Please see article below from Artemis, received yesterday afternoon – 25/02/2021

Do equities protect investors from inflation?

Economists are divided over what comes next for inflation. Simon Edelsten assesses the threat of inflation in the East versus the West. He explains why investing in strong companies with high margins may reduce capital risk, should inflation overshoot.

In the past decade, inflation has grown by a compound rate of just 1.8% a year. By comparison, measured in sterling, global equities have risen by 177% – an impressive 10.8% a year.

It might surprise those whose faith lies purely in bricks and mortar that the average UK house price rose by just 30-40%, depending on which index you use, during the same period. That is equivalent to an annual rate of around 3%.These low levels of inflation have surprised monetarist economists who predicted sharp rises after the introduction of quantitative easing in 2008. According to Milton Friedman’s theory: ‘Inflation is always and everywhere a monetary phenomenon.’ So this expansion of money supply should have caused inflation. It clearly did not.

Today economists are once again raising the alarm. Money supply growth in the US is now twice what it was in the aftermath of the global financial crisis. And now the new Democrat administration has proposed a stimulus package of a further $1.9tn (£1.4tn). Meanwhile, regulators are encouraging looser bank lending, and the Federal Reserve has moved from a target of capping inflation at 2% to ‘average inflation targeting’ – in other words, it will now let inflation rise further before it raises interest rates.

What next for inflation?

Economists are divided over what comes next. Many have reverted to Keynesian-type discussions about supply constraints. They note that China no longer has an abundant, inexpensive labour supply and is falling under the lengthening shadow of the one-child policy that ran from 1980 to 2015. That might point to wage inflation, but we are currently seeing higher levels of unemployment in the West, so that seems unlikely.

Rates offered on government bonds also seem far too low to suggest a sharp spike in inflation is imminent – the UK 10-year bond currently yields 0.28%, and CPI inflation for 2020 was just 0.8%.

However, some cynical souls warn that western governments have a vested interest in letting inflation loose. It is the only way they can rid themselves of the debt they have built.

In the circumstances, taking measures to protect one’s savings and investments against an unexpected rise in inflation seems prudent. That is not a forecast of high inflation – we have seen too many of those prove wrong. Rather, it is recognition that the risks of this threat to wealth have risen.

Lessons from history

As equities give stakes in the real economy, they have long been seen as a way to protect savers from inflation. This theory was at its height in 1972. Over the succeeding three years inflation rose to an eye-watering peak of 24%. And equities? The UK equity market fell 73% between May 1972 and December 1974. The charts then show markets recovering, but in real terms these rises amounted to little. Cost-of-living rises above 20% a year and punitive capital gains taxes took their toll.

The inflation of the early 1970s was caused by the US taking the dollar off the gold standard and by the sharp rise in oil prices – rather different threats to those likely today. All the same, lessons from history on which sectors fared well and badly may be useful.

The 1970s market started from much higher valuations than we see today – perhaps a result of overconfidence in the ability of equities to cope with inflation. Some sources quote the then FT30 index traded at 19 times earnings compared with the FTSE 100’s forecast price-earnings (P/E) multiple today of 15.5.

In those days the index was made up of companies with rather less international exposure and often rather more debt. Inflation drove lending rates higher, leaving banks and property companies worst affected. As their loans matured, companies were forced to refinance at much higher interest rates.

Today’s equity market is notably different in how well-financed and internationally successful our larger companies have become. They have generally reduced their debt exposure since 2008, and many have much greater power to pass on cost increases than in the 1970s.

In the 1970s equity market the best shares to hold were oil companies (which benefited from the creation of the Opec cartel) and, in the latter part of the decade, nickel miners. These enjoyed the recovery combined with supply restrictions from environmental rules introduced by Jimmy Carter. Similarly, today we would argue that only the world’s largest industrial mining companies are keeping up with increasing environmental regulation and able to invest in automation to improve productivity.

It is also striking that some of the best – or least bad – equities to hold through the 1970s were technology companies, such as Racal. Even though markets may have valued future earnings less highly (given the way the cost of living was expected to rise while you waited), companies that produced very high revenue growth and high margins delivered acceptable returns. Racal rose from 137p and a P/E of 11.7 in 1974 to 208p and 17.5 P/E at the end of 1976.

History suggests that ‘growth’ stocks with good pricing power can do well as inflation rises and that many ‘value’ stocks, such as banks and property, may not – the converse of some current recommendations.

The strong response

We always favour companies with high barriers to entry. These should give a company pricing power, whether inflation comes or not. We also avoid companies with large amounts of debt (rising cost of debt often causes the most trouble in times of inflation). Our selection process also tends to favour companies with high margins – therefore companies that will generally cope well with higher labour costs or increases in the cost of raw materials.

Such investments have performed well over the past 10 years. They may lack the cyclicality the market currently prefers as economies recover, but longer term such strong companies will benefit as much as others from the more normal economic prospects ahead. As we stand, it seems likely that 2021 will be an easier year in which to manage a business than 2020. However, as we were reminded last year, predictions are vulnerable to the unexpected.

Governments have very large stimulus packages prepared and would prefer to prioritise creating work and income over worrying much about inflation.

As asset managers, we must capitalise on the growth opportunities but be alert to the risk of inflation. We believe a balance of strong companies, diversified globally and across different sectors, should reduce capital risk. We will know if it works only if inflation does overshoot. We hope it does not, but it is best to be prepared.

Please continue to check back for our latest updates and blog posts.

Please see below an article from Invesco, which was published on Tuesday (23/02) and received yesterday, which details Invesco’s views on the Biotech sector:

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below for this week’s Markets in a Minute update from Brewin Dolphin:

Equities mixed as inflation offsets vaccine optimism

Global stock markets gave a mixed performance last week, as encouraging quarterly earnings and vaccine optimism were offset by concerns about rising inflation.

Most major US indices ended the week lower, with the Nasdaq down 1.57% amid an increase in longer-term interest rates. The S&P 500 also fell by 0.71%, as inflation fears returned and the yield on the benchmark ten-year Treasury note increased to its highest level in almost a year.

In Europe, the benchmark STOXX 600 ended the week up 0.21%, following news that the UK and Switzerland are set to ease lockdowns and the European Commission has signed a deal for a further 200 million vaccine doses. Gains were held back by concerns that higher inflation could result in central banks tightening monetary policy. The FTSE 100 added 0.52%, whereas Germany’s Dax declined by 0.4%.

In Asia, Japan’s Nikkei 225 topped the 30,000 milestone for the first time in more than 30 years, ending the week up 1.69% after the country started its vaccination roll out. In China, where trading reopened on Thursday following the Lunar New Year holiday, the Shanghai Composite gained 1.12% whereas the large-cap CSI 300 slipped 0.5% after the People’s Bank of China drained RMB260bn ($40.2bn) of liquidity from the financial system.

Last week’s markets performance*

FTSE 100: +0.52%

S&P 500: -0.71%

Dow: +0.11%

Nasdaq: -1.57%

Dax: -0.40%

Hang Seng: 1.56%

Shanghai Composite: +1.12%

Nikkei: +1.69%

*Data from close on Friday 12 February to close of business on Friday 19 February.

FTSE boosted by UK reopening plans

The FTSE 100 recovered from Monday’s early heavy losses to end the day up 0.18% after details of the UK’s reopening plan were revealed.

The first step will see all pupils in England return to school from 8 March, with some outdoor gatherings allowed from 29 March. Outdoor hospitality could open from 12 April, and indoor hospitality and hotels may open from 17 May. Stocks across hospitality, retail and travel all rallied on Monday, with JD Wetherspoon gaining 8.7%, Mitchells & Butlers adding 4.5% and WHSmith rising 6%.

In the US, a sell-off in technology shares led to the Nasdaq posted its biggest drop in a month, down 2.46%. The S&P 500 declined 0.77%, marking its fifth consecutive day of losses and the longest losing streak in a year, amid expectations of higher inflation.

In Hong Kong, technology stocks suffered their biggest sell-off since mid-November, dragging the Hang Seng down 1.1% on Monday. The Shanghai Composite also slipped 1.5% in its worst day since 28 January.

UK stocks opened higher on Tuesday despite figures revealing a rise in unemployment to 5.1% in the three months through December. InterContinental Hotels added 3.9%, whereas HSBC declined 1.9% after reporting a 34% drop in annual profit.

UK retail sales slump in third lockdown

The latest retail sales figures laid bare the impact the UK’s third national lockdown is having on the economy. Data released on Friday showed spending in stores and online fell by 8.2% between December and January, with all sectors other than food and online outlets affected by Covid-19 restrictions. The decline was 3% worse than analysts’ forecasts.

Separate figures from the Office for National Statistics revealed public borrowing reached £8.8bn last month – the highest January figure since modern records began.

A small increase in tax receipts was outweighed by the £20bn annual rise in spending, which included £5.1bn of expenditure on coronavirus job support schemes.

The UK’s retail sales figures are in stark contrast with those of the US, which saw sales increase by 5.3% between December and January – the highest jump in seven months and far higher than economists’ predictions. It is thought the government’s second round of stimulus cheques played a big part in boosting consumer spending.

US consumer spending to stay firm The US coronavirus relief package, which was signed in December, also restarted enhanced weekly unemployment benefits, which means household spending could stay relatively firm until the next Covid-19 recovery bill becomes law.

Once the next package is passed, there could be another boost to growth from fiscal stimulus, which is likely to coincide with more of the US economy reopening, enabling households to deploy the roughly $1.5trn in ‘excess savings’ they have built up since April last year. Indeed, the preliminary service sector PMI for February, which was released on Friday, recorded its highest readings since 2014.

PMIs beat forecasts

Last week saw positive PMIs in the UK and Europe, suggesting businesses are becoming more optimistic about a pick-up in activity over the coming months.

In the UK, the IHS Markit/CIPS flash composite PMI jumped to 49.8 in February from 41.2 in January – a bigger improvement than anticipated. Hotels, restaurants and travel companies reported steep falls in activity, but at a slower pace than in January. Financial and business services firms enjoyed modest growth.

“Although the data hint at a renewed contraction of the economy in the first quarter, business expectations for the year ahead improved to the highest for almost seven years, suggesting the economy is poised for recovery.” said Chris Williamson, IHS Markit’s Chief Business Economist.

Meanwhile, the IHS Markit flash German manufacturing PMI rose to a three-year high of 66.6, up from 57.1 in January, while the corresponding index in France gained 3.4 points to 55. A figure above 50 indicates most businesses reported growth in activity from the previous month. However, the German and French services PMIs both declined to 45.9 and 43.6, respectively.

The eurozone’s manufacturing sector is benefiting from demand from Asian countries, whereas many services businesses have been closed in an effort to control the spread of Covid-19. The pan-eurozone manufacturing PMI rose to 57.7, whereas the services PMI fell to 44.7, its lowest reading in three months.

This weekly update from Brewin Dolphin is a useful short look at the Global markets for the past week.

Articles like these help us stay informed as to what is happening within the markets.

Please continue to check back for further blog content from us.

Please see below for Legal & General’s latest Asset Allocation Team Key Beliefs Article, received by us yesterday afternoon 22/02/2021:

The consumer economy

Tim Drayson, our head of economics, often warns us not to bet against the US consumer. Last week, the US retail sales numbers for January smashed forecasts and once again showed that stimulus works, especially direct cash payments to households. Around 25% of the $600 received by individuals earning $75,000 or less was immediately spent, generating a $30 billion bounce in retail sales across all categories. Perhaps as a sign that economic optimism is already well priced in, equity markets chopped around last week although Treasury yields have been drifting higher.

The price of everything…

Clients are asking whether stock markets are getting ahead of themselves. We push back on this. If equity prices move up in lockstep with your view of the future improving, you should become neither more nor less optimistic. Given we believe we are early in the cycle, the mantra should remain unchanged: stay long, buy the dips.

Price is no determinant of value or valuations; it is only useful in relation to what you get for what you’ve paid. Is $100,000 a lot for a car? It depends if it’s for a Golf or a Ferrari. This is one reason we use multiples to think about valuations. Multiples that have historically exhibited mean-reverting properties over the long run have had some predictive power for longer-term returns. Prices, though, are not mean reverting and tell you nothing about future returns.

We pay particular attention to relative valuation. The yield gap is one representative measure; it hasn’t moved much recently but is still high by historical standards. Moreover, early in the cycle it’s quite normal for valuations to shoot up. This rebound has, so far, looked quite similar to the one in 2009 in magnitude.

Our baseline is that this bull market will last until the next recession. There’s a lot of runway left before then, in our view, and we expect the S&P 500 to be materially higher before the bull market ends.

Real talk

Investors are becoming more worried about the rise in bond yields and the possible impact on equity markets. The recent choppiness in equities while yields have drifted up adds to their nervousness. Although we believe nominal and real yields will rise further (and by more than currently priced in the forwards), we think this should be well digested by equity markets. We note that the 2013 taper tantrum saw a 75 basis point spike in bond yields but ‘only’ a 6% correction in the S&P. (Tim recently discussed the possibility of new US tapering.)

Empirically, there’s not much evidence that rising real yields are particularly bad news for equities, especially from these very low levels. In fact, rising real yields have mostly been associated with higher equities. Historically, the correlation between real yields and equity markets has turned negative at much higher real yields.

It’s crucial to understand what is driving yield moves. As long as rising yields reflect a combination of higher inflation and better growth prospects, this should be positive for markets. Only when policymakers become worried should we be ready for change. Equity markets may panic when they see either a de-anchoring of inflation expectations or they need to bring forward the timing of policy normalisation. In our view, it is far too early for either of these, but clearly both need to be monitored very closely.

All about that base effect

The next round of stimulus is still being debated by Congress. Last week, Treasury Secretary Yellen commented that “the risk of doing too little is greater than of doing too much”. If such an approach is adopted, the direct uplift to household incomes will potentially be at least three times larger than included in the COVID relief bill at the end of 2020. This money should hit people’s accounts just as the US begins to re-open more fully. Alongside the excess household savings accumulated during the pandemic, this could fuel a surge in demand.

This makes us think about the implications of the money supply glut. None of us have seen money supply grow on the current scale, the only precedent being during the Second World War. Half of the increase in broad money supply sits directly in household accounts, and cash as a share of financial assets for non-financial corporates is at its highest levels since 1969. We believe that a significant amount of this cash will be spent, boosting growth, corporate profitability, and possibly inflation.

On inflation, we know there will be a pronounced base effect around the spring as prices fell sharply while the economy was locked down last year. This, plus later boosts from CPI components that were depressed by restrictions like airfares and hotel prices, could temporarily raise inflation above target-consistent levels.

The Federal Reserve has highlighted this potential outcome, with January’s minutes containing a discussion on why it would be prudent to look through this increase. This makes sense in our view as it is equally likely that inflation will fall back in the summer. Base effects reverse, and there are also some aspects of inflation that have been lifted by the pandemic but are likely to weaken once the economy reopens. Used-car prices are an example.

Further out, the inflation picture becomes much murkier. How much slack will be left in the economy? Does the jump in money supply matter? Are some of the structural disinflationary forces of the past decade, like technology, beginning to shift? How well anchored are inflation expectations?

We believe that inflation becoming high enough to constrain monetary policy is still a way off. But if we get there, central banks in developed markets might be surprised by how much they have to raise rates to reduce inflationary pressure. Money doesn’t play a role in their models, despite monetary aggregates generally being excellent predictors of economic aggregates, and they aren’t able to directly undo the monetary and fiscal one-two that’s been so effective at putting cash in consumers’ pockets.

Please continue to utilise these blogs and expert insights to keep your own holistic view of the market up to date.

Please see below this weeks Invesco Investment Intelligence update – received this morning – 22/02/2021

Monday 22 February 2021 – update

The diverging impact of virus containment measures on individual economies and the differing levels of fiscal stimulus was plain to see in US and UK January Retail Sales last week. The former exceeded expectations materially, growing 5.3%mom (see chart of the week), while the latter fell -8.2%mom, far worse than expected. With the vaccination rollout proceeding at a faster path in the UK (nearly 25% of the population have received a first shot compared to 12% in the US) and new cases, hospitalisations and deaths all declining sharply, the worst of the impact of the current lockdown may well be behind us, driving an easing of lockdown restrictions and some form of return to normality. Certainly, February’s Flash PMIs provided a more encouraging picture with the Composite rising from 42.6 to 49.8 on the back of a strong recovery in the dominant Services sector, hardest hit by recent lockdowns. Unfortunately, progress has been not as fast in other DMs, particularly Continental Europe (the weakening of the EZ’s Flash Services PMI reflected that) and prospects for EM look even less promising with vaccinations rates at just 0.1% across Africa and nearly 130 countries have yet to administer a single dose.

Money continues to flow into equity markets, but rising bond yields last week put a halt to progress in DM (-0.5%), which weighed on overall global returns (MSCI ACWI -0.4%). EM held up better and managed to eke out a small gain (0.1%). Weakness in DM was led by the US (-0.7%). YTD, EM (11.2%) have delivered more than double the return of DM (4.7%) and the region remains comfortably the most preferred market in the latest BofAML Global Fund Manager Survey. Small caps also declined (-0.5%), but here also performance diverged between DM (-0.7%) and EM (1.5%). They are up just under 10% YTD. At the sector level, commodity sectors made gains on rising oil and metals prices, with Energy (2.7%) ahead of Materials (1.3%), while Financials (1.8%) benefitted from rising bond yields and steeper yield curves. The reverse was true for defensive long duration sectors, such as HealthCare (-2.2%) and Consumer Staples (-1.2%), while IT (-1.2%) and Utilities (-1.8%) also underperformed. Against this backdrop Value (0.5%) was comfortably ahead of Growth (-1.2%), while Momentum (-1.8%) gave back some of its strong YTD outperformance. Despite a strengthening £, outperformance of the commodity and Financials sectors ensured that the UK outperformed (All Share 0.5%) on the back of a good relative week for large caps (FTSE 100 0.7%).

Upward momentum in government bond markets continued last week. The largest moves have been in the UST and Gilt markets, where the 10yr rose 15bp and 13bp respectively to their highest levels since last February (1.35% and 0.70% respectively). Yields are up 43bp and 50bp from their start of year levels and 85bp and 62bp from last year’s all-time lows. 10yr Bunds pushed higher too and after a 7bp rise to -0.31% are now up 26bp YTD and 53bp from their all-time lows. Even Italian BTPs, the star performer in recent weeks, saw yields rise 9bp. Unsurprisingly returns were negative with the Gilt index hit hardest due to its longer duration (12.4 years). IG suffered against a backdrop of higher government yields with weakness across the board, again led by longer duration £ markets (8.5 years). Globally spreads narrowed 3bp, but yields rose 6bp. HY continued to outperform in credit, as spreads narrowed 8bp and the YTM fell 2bp to an all-time low 4.6% (Yield to Worst is 4.05%).

The US$ was broadly flat on the week with the US$ Index down just 0.1%, leaving it up 0.5% YTD. Vaccination progress helped £ to its best week versus the US$ since mid-December, breaking through the $1.40 level for the first time since Q2 2018. It also gained against the Euro, moving above the €1.15 level for the first time since last March. Economically sensitive commodities continued to make gains. The Texas storm’s impact on US production helped push oil to new post-pandemic highs and it is now up 23% YTD. Copper, up 7.1% for the week, extended its surge to a new nine-year high amid warnings of a historic shortage as the global economy starts to recover. After its best year for a decade last year, Gold is off to its worst start in 30 years, falling further last week (-2.3%) and down just under 6% YTD. Rising UST yields aren’t helping as investors take profits and rotate into economically sensitive commodities. Even rising inflation expectations aren’t helping the metal.

Market performance last week (%)

Past performance is not a guide to future returns. Sources: Datastream as at 21 February 2021. See important information for details of the indices used.1

YTD market performance (%)

Past performance is not a guide to future returns. Sources: Datastream as at 21 February 2021. See important information for details of the indices used.1

Chart of the week: US Retail Sales (mom%)

Past performance is not a guide to future returns. Source: Datastream as at 18 February 2021.

• The direct impact of fiscal stimulus on the US economy was clearly highlighted in last week’s surge in Retail Sales for January. The headline number rose 5.3%mom – the first monthly gain since September, the largest rise in seven months and beating consensus expectations of a 1.1%mom rise by a considerable margin. Only last May have expectations been beaten to such a degree. This leaves them 5.8% higher than a year ago (and remember that was compared to a pre-pandemic economy) and a far faster recovery than in previous cycles.

• What drove the strong rise in sales? There was a seasonal boost following weaker than normal holiday spending in December, while the easing of virus restrictions clearly played a role too. However, the general consensus is that the renewed income support from the $900bn end of year fiscal package has been the dominant factor as the income dispersion of the spending was mainly driven by lower-income groups, the main beneficiaries of that package and historically where the propensity to spend any stimulus is the greatest. In that package most Americans received payments of $600 (up to $75k income and then tapered to no payment at $99k) with eligible families also receiving $600 per dependent child. These payments were made in early January. Monthly unemployment payments were also boosted by $300 per week for 11 weeks.

• And this is not the end of support for US households and consumption. Biden’s $1.9trn “American Rescue Plan”, currently going through Congress, is likely to see further payments to individuals of up to $1400 and $400 per week in additional unemployment payments. On current expectations these are likely to be paid out from mid-March. And on top of that, with “excess” savings as a consequence of the pandemic estimated by Goldman Sachs to hit $2.4trn by the middle of the year, there should be a further boost to spending from this source as the economy returns to some sort of normalcy. Even if Goldman’s estimate that under 20% of that will be spent, partly down to a large proportion of those “excess” savings being held by higher income groups, who are far less likely to spend it, that would still be enough to contribute roughly 2% to GDP growth, although Goldman’s attach a high degree of uncertainty to this number.

• It’s perhaps no wonder that consensus expectations for consumer spending are higher in the US (5.2%) in 2021 compared to both the EZ (3.9%) and UK (4.3%), which in turn should underpin a stronger recovery in Real GDP.

Key economic data in the week ahead

• Not a lot on the data front this week, so focus may well be elsewhere: on progress of the upcoming US stimulus package, Powell’s testimony to the US Congress and developments on the virus front, where the PM will be announcing his roadmap for easing restrictions in England and the EU Council meets at the end of the week.

• In the US on Tuesday the Conference Board Consumer Confidence index for February is forecast marginally higher at 90 from 89.3, but remains close to post-pandemic lows and a long way below the 133-level seen last February. Last week’s Initial Jobless Claims were higher than expected at 861k, a sixth consecutive week of more than 800k despite a drop in coronavirus cases. Thursday’s reading is expected at 840k, a modest improvement. Friday’s Personal Income data for January is estimated to have had a strong boost from additional stimulus payments. Incomes are estimated to have increased 10%mom. Friday also sees PCE Inflation data released with the closely watched Core reading expected to show a 0.1%mom increase, leaving it at 1.4%yoy.

• In the UK the Unemployment rate is forecast to have increased to 5.1% at the end of December when data is released on Tuesday, up from 5% in November. This would be the highest level of unemployment since October 2015.

• In the EZ, Germany’s Ifo Business Confidence for February is released on Thursday. After last week’s Flash Composite PMI showed a marginal improvement, a similar outturn is expected with a rise to 90.5 from 90.1, led by future expectations rather than current conditions.

• In Japan Industrial Production and Retail Sales for January are published on Thursday. The former is forecast to show a rebound to 3.9%mom, leaving it down -5.4%yoy, while the latter is expected to see a -1.3%mom decline, leaving it down -2.6%yoy. The expansion of the state of emergency beyond Tokyo the main culprit there.

• In China the Loan Prime Rate, the reference point against which banks price loans, is set on Monday. It was last changed in April 2020 and is expected to remain unchanged at 3.85% and 4.65% for the 1-year and 5-year rate respectively.

Please continue to check back for our latest updates and blog posts.

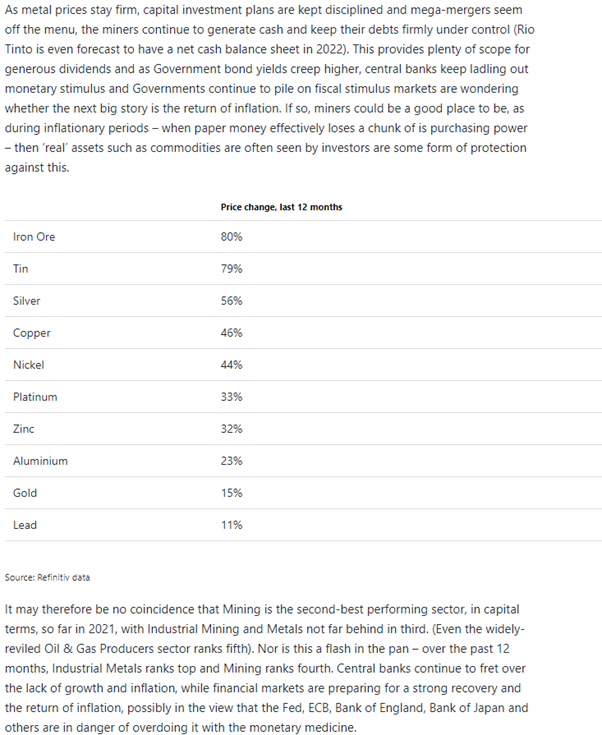

Please see below an article published by A.J. Bell last Tuesday (16/02) and received yesterday afternoon, which details the role Miners could play in plugging some of the dividend gap:

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below article received from AJ Bell yesterday afternoon, which explains how the events of the past 12 months have had major implications for consumers and companies, and how we now move forward.

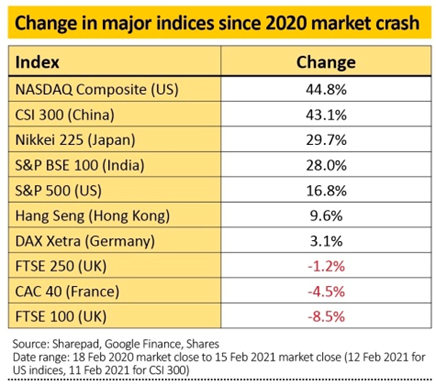

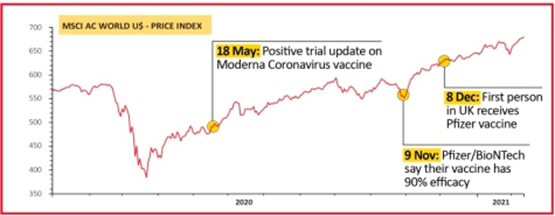

Despite all the upheaval of the past year, anyone glancing at the financial markets today might find it hard to believe investors were in the throes of despair 12 months ago.

Following the global markets crash in February 2020, the recovery has been spectacular. The US Nasdaq 100 and S&P 500 indices are at all-time highs, Japan’s Nikkei index is at a multi-decade high, China’s Shanghai index is at a multi-year high and the MSCI All Countries World Index is at a record high.

In the UK the FTSE 100 and FTSE 250 are still in negative territory since February 2020 although the losses aren’t nearly as extreme as they were when the pandemic first took hold.

Markets have been fuelled by support from central bank and government stimulus measures, low interest rates and optimism over the pace of economic recovery thanks to the creation of Covid vaccines.

Risk appetite is alive and well as shown by the surge in crypto currencies, the volume of investment grade bonds now trading with negative yields (bond yields fall when prices rise), herd behaviour on social networks regarding stocks, the deluge of cash shells to acquire businesses, the warm reception for new stock market listings and the race by private equity firms to deploy their mountains of cash through acquisitions.

Later in this article we look for cheap stocks that have still to play catch-up.

First, we explore what’s changed in terms of how companies do business and how we manage our money.

STRUCTURAL CHANGES

It almost seems as though nothing has changed; in fact, everything has changed. Much of what might be called ‘new’ isn’t new at all – many of the biggest trends to emerge in 2020 had been waiting in the wings for several years, the pandemic just brought them centre stage much earlier than expected.

The greatest change has been the shift to remote working (see When will we return to the office – if at all?), which had always existed on the fringe but had never been considered viable on a large scale. The surprise for many business owners was how off-the-shelf technology enabled them to quickly move to remote working without a hitch.

Moreover, remote working has brought benefits to many firms including cost savings, and it has improved the work/life balance for their employees. The flip side is that it is bad news for owners of city centre offices, transport companies and anyone who relies on either – or worse, both.

Companies with large central offices are mostly looking to downsize while those which were planning to expand have realised they can increase their staff numbers while staying in the same office and rotating their teams.

Those with several smaller regional offices may look to do away with them altogether and concentrate on making the working from home experience more fulfilling for their staff.

Bus and rail firms, which will have budgeted for a given level of revenue before the pandemic, now have to go back to the drawing board and rethink their plans, not least for capital spending, given they are likely to see far fewer passengers using their services in the future.

PERSONAL FINANCIAL HABITS HAVE CHANGED

The pandemic has brought behavioural changes, too. Ian Mattioli, co-founder and chief executive of wealth manager Mattioli Woods (MTW:AIM), says his firm has found that many people who, prior to last year, thought nothing of spending their disposable income on two or three holidays a year, are now saving the bulk of their surplus wages to give themselves a buffer in case they lose their jobs.

Recent announcements by holiday companies such as TUI (TUI) confirm that holidaymakers are being more selective. The ‘return to normal’ has failed to happen so far, with TUI reporting a 44% reduction in summer bookings compared with pre-pandemic (2019) levels, well short of its earlier expectation for a 20% drop.

WHEN WILL WE RETURN TO THE OFFICE (IF AT ALL)?

The latest AlphaWise survey from investment bank Morgan Stanley makes sobering reading for those hoping for a reopening of the economy by Easter.

According to the bank’s monthly telephone survey of 12,500 European office workers, despite the rollout of vaccines since its previous survey, employees’ expectations of when they can return to work have slipped from April to June.

As the survey says, ‘Clearly, this will not only impact office utilisation in 2021, but also leisure and retail property that depends upon the return to normal commuting patterns.’

Across Europe, 73% of office workers have been working remotely compared with half that proportion pre-Covid. Of these, 80% would like to work from home more in the future, with 51% happy to work out of the office one or two days a week, 29% three to four days a week and 14% every day of the week.

Chris Herd, founder and chief executive of remote infrastructure firm Firstbase, says remote work is ‘the biggest workplace revolution in history, and nothing will deliver a higher quality of life increase in the next decade than this’.

Herd believes new companies will be ‘remote first’, without the need for a corporate headquarters. Aside from the obvious cost savings, this allows them to hire the best people wherever they are in the world, not just within a certain radius. At the same time, companies which want to retain their staff will have to offer remote working as an option or risk losing them.

We are also becoming more discerning when it comes to shopping online for fashion. Gone it seems is the habit of picking six dresses for an event and sending five back, with retailers such as ASOS (ASC:AIM) noting a steady decline in the volume of returns throughout the past year.

If we aren’t getting dressed up and going out, or planning several trips to foreign climes, what are we spending our money on?

The latest Barclaycard study shows overall UK consumer spending fell 16% between 25 December and 22 January. Spending on essentials was up roughly 4%, with supermarket spending up 17% and online grocery spending up 127%, which is positive news for companies such as Ocado (OCDO).

Spending on non-essentials fell almost 25%, with health and beauty sales down 27% and clothing sales down 25%. With restaurants closed, takeaway and delivery sales jumped 33%, the highest growth on record for the category.

Total online spending was up 73% on the same period a year earlier and now accounts for a remarkable 55% of all retail sales, a genuine paradigm shift for the retail sector which has struggled to keep up with changing demand.

Moreover, most consumers believe they will stick with online shopping once vaccinations are commonplace as they now prefer the experience of ordering via their phone or computer and having their items delivered rather than schlepping to the shops in all weathers.

A SHRINKING HIGH STREET

Sadly, the flip side of this shift to online shopping is the high street as we knew it becoming a thing of the past. Footfall in January 2021 was down a staggering 77%, according to the British Retail Consortium, and the outlook for February is not particularly encouraging.

Few chains look to have the right financial strength and proposition to sustain a town centre presence long-term, with the list of likely survivors (among companies whose shares trade on the UK market) more or less measurable in single figures, principally Greggs (GRG), JD Sports (JD.), JD Wetherspoon (JDW), Marks & Spencer (MKS), Next (NXT), Primark-owner Associated British Foods (ABF), Sports Direct-owner Fraser (FRAS) and WH Smith (SMWH).

And, where previously an empty shop might have been turned into a café, bar or restaurant, the decimation of the hospitality industry means there are few players with the financial wherewithal to step in and take up the space, especially if footfall is permanently reduced.

According to the Coffer Peach Business Tracker survey, turnover for the hospitality industry was down 54% last year from £133.5 billion to just £61.7 billion. If anything, the fourth quarter trend was worse than the annual average, down 57% from £33 billion to just £14.3 billion.

All of this bodes poorly for commercial property companies for the next few years. Strong retailers will have their pick of the best sites and will likely demand low rents with much of the responsibility for upkeep passed onto the property owners.

STOCK MARKET WINNERS AND LOSERS

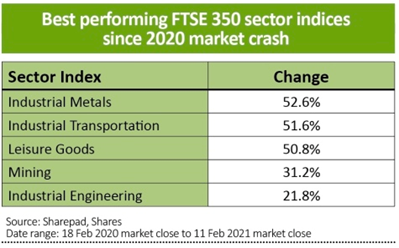

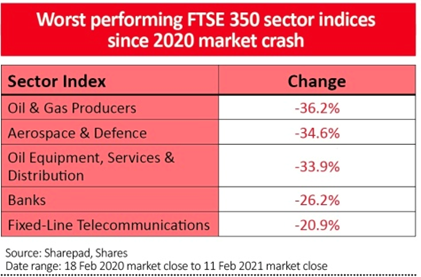

When sifting through what worked and what didn’t work over the past year in stock market terms, we have looked at both the broader FTSE 350 sector indices and individual stocks.

Unusually, industrial metals, mining, industrial transportation and industrial engineering have been the leaders in terms of performance, even though the global economy took an enormous hit during the pandemic and by most estimates it will take three to five years for world output to return to ‘trend’.

On the other hand, considering the devastation wrought on the hospitality industry, it’s somewhat surprising travel and leisure or pubs, restaurants and hotels weren’t among the worst FTSE 350 sector performers.

Instead, the worst sectors have been aerospace and defence, banks, fixed-line telecommunications, oil and gas producers, and oil and gas equipment and services, the last two despite a sharp rally in crude oil prices since the start of 2021.

STOCK-LEVEL ANALYSIS

It won’t be a surprise to investors that companies which were either already largely online or shifted their business model to online were among the biggest winners. The top performing FTSE 350 stock since the start of the Covid sell-off is AO World (AO.), up 307%. The online retailer of unglamorous items such as freezers, microwaves and washing machines became a stock market darling as domestic appliances became hot property during lockdown.

Spread betting firms like CMC Markets (CMCX) and Plus500 (PLUS) as well as gambling firms like 888 (888) and Flutter (FLTR) posted exceptional gains thanks to a surge in new account openings as those cooped up at home found new ways to entertain themselves by betting.

Savvy investors played the strong performance of overseas markets through collective investments, especially those with a US/technology bias, with Baillie Gifford US Growth Trust (USA) and Scottish Mortgage (SMT) clocking up gains of more than 100%.

Asia-focused trusts also found favour with Fidelity China Special Situations (FCSS) almost doubling and JPMorgan Japanese (JFJ) rising by two thirds.

Interestingly, less than half the constituents of the FTSE 350 index trade above their February highs today, and a third are still lagging the benchmark with losses of more than 10%.

The list of big losers is littered with travel and leisure, aerospace, financial and industrial stocks, along with real estate investment trusts (REITs). Curiously, many of the housebuilders are still heavily in negative territory with losses of 30% or more despite the continued strength of demand in the housing market – as shown by their recent results – and a clutch of technology stocks are also nursing heavy losses which seems counter-intuitive.

It is worth noting that since 9 November when Covid-19 vaccines started to be confirmed, recovery plays have been in fashion, with travel and leisure stocks such as Cineworld (CINE) picking up, and more defensives such as Unilever (ULVR) lagging the wider UK indices.

3 STOCKS TO BUY NOW

We have chosen three stocks which we think have been overlooked, with varying degrees of risk attached.

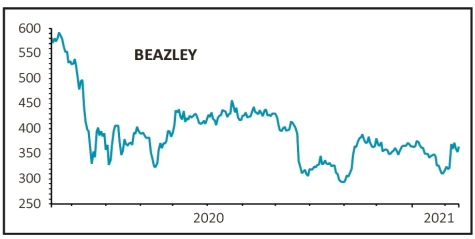

Shares in Lloyd’s market insurer Beazley (BEZ) are trading 38% below their pre-pandemic levels, which seems to us as though the market is driving with the rear-view mirror.

he firm may have posted a $50m loss for last year due to claims for cancelled events and other Covid effects, but this was half the amount analysts were expecting.

What excites us is the 15% increase in renewal rates as the insurance market tightened conditions in response to the pandemic. Chief executive Andrew Horton described himself as ‘very positive about the year ahead’, as having raised capital in May the firm is well placed to capture the strong rate tailwind.

With its strong underwriting discipline and focus on capital returns, Beazley can cover the same risks this year with a much greater profit margin which should lead to earnings upgrades and a sharp rerating of the shares.

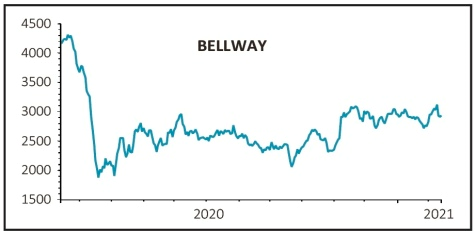

Mid-market housebuilder Bellway (BWY) posted a record build volume for the six months to the end of January, and what it called a robust forward sales book with orders for almost 5,900 new homes or 28% more than the same period a year earlier.

It also pointed to full year completions of 9,800 homes, an increase of 30%, and an improvement in its underlying operating profit margin of ‘at least 200 basis points’ (2%) over last year’s 14.5% margin.

Given how much brighter the outlook appears, it seems odd that the shares are still some 30% below their February 2020 level. Moreover, the valuation gap between Bellway and the rest of the sector seems abnormally wide.

We can only assume that investors are worried the end of Help to Buy and/or the stamp duty holiday will lead to disappointment, yet the valuation offers a healthy margin of safety in our view.

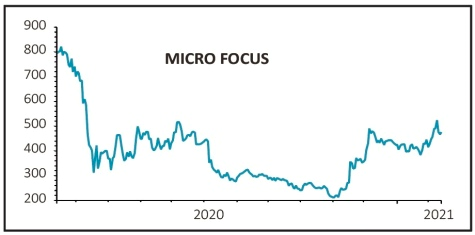

Infrastructure software supplier Micro Focus (MCRO) divides opinion like few other stocks. ‘Cheap for a reason’ is a typical response, which given its debt level and a surprise $2.8 billion writedown of goodwill in the 2020 results doesn’t seem unjustified.

The firm began its three-year turnaround plan in January last year, which was unfortunate timing, but if anything, the pandemic has forced it to grasp the nettle and cut down on unnecessary spending while focusing on key areas of opportunity.

The firm’s new guidance is for revenues to stabilise in the 2023 financial year, while its in-house IT infrastructure plan starting this year will generate further operational improvements and efficiencies.

For us, with the shares down 40% since last February, it’s a binary bet. Either the firm does what it promised which means the shares rerate, or it keeps disappointing and gets taken over by a private equity firm. This is a high-risk investment and investors should only get involved if they have money they can afford to lose.

Please check in again with us soon for further market analysis and news.

Please see the below article from Invesco received yesterday afternoon:

1. Growth

Over the years we have found we are much more likely to find attractive investment opportunities in healthy, growing companies – regardless of whether they are “growth” or “value”. A company that grows is not about investment style, it’s a fundamental building block of almost all of our good investment ideas. There are several ways in which companies can grow: new markets, new customers, new products, value accretive M&A etc.

In our experience, businesses that aren’t growing, tend to be going backwards. Not all growth opportunities enhance shareholder value, therefore it is important to understand the track record of the company and the management team and their ability to deliver an economic return from such ventures. We look for companies that are sustainably growing shareholder value through the cycle and can deliver returns above the cost of capital.

2. Price

Price isn’t about value investing. In our experience it is often the lowest multiple (“cheapest”) companies that prove to be value traps. Paying the right price is about understanding what a company is worth: it’s intrinsic value. It is only by doing the fundamental analysis and gauging the intrinsic worth that you can make a judgement on what is the appropriate price to pay for the asset. We want to pay less than what we believe the company is worth and will wait for the market to provide this opportunity.

3. Margins and moats

Most Investors want to invest in high margin businesses; it often infers the company is unique in the product or service that it offers. Apple would be a good example of this: a loyal customer base, who are embedded in their ecosystem, have no choice but to be loyal – giving Apple high margins. This ecosystem provides a wide investment moat. However, businesses that can sustain high margins while growing sales are rare and they tend to attract competition. Companies that have low margins can be attractive also, as long as they have a moat which is defendable. In fact, sometimes having low margins can be an effective competitive strategy and enable a company to take market share from less effectively run competitors.

Ryanair is a great example of a low margin businesses, that has been successful; its moat is its lower cost base than competitors, this in turn drives volume growth which allows them to drive supplier costs down further. Customers ultimately win as they receive lower prices. The key is determining which companies can maintain their moats, allowing them to achieve future growth.

4. Owners and management

We want management to act like owners of a company; they should be aligned with us as investors; both in how they are remunerated and how they deploy capital. Some of our best investments have been in family and founder owned enterprises. These agents act as owners on our behalf and act in the best interests of the business for the long term, rather than trying to meet next quarters earnings.

In the absence of material share ownership (the gold standard in our view) management teams should have clear, simple and measurable financial targets that incentivise good capital discipline, with particular focus on cash generation and returns on capital. Companies need to clearly define hurdle rates of return for capital investment and acquisitions, ensuring that they are value accretive for shareholders.

5. Balance sheet and leverage

While leverage can provide increased returns, it also comes with added risk. Taking on balance sheet risk in economically cyclical companies is particularly high risk. Leverage should be used in a risk conscious way that is appropriate to the individual company and industry. Conversely, those companies with net cash, which they are able to deploy at attractive rates should be seen as desirable; while returning cash to shareholders is another lever to add value.

We’ve found that many of our founder owner businesses run with net cash, oftentimes indicative of their prudence and focus on cash generation. The combination of cash to deploy in the hands of aligned management team can provide both optionality and potentially greater downside protection.

6. Cash flow and dividends

Our preferred metric for valuing companies is free cash flow; it is less easily manipulated than earnings. Quite simply cash is the best measure of a company’s health; without being self-financing from a cash flow perspective, the business cannot be a going concern for any material period of time. Cash flow allows the company to pursue those opportunities which enhance shareholder value: investing at attractive rates, paying down debts, buying back shares or paying a dividend. We believe that investing in companies that can sustainably grow their dividends over time will not only provide an important contributor of return, but provides an important discipline for companies in managing their cash flow.

7. Different lenses

We believe that the fundamental analysis we do is exhaustive: we read a great deal of both recent and historic annual reports , listen to management earnings calls, speak to analysts and experts, as well as competitors and customers. We try to build a deep, holistic understanding of the business, the opportunities and risks that it faces. Ultimately, we seek to make a judgement on how the business will fare in the future, versus the price we are being asked to pay for it today.

However, as investors we are not all knowing; we all have our inadvertent biases. We therefore also evaluate companies through independent lenses, for instance EVA (understanding a firms economic rather than accounting profit) and QRR (assessing accounting and earnings quality). Our best investments tend to survive not only our scrutiny, but those of our independent partners as well.

This is an interesting article giving in an insight into how some of the big investment firms choose the right investments for their funds.

Please continue to check back for a variety of blog content from us.

Please see below a recent article from Aegon regarding the future of Pan-European mobile networks, received by us today 17/02/2021:

Throughout the years, investors and politicians have talked a lot about the desire for a pan-European telecom company. Now, with 5G mobile technology, their wishes may finally come true – but not in the form they expected! Most of us anticipated a merger between some large European telecom companies, such as Orange or Deutsche Telekom. But such a merger does not offer many opportunities to cut costs as they operate in different countries and have no network overlap.

There is one area, however, where telecom companies can share costs and that is in operating mobile towers – the so-called ‘masts’ with mobile radio equipment. We anticipate that we will see the establishment of pan-European tower companies in 2021. In fact one is almost there: Cellnex, from Spain. US competitor, American Towers is also building a presence in Europe, while Vodafone, Deutsche Telekom and Orange all want to manage their tower portfolios as a separate business. Together, they have the potential to create a pan-European infrastructure leader!

Until recently, the European Commission preferred (generally speaking) to have four mobile network operators in each country. This promotes competition and leads to lower prices for mobile telephony. From a cost perspective though, it is more efficient to have one network that can be used by all citizens. It is a bit like the national railways in continental Europe. We do not duplicate the railway network but have only one infrastructure in each country. So, it makes sense to share infrastructure.

For example, Cellnex, will run mobile towers for three telecom operators in France. This brings enormous cost synergies as well as delivering a lot of cash to operators selling their networks. Moreover, it will also help the quality of mobile networks since towers in remote (and unprofitable) areas can now be shared by multiple operators. This is in contrast to times past when many of the larger telecom companies were reluctant to share infrastructure. A high-quality network was deemed a key competitive advantage, something they wanted to keep for themselves.

Today, the returns of telecom operators are under pressure, due to heavy competition. The telecom companies also need a lot of cash to build out their 5G networks (which require more antennas). Furthermore, they often need to invest in their fibre networks. Coincidentally, there is a strong demand for infrastructure assets, due to low interest rates. The valuation of infrastructure assets is very high, compared to the valuations of the traditional telecom operators. So, asset sales are likely to continue.

What can we expect in 2021? In general, the establishment of tower companies will increase the quality of mobile networks throughout Europe. The large telecom operators, such as Orange, Deutsche Telekom and Vodafone could unlock a lot of value through selling their assets. And if they were to merge their tower businesses, we would have a pan-European mobile infrastructure! These assets should be very good collateral for bond financing. However, bond holders of the telecom operators may want to think twice about credit risk if the family silver is sold.

Note: Aegon hold positions in Vodafone, Deutsche Telekom and Orange in their portfolios.

This is an insightful and thought-provoking article regarding one of the biggest markets of modern times and its potential future movements.

Please continue to keep your own holistic view of the markets up to date by reading articles such as these on a regular basis.

Please see below this week’s Markets in a Minute update from Brewin Dolphin – received late yesterday afternoon – 16/02/2021

Equities reach record highs as vaccine roll out accelerates

After a volatile few days, global equities reached record highs last week as the vaccine roll out gathered pace and data revealed a decline in coronavirus cases.

The S&P 500 ended the week up 1.23%, with the communication services sector outperforming following strong gains in Twitter and video gaming shares. Energy stocks climbed higher after front-month Brent futures prices reached more than $60 per barrel, up from less than $20 last April.

The STOXX Europe 600 gained 1.09% last week, although performance was mixed in Europe with Germany’s Dax largely flat, France’s CAC 40 up 0.78%, and the UK’s FTSE 100 gaining 1.55%. Hopes of a large US economic stimulus package drove gains, but these were hampered by poor GDP data from the UK and eurozone.

In Asia, markets in China and Hong Kong rallied ahead of the Lunar New Year holiday, with the Shanghai Composite surging 4.54% and the Hang Seng gaining 3.02%.

Last week’s markets performance*

FTSE 100: +1.55%

S&P 500: +1.23%

Dow: +1.00%

Nasdaq: +1.73%

Dax: -0.05%

Hang Seng: +3.02%

Shanghai Composite: +4.54%

Nikkei: +2.57%

*Data from close on Friday 5 February to close of business on Friday 12 February.

FTSE surges higher as oil price nears $65 per barrel

The FTSE 100 enjoyed its best day in more than a month on Monday, ending the day up 2.5% to 6,756.11 following positive news on the vaccine front. More than 15m people in the UK have had their first jab, and it is now being offered to the over-65s and clinically vulnerable.

Oil majors BP and Royal Dutch Shell surged 6.5% and 6.1%, respectively, on Monday after oil prices were further boosted by supply concerns. The oil price is now nearing $65 per barrel.

Positive sentiment led to a sell-off in UK government debt. The yield on the 10-year gilt rose to 0.57%, its highest level since March 2020.

After a shaky start, countries in Europe are also starting to ramp up inoculations. The STOXX Europe 600 finished Monday 1.3% higher, while Germany’s Dax gained 0.4%.

Elsewhere, Japan’s Nikkei 225 surged past 30,000 for the first time since 1990, after data showed its economy grew 3% in the fourth quarter, far higher than analysts had predicted. The US stock market was closed on Monday for Presidents Day.

Rising commodity prices and coronavirus optimism continued to boost UK stocks on Tuesday morning, with the FTSE 100 up 40 points in early trading to 6796 – its highest level since 15 January. HSBC topped the leader board with a 3.2% gain.

After closing for the Lunar New Year holiday, Hong Kong’s Hang Seng surged 1.8% in its first session in the Year of the Ox.

Sharp drop in coronavirus cases

A drop in new Covid-19 cases and hospitalisations helped to drive global equities to new highs last week.

In the US, the seven-day average of new coronavirus cases has fallen by nearly 64% since its January peak, while the number of hospitalisations has fallen from 130,000 to 67,023. UK data shows the R number is below one for the first time since July, with the number of cases down 18% week-on-week.

According to the World Health Organization, there has been a 17% decline in new Covid-19 cases worldwide, although it warned data from smaller countries may be incomplete. Experts said the emergence of more contagious variants poses continued risks, and that ongoing travel bans and lockdowns in many countries show the disruption is far from over.

Economic woes continue

Although there is more optimism about the end of the pandemic, US consumer sentiment fell unexpectedly in February, demonstrating that households are still worried about the economy. The University of Michigan’s preliminary Consumer Sentiment Index declined from 79 to 76.2, while the measure of what consumers expect in the next six months dropped to 69.8, the weakest reading in half a year.

A Reuters poll showed the US economy is expected to reach pre-Covid-19 levels within a year as the proposed $1.9trn fiscal bill helps to boost economic activity. However, employment will likely take more than a year to fully recover.

Meanwhile, figures from the Office for National Statistics showed the UK economy contracted by 9.9% in 2020 – the largest drop since 1709 – although it avoided a double-dip recession with 1% growth in the fourth quarter. The fall in output was more than twice as deep as during the global financial crisis of 2009.

The third lockdown is expected to cause the UK economy to shrink further in the first quarter of 2021, but the Bank of England forecasts a rebound in the spring as restrictions start to be lifted. In the eurozone, the economy is expected to grow by 3.8% in 2021 and 2022. Although the forecast for 2021 is lower than the previous projection of 5% growth, the European Commission expects the economy to return to pre-pandemic levels in 2022, earlier than previously anticipated.

Gold price holding up

Last week saw softer-than-expected inflation data from the US, with the core consumer price index unchanged in January – below estimates of a 0.2% increase. This pushed down Treasury yields in the middle of the week, but they increased again on Friday to the highest levels seen since March.

The price of gold is holding up fairly well against a backdrop of rising bond yields and a surging stock market. This is because real bond yields, the most important macro variable for the gold price, have moved a bit lower.

Another quick update from Brewin Dolphin, these updates are a good way of keeping up to speed with developments in the markets. Please continue to check back for our latest updates and blog posts.