Please see below ‘Markets in a Minute’ article received from Brewin Dolphin yesterday evening, which provides a global market and economic update.

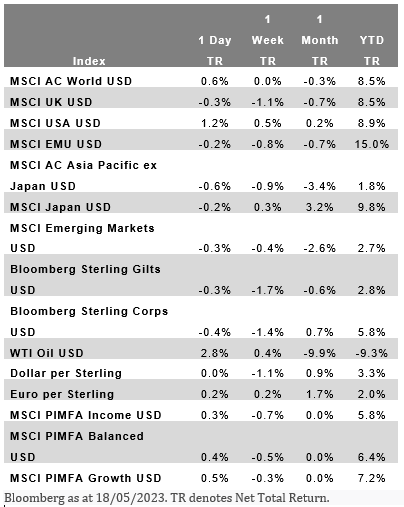

Most major markets finished in the red in a week that saw worse-than-expected economic data from the UK and Germany.

In Europe, the FTSE 100 lost 1.9% as UK inflation rose by a higher-than-expected 8.7%. Pan-European Stoxx 600 lost 1.6% as the German economy contracted 0.3%, taking it into recession.

Over in the US, the S&P 500 rose 0.3% and the Nasdaq added 2.0% as hopes were raised of an agreement on the debt ceiling and optimism over artificial intelligence boosted chip stocks. Meanwhile, the Dow lost 0.6%.

Asia saw all markets decline due to concerns of the US debt ceiling despite a boost in tech stock.

Food inflation falls in May

The FTSE 100 dropped 1.38% on Tuesday (30 May), as UK shop price inflation rose to an annualised 9% in May, up from 8.8% in April, the highest rate in 18 years, according to the British Retail Consortium (BRC).

The BRC announced Tuesday that annualised food inflation fell to 15.4% in May, declining from 15.7% in March. The decline is driven primarily by a fall in energy and commodities costs.

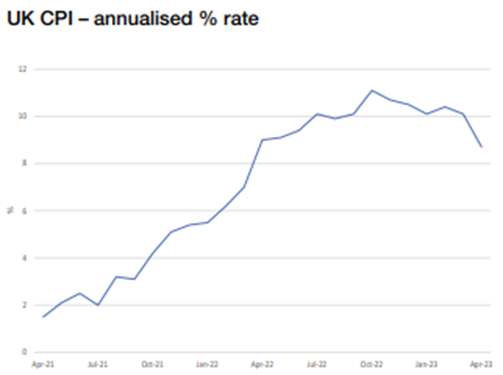

UK inflation remains persistently high

Figures from the Office of National Statistics released last week showed that the UK Consumer Price Index (CPI) rose by an annualised 8.7% in April, down from 10.1% in March and higher than a predicted 8.4%. Falling energy and gas prices contributed to the decline but remain a main driver of inflation alongside food and non-alcoholic beverages. On a monthly basis, CPI rose by 1.2% in April compared to 2.5% in April 2022.

Core CPI (excluding energy, food, alcohol and tobacco) rose by 6.8% in the year to April, up from 6.2% in March, the highest level in over 30 years.

The higher-than-expected inflation figures have led to a sharp decline in bonds, as investors expect the Bank of England (BoE) to raise interest rates further this year. The yield on two-year gilts rose to 4.4% on Wednesday last week, up from 3.7% earlier in the month. Yields rise when bond prices fall.

UK mortgage costs rose by up to 0.45 percentage points at the end of last week, with rates on fixed-rate deals now reaching 5.0% and over. The average two-year and five-year fixed-rate deals are now 5.63% and 4.80% respectively, according to USwitch.

Mortgage lenders have pulled nearly 800 residential and buy-to-let mortgage products from the UK markets in the anticipation of further interest rate hikes, figures from Moneyfacts show. Residential mortgages have fallen by almost 7% in a week, while buy-to-let products have dropped by more than 14%.

Chancellor Jeremy Hunt said on Friday that he was comfortable with the UK entering a recession if this would help bring down inflation, and that he would support the BoE raising interest rates, even as high as 5.5%, to stifle price growth.

UK retail sales volumes rise

British shoppers increased their spending last month as UK retail sales volumes grew by 0.5% in April, rebounding from a fall of 1.2% in March.

The non-food stores sector was boosted by strong performance in the other non-food stores sector, which saw 2.1% monthly growth thanks to strong sales of watches and jewellery and sports equipment. Clothing store sales volumes grew by 0.2%, while household goods fell by 0.2%.

Food store sales rose by 0.7% following a fall of 0.8% in March. Automotive fuel sales volumes fell by 2.2% in April following a 0.1% rise in March.

On a quarterly basis, sales volumes rose 0.8% in the three months to April compared to the previous three months, the highest rate since August 2021.

US debt ceiling agreement reached

US president Joe Biden and House of Representatives speaker Kevin McCarthy have agreed to suspend the US debt ceiling into 2025. The deal would see non-defence spending remaining roughly flat in 2024 before increasing by 1.0% in 2025. Defence spending would increase to $886bn, in line with president Biden’s previously proposed defence budget. The White House estimates that government spending would be reduced by at least $1tn, but no official calculations have been released yet. Most of these savings would come from capping spending on domestic programmes for housing, border control, scientific research and other discretionary spending.

The deal will need to be approved in the House of Representatives and the Senate before 5 June, when the US could default. While some lawmakers are expecting the deal to go through, several Republicans have publicly stated they will vote against it.

The deal has faced bi-partisan criticism; Republicans have argued it does not go far enough to reduce spending or target Biden’s student loan forgiveness plan, while Democrats have targeted the inclusion of work requirements for federal assistance.

Germany enters recession

Germany has entered a recession as the economy contracted 0.3% between January and March, according to government figures. The figures follow a 0.5% contraction in the final quarter of last year. A recession occurs when a country’s economy shrinks for two consecutive quarters.

Germany’s annualised inflation rate hit 7.2% in April, exceeding the eurozone average rate of 7.0%.

An increase in private sector investment and construction at the start of the year was offset by a decline in consumer spending. Household spending fell by 1.2% in the first quarter, as consumers reduced spending on food and beverages, clothing and footwear, and furnishings. Government spending also decreased by 4.9% compared to the previous quarter.

Please check in with us again soon for further relevant content and news.

Chloe

01/06/2023