Please see below commentary received from Fidelity International yesterday afternoon, which discusses how the US election result will likely impact the US economy as well as global trade. The article suggests that there may not be substantive changes in these areas and explains why.

As the dust settles on the US elections, a couple of uncertainties remain. Control of the Senate will not be resolved until runoffs are conducted in January 2021, to name one example. But investors weighing how much has changed should also consider the broader trends that remain in place. When it comes to key elements around geopolitics and economic strategy, will it be much more a case of style over substance?

Focus on the US

First, against a backdrop of a rolling pandemic crisis, both the near-term response and the medium-term consequences will mean an inevitable focus on the domestic economy. This implies an ongoing use of both fiscal and monetary policy to support the demand side of the economy, and additional investment in infrastructure to stimulate economic activity. The possibility of a split Congress means that higher-end estimates for fiscal stimulus, such as those anticipated under ‘blue wave’ scenarios of Democratic control of both houses, will probably fail to materialise. Once again, the Fed will be expected to carry more of the weight. Still, as we go through the coming quarters, the imperative for the White House and Congress will be to iron out the particular targets of spending (albeit at the lower end of the range of estimates), with areas such as infrastructure or healthcare likely to be beneficiaries.

Geopolitics unmoved?

Second, again discounting the issue of partisan approach, it is hard to see a meaningful near-term change in the geopolitical landscape, with key areas such as US-China relations potentially remaining fragile if we look at rhetoric from all sides of the US political spectrum over the course of this year. In many ways the narrative of competitive threat and security risk will just act to reinforce a need for investment closer to home. And while recent months have highlighted that global trade flows continue despite tariffs and other bilateral barriers, these flows are also likely to grow more regional over time as shorter supply chains become a priority in the wake of Covid.

The view from Asia

Third, I expect the direction of US economic strategy outlined above will continue to act as a drag on the US dollar in relative terms. Despite what is likely to be a more limited scale in a split Congress scenario, US stimulus measures and their impact on currency markets should, at the margin, ease conditions for Asia and developing markets globally. This, combined with a greater success in containing the spread of Covid-19 across large parts of Asia, will see a scope for not only a broader-based recovery in the region, but for Asia to increasingly decouple from what is being experienced elsewhere in the world.

Market implications

Turning to markets and how investors should be positioned as we head into 2021, clearly the points above speak to the attraction of non-dollar denominated assets. With the prospect of increased volatility, this suggests a good risk-reward balance in Asian fixed income markets, and in particular Chinese government bonds and Asian high yield bonds. On the equity side, we see value in markets such as India and across South East Asia, which have lagged much of the rest of the region over the course of 2020, and also for Japan, given the ongoing focus on corporate reform combined with attractive valuations. As the dust settles on the 2020 US elections, these are some of the broad global trends to watch.

We will continue to provide market analysis and relevant content from the world’s leading investment experts, so please check in again with us soon.

Please see below the latest bulletin received from Brooks MacDonald this afternoon, which provides a refreshing update on the continuous rise in the markets following the US election result and the Pfizer vaccine news.

What has happened

The news from Pfizer/BioNTech catalysed a broad market rally across Europe although the momentum did fade at the latter end of the US session and coming into Asian markets. The rally had a decidedly cyclical skew with the unloved hospitality and leisure sectors seeing a sizeable boost.

The Pfizer vaccine

Given the squeezed timescales for a coronavirus vaccine, there were always many fears about the chances of a successful vaccine. One of the key determinants of ‘success’ is efficacy, and the Pfizer candidate is reporting over 90% which, for comparison, is hugely above that of the average flu vaccine which is around 50%. Politicians globally welcomed the news but advised caution that this would provide a quick win given the need to ramp up production and raised concerns around logistics given the vaccine needs to be deep frozen until the day of use. It is too early to say whether this vaccine news is a genuine game changer, but it is a salient reminder of how aggressively the under owned value and cyclical areas can snap back. Whilst the post pandemic world is likely to continue to be dominated by low growth, low inflation and low interest rates, favouring growth sectors, some balance is required given how cheap the cyclical/value areas of the market are.

Internal Market Bill falters

The House of Lords voted to remove the clauses from the internal market bill that would allow ministers to disallow elements of the EU withdrawal agreement. Despite this the government said it would progress with the provisions and add them back to the bill when it returns to Commons debate in December. The House of Lords defeat puts more pressure on PM Johnson as EU/UK trade talks reach their conclusions and President-Elect Biden’s victory swings the balance of power towards a multilateral approach to negotiation. Biden has previously warned that any destabilisation of the Northern Ireland peace process would make a US/UK trade deal very unlikely.

What does Brooks Macdonald think

Whilst a Biden win is not a surprise for markets, many of the existing risks and opportunities in the world need to be revisited with a fresh lens. Brexit is a particularly interesting case as the EU may feel emboldened by the prospect of closer US relations, possibly encouraging a more aggressive position with the UK. This risks an impasse with the UK at exactly the time when Sterling will need clarity over the state of EU/UK talks.

Index

1 Day

1 Week

1 Month

YTD

TR

TR

TR

TR

MSCI AC World GBP

1.4%

5.7%

1.8%

8.8%

MSCI UK All Cap GBP

5.2%

9.8%

3.4%

-16.2%

MSCI USA GBP

0.9%

5.3%

1.0%

13.9%

MSCI EMU GBP

4.9%

11.0%

2.6%

-0.3%

MSCI AC Asia ex Japan GBP

0.9%

3.8%

4.8%

16.7%

MSCI Japan GBP

-0.4%

2.3%

1.9%

4.4%

MSCI Emerging Markets GBP

1.5%

5.1%

5.3%

10.0%

MSCI AC World IT GBP

-0.6%

6.4%

-0.7%

32.5%

MSCI AC World Healthcare GBP

0.3%

5.2%

0.4%

12.0%

Barclays Sterling Gilts GBP

-1.3%

-2.2%

-1.5%

5.7%

Barclays Sterling Corps GBP

-0.4%

-0.3%

0.1%

4.9%

WTI Oil GBP

8.6%

7.5%

-1.7%

-33.4%

Dollar per Sterling

0.1%

1.9%

1.0%

-0.7%

Euro per Sterling

0.7%

0.4%

1.1%

-5.7%

MSCI PIMFA Income

1.7%

4.3%

1.4%

-1.6%

MSCI PIMFA Balanced

1.9%

4.9%

1.6%

-1.6%

MSCI PIMFA Growth

2.3%

6.0%

1.9%

-1.6%

Although this appears to be the light at the end of the tunnel, we are likely to see more volatility as the markets recover. Please check in again with us soon for further market data and news.

Please see below the latest bulletin from Brooks Macdonald, which has just been received and provides their weekly market commentary:

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below this week’s Monday Market Update from Blackfinch investments – received today 09/11/2020.

Blackfinch Group Monday Market Update – Issue 16 – 9th November 2020

UK COMMENTARY

• Boris Johnson placed England in a second national lockdown. Although the rules are not quite as strict as the first time round, the public is under specific guidance on movement until 2nd December at least.

• The UK Manufacturing Purchasing Managers’ Index (PMI) for October was revised up to 53.7 from the flash estimate of 53.3. This was below September’s level, with the main drag attributed to a contraction in the consumer goods industry, blamed in part on regional lockdowns.

• The IHS Markit/CIPS UK Services PMI Business Activity Index was reported as 51.4 in October, down from 56.1 in September. However, a value above 50 still indicates an increase in activity.

• The Office for National Statistics reported that the UK’s headline measure of labour productivity fell by 1.8% year on year in the second quarter

• The Bank of England voted unanimously to implement a £150bn bond-buying exercise, ahead of market expectations for a repeat of the current £100bn. The gilt purchases will begin in January when the existing programme expires and will last throughout 2021.

US COMMENTARY

• All focus was on the presidential election. Donald Trump fared better than anticipated in the polls, but by close of business on Friday it appeared Joe Biden had the lead. Over the weekend he was confirmed as victor. Whether the current President will concede the election is another matter entirely.

• The Senate appears likely to remain Republican, creating a divided government in the US. This also continues the trend seen so regularly in the past ten years, including in the second half of President Trump’s term.

• Initial jobless claims fell to 751,000, however economists had predicted a figure of 735,000

• The total unemployment rate fell to 6.9% from 7.9%

ASIA COMMENTARY

• The Caixin/Markit PMI came in at 53.6 for October, marking the sixth straight month of manufacturing expansion in China

• Japan’s benchmark equity index, the Nikkei, reached a near thirty-year high at the close of business on Friday

A good update from Blackfinch Investments, providing a short summary of events from around the world over the past week.

Please continue to check back for our latest blog posts and updates.

Please see below article received from T. Rowe Price this morning following the US election results. The commentary includes predictions on Biden’s priorities and policy proposals and the effects of this on the global markets.

Democrat Joe Biden’s policy proposals as the next US president (pending the outcome of potential legal challenges) could have mixed implications for investors if implemented, according to T. Rowe Price investment professionals. On the positive side, many see Biden as likely to prioritize additional major fiscal stimulus to help the economy continue to recover from the steep downturn caused by the coronavirus pandemic. However, Biden also supports corporate tax increases that would be used to fund some of the additional spending. It is far from certain that they would be enacted given Republican opposition.

Spending and Taxes

Mark Vaselkiv, T. Rowe Price’s chief investment officer (CIO) for Fixed Income, believes that Biden is likely to seek additional funding for states and municipalities. “The economy is weakest at the state and local level, where governments need help to mitigate cuts in essential services amid quickly declining revenues,” Vaselkiv asserts. This push for funds for localities could help stabilize and support the credit quality of municipal debt for years to come as the economy recovers from the pandemic, he says.

Biden has proposed raising corporate taxes to halve the tax cut enacted by the Tax Cuts and Jobs Act (TCJA) of 2017. Biden’s plan involves increasing the corporate income tax rate—currently a flat 21%—to 28%. That would still leave the rate meaningfully lower than the pre‑TCJA rate of 35%. President‑elect Biden would also likely try to boost taxes on the foreign income of US companies and institute a form of alternative minimum tax for corporations. However, Republican opposition could limit or prevent some of these measures to increase taxes.

Short-Term Effect on Corporate Earnings

Biden’s outlined tax hikes, if implemented, could reduce after‑tax corporate earnings. David Giroux, T. Rowe Price CIO of Equity and Multi‑Asset and head of Investment Strategy, says that the tax rate increases proposed by Biden could collectively reduce after‑tax profits for companies in the S&P 500 Index. However, some industries could benefit from increased spending. Global Focused Growth Equity Strategy Portfolio Manager David Eiswert agrees that US companies would experience an “earnings reset” if the Biden tax plan passes, although he also believes that the effects would be “manageable and likely offset, in part, by fiscal stimulus.”

Looking at corporate bonds, Vaselkiv asserts that “Biden’s tax increases would impact equities more directly than corporate credit, probably hitting the wildly profitable giant tech stocks the hardest.” A tax hike would not necessarily hold back growth, Vaselkiv adds, noting that US corporate earnings and the broader US economy both continued to grow after tax hikes during the Clinton and Obama administrations.

According to T. Rowe Price Chief US Economist Alan Levenson, the first order of fiscal business for Biden will likely be a debt‑financed coronavirus response and economic rescue package. Biden will probably wait until later in 2021 to try to implement his broader vision for economic renewal, with roughly half of the 10‑year cost expected to be offset by tax and other revenue increases. “The implied addition to debt is manageable because borrowing rates are low relative to the economy’s potential growth,” he explains.

Tensions with China seem to resonate across the political divide.

– Quentin Fitzsimmons, International Fixed Income Portfolio Manager

Pressure on China to Continue

All signs suggest that, as president, Biden will take a tough stance toward China on market practices and human rights issues, though he will likely seek multilateral partnerships and engage levers beyond trade in any renegotiation of the US‑China relationship.

“Tensions with China seem to resonate across the political divide,” says Quentin Fitzsimmons, a London‑based T. Rowe Price International Fixed Income portfolio manager. He believes Biden will maintain pressure on China to address concerns about intellectual property rights in the technology sector. “It’s tough to say how US‑China relations will evolve in a Biden presidency,” Science & Technology Equity Strategy Portfolio Manager Ken Allen states, “but if volatility were to lessen, that could be a positive for technology companies that are perceived as having some exposure to trade tensions between the two countries.”

However, according to Levenson, Biden may face tensions between reengaging more constructively with allies on trade while seeking to re‑shore critical supply lines and manufacturing jobs in general.

Industrials Could Benefit from Push Toward Energy Efficiency

Biden has indicated that he will seek higher levels of federal procurement spending and tax incentives to create jobs and drive economic development by rebuilding critical infrastructure. This push would focus on reducing carbon emissions and investing in clean‑energy technologies, although it could face opposition from Republicans in Congress.

Jason Adams, portfolio manager of the Global Industrials Equity Strategy, believes that, if implemented, Biden’s ambitious plans could accelerate advances in energy efficiency and emissions reductions. “Many industrial companies are part of the solution in this regard,” he says. Potential beneficiaries, he adds, could include companies specializing in air compressors, rail transport, commercial aircraft, electric vehicles, and industrial gases.

Conversely, US defense spending “faces the prospect of several years of a modest downward trajectory after a seven‑year upcycle, which would have been likely regardless of who was elected as the next president,” Adams asserts.

We don’t think there’s anything Biden will do that would change our view that…oil will remain in a long‑term bear market….

– Shawn Driscoll, Global Natural Resources Equity Strategy Portfolio Manager

Health Care Policies May Expand Market for Medicare-Focused Firms

Expanding access to health insurance also appears to be a priority for Biden, who has proposed lowering the age requirement for Medicare eligibility to 60 years from 65 and creating a new Medicare‑administered public option that would automatically enroll low‑income Americans who aren’t eligible for Medicaid. Health Services Analyst Rouven Wool‑Lewis believes that, if implemented, these policies could expand the market for Medicare‑focused managed care organizations while potentially siphoning away some customers from private health insurance providers.

President‑elect Biden and President Trump advocated different solutions to curb drug costs. Pharmaceuticals Analyst Jeff Holford says such proposals are more likely to be enacted in the Biden administration, which could negatively impact pharmaceutical stocks. Holford also notes, however, that the politics of health care legislation are complicated given the strong relationships that politicians across the political divide have with the pharmaceutical industry.

Potential for Heightened Bank Regulation

The Biden administration might seek to impose stricter rules and enforcement policies for banks. These potential measures could include additional limits on bank dividends and share buybacks as the U.S. recovers from the pandemic and its fallout. However, Gabriel Solomon, portfolio manager of the Financial Services Equity Strategy, believes that the regulatory environment may prove “less adversarial” than during the Obama administration, after lax bank regulation was widely viewed as contributing to the global financial crisis of 2008–2009.

Regulatory Moves Likely to Have Little Impact on Oil Market

Biden’s platform, as well as his comments on the campaign trail, suggests that he will try to tighten regulation of the fossil fuels industry, which would likely result in higher compliance costs for oil and gas companies. Biden has also voiced support for a moratorium on new oil and gas lease sales on federal lands and potentially halting the issuance of new drilling permits in these areas.

Shawn Driscoll, portfolio manager of the Global Natural Resources Equity Strategy, contends that conditions in the global oil market, not the regulatory implications of Biden’s election, are likely to have more influence on energy company earnings. “We don’t think there’s anything Biden will do that would change our view that, outside of the occasional countercyclical rally, oil will remain in a long‑term bear market because of rising productivity and falling output costs.”

Once Biden has been inaugurated, he will be faced with an ongoing pandemic, a struggling economy, and a divided country. It will be interesting to see how he tackles these challenges during his first few months in Office. Please check in again with us soon for further up to date content.

Democrats have taken control of the Presidency under Joe Biden but control of the Senate is still in question. Managers from BNY Mellon Investment Management outline how they expect the result to impact markets and sectors over the coming months should results hold

Joe Biden has won the US presidential election, but it is still unclear if Republicans have retained control of the Senate. The latter could hinder implementation of the Democratic Party’s future policy program.

It was against the backdrop of a global pandemic that an often bitter election campaign played out: now, the question for investors is how different asset classes are likely to respond and what political power a Biden White House can realistically assert if Congress remains split.

Regardless of a favorable outcome for Biden’s team, the prospects of a Democratic-sponsored hike in corporate taxes, a focus on a ‘green’ agenda and the potential for increased cooperation in the international sphere could possibly face Republican opposition.

Despite Biden’s win – and beyond party politics – Newton Investment Management global equity portfolio manager Paul Markham believes it could be a tough challenge for his party to satisfy its political base for new social policies, given the US’s poor governmental financial position – on account of its efforts to tackle the Covid-19 pandemic.

“Higher taxation or further increases in government spending could cause headaches for the Democrats – the forthcoming four years will be very difficult– and what has been pledged by the party in terms of social and health care may prove hugely challenging to actually deliver. Democratic pledges on social and healthcare changes could be especially difficult to deliver, given the currently challenging government financial predicament,” he says.

April LaRusse, Insight Investment’s head of investment specialists, believes key government policies are likely to remain unchanged under Biden, though she adds that the Presidential change and a wider mood shift could benefit risk markets.

“In our view, if the Senate does remain in Republican control, this outcome could mean key policies like corporate taxes will be unchanged. That said, we would expect to see government bond yields move somewhat higher and risk assets rally, though not to the extent seen in 2016 given existing Fed policy. While an infrastructure deal might be less likely, so is further trade escalation, and so we may see trade-exposed names benefit from that.”

In contrast, Alcentra co-chief investment officer Leland Hart is more concerned by the election outcome, in light of the potential market uncertainty it could generate.

“We view the latest election outcome as a fairly negative result given the political uncertainty that may ensue. Ultimately, it means we could soon start to lose clarity on whether there will be decisive action by government and continued strong support for the economy,” he says.

Hart says decisions on where and how support to sectors of the economy is delivered could become more complex and subject to political division between Republicans and Democrats. “In the recent past both sides have tended to politicize decision marking, often with a negative impact on markets, including private credit markets.”

Newton Investment Management global strategist and member of the Real Return Team, Brendan Mulhern supports the view that potential bi-partisan conflict risks slowing economic progress and could dent market confidence.

“The lack of action a split House and Senate might bring about has been on display this year with the Republicans and Democrats unable to agree on another fiscal package to support the economy. It’s difficult to say how much of this is down to the two parties playing politics ahead of the election but if the House and Senate is still split there may be concerns that policymakers in Washington will not be able to act decisively to counter the impact of the Covid-19 pandemic on the economy. This may come to weigh on market sentiment and expectations,” he says.

John Bailer, lead portfolio manager of US dividend-oriented and large cap strategies at Mellon, also feels the Biden administration could adopt a moderate approach. On a more optimistic note he adds that, ahead of the election, the market was pricing in a Democratic sweep, so some sectors – such as financials, energy and defense which performed poorly before the election – might now rally.

He adds: “The most meaningful change would happen with executive orders and appointees to Government agencies.”

“I would expect more international cooperation, therefore helping companies hurt by the trade wars. Mergers & acquisitions could slow with a more consumer focused Department of Justice. Since 1933, a divided government with a Democratic President has led to 13.60% returns in the S&P 500, which has been better than average.”

Newton head of fixed income Paul Brain is also optimistic government spending could continue to support the US economy and hopes international trade relations might also thaw under Biden. Separately, he also expects to see a rise in US Treasury yields following the latest election.

“We would expect to see a new stimulus package put in place and global trade relationships improve a little, even if some US trade pressure remains on China. The US dollar could bounce back now that election uncertainty has been removed, but the trend is still likely to be lower against Asia in particular.

“In bond markets, we would expect yields in the US Treasury market to rise faced with the prospect of more government spending, with the curve steepening. Investors in risk assets such as credit may be concerned about the potential for increased corporate taxes later, though initially, government spending plans look set to dominate and improve the outlook. We would expect the US dollar to weaken over time as domestic spending increases and sucks in imports and emerging markets outperform.”

For Jeff Burger, senior portfolio manager, Mellon, one asset class that may benefit is municipal bonds. “Under a Biden Presidency infrastructure spend may actually pick up – funded largely by the sale of municipal bonds. Here, we believe there could be an emphasis on ‘green’ and environmentally sensitive projects as a way of providing economic stimulus,” he says.

Burger also raises the prospect of a push by Democrats to raise corporate taxes. If successful, this could also spark inflows into municipal bonds, given the tax exemptions they offer investors, he says.

Meanwhile, Insight fixed income fund manager Gautam Khanna believes the Senate staying Republican under a Biden presidency means game-changing policies are less likely. In his view, markets will take comfort that further trade flare-ups are less likely (a positive for emerging markets and trade-exposed names), while possible Senate resistance to tax hikes will also be viewed positively.

However, the Senate could also look to curtail Democrats’ fiscal spending ambitions, with pandemic relief packages and renewed infrastructure spend likely to face deadlock. The potential deregulation roll-back may also hurt sectors such as energy and autos, he adds.

“If the pandemic continues to deteriorate and anarrow Republican Senate majority is a roadblock to a larger fiscal stimulus package, this ‘stimulus disappointment’ could cause increased volatility, offsetting the positive certainty on the tax front,” he says. “Nonetheless, markets are often comfortable with a lack of real policy change – so, for now, we see that result as positive for risk.”

Global equities: The long term view

For the Walter Scott investment team, the outcome could represent a change of direction in US policy with the prospect of higher taxation (albeit with more fiscal stimulus), wider health care benefits, a higher minimum wage and a re-engagement on climate changes issues. Even so, just how much of that agenda will actually be enacted depends on the extent to which a Republican Senate might counter some of these policies, aside from the question of government finances. They add: “Markets have increasingly anticipated policy shifts, but whatever the political landscape, we’re confident the US will remain a haven for enterprise and innovation. We’ve found that long-term growth patterns for businesses able to adapt and innovate are rarely significantly altered, whatever the political twists and turns.

Please keep checking back for updates on the US Election aftermath, the ongoing Pandemic and a range of investment commentary from some of the world’s leading investment houses.

Please see below an article received early this afternoon from Legal & General Investment Managers which provides their latest views on the U.S. Election:

It looks like the end could be in sight, and all signs are pointing towards a Biden victory, despite Trump’s delaying tactics. Once the election is settled, investment houses will have a clearer picture for the future and will be able to position themselves accordingly.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below update received from Blackfinch Group yesterday afternoon which provides an insight into the ongoing race to the White House and the consequences of US events on the markets.

CONTINUED MONITORING OF THE PORTFOLIOS At Blackfinch Asset Management, we did not play politics with the portfolios and stuck closely with our strategic asset allocation. Tactical overlays were driven by our views of global markets, without placing a “bet” on who would win the White House. As such, the portfolios are robust enough to benefit from either a Trump or Biden victory. Clearly from the polls, it’s extremely difficult to predict outcomes of such huge events, and furthermore the reaction of global markets when outcomes become more certain.

The United States is a large, diverse and wealthy nation, and our asset allocations to the market reflect this. However, our tactical positioning is under continuous review. We will endeavour to update you on portfolio activity as the political backdrop evolves. As it stands, we do not envisage any changes to the portfolios under a Biden presidency and the portfolios are well positioned in this regard.

THE PRESIDENTIAL RESULT The presidential election dust is settling in the United States and it points to there being a new president in the White House. Yet, over 24 hours on, this is by no means guaranteed. What we do know, at the very least, is that the polls predicting a landslide victory for Biden were wrong, and it was a much more closely fought election than they made out. Question marks will remain as to how much the polls can be relied upon in such crucial events like a presidential election when all is said and done.

As it stands on the morning of 5th November, Biden has gathered 264 electoral votes out of the required 270 needed for a majority victory. He is ahead in Nevada as votes continue to be counted, a state that would provide the remaining six electoral college votes to win the presidency. Biden won critical states in Arizona, Wisconsin and Michigan, states that Hillary Clinton failed to win in 2016 and which then, ultimately, created a path for Trump to take office in the White House. Trump, this time round, has already gained more votes than he did in total in 2016, boosted by a greater turn out, and retained key battleground states in Florida and Texas. Trump could take all remaining states outside of Nevada and the United States will still have a new president in Joe Biden.

It is doubtful that events will be smooth sailing from this point, with Trump already threatening to challenge the result in the Supreme Court. This could lead to weeks of political wrangling as the election is extended into a rare legal battle. Any stimulus bill to cushion the longstanding effects of the ongoing pandemic would likely be pushed out to 2021 as Congress deals with the ramifications of a challenge on the presidency.

MARKET OUTLOOK Markets, at least in the short-term, are ignoring the risks of a delayed stimulus package and a potentially uncertain political backdrop as the Republicans look set to retain control of the Senate. A Senate controlled by the Republicans with a Democratic president would quash any “Blue Wave” trade whereby a shift towards fiscal over that of monetary policy would lead to much higher government spending, higher yields and a return of outperformance from cyclical sectors. A Republican-controlled Senate also reduces the likelihood of increased regulation and anti-trust challenges of the Big Tech companies such as Google, Facebook and Amazon.

Equities rallied yesterday, particularly the tech-heavy NASDAQ, while long Treasury yields fell dramatically as a rotation out of the Blue Wave trade developed when a Biden/Republican combination in the White House and Senate looked likely. Although uncertainty remains, this political combination in the White House and the Senate continues to be the greatest likelihood of outcomes from the election. The political rhetoric from the campaign trail should be dialled down now, resulting in a more centrist presidential administration than there perhaps otherwise would have been if the Democrats gained control of the Senate. Biden may reverse many of the executive orders issued by Trump during his four years in office, but overturning legislation with a Republican Senate will be much more challenging. Political gridlock would ensue, and that should be good for markets and volatility.

Although Biden appears to be edging closer to victory, we do not know how long it will take before the election result is revealed, as turbulence surrounding vote-counting continues. Please check in again with us soon for further updates.

Please see latest emerging markets article below from Invesco – received 05/11/2020

Emerging markets beyond COVID-19: all about picking and choosing

02 October 2020

Arnab Das – Global Market Strategist

In the context of slow global growth, we believe investors can benefit from reducing home bias in favour of emerging market (EM) exposures. However, EM investing is much more than simply buying or selling the market.

“Despite not slowing the virus, many EMs are reopening national economies and opting for regional lockdowns.”

Arnab Das, Global Market Strategist

In the context of slow global growth, low inflation and ultra-low yields (at least for some time to come), we believe investors can benefit from reducing home bias in favour of emerging market (EM) exposures. However, EM investing is much more than simply buying or selling the market.

Re-assessing emerging markets in the world beyond COVID-19

Post-lockdown re-openings, secondary outbreaks and rising global tensions raise crucial questions about the cycle and the long term, arguably more in EM than other asset classes:

1. Boost or cut EM exposure? Should investors seek higher growth hopes, inflation risks and hence yields in EM, expecting the global economy to recover sustainably, with low inflation, loose fiscal and monetary policies and a supportive financial environment? Or reduce EM exposure in fear of faltering recovery, rising inflation, higher trade/investment barriers, or all of the above?

2.Treat EM as one or pick and choose among countries and asset classes across the EM complex, including local currency, hard currency debt, or equity – as opposed to shifting index exposures?

We expect global financial conditions to continue to support EMs despite clear and present dangers, which we believe are reflected in higher risk premiums in many EMs relative both to developed markets (DM) at present and relative to EM history.

Easy macro policies, financial conditions, low inflation globally should support a gradual global recovery and ‘risky’ asset classes including EM, despite COVID-19 challenges.

We also believe investors should emphasize selectivity in EMs over time. Over the longer term, we expect EMs to reform domestic and international policies, causing growth models as well as macro and corporate performance to diverge. Investors should therefore be able to boost returns and may even be able to lower volatility via selective country and asset-class weightings.

The COVID-19 Great Compression…

The world suffered a “Great Compression” during the first half of 2020 as governments adopted lockdowns to protect public health, sacrificing private income and wealth. Deliberately compressing activity is very different than conventional recessions, in which monetary policy is tightened to stop inflation; or depressions, in which policy is too tight, causing financial stress or crises and multi-year downturn.

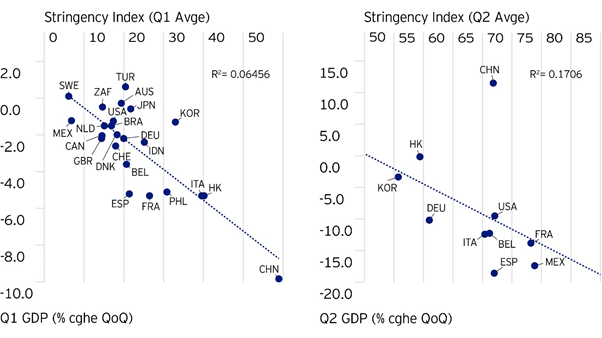

Almost regardless of economic structure – led by manufacturing, services, domestic demand or international trade, or size of government, the tighter the COVID-19 lockdown, the steeper the fall in GDP (Fig. 1, left chart).

Fig 1. A Great Compression: COVID-19 lockdown stringency closely related to GDP performance

GDP growth, QoQ vs. quarterly lockdown stringency averages. Left-hand side, Q1. Right-hand side, Q2. Source: Lockdown Stringency Index, Blavatnik School of Government, Oxford University. National statistical agencies, IMF, Invesco. Data as at various release dates during 1H2020. NB: Excluding China from the Q2 sample raises the R-squared tightness of fit to 0.68.

This downturn was much faster, deeper and wider than economic downturns, which are more gradual and tend to respond to monetary or fiscal easing more directly; wars in which productive capacity is destroyed and must be rebuilt; or natural disasters, which tend to be much more geographically concentrated. Hence, mapping the COVID compression, the current rebound and recovery ahead requires factoring in the conceptual similarities in lockdowns and practical differences in reopening.

Despite the shared compression, we therefore expect much greater differentiation as economies emerge from lockdowns, given vast differences in economic characteristics, macro policies and effectiveness in containing COVID-19. China, first into the pandemic and lockdown in Q1 and first to rebound in Q2, is weakening the global link between lockdown intensity and GDP (Fig. 1, right chart).

… is pushing EMs to re-open, despite rising caseloads and deaths due to policy limitations –

Despite not slowing the virus, many EMs are reopening national economies and opting for regional lockdowns. These policies are not so different from China and DMs with effective lockdowns and regional outbreaks; or the US and UK, which are re-opening generally but locking down regionally, because of ineffective national lockdowns.

We reckon most EMs and DMs will not reimpose economy-wide lockdowns but continue with regional lockdowns unless they face severe second waves.

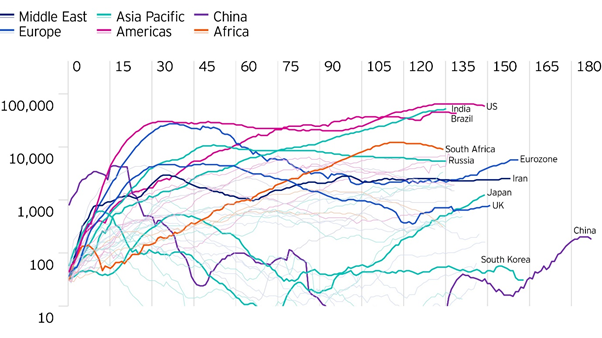

Fig 2. Pandemic performance varies widely across DM and EM economies

Officially confirmed infections, rolling seven-day average. Source: Johns Hopkins Coronavirus Resource Center, Invesco. Data as at 3 August 2020. NB: Y-axis is on a log scale, base 10; 10-fold increases in caseloads occupy the same distance, to help in visualizing the exponential “reproductive rate” of the novel coronavirus behind COVID-19.

But there the similarities end: many EMs lack adequate space for social distancing; public hospitalization and treatment; and public borrowing to compensate for private income lost during lockdowns.

These challenges threaten DMs but are more severe in EMs – another reason the bar will be high for further nationwide lockdowns, reducing the chances of a double-dip economic compression and pressures on EM currency and asset valuations.

After all, its lockdowns and fear of the virus that have hit economies hardest, much more than the direct impact of illnesses and fatalities.

Re-opening rebound set to give way to a gradual, highly differentiated recovery

As lockdowns are released, we expect a re-opening rebound in many countries during Q2-3 as pent-up supply and demand are released. But afterward, we expect more gradual and differentiated recoveries as vast variations in fiscal space, in economic characteristics and in demographic exposure to the virus all come into play.

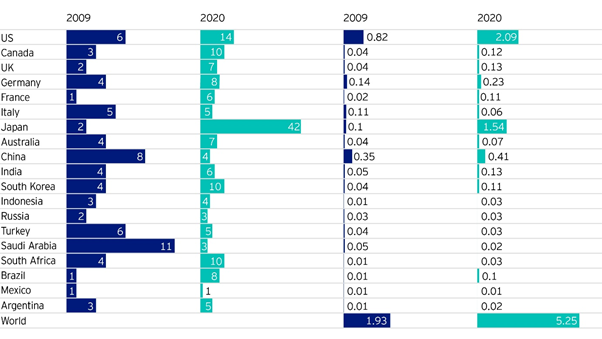

For example, fiscal support varies significantly across the G20 group of largest EM and DM economies, as well as from fiscal responses to the Global Financial Crisis – but is far larger as a share of global GDP today than in 2009.

These variations amid strong global fiscal support give us confidence that country performance will be differentiated amid global recovery.

Fig 3: 2020 fiscal support varies widely by country and compared to the 2009 Global Financial Crisis

Percent share of 2009, 2020 national GDP – left; percent share of global GDP in 2009, 2020 – right. Source: IMF Policy Tracker, IMF GDP Data, Atlantic Council, Invesco. Calculations based on data at various national release and announcement dates, and Atlantic Council as at 26 July 2020. 2009 based on IMF, Eurostat and G20 data. NB: Calculations exclude deferrals and guarantees; include discretionary fiscal support programs (aside from “automatic stabilizers”), announced and implemented programs.

Evolving international system points to gains from diversification and selectivity

During the heyday of globalization 1989-2009, EM investment was about capital gains generated by the convergence of high EM risk premiums to DM levels thanks to economic and financial integration.

The GFC slowed both globalization and global growth, and EM investment shifted to yield seeking and loss avoidance – essentially a carry play. Now, as international tensions rise, we expect EM countries to continue to adopt different regulatory, technological and policy frameworks, trade/investment partners and ultimately varied growth models. Therefore, the cyclical divergence now unfolding should lead to sustained diversity in economic performance.

This is a new world order in which, in the context of slow global growth and inflation and ultra-low yields (at least for some time to come), investors can benefit from reducing home bias in favour of EM exposures.

And capitalizing on diverging EM policy choices and performance would be enhanced by actively picking and choosing EM regions, countries, currencies, sovereign and corporate debt and equity to overweight and underweight.

Please continue to check back for our regular blog posts and updates.