Please see below article from Brooks Macdonald analysing the potential impact on global equities resulting from the US Federal Reserve’s recent decision to hold interest rates. Received today – 16/06/2023.

Please check out blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Please see the below article from Evelyn Partners providing their thoughts on the FED’s decision to hold interest rates at their present level. Received this morning 15/06/2023.

What happened?

The Federal Reserve met yesterday and chose to hold rates at their current level, for the first time after 10 consecutive meetings where they made increases. This was in line with the market expectations and means the target range remains 5% – 5.25%. The Fed also published their quarterly ‘dot plot’ which shows where committee members see rates heading in the future. It showed rates peaking this year at a level of 5.6%, which is approximately 50 basis points higher than they had been expecting at their March meeting. Expectations for the year end 2024 and 2025 were also revised higher, to median values of 4.6% and 3.4% respectively.

What does it mean?

The long awaiting Fed ‘pause’ has finally arrived, but in rather more hawkish fashion than markets might have expected. The updated dot plot reveals that federal reserve officials expect not one, but two more rate increases before a peak in rates by the end of the year.

Economic data has generally been stronger than expected. Inflation, particularly the ‘core’ excluding food and energy figure, has not fallen away as quickly as some officials had expected, and the jobs market remains extremely resilient. The Feds own projections released yesterday revealed a more negative outlook for inflation and more positive stance on the growth and jobs.

The contradiction of not increasing rates at this meeting but signalling more to come was difficult to communicate in the press conference which followed the meeting. Federal reserve chair Jerome Powell said that pausing at this juncture would give the committee “more information to make decisions” and would “allow the economy a little more time to adapt as we make our decisions going forward”. He also said that he expected the next meeting in July to be a “live one”, sending an indication to markets that an increase is likely then.

Committee members of a more dovish outlook likely remain concerned about the recent failure of three mid-sized banks, which began with troubles at Silicon Valley Bank in March. Powell sounded a note of caution on this yesterday, saying “We don’t know the full extent of the consequences of the banking turmoil we’ve seen”, adding “It would be early to see those”.

Market expectations before the meeting were that there would likely be one further rate hike, so there was some surprise as a further increase was priced in. 2 year treasury bond yields, moved up nearly 20 basis points on the announcement before settling back slightly. The US dollar strengthened relative to sterling by about half a cent and the equity market fell before regaining previous levels.

Bottom Line

The Fed has stopped hiking rates, but only momentarily, signalling to markets that two further 25 basis point rises can be expected before the end of the year, to tame inflation which is not falling as fast as officials has hoped.

While these developments look slightly contradictory, it does give the Fed maximum flexibility for where policy goes from here – if there were to be some big development in the data in the coming months, they can change course.

From our perspective, little has changed – the Fed is close to the top of its interest rate hiking cycle, meaning a headwind for bonds and more interest rate sensitive areas of the equity market will subside.

Please check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

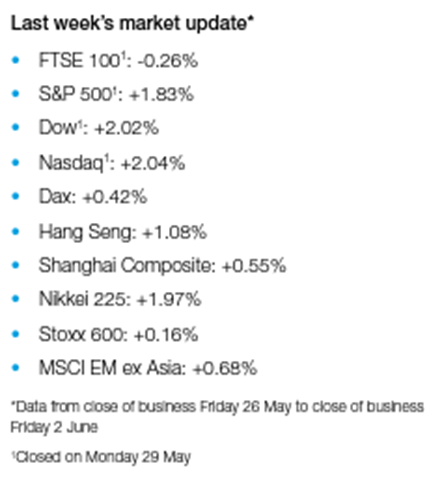

Please see below, the latest ‘Markets in a Minute’ update from Brewin Dolphin which provides a brief analysis of the key news and data from markets over the past week. Received yesterday evening – 13/06/2023

Stocks mixed as eurozone falls into recession

Stocks were mixed last week after revised data showed the eurozone slipped into a mild recession in the first quarter of the year.

The pan-European Stoxx 600 fell 0.5% and Germany’s Dax declined 0.6% following a slew of weak economic data for Europe. The UK’s FTSE 100 lost 0.6% ahead of this week’s interest rate decisions by the US Federal Reserve and European Central Bank (ECB).

In contrast, US indices ended the week in the green, with technology stocks boosted by the unveiling of Apple’s virtual reality headset. The S&P 500 entered bull market territory – up more than 20% from its October lows – and finished the week up 0.4%.

Japan’s Nikkei 225 also enjoyed solid gains, rising 2.4% to hit a 33-year high. This came after the Cabinet Office said Japan’s economy grew by more than initially estimated over the first quarter of the year. China’s Shanghai Composite ended the week flat as inflation figures for May raised concerns about the risk of deflation.

Investors await US CPI report

Stocks started this week on a positive note as investors awaited the release of Tuesday’s US consumer price index (CPI) report. The S&P 500 and the Nasdaq rose 0.9% and 1.5%, respectively, on Monday (12 June) to reach their highest closes since April 2022. Economists expect the CPI for May to show a meaningful easing of inflation to 4.1% year-on-year, according to a poll by Reuters. This would add to the case for a pause in US interest rate hikes this week.

Elsewhere, a report from the Confederation of British Industry (CBI) gave a more encouraging outlook for the UK economy. The CBI expects the economy to grow 0.4% this year and 1.8% in 2024, much better than its initial forecast of a 0.4% contraction in 2023 and 1.6% growth in 2024. It also expects food inflation to fall from 15.5% in 2023 to 4.4% next year.

Eurozone GDP shrinks by 0.1% in Q1

Figures released by Eurostat last week demonstrated the impact that the rising cost of living is having on consumer spending in the eurozone. The revised gross domestic product (GDP) data showed the eurozone’s economy contracted by 0.1% in the first quarter of 2023 and in the final quarter of 2022. This means the eurozone slipped into a technical recession, which is defined as two consecutive quarters of declining GDP.

Retail sales figures for the eurozone were also disappointing. The seasonally adjusted volume of retail trade was flat in April, missing expectations for a 0.2% increase. This followed a decline of 0.4% in March. Among individual countries, Germany saw a 0.8% increase in sales, whereas France saw a 1.3% decline.

Meanwhile, factory orders in Germany unexpectedly fell by 0.4% in April from the previous month, according to figures from Destatis. This followed a 10.9% slump in March. On an annual basis, orders were down 9.9%, following an 11.2% fall the month before.

UK house prices fall sharply

Here in the UK, data from mortgage lenders Halifax and Nationwide showed the first annual drop in house prices for over a decade. Halifax reported a 1.0% year-on-year decline in May, the first drop since 2012. Nationwide reported a bigger 3.4% annual decrease in May, the steepest decline for 14 years.

Robert Gardner, Nationwide’s chief economist, said the drop largely reflected base effects, with prices broadly flat over the month after taking account of seasonal effects. “Recent Bank of England data had shown some signs of recovery in housing market activity, although the number of mortgages approved for house purchase in March was still around 20% below pre-pandemic levels,” he said.

Gardner added that headwinds to the housing market look set to strengthen in the near term. “While consumer price inflation did slow in April, it was a much smaller decline than most analysts had expected. As a result, investors’ expectations for the future path of the Bank Rate increased noticeably in late May, suggesting it could peak at around 5.5%, well above the 4.5% peak that was priced in around late March.”

US jobless claims hit 18-month high

In the US, the number of Americans filing new claims for unemployment benefits surged to the highest level since October 2021. Initial claims jumped by 28,000 to a seasonally adjusted 261,000 for the week ending 3 June, well above the 235,000 claims forecast by economists in a Reuters poll.

Volatility in week-to-week data means it is too early to say whether layoffs have increased. The four-week moving average of claims, which is considered a better measure of labour market trends, rose by just 7,500 to 237,250. Continuing claims (the number of people who received unemployment benefits for two or more weeks) unexpectedly fell to their lowest level in nearly four months.

China’s factory gate deflation deepens

Over in China, factory gate prices fell at the fastest pace in seven years in May as demand faded. The producer price index fell by 4.6%, marking the eighth consecutive month of declines, according to the National Bureau of Statistics. This was the steepest fall since February 2016. The data added to concerns that China is facing the risk of deflation – where prices decrease in a sign of a weakening economy. Consumer prices rose by just 0.2% year-on-year in May, and real estate and factory activity have slowed sharply.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economics updates from leading investment houses.

Please see below article received from Brooks Macdonald yesterday afternoon, which provides a global market and economic update.

China continues to be a global inflation outlier, with consumer price pressures absent, while producer prices fall further into outright deflation

Central banks from US, Europe and Japan decide on interest rates this week, hot on the heels of surprise hikes from Australia and Canada last week

US consumer price inflation in focus this week, and while inflation rates are expected to fall, core prices are still being judged as relatively stickier

The flipside of sticky inflation, economic growth is proving more resilient, as UK Confederation of British Industry (CBI) last week upgrades its economic outlook for this year and next

What happened last week and what are the highlights ahead for markets this week

Global equities arguably had a better week last week than bonds, thanks to continued resilience of large cap US technology stocks in particular. For bond markets meanwhile, surprise hikes from central banks in Australia and Canada spooked bond investors, as they worried about the read-across for the US Federal Reserve (Fed) who meet later this week. Yields on US 10-year Treasuries were up +4.9 basis points (bps) on the week (including +2.1bps on Friday), finishing the week at 3.74%. Looking to the week ahead, we have central bank interest rate policy decisions, in calendar order from the Fed (Wednesday), the European Central bank (ECB, Thursday), and the Bank of Japan (BoJ, Friday). For the Fed, ahead of the meeting, we also get the latest May monthly reading of US CPI (Consumer Price Index) inflation on Tuesday. Rate hikes this week are thought to be most likely to come from the ECB, with the Fed expected to ‘skip’ a hike until July, while the BoJ is expected to continue to stay unchanged. In economic data due elsewhere, US Retail Sales are due Thursday and before that UK monthly GDP (Gross Domestic Product) for April is due Wednesday – expectations are for a month-on-month gain of 0.2%.

China continues to be a big global inflation outlier

Against the sticky and still-high inflation ‘run-of-play’ that we are seeing in most developed economies globally at the moment, economic data out from China on Friday gave markets an important reminder that the world’s second-biggest economy has a very different message: China continues to be a global inflation outlier. China’s latest CPI print for May edged up only slightly to 0.2% year-on-year (versus 0.1% year-on-year in April), while PPI (Producer Price Index) deflation looked entrenched, plunging -4.6% year-on-year. On PPI specifically, it was the eighth straight month of producer deflation and the steepest fall since February 2016. All in all, with inflation currently absent in China, that leaves its central bank with lots of room for manoeuvre to support its economy over the reminder of this year, should it be needed.

Central banks from US, Europe and Japan decide on interest rates this week, hot on the heels of surprise hikes from Australia and Canada

Last week’s central bank meetings from the Reserve Bank of Australia (RBA) and the Bank of Canada (BoC) are an important lead into this week in terms of how their actions has shaped expectations. Both the RBA and the BoC had been expected to leave their rates unchanged, but in the event, both hiked by 25bps. The BoC was particularly noteworthy – after its previous last hike in January, the Canadian central bank had signalled a pause, keeping rates on hold at their March and April meetings. That willingness to sit back however disappeared last week, and Canadian interest rates, at 4.75%, are now at 22-year highs. Driving the increased hawkishness has been inflation stickiness, a theme common to many central banks recently – in Canada’s case, annual CPI inflation rose to 4.4% in April, the first increase in 10 months.

The most important central bank of them all? US Federal Reserve meets

The focal point this week is the Fed rate announcement due Wednesday. For this week, Fed Funds futures are currently pricing in a circa 30% probability of a June hike of 25bps. By contrast, it seems the Fed might yet ‘skip’ a hike in June, only to post a rate-hike at their following meeting in late-July, where the probability of a hike rises to circa 55%. Also, important to look at this week with the Fed’s statement will be their latest Summary of Economic Projections, including their so-called ‘dot-plot’ of interest rate expectations. Feeding into the Fed’s rate decision will be the US CPI print due tomorrow. While the CPI ‘all-times’ annual rate is expected to drop to 4.1% in May (from 4.9% in April), much of that drop comes from the tougher comparative last year when energy and food prices were soaring. For the core CPI print (excluding energy and food prices), this is expected to be running higher at 5.3% but still down on April’s 5.5%.

The flipside of sticky inflation, economic growth is proving more resilient

For most western economies, inflation continues to be above target, especially in the case of core prices. Driving this inflation stickiness however, the flipside is that GDP data for some economies is proving to be somewhat more resilient than had been feared at the start of this year. Take the UK for example – estimates out last Friday from the UK CBI point to +0.4% GDP growth this year (up from a contraction of 0.4% previously), followed by +1.8% in 2024 (versus +1.6% previously). As the CBI noted in its press release “the [UK] economy looks to have fared better than expected in first half of 2023, and is set to steer clear of a recession … tailwinds to growth have strengthened since our previous forecast in December 2022: the global outlook has improved”.

Please check in again with us soon for further relevant content and market news.

Please see this week’s Tatton Monday Digest discussing the key economic news from the past week:

Overview: disinflation sentiment cheers investors

Last week was another positive one for global stock markets, with the narrative of a soft economic landing in 2023 appearing to gather support. Stock market gains in June have been spreading to the mid and small cap market segments, rather than just for a handful of mega-caps. In the US, the mostly small cap Russell 2000 index has risen about 8%, versus 4% for the mega tech-heavy NASDAQ 100. Europe has also seen similar moves, suggesting investors are gaining confidence that the headwinds to growth are turning towards tailwinds, thereby preventing a recession.

Even emerging markets have started June in a more upbeat fashion, compared to a rather muted May. This should probably be seen as win, given the disappointment around China. The world’s second-largest economy – and by far the biggest component of MSCI’s EM index – has been struggling under the weight of expectation for months now. The anti-climax has induced another policy move by Chinese authorities, this time asking banks to reduce interest payments to depositors and to indicate a round of equity market support. There is plenty of liquidity in China, but depressed investor confidence has made valuations there very cheap, so we may be in for a sharp bounce in Chinese equities should the authorities succeed.

Further China policy easing will be another tailwind, and not just for China. However, until the inflation picture really improves in the developed world, central banks will still feel obligated to keep raising interest rates. Last week, both Canada and Australia surprised markets by both hiking rates another 0.25%. This week it could be the turn of the US Federal Reserve (Fed), with its Open Market Committee meeting on Wednesday. Markets have come to expect another rate rise, if not next week, then in July. For what it’s worth, we are not so sure. May’s payroll survey showed a sharp jump in the number of people employed but was quite downbeat in other areas, and the unemployment rate rose to 3.7%. Another factor that could stay the Fed’s hand is the resumption of US Treasury financing after the debt ceiling resolution. The Fed’s current account must be replenished – by issuing large amounts of short-term government debt at competitive rates – and that could drag money away from those rather stressed US regional banks. After March’s unnerving (and economy damaging) episode, another rate rise now risks worsening the situation and causing a second round of bank failures.

We wrote last week that optimists had gained the upper hand over the pessimists and last week’s market gains tell a similar story. It seems that while markets are never without their worries even the pessimists may find it difficult to be apocalyptic when the sun shines.

Japan’s new rising sun?

Japan is having a moment. Over the last three months, its stock market has been the best performer of all the headline regions we track. In the middle of May, the Topix returned to its highest level since 1989, and in June it has taken another leg up, rallying strongly last Monday and Tuesday in particular. Inflation, something that has been virtually absent in Japan for more than three decades, came in at 3.5% in April – coming down from the 40-year high of 4.3% in January. Many investors, both foreign and domestic, expect wage growth will follow. For these reasons and more, markets are more positive about Japan than they have been for a generation.

Celebrating inflation might sound odd, given western economies are still desperately fighting price increases. But deflation has been one of Japan’s biggest problems during its stagnant period, reinforcing savings habits and holding back investment and growth. Inflation has now been running above the Bank of Japan’s (BoJ) 2.0% target for 13 months. But while these sustained price pressures are extremely unusual in Japan, the 3.5% April figure is hardly a cause for concern. The comparative lack of runaway inflation allows the BoJ much more leeway than its global peers. Its interest rates have stayed anchored below 0%, in sharp contrast to the aggressive tightening seen in the US. Lately there have been signs of a rise in the BoJ’s balance sheet. For foreign investors, this has helped underpin the belief that Japan is a safe haven in a risky world.

Before getting carried away, we note Japan has generated similar hype in the past, only for market rallies to peter out when the economy inevitably disappoints. Current detractors say Japan’s inflation is mostly coming from global factors, rather than domestic price pressures, as well as its cyclical sensitivity. Ties with China have been a positive for Japan in the past, but China’s recently disappointing growth has turned this factor into a negative for now. Some have also argued Japanese profitability is only a consequence of the falling yen value, and not a sign of genuine underlying improvement. But this is an oversimplification, as the rise in profitability is not just linked to exporters, but is broad-based across the whole economy. With the home bias among Japanese consumers, we would not expect this if currency depreciation was the only factor at play.

One could just as well argue it is a positive that Japanese profits have kept up in dollar terms – something that was difficult in the past. Moreover, the fall in the yen will have secondary impacts on Japanese exporters, making their products more attractive. If this continues with domestic corporate improvements and economic optimism – as is the case at the moment – it will only strengthen the case for Japan as an investment destination. Japan always does best when it is outward facing and connected to the global economy. Thankfully, its policymakers now seem to recognise that fact.

Please check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Please see below article from Waverton investment management discussing financial markets over the last five years. Received today – 08/06/2023.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economics updates from leading investment houses.

Please see the below article from Brewin Dolphin providing their market commentary. Received yesterday afternoon 06/06/2023.

Stock Markets Rally on US Debt Ceiling Deal

Several indices enjoyed solid gains last week after US lawmakers passed the debt ceiling deal, averting what would have been the country’s first-ever default. The House of Representatives and the Senate passed the legislation after US president Joe Biden and speaker Kevin McCarthy reached an agreement following several weeks of tense negotiations. Stocks were also boosted by the release of a forecast-busting nonfarm payrolls report on Friday. The Nasdaq rose 2.0% in its sixthconsecutive weekly gain, while the S&P 500 added 1.8% to close at its highest level in over nine months. The positive sentiment helped the pan-European Stoxx 600 claw back earlier losses to end the week up 0.2%. In Asia, disappointing factory data from China saw the Hang Seng hit a six-month low on Wednesday before finishing the week up 1.1%. The FTSE 100 was the only major index to end the week in the red, as news of the debt ceiling deal failed to outweigh concerns about China’s economic recovery.

US services sector figures disappoint

Stocks slipped on Monday (5 June) following the release of disappointing US services sector readings. The S&P 500 fell 0.2% after the Institute for Supply Management’s (ISM) non-manufacturing purchasing managers’ index (PMI) fell to 50.3 in May, just above the 50.0 mark that separates growth from contraction. This was well below the 52.2 forecast by economists in a Reuters poll. Monday also saw the release of services sector data for the UK. The S&P Global / CIPS services PMI measured 55.2 in May, down slightly from April’s one-year high of 55.9. Services sector cost inflation hit a three-month high as increased salary payments more than offset lower fuel costs. The FTSE 100 ended Monday’s trading session down 0.1% after enjoying an earlier rally on the back of higher oil prices.

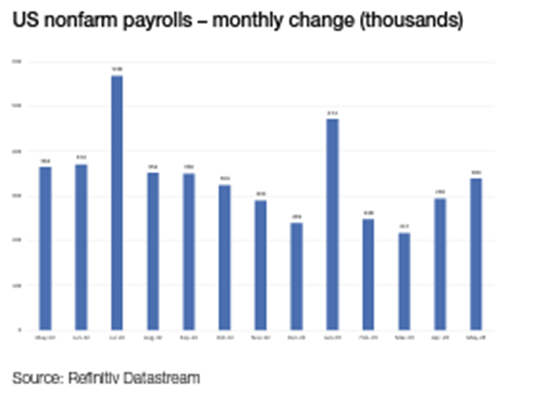

Nonfarm payrolls smash forecasts

The release of the closely watched US nonfarm payrolls report last Friday saw stock markets end the week on a high note. The US economy added 339,000 new jobs in May, according to the Bureau of Labor Statistics. This was almost double expectations of around 195,000. Figures for the previous two months were also revised upwards.

However, not everything in the report signalled strength. The ‘household’ survey, which is based on a survey of around 60,000 US households, showed that jobs growth fell sharply in May. In contrast, the ‘establishment’ survey, which incorporates the payroll records of some 144,000 nonfarm establishments and government agencies, rose. Taking an average of both surveys suggests jobs growth was the weakest in over a year. The unemployment rate also rose to 3.7%, higher than any estimate in Bloomberg’s survey of economists. The data came two days after figures showed US job openings unexpectedly rose in April, indicating persistent strength in the labour market. There were 1.8 job openings for every unemployed person in April, up from 1.7 in March.

US manufacturing contracts further

The latest US manufacturing sector data added to an increasingly mixed picture for the US economy. ISM’s manufacturing PMI fell to 46.9 in May, the seventhconsecutive month it has stayed in contraction territory. The new orders sub-index dropped to 42.6. In contrast, companies continued to increase hiring in May and inflation eased. The survey’s measure of prices paid by manufacturers decreased sharply to 44.2 from 53.2, defying expectations for a modest increase.

Eurozone inflation eases

In the eurozone, headline inflation fell by more than expected in May to 6.1% year-on-year from 7.0% in April. This marked the lowest level since February 2022. Core inflation, which excludes volatile food and energy prices, also eased more than anticipated to 5.3% from 5.6%. Nevertheless, European Central Bank (ECB) president Christine Lagarde said inflation was still too high and “set to remain so for too long”. The ECB is expected to raise interest rates by a further 0.25 percentage points when it meets on 15 June and again in July or September, according to Reuters.

Separate data showed economic sentiment in the eurozone fell by more than expected in May. The European Commission’s index declined to 96.5, the lowest level since November 2022. The decrease was driven by lower confidence in industry, services and, particularly, retail trade. Construction confidence remained broadly unchanged, while consumer confidence continued recovering, albeit at a reduced pace.

China factory activity slumps

Over in Asia, markets tumbled last Wednesday following the release of China’s official manufacturing PMI. The index dropped from 49.2 in April to 48.8 in May, the weakest level since the country ended its zero-Covid policy in December. Production activity fell into contraction for the first time since January, dragged down by declines in new orders and exports. The non-manufacturing PMI, which measures sentiment in services and construction sectors, fell to a weaker-than-expected 54.5 in May, which was also the lowest level in four months.

Please check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Please see below, the ‘Daily Update’ from EPIC Investment Partners, detailing inflation expectations and highlighting the key news from markets. Received today – 06/06/2023

Mark Zandi, Moody’s chief economist, believes the Federal Reserve should not “sacrifice the economy to the altar of a 2% inflation target”, adding that he expects the Fed to pause the run of interest rate hikes at the upcoming meeting. Over the weekend, Zandi tweeted “Why should the Fed sacrifice the economy to the altar of a 2% inflation target (closer to 2.5% for CPI), when most Fed officials probably think a 3% target makes more sense? The zero lower bounds is too close at 2%. They wouldn’t (shouldn’t) let on they have this view, but…,”. He went on to say “The Fed appears set to pause its rate hikes at its upcoming meeting. Thank goodness. Economic growth is fragile, the strong May payroll job gain notwithstanding. Hours worked are falling, so despite all the jobs, aggregate hours worked have gone nowhere this year”.

Another reason he believes the Fed should hit the pause button is the recent stress within the banking sector. Zandi said that government actions had curtailed the deposit run. However, he believes the sector is still “fragile” and depositors are still “on edge” as they continue to move their cash into money-market funds.

Moody’s has also stated that the recent deal on the US debt ceiling will have a minimal impact on the US’ credit profile. “The outcome is consistent with the stable outlook on the US’ Aaa sovereign credit rating,” they said in a statement, adding the agreement “does not change our assessment of the US sovereign credit profile given the act’s limited impact on the federal government’s fiscal position, institutions and governance strength, and the broader economy”.

Also, for those of you that only turn left when boarding a plane and would not dream of flying any lower than first class, Qatar Airways have some bad news for you. The airline, considered by many to be the best in the world, has announced that it will not have first-class berths on its next-generation long-haul aircraft. Akbar Al Baker, Qatar’s Chief Executive Officer, said the investment in the most luxurious seats does not justify the returns, given that Qatar’s business-class offering provides many of the same perks.

So, sorry, going forward you’ll just have to slum it in business class.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below, a ‘Monday Digest’ from Tatton Investment Management discussing the key economic news from the past week. Received this morning – 05/06/2023:

Overview: markets take good news in their stride

In last Tuesday’s digest, we suggested that with the absence of any good news, markets were likely overreacting to the relatively low probability of a US debt default. As it turned out, last week, not only did we get a resolution to the US debt ceiling brinkmanship, but also the welcome news that inflation pressures across Europe were declining faster than expected, while the US jobs market remains paradoxically both vibrant and at the same time showing signs of slowing down (with unemployment going back up). Unsurprisingly stock markets staged a brief relief rally on the debt ceiling resolution, but began wobbling again when Chinese, US and European manufacturing sentiment data showed sure signs of contraction.

On the back of this, bond yields stopped their ascent and declined over the course of the week on the expectation that manufacturing headwinds should persuade central bankers to stop hiking rates. The extraordinarily robust US job market figures on Friday did not appear to change this narrative for bonds, while equities took the strong economic news as outright positive for a change. This came despite expectations for the first rate cut being yet again pushed out further into the future – now only expected for January 2024 (Back in January this year it was implied for the middle of the year).

There is little doubt in our minds that higher rates and higher yields for longer will leave more collateral damage in their wake. But in all, last week was a good one for the optimists, who may well believe equities look more attractive versus bonds again. As to the already seriously expensive US stock market, those same optimists might argue this is mainly driven by companies that will shape our society’s future, and therefore justify the hefty premium. Pessimists, however, will point to the higher-for-longer risks emanating from high interest rates and lending costs eventually driving down demand (and profits), causing a recession-triggering debt default cycle. They might also point out that US tech firms will have to generate almighty profits to justify current valuation hype. Optimists are holding sway just now, but whether it stays this way over the coming weeks remains uncertain. Stay tuned.

The Eurozone is still in an inflation fight

The good mood has excited some investors about Europe’s prospects. Inflation numbers are coming down even more quickly across the continent than had been expected. German inflation fell to 6.3% in May, below the forecast figure of 6.8% and substantially lower than the previous month’s 7.6%. France, meanwhile, saw annual price increases drop to a rate of 6%. For the Eurozone as a whole (6.1% year-on-year), inflation is back to levels seen at the beginning of last year. With some relief we can say that the worst of the European energy crisis is behind us, and surely not a moment too soon. Over time, this should also feed through into wider goods and services to help alleviate second-round price pressures. The European Central Bank (ECB) meeting last month delivered just a 0.25% hike, the smallest of this cycle and a signal that rates are approaching their peak. News that inflation is falling faster than expected increases these expectations, with some investors now predicting the ECB could stop raising rates as soon as July. In any case, the market is pricing in just another 50 basis points from here.

These are certainly encouraging signs, but we should not get ahead of ourselves. While falling energy prices should give the ECB confidence that there is not much more inflation to worry about in manufacturing, services, on the other hand, are showing much more persistent inflationary signs. Strong demand – a rebound from the winter cost-of-living contraction – has allowed service providers to up their prices, and higher wages are being passed on too. The wage factor is a particular concern for the ECB, which considers a cooled labour market the key to taming underlying inflationary pressures, over the long-term at least. In that respect, the signals policymakers really care about – the ‘sticky’ prices – are not as positive as one might imagine from the headline data. This is not to suggest the ECB will follow the BoE’s lead in nailing its hawkish colours to the mast, but merely to point out policymakers will probably be more cautious in believing the hype than some market participants. In particular, due to developments in services and wider labour market concerns, we expect the ECB therefore to sacrifice medium-term economic growth for the sake of continued inflation fighting.

UK’s housing market back under pressure

Britain’s housing market has fared reasonably well over the last year or so, all things considered. However, that resilience is being tested now. Figures released last week showed the number of homes sold in April was 25% lower than a year before, and 8% below the previous month’s figure. Rapid interest rate rises – and the fear of more ahead – are now clearly having a big impact. Earlier in the week, UK lenders pulled out of almost 800 mortgage deals. The number of residential mortgage deals fell by almost 7% in one week alone. Thin volumes often precede falling prices – sometimes sharply – and fewer mortgage offerings dampen the outlook further, almost certainly reducing demand for residential property. So far, the housing market has managed to escape the gloom engulfing most other parts of the UK economy. This is unlikely to remain the case for long.

To make matters worse, it is likely that the impact of rate rises on the housing market will increase over the rest of the year. Around 1.8 million households need to re-mortgage this year, and the majority of those have not yet done so. It is possible some are hoping rates will come down – or at least moderate – as the UK economy worsens. But all the latest communications from the Bank of England suggest they are still extremely concerned about lingering inflation, and are prepared to raise rates further if need be. When those households do re-mortgage, they could find themselves in an even worse situation. Given improved mortgage criteria checks, this should not lead to widespread distressed sales, but it will absorb discretionary spending ability, which will hurt the wider economy.

Structural weaknesses in the UK’s housing supply prevent many building projects and means Britain’s ratio of homes to people is among the lowest in western Europe. This partially explains why prices have been able to grow so dramatically despite increasingly stretched affordability. But while structural imbalances may alleviate downward pressure on prices, they are hardly anything to be pleased about. Like many structural imbalances in the UK, they are ultimately a barrier to long-term prosperity and a sign of deep-rooted challenges. The housing market’s latest malaise is yet another example.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see the below article from AJ Bell received this afternoon giving a market update for today (Friday 2nd June 2023):

Market attention on Friday turned to the US employment report and, further out, the next interest rate decision by the Federal Reserve, after legislators passed a bill that will prevent the US government from defaulting on its debts.

Stocks were higher ahead of the May nonfarm payrolls report, due out at 13:30 BST.

The FTSE 100 index was up 74.26 points, 1.0%, at 7,564.53 at midday in London. The FTSE 250 was up 225.09 points, 1.2%, at 19,052.85, and the AIM All-Share was up 5.05 points, 0.6%, at 789.50.

The Cboe UK 100 was up 0.8% at 754.70, the Cboe UK 250 was up 1.3% at 16,610.82, and the Cboe Small Companies was up 0.4% at 13,632.09.

The US Senate voted to suspend the federal debt limit, capping weeks of fraught negotiations to eliminate the threat of a disastrous credit default just four days ahead of the deadline set by the Treasury.

Economists had warned the US government could run out of money to pay its bills by Monday. This left almost no room for delays in enacting the Fiscal Responsibility Act, which extends the government’s borrowing authority through 2024 while trimming federal spending.

Hammered out between Democratic President Joe Biden and the opposition Republicans, the measure passed the Senate with a comfortable majority of 63 votes to 36 a day after it had sailed through the House of Representatives.

‘Risk sentiment has improved markedly with the passage of the US debt ceiling deal through Congress,’ said Fawad Razaqzada, market analyst at City Index and Forex.com

As US President Joe Biden prepares to sign the legislation into law, attention now turns to the key US nonfarm payrolls report for May. It is expected to show an increase in jobs of 195,000, up from 253,000 in April.

‘US jobs numbers this afternoon may provide some pointers to the next move by the Federal Reserve, whose decision making no longer needs to consider the potential financial stability risks associated with default on US debt,’ said AJ Bell investment director Russ Mould.

‘If the non-farm payrolls data indicates continued tightness in the labour market, the Fed may feel it has to continue with rate rises when it meets on 14 June.’

Fed Governor Philip Jefferson and Philadelphia Fed President Patrick Harker both made the case on Wednesday for a pause in interest rates hikes at the next meeting on June 13 and 14.

Stocks in New York look to continue their rally on Friday. The Dow Jones Industrial Average, the S&P 500 index, and the Nasdaq Composite all were called up 0.5%. On Thursday they ended up 0.5%, 1.0%, and 1.3%, respectively.

The dollar was mostly lower midday Friday in Europe.

The pound was quoted at $1.2530 at midday on Friday in London, up slightly compared to $1.2523 at the equities close on Thursday. The euro stood at $1.0770, higher against $1.0737. Against the yen, the dollar was trading at JP¥138.88, unchanged from Thursday.

Despite its softness ahead of the US jobs report, the dollar is set to rise further, Brown Brothers Harriman thinks.

‘Banking sector concerns and dovish market pricing for Fed policy had been major negative headwinds on the dollar in recent months, but those have finally begun to clear,’ BBH said. ‘Now, we believe passage of the debt ceiling deal removes the final headwind for the dollar, and so we see this recent rally continuing.’

Please check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.