Please see below article received from AJ Bell yesterday morning, which provides a cautionary commentary on the historic effects of inflation and dissects current market behaviour.

Even a reading of 1.5% inflation in the UK’s consumer price index is giving stock markets the jitters, although that it still a very, very, very long way below the sort of levels which gave investors terrible trouble in the 1970s and early 1980s.

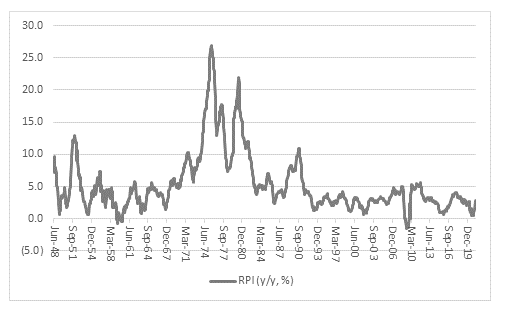

Back then inflation, as measured by the retail price index (for which there is a longer dataset), was roaring away in the twenties. That hurt consumers’ spending power, as their savings lost value in real terms, and dissuaded companies from investing, as the returns on any new projects could not compete with the double-digit interest rates on offer.

Yet the experiences of the 1970s clearly have stock market investors on their guard.

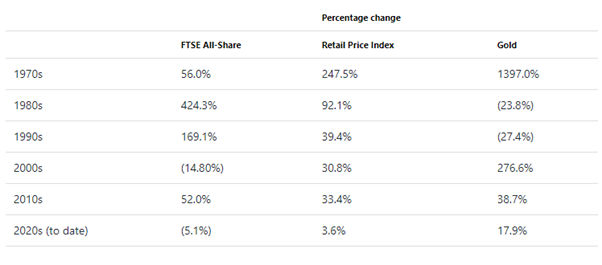

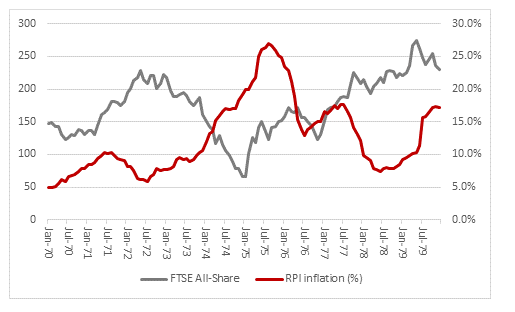

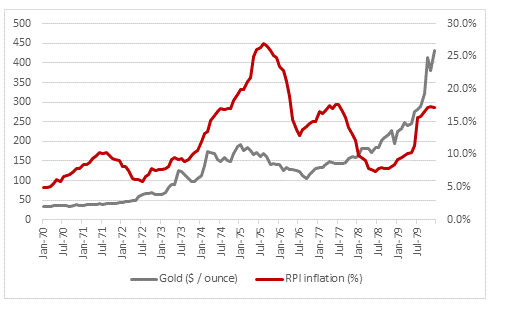

The FTSE All-Share rose by a perfectly respectable 56% in the 1970s, but the retail price index rose by 248%, so equities did not offer as much protection as hoped. Gold did, since the precious metal surged by nearly 1,400%.

Equities came into their own in the 1980s and 1990s as inflation ebbed, interest rates came down and lower returns from cash and bonds persuaded investors to gravitate toward stocks. Gold all but disappeared from view, only to reappear as Governments began to shake the magic money tree in response to the Great Financial Crisis and then came to view such shaking as standard operating procedure in the 2010s and early 2020s.

Investors will also know that the real damage to equity portfolios was done in the late 1970s, when a second wave of inflation hit home, after the appalling state of the UK’s public finances finally caught up with it.

That was also when gold really came into its own, as investors shunned cash and paper assets in favour of ‘real’ assets.

That sequence of events supports the analysis proffered by Jens O. Parrson in his book Dying of Money who studied the surge in American inflation in the 1970s with the even more dramatic surge in Germany in the 1920s:

‘Everyone loves an early inflation. The effects at the beginning of an inflation are all good. There is steepened money expansion, rising government spending, increased government budget deficits, booming stock markets and spectacular general prosperity, all in the midst of temporarily stable prices. Everyone benefits and no-one pays. That is the early part of the cycle. In the later inflation, on the other hand, the effects are all bad. The government may steadily increase the money inflation in order to stave off the later effects, but the later effects patiently wait. In the terminal inflation, there is faltering prosperity, tightness of money, falling stock markets, rising taxes, still larger government deficits and still roaring monetary expansion, now accompanied by soaring prices and ineffectiveness of all traditional remedies. Everyone pays and no-one benefits. That is the cycle of every inflation.

Economists, investors, consumers, savers and above all central bankers will be hoping that Parsson is wrong.

But no-one can ignore how the early building blocks of Parsson’s argument are in place – money supply is rocketing in the US, UK, Europe and Japan; Government deficits are off the clock as they spend like fury to stave off the economic after-shocks posed by the pandemic; asset prices are surging; and calls for yet more spending and stimulus are much louder than those for a scaling back of either fiscal or monetary stimulus. Faith in the existence of a magic money tree that can dispense wealth without consequence is running high.

And yet no central banker can pretend we are in a normal situation or that they are in control. Policies described as emergency measures in 2008-09 are now the norm, as interest rates remain anchored at record lows and Quantitative Easing programmes continue to run at full tilt. Any attempts to row back on those policies prompt financial market volatility and a rapid spill-over in to the ‘real’ economy, as we saw in 2018 and 2019. Global debts continue to accumulate, providing only the weakest of foundations for any economic recovery and ones that are prone to quickly buckling, as we saw globally in 2007-09, in 2011-13 in Southern Europe and around the world again in 2021. Annual Government budget deficits stand at their highest level since the 1940s in many cases and aggregate deficits are in many cases setting new all-time highs on a monthly basis.

Meanwhile, stock markets, cryptocurrencies, non-fungible tokens continue to surge, or at least do so until the threat of rising interest rates, less QE and a drop in the amount of free money with which to idly speculate raises its head once more.

No-one knows what is coming next – inflation, deflation or even stagflation – and investors cannot afford to be too dogmatic about their portfolio allocations, as the three different outcomes require a different response from investors as they seek to augment or at least protect their wealth.

If history is any guide, equities offer some protection against inflation, but with a focus on pricing power, life’s essentials and raw materials. Bonds and cash, both of which are to be avoided in an era of inflation or stagflation, would help in a deflationary environment. And in the case of stagflation, index-linked cash flows such as rents from property, infrastructure projects and index-linked bonds would help, as would gold, at least if the experience of the 1970s is repeated.

Investors therefore need to be prepared for anything with a balanced portfolio that covers all eventualities, because the ultimate outcome is just too hard to predict and also because valuations will reflect different market views at different times.

Just over a year ago, the prospect of inflationary surge was seen as very unlikely and bonds were doing well, shares were doing badly and gold was being completely ignored.

Now, the consensus view is that inflation is indeed coming, as evidenced by how well mining shares and commodity prices have done and sharp falls in bond prices and rapid increases in Government bond yields (albeit from a low base).

Perhaps it is therefore time to start wondering whether it is time to go against the crowd once more.

We will continue to publish relevant content, market analysis and news. Please therefore, check in again with us soon.

Stay safe.

Chloe

24/05/2021