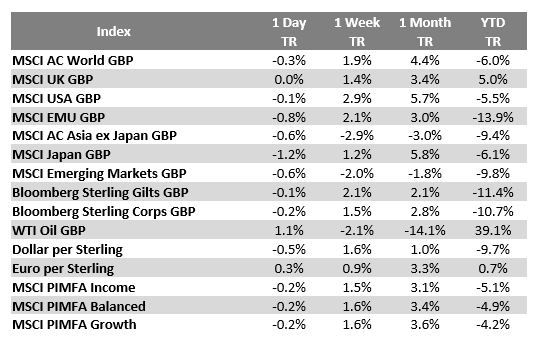

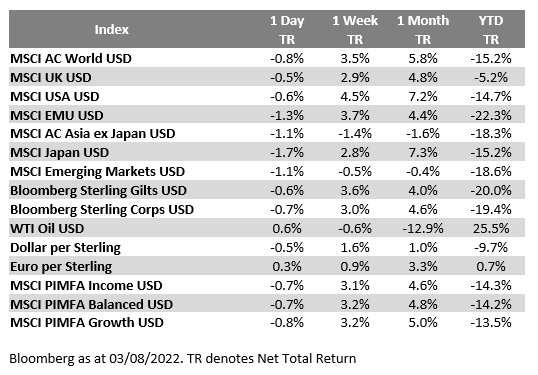

Asset Market Performance

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below the latest Blackfinch Group – Monday Market Update, which was received this morning (25/07/2022):

UK COMMENTARY

UK inflation hit a fresh 40-year peak of 9.4% in June, according to the Office for National Statistics (ONS). This was the ninth consecutive month-on-month rise for the consumer prices index, as the cost-of-living crisis worsened.

Purchasing Managers Index (PMI) survey data for the manufacturing sector – which measures manufacturing output – fell to 49.7 in July, below the 50 mark that indicates an expansion. This was the first time the measure has fallen since the first pandemic lockdown in May 2020.

The ONS reported a record surge in Britain’s borrowing costs in June, pushed up by soaring inflation. This put the government’s budget deficit on course to exceed £100bn this year, almost double its pre-pandemic level.

House prices across the UK rose at an annual rate of 12.8% in May, up from 11.9% in April, according to the ONS. This pushed the average UK house price to £283,000 in May, £32,000 higher than the same time last year.

NORTH AMERICA COMMENTARY

US existing home sales were weaker than expected in June, falling 5.4%. This was the slowest pace of sales since June 2020, when sales plunged at the start of the pandemic.

EUROPE COMMENTARY

The European Central Bank (ECB) raised interest rates by a bigger-than-expected 0.5%. This was the central bank’s first rate hike in 11 years and was prompted after inflation for the eurozone reached 8.6% in June, far above the ECB’s 2% target.

The European Commission proposed a major gas demand reduction plan to prepare the European Union (EU) for supply cuts from Russia. It urged EU member states to cut gas use in Europe by 15% until next spring.

Eurozone’s PMI data signalled a contraction in business activity in July, adding to a string of poor economic results. S&P Global’s interim composite PMI fell from 52.0 in June to 49.4 in July, significantly below economist’s forecasts.

RUSSIA COMMENTARY

Russia resumed critical gas supplies to Europe through Germany, reopening the Nord Stream gas pipeline. However, uncertainty over whether Europe could avert a winter energy crisis persisted.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

An educational article received from A J Bell today:

Help, I’ve nearly breached my lifetime pensions allowance and my 75th birthday is near

Thursday 21 Jul 2022

I turned 70 last month and haven’t yet started taking an income from my pension. My fund enjoyed 20% growth last year and as a result I’m perilously close to the lifetime allowance. I’m thinking about withdrawing some money from my SIPP and putting it in an ISA to keep below the lifetime allowance as my 75th birthday approaches. Is this sensible?

Robert

As with many things in this complicated part of pensions, the answer is ‘it depends on your circumstances’.

The lifetime allowance, currently set at £1,073,100, is designed to limit the amount you can save tax-efficiently in UK pensions. If you breach your lifetime allowance you will pay a lifetime allowance charge on the excess.

This lifetime allowance charge will be:

25% if you leave the excess in your pension and take it as an income, with income tax levied on top of that;

55% if you take the excess as a lump sum, with no income tax due.

There are a number of ‘benefit crystallisation events’ that trigger a lifetime allowance test, including taking your 25% tax-free cash, buying an annuity or entering drawdown.

There is also a test at age 75 which is designed to capture any growth in your crystallised fund value, plus any as-yet uncrystallised funds you have.

For example, at age 70 someone might have crystallised £750,000 in drawdown and £250,000 by taking their 25% tax-free cash – £1 million in total. This would use up 93.18% of their lifetime allowance (assuming they are entitled to the standard lifetime allowance of £1,073,100).

If over the next five years their fund increases in value to £1.3 million then the age 75 test will capture that growth – meaning a lifetime allowance charge would be payable.

The simple answer to the question ‘could you take money out of a pension to avoid the age 75 test’ is ‘yes’. However, whether that will benefit you or not will depend on your circumstances. You certainly won’t be able to dodge the lifetime allowance test altogether.

If your investments have gone up by 20% in single year that suggests you’ve taken a fair amount of risk – and therefore your investments could also fall in value significantly in any given year. If this happens, a large withdrawal designed to reduce your tax burden may in fact increase your tax burden.

This is probably easiest to illustrate with an example. Take someone aged 74 with a crystallised £1.2 million fund who withdraws £200,000 to avoid paying a lifetime allowance charge on their drawdown fund at age 75.

For simplicity, let’s assume this is their only income and so they pay almost £70,000 in income tax – including paying higher and additional-rate tax on portions of the withdrawal.

Over the year their investments drop in value by 20%. Based on the original value of £1.2 million, this would imply at age 75 their fund would have been worth £960,000 had they done nothing – well below the lifetime allowance.

They could then have managed their income after the age of 75 to minimise their tax liability – for example by ensuring they never pay more than basic-rate income tax.

If passing money onto loved ones is a consideration, you should also bear in mind that pensions are usually free from inheritance tax and can be passed on tax-free to loved ones if you die before age 75. After age 75, income tax is payable at the beneficiary’s appropriate rate – but withdrawals can be managed to minimise the tax due.

Money held in an ISA, on the other hand, is always free of income tax but will form part of your estate for IHT purposes (although it is possible to gift money while you’re alive to reduce any potential IHT bill).

In short, this is far from straightforward and whether your approach reduces the amount of tax you pay will depend on circumstances.

For this reason, I’d strongly recommend engaging the services of a regulated adviser, who can help you make the best decision based on a review of your entire financial position.

Comment

I think the starting point is that if you have breached the Lifetime Allowance this means you have good pension assets, that is great news.

You have a wide variety of options, and the right advice will be based on your own personal circumstances, objectives and risk profile etc.

In this situation do take independent financial advice.

Please see below this week’s Markets in a Minute article from Brewin Dolphin received this morning – 20/07/2022

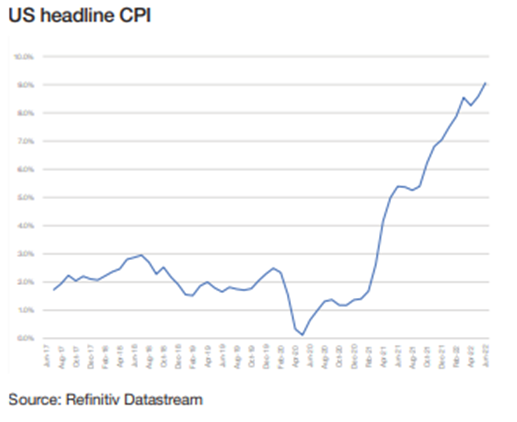

Stocks volatile as US CPI tops forecasts

Stock markets were volatile last week as US inflation rose at a faster rate than expected and the European Commission lowered its growth forecasts.

US indices fell sharply on Wednesday after the Labor Department reported that the consumer price index (CPI) had hit a new 41-year high in June. However, separate inflation data released on Friday was interpreted as good news by investors and helped to limit losses for the week. The S&P 500 finished the week down 0.9%, while the Dow and Nasdaq slipped 0.2% and 1.6%, respectively.

The pan-European STOXX 600 fell 0.8% and Germany’s Dax declined 1.2% amid ongoing concerns that Russia may extend the closure of the Nord Stream 1 gas pipeline to Germany. The FTSE 100 eased 0.5% as an unexpected expansion of UK gross domestic product (GDP) helped to limit losses.

In China, the Shanghai Composite fell 3.8% as GDP in the second quarter grew by just 0.4% from a year earlier, down from a 4.8% expansion in the first quarter.

Rising oil prices boost energy shares

The price of Brent crude oil rose 2.6% on Monday (18 July) after a meeting between US president Joe Biden and Saudi Arabia’s Crown Prince Mohammed bin Salman didn’t result in a pledge to raise oil output. This boosted energy shares and helped the FTSE 100 climb 0.9% on Monday. In the US, the S&P 500 slid 0.8% after Bloomberg reported that Apple was planning to slow hiring and spending growth next year.

The FTSE 100 started Tuesday’s trading session in the red as investors digested the latest UK jobs data. The unemployment rate held at 3.8% in the three months to May, while the number of people in employment rose by 296,000 – the biggest increase since the three months to August last year. However, regular pay in real terms (excluding bonuses and adjusted for inflation) was 2.8% lower than a year ago.

US consumer inflation hits 9.1%

Last week saw the release of the closely watched US CPI, which showed consumer prices rose by 9.1% in the 12 months to June, the fastest pace since 1981. This was higher than the 8.6% jump seen in May and the 8.8% rise forecast by economists.

Gasoline prices surged by 59.9%, while the price of food and shelter increased by 10.4% and 5.6%, respectively. Core CPI, which strips out volatile food and energy costs, Markets in a Minute 19 July 2022 rose by 5.9% from a year ago, higher than the 5.7% estimate but lower than the March peak of 6.5%.

On a monthly basis, consumer prices increased at a fasterthan-expected rate of 1.3% after advancing by 1.0% in May. Adjusted for inflation, workers’ hourly wages fell by 1.0% month-on-month or 3.6% from a year ago.

Inflation expectations decline

Fears that inflation could result in the Federal Reserve hiking interest rates by 100 basis points at its next policy meeting were somewhat alleviated by a drop in consumers’ inflation expectations. The University of Michigan’s consumer sentiment survey for July showed Americans expect inflation to measure 2.8% in five years’ time, down from 3.1% previously and the lowest level in over a year.

Meanwhile, there was also a lower-than-expected rise in import and export prices in June. According to the Labor Department, import prices rose by just 0.2% from the previous month, following a 0.5% increase in May. Economists were expecting import prices to advance by 0.7%. Export prices rose by 0.7% in June after surging by 2.9% in May.

European Commission cuts GDP forecast

Over in Europe, the European Commission lowered its GDP growth forecast for 2023, saying the war in Ukraine had set the economy “on a path of lower growth and higher inflation” when compared with its spring forecast. The EU economy is expected to grow by 1.5% next year, while the euro area is expected to grow by 1.4%, both down from the previous 2.3% projection.

Valdis Dombrovskis, European commissioner for trade, said: “Russia’s war against Ukraine continues to cast a long shadow over Europe and our economy. We are facing challenges on multiple fronts from rising energy and food prices to a highly uncertain global outlook.”

Inflation is expected to peak at 8.4% in the third quarter in the euro area, before declining steadily and falling below 3% in the last quarter of 2023. However, the commission said this will depend on the evolution of the war – in particular, its impact on Europe’s gas supply.

UK economy returns to growth

Here in the UK, the economy returned to growth in May, with GDP expanding by 0.5% from the previous month, following a 0.2% decline in April. This was mainly driven by a large rise in GP appointments. Economists had been expecting zero growth in May because of the rising cost of living.

Consumer-facing services fell by 0.1% as retail trade declined. However, this was better than the 0.8% contraction in April thanks to a surge in holiday bookings. Production grew by 0.9% while construction expanded by 1.5%, the seventh consecutive month of growth.

Please continue to check back for our latest blog posts and updates.

Please see below article received from Brooks Macdonald this afternoon, which provides the latest update on global markets.

What has happened

Monday started with a more optimistic tone as earnings reports from Goldman Sachs and Bank of America both beat expectations, an important test after the misses from the financial sector last week. The news that Apple was set to slow hiring and spending in 2023 drove risk appetite lower however with US indices ending down for the day after a sell-off that took place after the European close.

European gas supplies

The timing of the reopening of the Nord Stream 1 pipeline remained high on investors’ agenda on Monday with Gazprom saying that they were unable to fulfil their supply obligations to at least one major customer due to ‘extraordinary’ circumstances. This added to a downbeat assessment of the security of European gas supplies ahead of Thursday’s scheduled reopening. In a sign that the high natural gas price is also weighing on utilities, Germany’s Uniper, applied to extend their credit line from state-owned KfW. There were also reports of a draft EU document that assessed the potential damage caused by a cut-off of Russian gas supplies, with EU GDP hit by 1.5% in the worst case scenario.

Earnings Season

Markets were happy to shrug off the concerns over European energy security earlier on Monday, focusing on the upcoming earning season. Goldman Sachs saw an almost 50% decline in net income for the second quarter but the results came in ahead of market expectations. Comments from the bank suggesting that they may look to pause hiring replacements for departing employees painted a more cautious assessment of the upcoming year however it required similar comments from Apple to catalyse the risk off tone late in the US session. Netflix reports later today and given the poor run of recent earnings results, and stock market reaction, investors will be watching the results closely. Markets may be less keen to extrapolate any Netflix weakness across the broader sector as in recent earnings seasons, at least some of Netflix’s weakness was idiosyncratic rather than a poll on the overall health of the technology sector.

What does Brooks Macdonald think

Yesterday’s price movements, driven by the earnings and guidance from companies, underlines how important corporate results are to market levels. So far this year we have seen heavy falls to the price of companies whilst the earnings expectations have remained robust. Whether or not the market is now ‘cheap’ is largely determined by how earnings develop over the next 12 months.

Index

1 Day

1 Week

1 Month

YTD

TR

TR

TR

TR

MSCI AC World GBP

-0.8%

-0.9%

4.6%

-9.3%

MSCI UK GBP

0.9%

0.3%

3.1%

2.4%

MSCI USA GBP

-1.8%

-1.4%

6.2%

-9.9%

MSCI EMU GBP

0.8%

1.1%

0.5%

-16.4%

MSCI AC Asia ex Japan GBP

0.8%

-0.8%

1.0%

-6.9%

MSCI Japan GBP

-0.6%

-2.2%

3.0%

-10.1%

MSCI Emerging Markets GBP

0.9%

-0.8%

0.1%

-8.5%

Bloomberg Sterling Gilts GBP

-0.5%

-0.4%

1.2%

-15.0%

Bloomberg Sterling Corps GBP

-0.3%

-0.3%

0.7%

-14.0%

WTI Oil GBP

4.1%

-2.2%

-4.7%

54.2%

Dollar per Sterling

0.8%

0.5%

-2.4%

-11.7%

Euro per Sterling

0.2%

-0.5%

1.2%

-0.9%

MSCI PIMFA Income

-0.4%

-0.5%

2.0%

-8.0%

MSCI PIMFA Balanced

-0.5%

-0.6%

2.4%

-8.0%

MSCI PIMFA Growth

-0.6%

-0.6%

3.0%

-7.2%

Index

1 Day

1 Week

1 Month

YTD

TR

TR

TR

TR

MSCI AC World USD

0.2%

-0.1%

2.8%

-19.7%

MSCI UK USD

1.9%

1.1%

1.4%

-9.4%

MSCI USA USD

-0.8%

-0.6%

4.4%

-20.2%

MSCI EMU USD

1.8%

1.9%

-1.3%

-26.0%

MSCI AC Asia ex Japan USD

1.9%

0.0%

-0.7%

-17.6%

MSCI Japan USD

0.4%

-1.5%

1.2%

-20.4%

MSCI Emerging Markets USD

1.9%

0.0%

-1.7%

-19.0%

Bloomberg Sterling Gilts USD

0.9%

0.7%

-0.1%

-24.6%

Bloomberg Sterling Corps USD

1.1%

0.9%

-0.6%

-23.6%

WTI Oil USD

5.1%

-1.4%

-6.4%

36.4%

Dollar per Sterling

0.8%

0.5%

-2.4%

-11.7%

Euro per Sterling

0.2%

-0.5%

1.2%

-0.9%

MSCI PIMFA Income USD

0.6%

0.3%

0.3%

-18.6%

MSCI PIMFA Balanced USD

0.5%

0.2%

0.7%

-18.6%

MSCI PIMFA Growth USD

0.5%

0.1%

1.2%

-17.9%

Bloomberg as at 18/07/2022. TR denotes Net Total Return

Please check in again with us shortly for further relevant content and news.