The revelation from US pharmaceutical company Moderna that its vaccine was 94.5% effective in treating coronavirus, with no significant safety concerns, sent global stock markets up between 1% and 2% on 16 November.

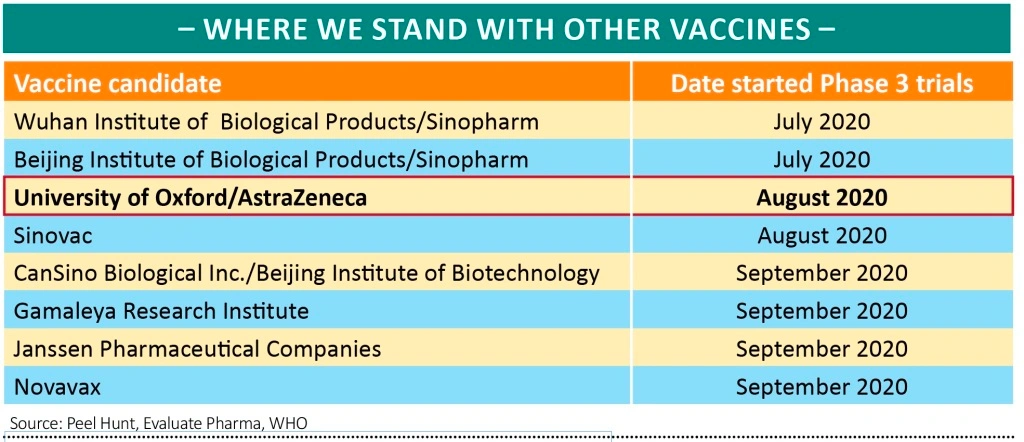

This compares with a bump of around 5% in response to the positive update from Pfizer and BioNTech a week earlier and suggests there may be diminishing returns from further vaccine news – with the table showing some of the main other candidates, several of which are centred in China.

The most meaningful will probably come from Astrazeneca (AZN) which is due to report on its vaccine, being developed together with the University of Oxford, in the next month.

According to Adam Barker, analyst at Shore Capital, AstraZeneca’s treatment ‘doesn’t have to hit a 90%+ efficacy bar to still be useful, and it remains the most stable of all the candidates at refrigerated temperatures’.

The market winners and losers were much the same on the Moderna news as the earlier vaccine catalyst, with hotels and airlines racking up large gains and previous lockdown ‘winners’ including online retailers suffering losses, albeit the moves were not as spectacular.

Moderna claimed preliminary analysis of its late-stage trials involving more than 30,000 volunteers showed the vaccine prevented the most serious cases of infection, with no severe cases at all among those who received it. ‘That for me is a game-changer’, said Moderna chief executive Stephane Bancel. Moderna shares initially soared 12% on the news.

Like the Pfizer/BioNTech vaccine, which claims to be more than 90% effective, the Moderna treatment uses mRNA technology designed to turn the body’s own cells into vaccine ‘factories’, creating copies of the virus’s ‘spike protein’ which in turn stimulates the production of antibodies. Both firms have struck significant supply deals with the US government.

While the results are preliminary and the technology has yet to be approved, both firms are expected to ask the US Food and Drug Administration for emergency-use authorisation dependant on follow-up safety data later this month.

Crucially, while the Pfizer/BioNTech vaccine has to be stored at ultra-low temperatures of -60 to -80 degrees Celsius until a few days before use, the Moderna vaccine is stable at normal refrigerator temperatures of -2 to -8 Celsius and can be kept for up to 30 days or can be frozen if needed. This gives it a significant advantage in terms of ease of distribution.

A good update from AJ Bell with some more positive vaccine news this week, this is another step in the right direction.

Please continue to check back for our latest blog posts and updates.

Please see below market update received from Brooks Macdonald this afternoon, which makes reference to ongoing Brexit negotiations and Pfizer’s upgraded vaccine efficiency rating.

What has happened

The hangover from Monday’s market exuberance continued as rising US restrictions offset positive Pfizer news. The US closed down over 1% with technology marginally outperforming in line with previous COVID centric sell-offs.

Latest on the virus

Positively, the Pfizer efficacy rate was upgraded to 95% but more importantly the efficacy rate for those older than 65 is 94%. Given the over 65s are those most at risk of serious COVID complications it is undoubtedly the most important age group to defend through a vaccine. This was not enough to distract markets from the US new case growth which continues to rise. In New York City schools will now close as the city’s positivity rate of first time COVID tests is above 3%, the threshold previously set. Colorado has urged residents to not travel around Thanksgiving and Minnesota has closed gyms, restaurants and bars. In Europe, numbers are showing signs of plateauing in some regions but France, one of the worst effected countries, looks likely to extend its lockdown due to end at the start of December. The main concern for markets is that relatively heavy restrictions (but ones that stop short of the actions in March/April) only seem to stabilise new cases rather than see them drop significantly. With winter coming this likely heralds an era of tougher restrictions interspersed with periods of loosening rather than the other way around.

EU Summit today

There was hope last week that today’s EU Leaders Summit may discuss a draft Brexit deal, but this has now been rolled into yet another week. On the agenda however will be the tough topics on the EU’s long-term budget and the recovery fund. We were reminded over the late summer that these topics weren’t exactly sorted when the vague ‘rule of law’ requirements led to a spat between some of the fiscal blocs within the EU. Indeed only this week, Hungary and Poland used their veto over conditions that would link access to budget funds to ‘adherence’ to the rule of law. Today’s meeting could therefore be a source of headlines even without a Brexit deal to deliberate.

What does Brooks Macdonald think

Whilst Brexit might not be on the agenda today, Sterling did falter overnight as the Times reported that EU leaders are asking the Commission to publish their no-deal contingency plans ahead of year end so businesses could prepare for that scenario. There is plenty of noise out there and expect some comments post today’s summit from the EU on the state of the talks but given the backlash against the hard line taken at the last meeting, expect calmer words this time.

We will provide further market analysis as the UK approaches its final week of Lockdown 2.0. Please check in again with us soon.

Please see the below content from Blackfinch Asset Management:

The role of an active manager is to make investment decisions based on analytical research, forecasts, judgement and experience with the aim of outperforming a specific benchmark or achieving a target return. This is as opposed to passive management, which involves tracking a market index.

The optimal environment in which active fund managers should thrive is when there are heightened levels of stock market volatility. Large swings in market direction create attractive investment opportunities as well as compelling exit points for profit taking. Arguably, markets have rarely been more volatile than in 2020. As a result, we’ve been extremely vigilant in assessing and monitoring the actively managed funds to which we allocate within our portfolios.

Our Approach to Active and Passive Managers

We’re whole-of-market investment managers, meaning we have the luxury of being able to make investment decisions freely, without fear of compromise. We’re unbiased in our investment selection. This extends not only across underlying fund houses, geographic regions and asset classes, but also when it comes to selecting between active and passive mandates.

We blend active and passive strategies within our portfolios, recognising the benefits that both approaches bring. When selecting an actively managed fund, we expect to clearly see value being added over and above an equivalent passively managed fund.

It’s important to establish whether a fund is delivering outperformance versus its selected benchmark. We’re also just as concerned about how it’s performing against its comparable peer group. This helps us to ensure that our investment screening process enables us to identify active managers with the ability to deliver attractive risk-adjusted returns versus other similar mandates.

Active Equity Managers

Equities are the main driver of performance in most portfolios. Our most recent assessment showed that, out of all actively managed equity funds to which we allocate, 84.6% have outperformed their respective benchmarks this calendar year. Perhaps even more comforting is that when compared to their peer groups, an impressive 92.3% of our underlying funds have outperformed their peer groups.

North America

Notably, within the North American equity sector, one of our core active equity funds has delivered a year-to-date return of 84.5%. This is some 71% ahead of the base market and equivalent passive mandate.

Asia and Emerging Markets

China, emerging markets and Japan have also been areas where our active managers displayed strong returns over equivalent passive and sector comparators. Of course, past performance should not be used as a guide for future returns. These impressive returns do mask some periods of significant volatility. However, when used at the correct weight and managed appropriately, these funds can be a fantastic component in a portfolio.

UK

On the flip side, within our UK equity allocation the margin of outperformance from active managers was far less, particularly in the large cap space. While outperformance was achieved, the difference between active managers and their passive equivalents was around just 2-3% after fees. We feel this performance differential is down to the notable challenges that the UK market has faced this year above and beyond the pandemic. For this reason, we remain comfortable in maintaining our current underweight to the region.

Ongoing Assessment and Monitoring

As ever, we’re conscious that the investment backdrop can change at a moment’s notice and we remain vigilant in our allocation to active managers. This is reflected in how we stick to our established process and also highlights the importance of regularly screening and assessing both active and passive mandates. This discipline helps us to ensure we don’t become wedded to ‘star’ managers and continually focuses attention on selecting the correct strategy depending on the particular stage of the market cycle.

As you may have seen with some of our other blog content, we regularly share updates from Blackfinch Asset Management as we believe they are a very good investment management firm. They have a good solid ESG proposition built in to their investments and as you can see in this article, they have a very good approach to investments and are varied in their methods to help deliver the right returns depending on the clients circumstances.

As Blackfinch note in the article, they are conscious that the investment backdrop can change at a moment’s notice and remain vigilant in their allocation to active managers.

We share the same view, and one of the ways we remain vigilant is by staying up to date on markets by taking in a wide range of views from across markets to help us get a handle on what’s going on.

We are also vigilant with the investments that we recommend to our clients and review these on an ongoing basis to ensure that they are doing exactly what they say they will and looking after clients assets in the right way. This is part of our ongoing research and Due Diligence.

Please keep an eye out for further updates from both us and from a range of different fund managers and investments houses.

Please see below this week’s market commentary update article from Brewin Dolphin, which was received late yesterday evening:

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below blog received from Legal & General yesterday afternoon. We have followed the markets’ reaction to both negative Covid-19 statistics and positive vaccine news. This commentary focuses on the effects of British and US politics on investments.

Cummings and goings

Last week, Downing Street’s internal soap opera spilled into the public domain. With the departure of Lee Cain and more importantly Dominic Cummings, two key advisers to Boris Johnson who were instrumental in the Vote Leave campaign, there are now questions about the future direction of policy.

In particular, there is speculation that the government may need to make significant compromises to get a Brexit deal over the line in the coming few weeks. Clearly progress has been made in some areas but, as both sides willingly admit, significant differences remain on some seemingly intractable issues such as fishing rights, the level playing field, and governance.

Another factor is the interaction between the UK and the new US President-elect. Joe Biden made clear his concerns that the (recently defeated) Internal Market Bill could undermine the Good Friday Agreement. But to what extent could this influence negotiations with the EU?

One line of reasoning is that the UK may need to compromise with the EU if it looks as though a transatlantic trade deal will be less of a priority to a Biden administration. But, regardless of the occupant of the White House, it was never likely that a deal with the US would be straightforward. It is therefore unclear whether the change in US government will have a material influence on the UK’s negotiating stance.

The market consensus is that a last-minute deal can be reached. Given the importance to our sterling-denominated long-only funds (where any unhedged foreign-asset exposure results in a short sterling position), we continue to watch developments closely.

Tick, tock tech?

The positive vaccine news last week was like a shot in the arm to much of the equity market. Not so for the tech sector, however, which has performed strongly through the lockdowns. Yet while a vaccine – hot on the heels of Biden’s election victory – may bring about some market normalisation and appear to dampen the relative attractiveness of tech in the short term, the structural trends that have been the backbone of our longstanding tech position look set to continue, in our view.

Despite the rally this year, valuation is not a large concern for us. Tech stocks do trade at a premium to the market, but the sector’s outperformance has been driven by superior earnings growth rather than any re-rating, a big difference compared with the 1990s tech bubble.

And while Biden and the Democrats may be regarded as a headwind for tech, governing with a (likely) split Congress probably means a continuation of the status quo and very little policy that could significantly move markets. There will likely be an acceleration of antitrust investigations into big tech, but so far such investigations have delivered somewhat toothless conclusions.

Biden did not show a particular passion for tech regulation either before or during the campaign, and centrist appointments to his government would signal a more market-friendly approach than some feared earlier in the year (the decision to select Kamala Harris instead of, for example, Elizabeth Warren as vice president is a prime example).

Furthermore, over the medium term the US has little incentive to over-regulate domestic companies given tech’s importance in the broader geopolitical rivalry with China.

The tech selloff early last week thus gave us an opportunity to top up our overweight in the sector, but we remain alive to the concentration risk this position carries. Within portfolios we continue to balance this risk with positions in some of the least-loved corners of the equity universe, such as European travel and leisure.

This time is different?

Back in April (which feels like a lifetime ago), we downgraded our medium-term duration view to underweight. With the post-election/vaccine selloff, we have taken the first steps to moving that view back towards neutral.

Taking the Federal Reserve’s (Fed) ‘dot plot’ at face value implies that rates will be on hold until the end of 2023. From that point forward, if we assume a similar hiking cycle to the last one (i.e. once per quarter), we get to an average Fed funds rate of 0.5% over the next five years. The last cycle was admittedly slower than previous iterations, but given the Fed’s recent switch to average inflation targeting and its repeatedly quoted ambition to wait until inflation is above target on a sustained basis before tightening policy, there is an increased chance that the central bank will again hike gradually, all else equal.

Further along the curve, the difference between 10-year and five-year yields (also around 0.5% currently) is in line with the average of the past five decades. It follows that, with the front five years of the yield curve in line with the dot plot and the slope of the next five years back to ‘normal’, a neutral view is consistent with a 10-year treasury yield of 1%, a level that it is gradually approaching.

One key risk is that the curve steepens further on ‘crowding out’ or supply concerns in the event of another big fiscal package. That has become less likely since the US election (notwithstanding the runoff for Georgia’s senate seats), although the current COVID-19 wave in the US could focus minds on Capitol Hill.

Even if we do see a stimulus package between now and the end of the first quarter of 2021, it feels as though $1 trillion is the tipping point between a positive and negative surprise on this front.

As we move into the final weeks of what has been an eventful year, we will continue to publish up to date market analysis and relevant content. Please check in again with us soon.

• UK gross domestic product (GDP) rose by 15.5% in the third quarter, the fastest increase on record. However, the pace of growth is noticeably slowing, with an expansion of just 1.1% in September, following increases of 6.3% in July and 2.2% in August.

• The National Institute of Economic and Social Research predicts that the UK economy will shrink around 2.2% in the last quarter of the year. It estimates that growth will drop to 0.3% in October, and contract by 12% in November, before rebounding in December. This is if the current lockdown ends on 2nd December as planned.

• The UK jobs market data was weaker than expected, with the unemployment rate reaching 4.8% in October

• In the third quarter redundancies reached a record high of 314,000, an increase of 181,000 on the previous quarter

• Total retail sales increased 4.9% in the four weeks to October 31st against a decline of 0.3% in the same period the previous year

• UK ministers put the finishing touches to the National Security and Investment Bill. This increases their ability to block takeovers by foreign companies on national security grounds.

US COMMENTARY

• Joe Biden’s election victory over Donald Trump was all but confirmed. However, Trump has shown no signs of conceding, so question marks remain over how smooth the transition may be.

• The Republican party retains control of the Senate, which will no doubt hamper Biden’s ability to enact all of his election promises

• Initial jobless claims fell to 703,000 last week, the lowest amount since March

EUROPE COMMENTARY

• Eurozone GDP rose 12.6% in the third quarter according to the second estimate of the quarterly economic data. There was a slight downwards revision to the initial estimate of 12.7%. On an annual basis this means that GDP fell 4.4%.

COVID-19 COMMENTARY

• The vaccine in development by Pfizer and BioNTech successfully prevented more than 90% of candidates from contracting COVID-19 in a preliminary test of 43,500 people. The companies have confirmed that they would be able to supply 50 million doses by the end of the year and around 1.3 billion in 2021. Each administered vaccine would require two doses.

Another quick update from Blackfinch, these updates are a good way of keeping up to speed with developments in the markets.

Please continue to check back for our latest blog posts and updates.

As we discussed in Part 1 of this blog: https://www.pandbifa.co.uk/where-are-we-now-part-1/ , I had the privilege of listening to a great interview held between Karen Ward of J. P. Morgan and Dr. Gertjan Vlieghe, a voting member of the Bank of England’s monetary Policy Committee. This blog covers the second half of the interview, which I have based on my notes and which hopefully does not distort the discussion. To re-iterate, the following is based on my interpretation and I believe I have been faithful to the key content and questions and answers discussed.

Karen raised the topic, ‘About negative interest rates and stimulating growth?’

Gertjan responded, ‘Macro Economists think about ‘real interest rates’. These have been around for a while. It’s (about) nominal interest rates at 0% or below. If you lower interest rates further, banks will start to lose money, lose deposits and therefore can’t lend.’

‘In reality, (in Europe) there has been no large-scale withdrawal of deposits. People/corporates are willing to pay to keep deposits in the banks. Is the UK fundamentally different? Probably not. So, it (negative interest rates) could achieve further stimulus to the economy.’

Gertjan continued, ‘My reading and very extensive studying found that it did not impede lending and it did not reduce bank profitability. It worked as intended. The risk of unwinding macro stimulus is low’, (in Gertjan’s opinion).

Karen then asked, ‘But has it worked?’ (in Japan and Europe)

Gertjan responded, ‘The question is, if negative interest rates were never used, would it be even worse? Actually, it would have been.’

Karen went on to enquire, ‘How will this interest rate persist? How will it reverse?’

Gertjan answered, ‘I am a believer in the ‘low for long’ story and the importance of demographics. We have seen a big increase in longevity without a commensurate increase in the retirement age. Reduced capital amounts for businesses and increased need for savings generates a world where the equilibrium for interest rates is very low. Look at what is happening in Japan – look how their interest rates are.’

Gertjan further discussed the global ageing demographics, except for the Middle East and Africa, who are much younger. He added ‘The one way to adjust this is to increase the pension age.’ He did not clarify whether he was referring to the State Pension age or the minimum pension age – probably both!

Karen then went on to ask, ‘What are the Bank’s specific forecasts for inflation?’

Gertjan replied, ‘Now at 0.5% for the next two quarters, then it will rise and be roughly at target in 2 years and slightly above in 3 years.’

Karen continued, ‘Is there a risk post-vaccine of seeing a bottleneck-demand pushing up against supply?’

Gertjan responded, ‘If inflation is rising because the economy is roaring back, we will take action. The Covid shock is dominant on demand but there is some element of supply shock. We are looking for a sustained inflation affect.’

Karen moved on and asked, ‘Climate change – who’s responsibility is it?’

Gertjan replied, ‘It is not for the Bank of England to decide how green the economy should be – it is political. We (the Bank of England) have a mandate for financial stability. If you look long-term, certain assets could potentially lose a lot of value. Fund Managers should take this risk seriously, so you don’t start losing money. We (the Bank of England) want to lead by example – everybody should do this kind of reporting.’ I believe he was referring to environmental-based reporting.

One of Karen’s final questions on the matter was, ‘Should we review our framework and targets?’

Gertjan answered, ‘The Government sets us an inflation target of 2% CPI. It’s OK for us to periodically review our toolkit.’

Summary

The whole interview was just over an hour long but was well worth listening to. I understand that Gertjan is only one voting member of the Bank of England’s MPC, but if they all have his level of understanding and grasp on the issues and potential solutions, then I think we are in good hands.

The Bank of England’s independence and the range of tools available to them will help the Government with their drive to get the UK economy fully recovered as soon as possible.

We still have our headwinds, but distribution of vaccines will considerably aid our recovery here in the UK and globally.

Blackfinch Comments on The Government’s New Climate Governance Objectives:

It has been quite a week in financial markets with the announcement of a potential vaccine for COVID-19. In a joint effort by Pfizer and BioNTech, the promising vaccine candidate is stated to have an initial success rate of 90%. The announcement was met with a wave of relief across markets. Cyclical sectors, being most closely tied to economic change, began to outperform those that have benefited greatly from stay-at-home policies.

Positive Developments on Climate Governance

While the vaccine candidate took the spotlight, there were some positive developments from the UK Government regarding its commitments to green finance and sustainability goals. Spearheaded by the Chancellor, Rishi Sunak, the UK has set out to “bolster the dynamism, openness and competitiveness” of the financial services sector.

The focus is on ensuring that the sector can continue helping to combat the effects of climate change. This can include reducing carbon emissions in the face of global warming, and increasing investment in renewables, for a greener economy and world.

In seeking to achieve these objectives, the UK Government will issue the first ever Sovereign Green Bond in 2021. It will also become the first country in the world to make the recommendations of the global Task Force on Climate-Related Financial Disclosures (TCFD) an official requirement.

TCFD-aligned disclosures will be mandatory for UK businesses including those within financial services. Companies will be required to disclose their climate-related risks on a regular and transparent basis.

The Chancellor also added further comment around ensuring that the UK will continue to pioneer new technologies and shift sector activity towards a future of net zero carbon dioxide emissions.

Helping to Meet Targets Through Investing

Blackfinch’s investment goals are fully aligned with these new proposals and objectives from the UK Government. We’re a signatory to the Principles for Responsible Investment. This reflects our commitment to environmental, social and governance (ESG) principles, with these central to our investment processes. We recognise that financial services plays an important role in the drive for net zero emissions.

The issuance of a Sovereign Green Bond will help the UK to meet its 2050 net zero target and other environmental objectives. The money raised from the bond can help to finance projects to tackle climate change and to invest in related infrastructure such as buildings, roads and power supplies.

There’s a great opportunity for Blackfinch to support this target via the portfolios offered by Blackfinch Asset Management. We seek to allocate funds to this exciting and growing sector of the sovereign bond markets.

Meanwhile, at Blackfinch Energy, our investment focus is on real assets such as wind and solar farms. Similarly, at Blackfinch Property, we invest across sectors, including in eco-living developments. These are all sectors the Government is actively targeting in its push to address climate change and invest in the UK’s infrastructure. We will continue investing in these areas in pursuit of these common goals.

A New Era for Climate Governance Reporting

The TCFD was created to improve and increase reporting of climate-related financial information. The commitment from the UK Government to make disclosures mandatory is an important development. The standards set by the TCFD can allow investors and businesses to better understand the material financial impacts of a firm’s exposure to climate change. This is something we wholeheartedly support.

There’s still work to be done as the mandatory disclosure for firms doesn’t come into effect until 2025. Nevertheless, it’s a key step forward and UK businesses, including those in financial services, can look to adopt it. For us, any such requirement would become an integral part of our ESG process.

In a further show of commitment by the Government, it also outlined a new related system of classification. Once implemented, this can provide a framework for determining which of a firm’s activities can be defined as environmentally sustainable. Again, the aim is to improve understanding of the impacts that firms and their activities and investments have on the environment. This is as the UK transitions to a sustainable economy.

These developments towards sustainable finance and greater disclosures will help to ensure that the UK is a global leader in working towards a sustainable future. We fully support the Government’s objectives and look forward to investing in opportunities arising from these initiatives.

This is good input from Blackfinch. As we wrote over the summer in one of our ESG blogs, Blackfinch have a very good ESG proposition within their investments and this is something we recommend to our clients.

They are ahead of the game in terms of ESG as we have been reporting on, we expect the rest of the industry to continue movement towards good ESG propositions.

Keep an eye out for further content on ESG from fund managers such as Blackfinch and our own original content.

I had the privilege of listening to a webinar on Wednesday afternoon, which was hosted by Karen Ward from J. P. Morgan and also featured Dr. Gertjan Vlieghe. Karen is JPM’s Chief Market Strategist for EMEA (Europe, Middle East and Africa) and Dr. Gertjan Vlieghe is a voting member of the Bank of England’s MPC (Monetary Policy Committee).

The interview covered a wide range of important topics and I took notes in order to interpret the speakers’ key points. Please note: Gertjan did point out that the opinions expressed where his views and not necessarily those of the Bank of England’s MPC.

Karen on the topic of the Pfizer vaccine:

‘A 90% efficacy rate is a ‘Game Changer.’ The timing is excellent (of the vaccine against the current backdrop of a high second wave of the virus). How quickly will we get to that important point of herd immunity?’

Karen went on to ask Gertjan, ‘If the vaccine is distributed, could we be looking at a very strong bounce back in the second half of 2021?’

Gertjan replied, ‘Only if the vaccine works. In a way, the vaccine is already in the forecast. That is precisely what our central forecast is.’

Karen then asked, ‘What will you be tracking to assess the degree of long-term scarring?’

Gertjan’s response was ‘Unemployment dynamics – it’s difficult to all get back into a job. There is still some slack in the economy and levels of unemployment will not come back down for a long time. We will need stimulus.’

In relation to Brexit, Karen asked, ‘How is it going and what are the changes that will affect Q1 2021 and the longer term?’

Gertjan responded, ‘This is a longer-term issue. There is a trade-off between sovereignty and smooth and open trade. It will have a purely economic consequence. We will have less trade, less competition and less technological diffusion. This is very important for the country, but not for monetary policy. It has also dampened investment (in UK businesses). To what extent are UK firms ready? How much disruption will there be in the short term? How will financial markets react? This will impact on monetary policy; it’s about how smoothly we transition.’

Karen on Central Banks, ‘Have Central Banks been monetarily financing governments?’

Gertjan replied, ‘On ‘Co-ordinated action’, I’m not entirely happy with it.’ Fiscal policy is doing the heavy lifting and monetary policy is helping.

He continued to remark on QE (Quantitative Easing), ‘We expand reserves beyond what banks really need. The macro-economic impact is very small and expansion in reserves does not lead to a proportionate response in lending. In 2008/2009, re QE, we had no high inflation. If inflation does come back, we know what to do; there is no constraint.’

Karen’s next question was, ‘Could a government less focused on austerity contribute to a higher velocity of money?’

Gertjan responded, ‘Completely, absolutely. Timing is crucial in relation to the government flipping back into debt reduction mode.’

Karen then asked, ‘What can the Bank of England do to support the economy?’

Gertjan replied, ‘The impact of QE on the economy is state-contingent. When market functioning is impaired, QE can have a big impact. Expectations of future real interest rates are really very low. The stimulus power (of QE) now is very low. With regards to technical constraints, it’s important to understand that they are self-imposed – we can change the rules.’

Comment

This update is based on my interpretation and notes from the first half of the webinar’s discussion and I have tried to stay faithful to the content.

From my point of view, I was happy with the Dr.’s input as he obviously understood everything in detail and had no problem with any of the questions put to him by Karen. He also gave me confidence (based on his views), that these people on the Bank of England MPC really do know what they are doing and are a great aid to the recovery of our economy in the UK.

Summary

Over the next few days, I will work on a precis for Part 2 of the webinar for you, which starts with a discussion on negative interest rates.

If you have any topics that you think we should cover on markets, advice or planning issues, please let me know.

Please see the below updates from AJ Bell regarding this week’s news on the Pfizer vaccine:

Is the vaccine news a game-changer or just a good start?

There are high expectations for Pfizer and BioNTech to win with their Covid-19 vaccine following the latest trial update which triggered a global stock market rally and installed hope in people around the world.

The two companies will collate data until the third week of November before submitting to the regulators for approval. Safety is very important given the scale of deployment with potentially billions of perfectly healthy people being given the vaccine.

Assuming more data confirms the 90% effectiveness of the vaccine there are other considerations as more news arrives over the coming weeks.

The first big question is for how long the vaccine will provide immunity because there is no guarantee that vaccine-induced immunity will be any better than that afforded by infection.

Second, the science behind this vaccine is known as mRNA and it has never been commercialised which means no one knows for sure how to manufacture it at scale. The technology involves injecting a blueprint of the vaccine into the cells of the body so that they can make copies of the vaccine.

The vaccine needs a cold storage supply-chain because it has to be stored at minus 80 degrees centigrade. The lack of available cold refrigeration infrastructure, especially in poorer areas of the globe, may hinder distribution of the vaccine.

According to Shore Capital it is unclear at this point whether the study included patients with severe symptoms which is very important because if it didn’t it would mean the vaccine can so far only make mild cases more mild and not prevent hospitalisations.

Pfizer has targeted production of around 50 million doses for 2020 and 1.3 billion next year. Various countries have already secured agreements with Pfizer including the UK with 30 million doses. Shore Capital points out that because two doses are required and assuming wastage this would only cover around 12 million patients. It takes 28 days from the first injection to attain immunity.

The broker notes that the world will need more than one vaccine because a range of sub-groups are likely to respond differently to vaccines. Mark Brewer, analyst at FinnCap, argues that global herd immunity requires 60% to 70% of the population to become immune which given the huge numbers involved could take years to achieve.

In short, don’t expect the economy to open up quickly even if a vaccine is approved.

Two late-stage trials with results expected in the next few weeks are University of Oxford’s and AstraZeneca’s (AZN) study of compound AZD1222 and Moderna’s vaccine candidate mRNA-1273.

Both these studies include patients with severe Covid-19 symptoms and so a positive result may be more meaningful in terms of reducing hospitalisations.

Where we stand after markets’ vaccine boost

he near-5% gain for the FTSE 100 on 9 November reflected news of extremely positive results for the vaccine being developed by Pfizer and BioNTech.

This was the biggest gain since the index surged 9.1% on 24 March when investors reacted to a rescue mission by central banks during the wild trading seen at the outset of the global pandemic. Even this, more modest, November movement ranks among the 10 highest one-day percentage gains for the index.

In the spring there was considerable uncertainty on the path out of the coronavirus crisis and just how damaging it might be. Now the situation on both these variables is a little clearer and that helps explain why market rallied so strongly. Although it is not quite true to say the market has come full circle.

Has the ftse fully recovered?

As we write the FTSE 100 is still 15% below its pre-Covid levels – we take 20 February as being when investors really began to price in a material impact from the pandemic.

In contrast, the S&P 500 which, thanks to a combination of the US presidential outcome and the vaccine news, broke new record highs this week.

The gains across the Atlantic were less substantial than those enjoyed by the FTSE 100 and that hints at the changes in stock market leadership we are seeing in the wake of Pfizer’s big announcement.

Losers become winners and vice versa

While Wall Street is dominated by the big technology companies, the UK market has plenty of the old-world economy in its ranks, many of which have seen their valuations smashed on the rocks of the Covid crisis.

These beaten down ‘value’ stocks were suddenly in fashion and we saw some quite spectacular moves, while tech, which sits very much in the ‘growth’ category, and traditional safe havens like government bonds and gold were sold off.

Tech has been one of the few places to find earnings growth in 2020 and so investors have been happy to pay high prices in this area. Many investors now look to be taking the view that some of the worst-performing stocks this year now have a greater chance of earnings recovery, which means they can find growth at a cheaper price and so tech becomes less appealing as valuations start to become more important.

Travel Rebound

Drilling down to specific sectors, travel was clearly a big winner including British Airways owner International Airlines Group (IAG) which enjoyed intra-day gains of 40%.

Aircraft engine maker Rolls-Royce (RR.) continued the dizzying ascent it has enjoyed since addressing its own financial problems with a recent £2 billion rights issue. Hotels, as well as leisure and hospitality businesses, also soared on hopes they might be able to return to more normal levels of business in the not too distant future.

However, as the graphic shows many stocks remain some way below the levels they were trading at before the pandemic erupted, demonstrating just how far they have fallen in 2020.

Other Sectors Rising

Oil majors BP (BP.) and Royal Dutch Shell (RDSB) were also in demand as oil prices spiked, though again both their share prices and the Brent crude benchmark remain way below pre-Covid levels.

Housebuilders were fired by hopes of an improved economic picture as well as surprisingly punchy guidance from Taylor Wimpey (TW.) that 2021 would be materially ahead of expectations – confidence underpinned by an order book up from £2.7 billion a year earlier to £3 billion. Real estate investment companies, particularly those with exposure to shops and offices, also soared.

Left Behind In The Rally

Perceived lockdown winners like Just Eat Takeaway (JET) and DIY-firm Kingfisher (KGF) were losers on the day. The biggest faller in the FTSE 100 was online groceries firm Ocado (OCDO) which fell 16.1% to £22.83.

Consumer goods giant Reckitt Benckiser (RB.), which had done well earlier this year after receiving a boost from demand for health and hygiene products, also gave up some of its recent gains.

What Happens Next?

Let’s assume the most bullish assumptions are true and there will be a return to some normality by the spring. With very loose monetary policy in play and a possible spending splurge by those consumers which still enjoy a disposable income, there is the possibility of inflation increasing fairly rapidly.

This might see central banks execute a handbrake turn as they look to gain control of rising prices and begin withdrawing stimulus or even increasing ultra-low rates. In this article we talk about the investments which could do well if inflation returns.

Conversely, if there are unexpected delays in the development and distribution of the Pfizer vaccine and others potential vaccines, will investors be patient, or will they look to sell Covid-impaired names once more?

One must also consider the unresolved risks which persist around Brexit and the transfer of power in the US.

This week’s vaccine news is positive news, however it’s by no means the end of the road, its just a step in the right direction.

We may see further drops in the market and setbacks in terms of the Pandemic, but this is a very good start.

Stay posted for further market updates and blog content from us.

{kind=link}