Please see below the latest ‘Markets in a Minute’ article from Brewin Dolphin received late yesterday afternoon – 18/05/2021

Stocks slide as higher inflation sparks fears of rate hike

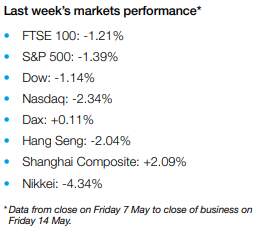

Global stock markets fell last week after a surprise surge in US inflation sparked fears of higher interest rates.

US stocks slipped from record highs, although a rally later in the week helped to moderate losses. The S&P 500 fell 1.4%, the Dow declined 1.1%, and the Nasdaq slid 2.3% as technology and growth stocks bore the brunt of interest rate jitters.

European indices were mixed. Germany’s Dax was largely flat, Italy’s FTSE MIB gained 0.6% and the pan-European STOXX 600 declined 0.5%. The UK’s FTSE 100 slid 1.2% as the pound rallied against the US dollar following local election victories for the Conservatives.

In Japan, where Covid-19 infection rates are accelerating, the Nikkei slumped 4.3% on news that a state of emergency will be declared in three more prefectures. In contrast, the Shanghai Composite rose 2.1% following a 6.8% surge in China’s producer price index – the largest gain since 2017.

Indian variant sparks lockdown easing fears

UK and European stock markets extended losses on Monday as the spread of a Covid-19 variant first identified in India raised concerns about the relaxation of lockdown measures.

On 17 May, lockdown restrictions were eased in England, Wales and most of Scotland, but prime minister Boris Johnson warned that “we must take this next step with a heavy dose of caution”. He said the Indian variant could make the next step of easing, due on 21 June, more difficult. The FTSE 100 ended the session down 0.2%, while Germany’s Dax slipped 0.1%.

Markets in Asia were mixed on Monday amid a raft of economic data from China. Industrial output grew by 9.8% year-on-year in April, in line with expectations, while retail sales grew by 17.7%, far worse than the 25.0% forecast. The Shanghai Composite added 0.8%, whereas Japan’s Nikkei fell by 0.9%.

Inflation fears persisted on Wall Street, sending the Nasdaq down 0.4%. The S&P 500 and the Dow shed 0.3% and 0.2%, respectively.

The FTSE 100 was up 0.5% at Tuesday’s open after data from the Office for National Statistics showed the UK unemployment rate fell again between January and March to 4.8%.

US core inflation jumps 0.9% in April

Inflation dominated the news headlines last week. The latest US consumer price index (CPI) revealed core inflation (excluding food and energy) jumped by 0.9% in April. This was the biggest monthly rise in nearly four decades and far higher than the 0.2% rise economists were expecting. The headline CPI increased by 4.2% on an annual basis, exceeding the 3.6% forecast.

On Wednesday, Federal Reserve vice chair Richard Clarida acknowledged that he was surprised by the jump in consumer prices, but said he still expects the increase to be temporary. He added that the previous week’s disappointing jobs growth report proves the ‘wisdom’ of keeping monetary policy loose.

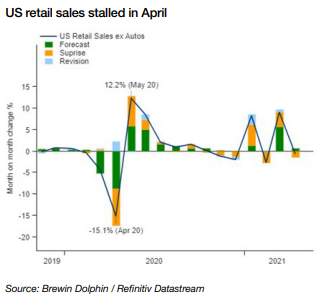

Last week also saw the release of the latest US retail sales data, which showed sales unexpectedly stalled in April as the boost from stimulus cheques faded. Economists had been expecting a rise of between 0.8% and 1.0% from the previous month. However, the increase came after a 10.7% surge in March, an upward revision from the previously reported 9.7% increase.

Economy recovering in Europe

Rising vaccination rates and the prospect of the easing of lockdown restrictions prompted the European Commission to increase its economic growth forecasts for the next two years. The euro area is expected to grow by 4.3% in 2021 and 4.4% in 2022, up from the previous forecast of 3.8% for both years. The broader EU economy is expected to grow by 4.2% in 2021 and 4.4% in 2022.

Meanwhile, the rapid roll out of the vaccine boosted UK gross domestic product (GDP) by a stronger-thanexpected 2.1% in March, the fastest monthly growth rate since August 2020. This helped to reduce the rate at which the economy contracted in the first quarter to 1.5%. However, March’s GDP was still 5.9% below the level seen in February 2020.

Chinese producer prices surge in April

Over in China, factory gate prices rose at the fastest pace in three-and-a-half years in April as raw materials prices surged. The producer price index jumped 6.8% from a year earlier, following a 4.4% increase in March. The consumer price index (CPI) rose by a less-than-expected 0.9% because of lower food prices.

Separate figures showed auto sales surged 8.6% in April from a year ago, marking the 13th consecutive month of growth, according to the China Association of Automobile Manufacturers. This means the country’s vehicle market has now fully recovered to pre-pandemic levels. In the first four months of 2021, new vehicle sales surged by almost 52%.

Weekly updates like these from Brewin Dolphin help us keep up to date with that is happening in the markets.

Please continue to check back for our latest blog posts and market updates.

Charlotte Ennis

19/05/2021