Please see below this week’s Markets in a Minute update from Brewin Dolphin – received late yesterday afternoon – 11/05/2021

Markets mixed as investors rotate out of growth stocks

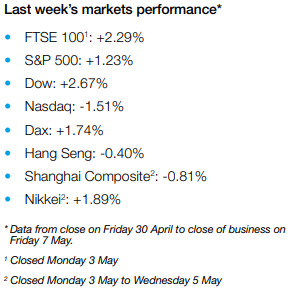

Equities were mixed last week as strong earnings results competed with a renewed rotation out of growth stocks.

The shift to higher-yielding value stocks weighed on the technology-heavy Nasdaq, which slid 1.5% in its worst weekly performance in two months. The S&P 500 and the Dow rose by 1.2% and 2.7%, respectively, after a rally on Friday helped to erase losses from earlier in the week.

The pan-European STOXX 600 gained 1.7% following better-than-expected earnings results and encouraging economic data. Germany’s Dax added 1.7%, while the UK’s FTSE 100 surged 2.3% to end its holiday-shortened four-day week above the 7,000 mark.

In Asia, several indices were closed on Monday through Wednesday for public holidays. Japan’s Nikkei gained 1.9% amid optimism about the global economic recovery, whereas China’s Shanghai Composite ended the week 0.8% lower.

Sterling reaches highest level since February

The FTSE 100 slipped 0.1% to 7,124 on Monday after the pound surged to its highest level against the dollar since February. Some of the factors behind the surge were the upcoming easing of lockdown restrictions, dollar weakness following Friday’s disappointing US payrolls report, and the Conservative Party’s victories in last week’s local elections.

US stocks also closed lower on Monday as the rotation out of growth stocks continued. The Dow slipped 0.1%, the S&P 500 declined 1.0% and the Nasdaq slumped 2.6%, marking its worst session since March.

European markets were sharply lower at Tuesday’s open, with the STOXX 600 down 1.6% and Germany’s Dax and France’s CAC 40 both down 1.7%. The FTSE 100 tumbled 1.9% following losses in Asia-Pacific markets overnight. Engineering group Renishaw and airline group IAG were among the top fallers in the blue-chip index.

US jobs data disappoints

After a flurry of data that suggested the US economy was roaring back to life, last week’s jobs figures came as a disappointment. Non-farm payrolls increased by just 266,000 in April, far lower than the anticipated one million new jobs. The unemployment rate rose to 6.1%, which was worse than the expected 5.8% rate.

US non-farm payrolls

Although the figures were disappointing, they lend weight to the Federal Reserve’s case for maintaining its accommodative monetary policy. Stocks rallied on Friday after the data helped to ease fears about an imminent rise in interest rates.

Elsewhere, the Institute for Supply Management’s gauge of manufacturing activity stood at 60.7 in April, below consensus estimates of around 65.0 and four points lower than in March. US services also grew at a slightly slower pace in April, with the index falling to 62.7 from March’s all-time high of 63.7.

BoE upgrades UK growth forecast

On Thursday, the Bank of England increased its forecast for UK GDP growth to 7.25% in 2021, up from its previous forecast of 5.0%. This would be the fastest growth rate since 1941’s 8.7% expansion, but it follows a contraction of 9.9% in 2020 – the worst for more than three centuries.

Andrew Bailey, the Bank’s governor, told an online news conference that the strength of the economic recovery needs to be put into perspective.

“Let’s not get carried away,” he said. “It takes us back by the end of this year to the level of output we had essentially at the end of 2019 pre-Covid. So that is good news in the context of where we’ve been, but it still means that two years of output growth have been lost to date.”

The upgrade to forecasts followed a better-than-expected economic performance during the third national lockdown at the start of the year. The economy shrank by 1.5% in the first three months of 2021, better than the Bank’s forecast of a 4% contraction.

Eurozone retail sales beat forecasts

There was good news on the eurozone’s economic recovery last week, with the latest retail sales data revealing month-on-month growth of 2.7% in March, thereby beating consensus forecasts. This marked the second monthly increase in a row. Germany and the Netherlands saw particularly strong growth of 7.7% and 8.4%, respectively.

Meanwhile, IHS Markit’s eurozone composite PMI rose to 53.8 in April, the highest since July 2020. The services sub-index rose to 50.5 – moving above the 50.0 figure, which separates growth from contraction, for the first time in seven months.

Europe’s vaccination programme is also gathering pace. As of 9 May, 27.9% of the European Union’s population had received at least one vaccine dose. In Europe as a whole, the figure was 24.1%, according to Our World in Data.

Please continue to check back for our regular blog posts and updates.

Charlotte Ennis

12/05/2021