Please see the below article received by AJ Bell late last night:

On average a Tory occupant of Number 11 has been better for ‘real returns’.

The Conservative Party’s Benjamin Disraeli, twice prime minister and thrice chancellor of the exchequer, once said of his bitterest political rival, who held each post on four occasions: ‘Well, if Mr Gladstone fell into the Thames that would be a misfortune; and if anybody pulled him out, that would be a calamity.’

The Tories’ latest Chancellor, Rishi Sunak, will be hoping for a warmer welcome for Wednesday’s Budget (3 March) and he is likely to measure success in terms of jobs, economic growth and ultimately opinion polls and votes.

Investors will be looking to their portfolios to gauge the effect of his policies and history suggests that the UK stock market has, for whatever reason, done better on average under Conservative chancellors than Labour ones, at least once inflation is taken into account.

Party On

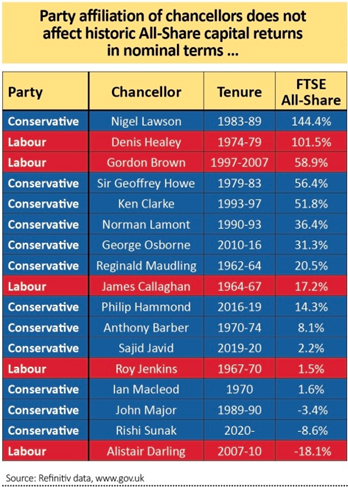

Since the inception of the FTSE All-Share index in 1962, the UK has had 17 chancellors, 12 of whom have been Conservative and five Labour.

At first glance, there is nothing in it between the two parties. Under Conservative chancellors, the FTSE All-Share has chalked up a total capital gain of 355%, in nominal terms.

That equates to an average advance per chancellor of 32.1% (including Macleod’s brief term with that of his successor, Anthony Barber), while under Labour the benchmark has risen by 161% for an average gain of 32.2%.

Across 34 years of Tory chancellorships that is a compound annual growth rate (CAGR) of 4.5% against 4.1% under 24 years of Labour in 11 Downing Street and two of the top-five best spells under a single chancellor actually come under Labour, again in nominal terms.

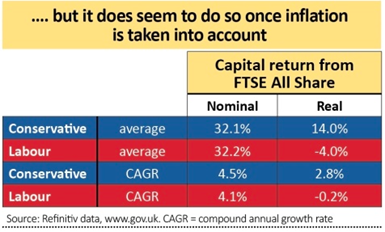

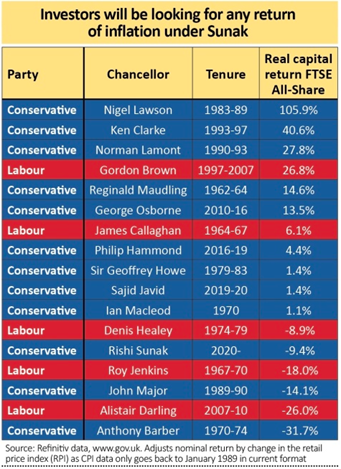

However, the picture changes profoundly when inflation is taken into account and capital returns from the FTSE All-Share are assessed in real (post-inflation) terms rather than nominal ones.

Here, Conservative chancellors come out well on top, as the withering effect of inflation upon investors’ returns from the stock market under Labour’s Healey chancellorship of the mid-to-late 1970s comes into play.

It must be noted that inflation also chewed up the nominal gains made by the FTSE All-Share under the Tory chancellors Sir Geoffrey Howe (1979-83) and Tony Barber (1970-74).

Beware A Return to Barber

As financial markets today ponder whether inflation is about to make a return, and the yield on the benchmark UK ten-year bond, or gilt, rises as prices fall, a repeat of the ‘Barber Boom’ is something that Sunak will be determined to avoid, even if he will be looking to support and boost growth as best he can, as the economic fall-out that followed was very painful for the UK and so painful that the Tories fell from office after a pair of general elections in 1974.

Not all of the inflation that tore through the British economy could be laid at the door of Barber’s policies, as the 1973 oil price shock had a huge amount to do with it, and this highlights the importance of factors which are beyond the control of any chancellor, no matter how diligent or skilled.

Alastair Darling could hardly have expected to inherit the 2007/8 financial crisis which prompted a deep recession and a wicked bear stock market. Norman Lamont inherited British membership of the Exchange Rate Mechanism, fought to defend the pound and a policy in which he did not believe and oversaw a devaluation of sterling which actually helped the FTSE All-Share to rally.

Sunak has had to contend with Covid-19 and the worst recession for three centuries, so perhaps he has been given the worst hand of all.

Even so, investors, looking at the world through the narrow perspective of their portfolios, will be wanting Sunak to think back to Barber. Inflation mangled portfolio returns for much of the 1970s and all the way through to the Thatcher-Howe prime Minister-chancellor team of 1979-83. Bizarre as it may sound, markets may therefore want to see a little inflation – and growth – but not too much, especially as any sustained surge in prices could force bond yields higher and even oblige the Bank of England to act and raise interest rates.

Markets came close to falling out of bed last week, as they pondered such a prospect, so as ever Sunak has a difficult balancing act going forward, as he juggles growth, jobs, the deficit and inflation, as well as votes.

Please continue to check back for more of our regular blog content.

Please see below article received from Jupiter yesterday evening, which analyses whether the measures announced by Rishi Sunak in Budget 2021 will sustain the UK’s economic and financial market recovery in the years ahead.

In every downturn, the UK Government’s finances turn down sharply. Tax receipts fall as job losses, bankruptcies and subdued spending impact the three big sources of revenue for the Treasury – income tax, National Insurance and VAT. But Government spending must rise to cushion the impact of a recession, through unemployment benefits and welfare payments.

There is always a moment at the depths of a downturn when the Government’s budget deficit looks awful and the prospect of a return to more balanced books nigh impossible.

Clearly this pandemic has a rather different dynamic, as the Government measures to support the economy from complete collapse during extended lockdowns, has pushed their spending to levels unprecedented outside wartime. Roughly 75% of the increase in the budget deficit has arisen due to these support measures – about £200bn. Today’s extension of such support until September will only increase the scale of this spending, all funded through borrowing.

Whilst tax receipts have fallen during the pandemic, they have done so only modestly – testimony to the success of the support in limiting the rise in unemployment and bankruptcies thus far. Tax receipts as a percentage of GDP have remained roughly in line with their long run average of 37% of GDP.

Government spending, by contrast, has risen from its more usual level of 40% of GDP to 55% and rising. Hence the Chancellor’s desire to ‘level with the British people’ on the unsustainability of current levels of borrowing and spending by Government and the need to rebuild public finances in the future.

The risk of raising taxes too soon into the post-pandemic recovery is that it saps the strength of the recovery. I believe there is bound to be a surge in consumer spending as individuals and families enjoy their freedom from lockdown to shop, eat out and holiday. But it won’t be until well into 2022 before we know the full scale of the likely bankruptcies to come, the peak levels unemployment will reach – today’s more upbeat forecast notwithstanding – nor the longer-term psychological impact on consumers of the pandemic on spending and saving habits.

Crucially, though, the Chancellor needs to remember the lesson of all his predecessors in the depths of a recession. The cyclicality of Government finances means that as the economy recovers, automatically Government spending will fall and tax receipts will rise. The end to Government support measures and a resumption of consumer spending will boost VAT receipts just as the support cheques cease to be written; in this regard, I believe the transition measures announced today are to be welcomed.

Clearly though, one of the most significant of today’s announcements is the planned increase in Corporation Tax as of April 2023 from the current 19% to 25%. While this does indeed give businesses clarity, it is nevertheless a substantial increase, which will in time impact on companies’ ability to return profits to shareholders, and at variance with widely held expectations that such hikes would begin sooner and would be more gradual in their introduction.

Investors will be considering the impact of this pending rise and will be asking themselves to what extent it can be offset by the generous-sounding 130% “super deduction” on business investment. While this is, in my view, an innovative and progressive policy, taken together with the upcoming rise in Corporation Tax, it is likely to mean that the economic growth benefits resulting from the policy will be somewhat front loaded.

Meanwhile, the decision to maintain income tax, National Insurance and VAT at their current levels should provide some support consumer confidence and household budgets as the country emerges from the pandemic. Nevertheless, the Chancellor’s explicit announcements of upcoming fiscal drag – the result of not adjusting taxation thresholds to take account of future inflation – reflects the reality of the situation of the post-pandemic economy. Although this is undoubtedly a progressive policy, put simply, the higher inflation rises, the more the Treasury is likely to benefit. Over time, should we enter a more inflationary environment, in public finance terms this may well turn out to have been a prudent decision, given the impact of rising inflation on the cost of servicing our national debt.

Turning to the UK equity market, it was no surprise to see rising share prices among those businesses that should be beneficiaries of further support to the domestic economy, such as banks and leisure stocks, alongside housebuilders. The latter may well benefit from the extension of the stamp duty holiday and mortgage guarantee programme, as well as a more benign backdrop through the extension of Government support through the summer’s transition from lockdown and re-opening to the end of measures such as the furlough scheme.

Looking to the longer term, to my mind, the truly prudent but wise Chancellor will not risk the upturn by setting out a plan for increased taxation in the years ahead, but keep his powder dry to see just how radically Treasury finances improve over the coming year, without any action on his part whatsoever. While today’s Budget announcements appear well placed to support the transition to life after the pandemic over the next couple of years, it remains to be seen whether the “front-loading” of business incentives to spend now but be taxed later leads to a slowdown in growth thereafter which might not have been necessary.

We will continue to publish relevant content and news as the vaccine roll-out in the UK continues to expand and the light at the end of the tunnel brightens. Please therefore, check in again with us soon.

Please see below an article from Brewin Dolphin received late yesterday evening, which details their overview on the Chancellor, Rishi Sunak’s budget, which was unveiled in Parliament yesterday:

As you can see from the above, the Chancellor has announced significant measures to help businesses get back on their feet and innovate and help the economy recover. It looks like businesses will bare the initial brunt of raising additional revenue for the Treasury and the freeze of the allowances and thresholds until 2026 after April’s increases will also generate some additional revenue.

Tax consultations are commencing shortly – we await the outcome of these.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

HM Treasury and HMRC quietly launched additional proposals on 11/02/2021 with the potential to have a much greater effect on retirement planning over the coming years.

The proposals

The main proposal is this: anyone who was a member of a registered pension scheme on 11 February 2021 (the date of the consultation) and had a right to take pension benefits before age 57 on that date, would keep that right as a protected pension age. That protected pension age (which in most cases would be 55) would be scheme specific and work similarly to existing protected pension ages. This would mean:

Anyone joining a new pension scheme from 12 February 2021 onwards would have an NMPA of 57 from 2028 for that scheme, although they may have other pensions that they could still access before age 57.

From 12 February 2021, anyone who transfers to a new scheme would lose the right to take benefits from that pension before age 57 (assuming the original scheme offered that right), unless they completed a block transfer.

One key difference highlighted between the rules for existing protected pension ages and these proposals, is that clients would not need to crystallise all the benefits within a scheme on the same date in order to keep their protected pension age.

Next steps

The timing of proposals like these is always difficult. The consultation doesn’t close until 22 April, and we don’t expect to see draft legislation from the Treasury until the summer. However, if the proposals do go ahead as they stand, transfers that take place from today could affect when clients are able to take benefits. While many people may not expect to retire at 55 or 56 (and until yesterday might have assumed it simply wouldn’t be an option), it still adds an additional consideration into people’s pension planning.

It’s still early days, and I’m sure you’ll see more about the industry’s thoughts about the proposals over the coming weeks. What seemed like a very straight forward upcoming pension change has suddenly become something to keep a keen eye on.

Our Comment

We need to see what the outcome is in the summer, but this is one to watch for those who are considering retiring early at age 55 or if you thought you might access your pension benefits, typically tax free cash, early at age 55 from 2028.

In real terms this will only be a few people, most in the UK haven’t got the pension assets they need for early retirement and shouldn’t access their pension funds too early either.

However, if you are one of the few that may have a plan to retire early or access your pension benefits early, at age 55, from 2028 you now need to be careful about any pension switching or consolidation. Let’s see what we get at the end of the consultation, hopefully draft legislation in the summer. Watch this space.

Steve Speed

03/03/2021

Technical content cut and pasted from Curtis Banks Technical Update.

Please see below the latest ‘Markets in a Minute’ article from Brewin Dolphin received late yesterday afternoon – 02/03/2021

Equities slide as rise in bond yields sparks tech sell-off

Global equities fell sharply last week after a steep rise in long-term government bond yields led to the worst technology sell-off in four months.

In the US, the S&P 500 recorded its biggest weekly drop in a month, falling 2.5%. The Nasdaq Composite suffered its worst decline since October, down 4.9%, as investors continued to rotate out of highly valued growth stocks into value and cyclical stocks. A rise in oil prices saw energy shares outperform, whereas consumer discretionary stocks were weak.

Stock markets in Europe also fell, with the pan-European STOXX 600 ending the week down 2.4%. The FTSE 100 dropped 2.1% as the pound rose to its highest level in almost three years, fuelled by the rapid roll out of the Covid-19 vaccine and hopes of economic recovery.

The global sell-off fed through to Asia, where the Nikkei fell 3.5% and the Shanghai Composite tumbled 5%. China’s large-cap CSI 200 recorded its worst weekly performance since October 2018, falling 7.7% as profit-taking hit companies in sectors such as semiconductors and electric vehicles.

*Data from close on Friday 19 February to close of business on Friday 26 February.

Budget leaks boost FTSE 100

The FTSE 100 rebounded on Monday, gaining 1.6% following a series of leaks about Wednesday’s budget. Housebuilders rallied on news that the government will launch a mortgage guarantee scheme to help buyers, with small deposits, onto the property ladder.

In the US, the S&P 500 gained 2.4% in its best session since June 2020. The Nasdaq surged 3% after vaccine optimism boosted risk assets and Treasury yields retreated. The Bank of England echoed sentiments from the Federal Reserve about accommodative monetary policy.

The rebound began to falter on Tuesday, with the Hang Seng and CSI 300 both declining by around 1% overnight. A top Chinese banking regulator said he was ‘very worried’ about bubbles in overseas financial markets and in China’s property sector. The FTSE 100 opened flat, with energy and mining stocks among the worst performers amid fears of slowing demand for commodities in China. Taylor Wimpey was the biggest gainer, adding 3.4% after it revealed the 2021 selling season had started positively.

Economic data stronger than anticipated

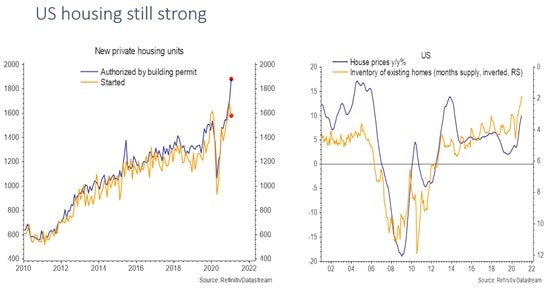

The yield on the ten-year US Treasury note increased to its highest level in over a year last week, as stronger-than-expected economic data fuelled fears about rising inflation. In the US, data revealed continued robustness in the housing market, with building permits hitting a new high and house prices continuing to surge.

Sales on new single-family homes increased by 4.3% in January to a seasonally adjusted annual rate of 923,000 units. Sales were helped by historically low mortgage rates and a shortage of previously owned houses on the market. The median new house price rose by 5.3% from a year earlier to $346,400.

The housing data added to solid PMIs published the week before, which showed a 1.3% increase in the prices that businesses receive for their goods and services – the biggest gain since the index was launched in 2009. Weekly jobless claims also hit their lowest level in three months at 730,000, while personal incomes increased by 10.1% in January following payments from the coronavirus relief package.

On Wednesday, Fed chair Jerome Powell sought to allay investors’ fears that stronger economic growth will result in monetary stimulus being removed sooner than expected. Powell said inflation remains soft and confirmed the Fed’s dovish stance. Stocks briefly recovered on Wednesday, but began their descent again the following day, suggesting Powell’s comments have done little to quell investors’ concerns.

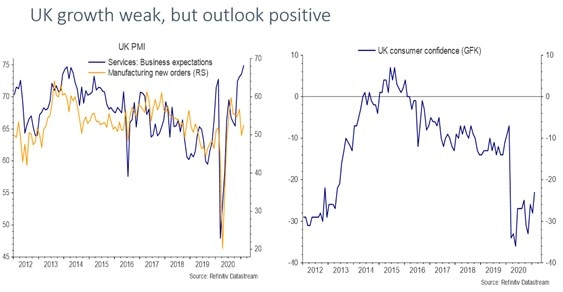

UK consumer confidence creeps higher

There is also optimism in some of the UK’s economic data. Manufacturing new orders remain in expansion territory, and the expectations component of the services PMI hit the highest level in over a decade. UK consumer confidence is also starting to creep higher.

Lockdown restrictions will start to ease in England from 8 March, with nearly all sections of the economy due to be reopened in late May. In Wednesday’s budget, Rishi Sunak is expected to announce that the furlough scheme will be extended until at least May. Around 20 million people in the UK have now received their first dose of the vaccine.

The vaccine rollout continues to lag in Europe, with just 6.4% of the European Union’s population receiving a jab. Despite this, the eurozone Economic Sentiment Indicator increased to 93.4 in February from 91.5 the month before – the highest level since March 2020. Fourth-quarter German GDP data was revised to a growth rate of 0.3% from an initial estimate of 0.1%, following strong exports and construction activity.

Over in Japan, the Reuters monthly Tankan Index, which tracks the Bank of Japan’s quarterly Tankan survey, recorded a positive reading among manufacturers for the first time since 2019, thanks to improving demand from overseas. Japan is also seeing a decline in the Covid-19 infection rate, which will see the state of emergency status being lifted for six prefectures a week earlier than planned.

Weekly updates like these from Brewin Dolphin help us keep up to date with what is happening within the markets. This week’s ‘Markets in a Minute’ article focuses on exploring some of the reasons behind the tech sell-off.

Please continue to check back for our regular blog posts and updates

M&G plc (M&G) is today joining the Powering Past Coal Alliance (PPCA) and announcing it wants to end investment in thermal coal by 2030 for developed countries and 2040 for emerging markets.

M&G’s coal phase out plan is a key step towards achieving its goal of net zero carbon emissions across its investment portfolios by 2050 at the latest, and helping to restrict global warming to 1.5 degrees in line with the Paris Agreement on climate change.

As stewards of long term capital, actively managing the savings of millions of people around the world, M&G will use its influence to accelerate the transition to a greener, cleaner economy with ambitious plans to cease all investment in new coal mines and coal-fired plants and to exclude public companies which cannot commit to a complete phase out of coal by 2030 in developed countries and 2040 in emerging markets.

As an asset owner, M&G will be implementing this approach to coal-related investments across its own internal portfolios over the coming year. As an asset manager, M&G will be working with clients to align existing mandates and funds to this position.

At the same time, through its growing range of sustainable investment funds, M&G is giving institutional clients and individual customers the opportunity to invest in technologies, infrastructure and services which offer financial returns as well as making a positive difference to the environment.

Speaking at PPCA’s Global Summit today, M&G plc Chief Executive, John Foley, said: “An accelerated phase-out of coal is essential if we want to limit global warming and ensure a sustainable future for our planet. We are delighted to join the PPCA and fully support its work to encourage businesses, governments and other organisations to commit to a transition away from coal in the run up to COP26 later this year.”

Welcoming M&G’s commitment to the PPCA, Nigel Topping, COP 26 High Level Climate Champion, adds: “Phasing out thermal coal is a critical early step on the race to net zero. PPCA is a key part of the COP 26 Energy Transition Campaign, and it is fantastic to see M&G making this commitment in response to attending the PPCA ministerial round table co-hosted by the UK and Canada.”

As our clients will know, Prudential’s PruFund range of funds are managed by M&G’s multi asset team, Treasury & Investment Office (T&IO) – one of the largest and most well resourced in the UK.

This is great news, and another step along the ESG road for M&G.

M&G plc aim to be carbon net zero as a corporate entity by 2030. Further, they aim to achieve 40% female and 20% ethnicity representation in their leadership by 2025.

Prudential Assurance Company aims to achieve net zero carbon emissions across AUMA (assets under management and administration) by 2050, of which the PruFund range is a material part, in line with the Net Zero Asset Owners Alliance.

The scale of PruFund allows the management team to use segregated mandates to apply a variety of implementation techniques for their ESG views, up to and including, exclusion of certain stocks or sectors from portfolios.

Currently their policy excludes investment in certain controversial weapons companies, namely cluster munitions and anti-personnel mines.

M&G look to the asset managers they select to engage with companies as active owners that help foster a more sustainable economy, participate in voting on key issues such as Climate Change and ensure that ESG is integrated into their investment processes. The majority of PruFund assets are managed by M&G, whose Responsible Investment team provide issuer and sector specific ESG risk and opportunity analysis and education on sustainability themes to portfolio managers and analysts.

Investments have recently been made with the PruFund range by purchasing a solar power plant in the Nevada desert.

Keep checking back for more ESG related content along with our usual market updates and outlooks from a variety of fund managers.

Please see below for Brooks MacDonald’s latest weekly market commentary received by us late afternoon 01/03/2021:

In Summary:

Yield rises remain the major driver of equity markets

Johnson & Johnson’s single shot vaccine is approved in the US, adding to the breadth of vaccine supply

Israel eases some restrictions as the UK is set to lay out its reopening plans

Yield rises remain the major driver of equity markets

Last week saw a large uptick in volatility as higher yields caused a sell-off in markets that focused on secular growth sectors such as technology. Meanwhile, previously unloved sectors such as banks performed strongly on the back of steepening yield curves and lower expected defaults in the future as the economy recovers.

Johnson & Johnson’s single shot vaccine is approved in the US, adding to the breadth of vaccine supply

The theme of the last few days has been a tightening of restrictions, rather than loosening, as several European countries needed to roll back liberties and Auckland, New Zealand entered a fresh lockdown. More positively, the Johnson & Johnson (J&J) vaccine has been approved in the US with the company saying they can ship 100 million doses in H1 2021. While the efficacy data was less compelling for the J&J vaccine, it is recommended as a single dose vaccine which makes the rollout of logistics simpler.

The change in yields has had an outsized impact on technology companies

The ‘price’ of a financial asset is the sum of its future cashflows adjusted for a discount rate. In practice this means the sum of a company’s future earnings which are adjusted for interest rates plus an extra company specific risk premium on top. Value companies tend to produce higher earnings now but less exciting earnings in the future. Growth companies, by contrast, produce little now but are expected to make outsized earnings in the future. Because the earnings in growth companies tend to be further away, the discount rate is more important. Due to the power of compounding, a small change in interest rates can significantly reduce the present value of future earnings 10 or 20 years away. This is exactly what happened last week when a pickup in interest rate expectations caused high growth companies to look less attractive. The moves were relatively small, with the US 10 year rising around 7bps to just over 1.4% but with valuations richer in the technology space, this was enough to catalyse a sell-off.

Of course, the question is whether central banks will let further yield rises happen. So far, the Federal Reserve have pushed back against expectations for sustained inflation but have broadly welcomed the pickup in yields, saying it is reflective of an improved economic backdrop. The next Federal Reserve (Fed) meeting is on 16-17 March, however this week we hear from a series of members including Fed Chair Jerome Powell. Should rapid rises in yields continue to be a theme, we expect the Federal Reserve to step in, at least verbally, to steady further rises. Yield rises can impact both financial stability and damage the economic recovery so central banks will be paying close attention.

Please continue to utilise these blogs and expert insights to keep your own holistic view of the market up to date.

Please see below an article from Legal & General Investment Managers Asset Allocation team, which was published late yesterday afternoon and details a variety of views on Bond Yield movements and their potential impact on markets:

As you can see from the above article, there are various factors to be considered when trying to assess how Bond Yield movements will impact on markets. I believe LGIM are saying that short-term bond yield increases may be unwanted, and there are fiscal tools (i.e. Quantative Easing) to help dampen demand and keep rates lower. Also, any potential equity sell-off which has stemmed from rate increases could be seen as a buying opportunity.

Other fund manager views could differ from the above.

I think the key message regardless, is to keep calm and remain invested for the long-term, markets will recover from short-term dips.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Fund managers Invesco published a paper last week called ‘Appetite for change: food, ESG and the nexus of nature’ which looks at the impact of the Covid pandemic on ESG considerations.

We have picked out some of the key points from this paper below and added our own commentary in blue.

ESG Recap

Before we look at Invesco’s paper and the points they raised, lets recap on what ESG is.

ESG stands for Environmental, Social and Governance. Investopedia definition for ESG is; ‘Environmental, social and governance (ESG) criteria are a set of standards for a company’s operations that socially conscious investors use to screen potential investments.’

The key points raised by the Invesco paper are as follows:

The COVID-19 crisis has demonstrated that humanity’s understanding of its own relationship with the natural world remains inadequate – often dangerously so.

The pandemic has particularly exposed the interconnectedness of numerous existential threats, all of which might be described as components of the “nexus of nature”.

One of the most perilous yet underappreciated of these threats is the unsustainability of prevailing attitudes towards food production and consumption.

From the use of resources in developing countries to policies and practices around factory farming in the industrialised world, this issue affects the entire value chain.

Guided by the idea of materiality and initiatives such as FAIRR (Established by the Jeremy Coller Foundation, the FAIRR Initiative is a collaborative investor network that raises awareness of the environmental, social and governance (ESG) risks and opportunities caused by intensive animal production), investors are increasingly applying environmental, social and governance (ESG) principles in this sector.

As well as promoting and protecting sustainable investments, these efforts are showing how positive change in one area can benefit the nexus of nature more widely.

Interconnectedness means that the ripple effects can encompass concerns including deforestation, biodiversity loss, waste pollution, climate change and human health.

The ‘nexus of nature’

The longer-term survival of our planet and its inhabitants is strongly connected to various existential threats that are themselves highly interrelated. They include climate change, overpopulation, deforestation, loss of biodiversity and – perhaps least appreciated – the ways in which food is produced and consumed. In turn, each of these has a major influence on our health and wellbeing.

The World Economic Forum’s latest Global Risks Report underlines this. Eight of the 10 potentially most impactful risks over the next decade can be linked to humanity’s tendency to take the natural world for granted. Only weapons of mass destruction and cyber-attacks can reasonably be thought of as removed from the nexus of nature.

Why is it so important to grasp how food production and consumption might fit into this picture? The short explanation is that many of the practices that have become commonplace in the face of ever-rising demand for animal protein have consequences that are both far-reaching and deleterious. There may be no better illustration than the circumstances behind the advent of COVID-19.

As has been extensively documented, one of the likeliest sources of the outbreak was a “wet market” where livestock was reportedly kept in close proximity to dead animals. Here, originating either in bats or pangolins, the virus is believed to have been transmitted to humans via a process of zoonosis.

Something analogous happened in the late 1990s, when the emergence of the Nipah virus provided a salutary demonstration of how the nexus of nature can function. Native fruit bats were driven from their traditional habitats by deforestation; they started foraging in trees near farms; through their bodily fluids, they infected land used for raising pigs; and the pigs duly passed the disease on to farmers and abattoir employees.

Similarly, the SARS virus of 2002 is now thought to have come from horseshoe bats, eventually reaching humans via consumption of cat-like mammals known as civets. This, too, was an ominous warning of our collective vulnerability to a type of natural hyperconnectivity that is often woefully underestimated or wilfully ignored.

At first glance, given the circumstances surrounding these examples, it may be tempting to infer that the nexus of nature is at its most threatening in relatively rural settings or in developing economies. In fact, this is far from the case. As we explain in the next chapter, the phenomenon is present throughout the value chain of food production and consumption and represents a genuinely worldwide concern.

According to the World Economic Forum (WEF), risks related to the natural world now dominate the existential threats confronting humanity. They have gradually displaced economic, geopolitical and societal concerns in recent years, particularly since 2011.

The top 10 potentially most impactful global risks over the next decade, as collated in the WEF’s latest report, are shown below. Note that even those classified as societal are in some way linked to nature.

Intensive food production through the lens of material ESG risk

The FAIRR initiative is a collaborative investor network that raises awareness of the ESG risks and opportunities caused by the intensive farming of animals. Through its research, it helps investors integrate such factors into their decision-making and active stewardship processes. FAIRR has identified 28 material ESG issues that could affect factory farms’ financial performance and returns. Set out below, they include community health impacts and infectious diseases.

Conclusion

The COVID-19 crisis has underlined the hyperconnectivity of multiple existential threats, all of them constituents of the nexus of nature. It has also highlighted the position within the nexus of food production and consumption, and in doing so it has provided a stark warning that many of the prevailing policies and practices within this arena are likely to prove unsustainable.

Of course, investors have no more entitlement than anyone else to pass judgment on what is right or wrong. They are not self-appointed saviours or heroes. They do not constitute a deus ex machina for this sector or any other.

Relatedly, investors do not have all the answers. In food production and consumption, as in so many corporate spheres, progress and transformation stem in the main from the companies themselves and from the gathering weight of scientific evidence.

What investors do have, though, is capital; and it is capital that enables positive, lasting change to take place. This has already been demonstrated in a variety of settings, and it is now increasingly being demonstrated in reshaping how we meet the challenges of feeding an ever-growing global population – as we will explore in more detail in our next paper.

By applying ESG principles, investors can make a difference – one likely to have far-reaching impacts. This is the essence of responsible investing and shareholder capitalism, as is already well known, but it is also the essence of the nexus of nature. Positive, lasting change in one area should lead to positive, lasting change in many others – just as the bleak effects of taking the natural world for granted in one area have been felt in many others in the past.

Deforestation, biodiversity loss, waste pollution, climate change, human health – responsible investments in food production and consumption can play a part in addressing all these issues and many more. Nature’s boundless imagination, as so admired by Richard Feynman, guarantees as much.

Feynman once also memorably remarked: “Nature cannot be fooled.” This truth has become all too obvious in recent decades and during 2020 in particular. By engaging with companies and policymakers and by supporting initiatives that prize sustainability, transparency and accountability, investors can go a long way towards helping ensure that humanity does not fool itself.

Our Comments

We have been talking about ESG for a while now, and as we have noted before, the pandemic has really put this topic under the spotlight. As you can see from the key points of the Invesco paper that we have picked out, ESG is a wide-ranging topic and is much more than just ‘being a ‘good’ investor.

The principles behind ESG need to be embedded in an investment framework which encourages positive change.

We build ESG into our ongoing due diligence process to ensure we have a wide range of ‘core investments’ for our clients, which not only seek to provide good returns, but also to drive ESG forward and make lasting and positive impacts in the world.

More investment managers and fund houses are launching ESG investments or starting to move in the right direction with their existing investment offerings, engaging with businesses they invest in.

The demand for ESG and socially responsible investments is growing. Even in the past few months, the term ESG is seen much more in the financial press now than it was.

One thing investors and we as an independent financial advice firm need to watch out for is ‘greenwashing’.

Greenwashing is the process of conveying a false impression or providing misleading information about how a company’s products are more environmentally sound. Greenwashing is considered an unsubstantiated claim to deceive consumers into believing that a company’s products are environmentally friendly.

This can be an attempt to capitalise on growing demand for socially responsible investments.

We recently watched a webinar by Royal London on responsible investing and they highlighted that 85% of funds labelled ‘green’ have misleading marketing* (*Source: 2degrees investing initiative, 2020).

We try to avoid ‘greenwashing’ by doing thorough due diligence, such as asking investment providers questions such as ‘what are their responsible investment policies?’ and ‘how is ESG integrated into investment decisions?’

Our due diligence process is also ongoing, we make sure we stay in regular contact with any of the investment providers we recommend ensuring we understand their investments and investment decisions on an ongoing basis.

The Invesco paper looked at here in this post, gives some food for thought. Invesco are a large investment house and we rely on their input and updates to help us get a handle on key investment issues alongside their peers. We quickly understand the consensus view.

Stay tuned for more on ESG and socially responsible investing along with our regular blog content providing updates and insights from a range of fund managers to help you understand what is happening in the markets and the world.

Please see below article received from AJ Bell yesterday afternoon, which provides a global review of bond markets and offers recommendations for potential future investment winners.

Zambia, Venezuela, Tajikistan and Armenia do not make a habit of featuring in this column, not least as they are a bit off the beaten track, even for the most intrepid adviser or client. But they catch the eye because each member of this quartet has seen an increase in interest rates this year, to take the total for 2021 so far to five increases and two cuts from global central banks (Mozambique is the fifth for those who are interested).

Five central banks have raised rates so far in 2021

“Many advisers and clients are unlikely to be stirred by events in Zambia, Venezuela, Tajikistan and Armenia but they may need to pay attention for three reasons.”

Those who are not interested will ponder the relevance of this possible trend, but they may need to pay attention for three reasons.

It could be an early ‘risk-off’ sign in financial markets. When markets become incrementally more cautious, they tend to cut their riskiest positions first. Frontier markets such as these, or even more generally, would fit that bill. Their central banks may be raising rates to try and lure capital back or at least reaffirm their credibility with overseas lenders.

It could be a sign that markets are, at the periphery, starting to deleverage or at least balk at the tidal wave of debt that continues to build – Bloomberg data shows that the total of global bonds in issue now stands at a record-high $67.6 trillion. And, generally speaking, when markets turn cautious, it is the peripheral markets that show distress first, rather than the core ones, as it is in the latter that the bulls always have the greatest faith and thus where they make their final stand before they capitulate and make way for the bears.

It could be a sign that inflationary worries are seeping into Government bond markets the world over (see this column, SHARES, 11 February 2021). Bloomberg research reveals that the value of global bonds with negative yields has dropped by $3 trillion this year so far, although that still leaves a total of some $14 trillion.

None of these things may come to pass. It could be that the deflationary force of interest payments, demographic trends and central bank intervention keep fixed-income investors in clover as they combine to keep interest rates and inflation well and truly anchored, to the benefit of the bond portion of any portfolio, especially the long-duration segment. Yet if any of the above three trends keeps running, then the meagre coupons offered by most fixed-instruments would leave them looking like return-free risk and speak in favour of short-duration exposure for anyone seeking bond-like ballast in their asset allocation plan.

“If any of the above three trends comes to pass, then the meagre coupons offered by most fixed-instruments would leave them looking like return-free risk and speak in favour of short-duration exposure for anyone seeking bond-like ballast in their asset allocation plan.”

Turning tide

A quick look at the benchmark 10-year bonds of key emerging markets might suggest that investors are taking risk off the table. Selling bonds here means yields are creeping up and prices creeping down. They might not look like big moves, but the very right-hand side of those lines show an upward shift in bond yields – to 6.59% from 6.15% in the last month alone in Russia.

Emerging market bond yields are moving higher

A look at developed market bonds suggests concerns over gathering debt. In Europe, for example, benchmark 10-year bond yields are creeping higher, despite the European Central Bank’s quantitative easing (QE) scheme. No wonder, when advisers and clients consider that the world’s debt pile soared by $24 trillion to a record $281 trillion in 2020, according to the Institute of International Finance. That was an extra 35 percentage points of GDP to take the debt/GDP ratio to 355%. Remember that the Global Financial Crisis started in 2008 when the global debt was ‘just’ $187 trillion.

Developed market bond yield are going up

Even the yield on 10-year Japanese Government Bonds (JGBs) stands at 0.10%, the top of the Bank of Japan’s target range and no different from late January 2016. Perhaps even loyal holders of JGBs are contemplating the return of inflation after 30 years.

10-year JGB yield sits at top of BoJ’s target range

China syndrome

“In a worst-case scenario, central banks may want to raise rates to curb inflation, if it really does run hot, but struggle to do so, because of the immediate impact this would have on economic growth – and financial asset prices.”

Again, all of these trends could yet fizzle out. In a worst-case scenario, they become more pronounced. Central banks may want to raise rates to curb inflation, if it really does run hot, but struggle to do so, because of the immediate impact this would have on economic growth – and financial asset prices. In this context, China is an interesting test case.

China did not hike overnight lending rates for long

The People’s Bank of China jacked up overnight borrowing costs in late January but quickly backed off as the Shanghai Composite index wobbled. As soon as policy was eased, share prices rose. The monetary authorities have a delicate balancing act ahead of them.

We will continue to publish market analysis and thought-provoking financial news, so please check in again with us soon.