Please see the below article from Brooks Macdonald detailing their discussions on global markets. Received this morning 03/02/2026.

What has happened?

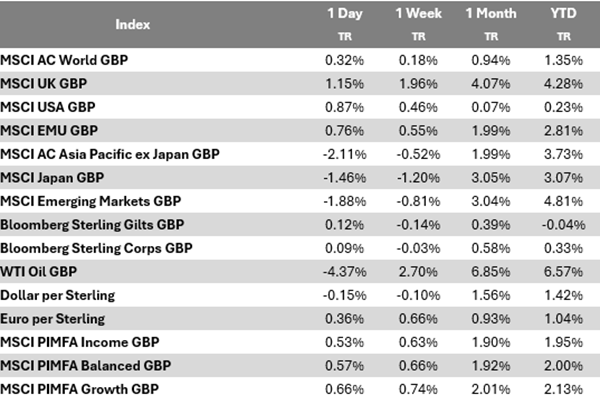

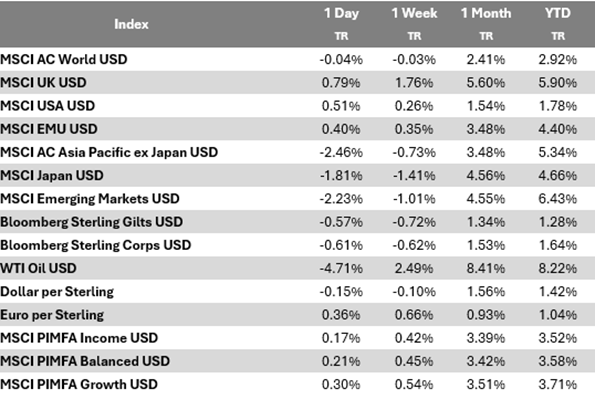

Equity markets staged a sharp rebound following the weekend volatility, with the S&P 500 rising +0.54% and ending just 0.03% below its all time high. While the Mag 7 lagged again (-0.10%) for a third consecutive session, leadership broadened meaningfully: small caps outperformed, with the Russell 2000 up +1.02%. The catalyst for the turnaround was a surprisingly strong ISM manufacturing release, which reached its highest level since 2022 and fuelled renewed optimism around the 2026 economic outlook. European equities echoed the upbeat tone as the STOXX 600 climbed +1.03% to set another record high. However, precious metals were an outlier. Gold fell -4.76% yesterday, marking a two day drop of -13.28%, its steepest since 2013 and the second largest since the 1980s. Silver experienced an even more dramatic move, plunging -6.96% on the day and -31.48% over two sessions, which was the biggest two day decline since Bloomberg’s daily price records began in 1950.

US data surprised on the upside

The ISM print was crucial in shaping yesterday’s risk-on sentiment. January’s reading rose to 52.6 (vs. 48.5 expected), returning to expansionary territory and exceeding most economists’ forecast. New orders surged to 57.1, the largest monthly gain since June 2020, reinforcing the picture of resilient underlying demand. Bond markets adjusted quickly as investors scaled back expectations for near-term Fed easing, with futures reducing the implied probability of a June rate cut from 87% to 70%. This drove Treasury yields higher, with the 2 year rising +4.9bps to 3.57% and the 10 year climbing +4.2bps to 4.28%.

Energy weakness eased inflation concerns

Oil prices extended their decline as geopolitical risk premium eased. Reports indicated that US Special Envoy Steve Witkoff is due to meet Iran’s foreign minister in Istanbul on Friday. It was an unexpected development but helped reverse the sharp risk-driven energy rally seen in January. Brent crude fell -4.36% to $66.30/bbl, while WTI dropped -4.71% to $62.14/bbl, relieving some pressure on inflation expectations. The US 2 year inflation swap declined -4.7bps to 2.55% as a result.

What does Brooks Macdonald think?

While the strong ISM reading reinforces the narrative of resilient US growth, the near-term policy outlook is clouded by the ongoing partial government shutdown. The BLS confirmed that Friday’s January jobs report will not be released as scheduled, again limiting visibility on labour market momentum. Political developments remain fluid: former President Trump urged House Republicans to approve the Senate backed funding deal, with a House vote expected today. From a market perspective, the combination of stronger activity data and easing energy prices paints a mixed but broadly constructive picture, but the underlying trends suggest a market sensitive to incremental information.

Please continue to check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Alex Clare

03/02/2026