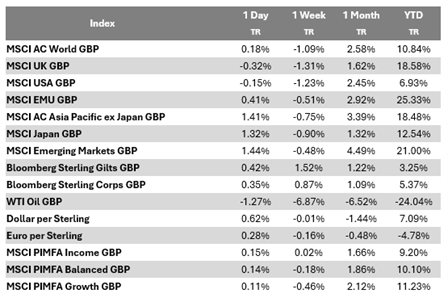

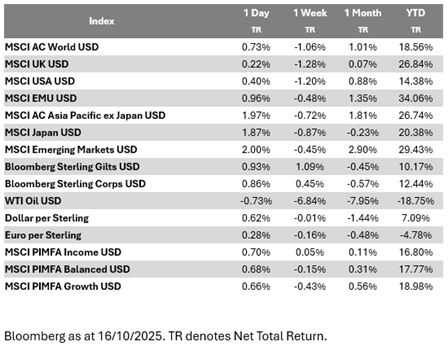

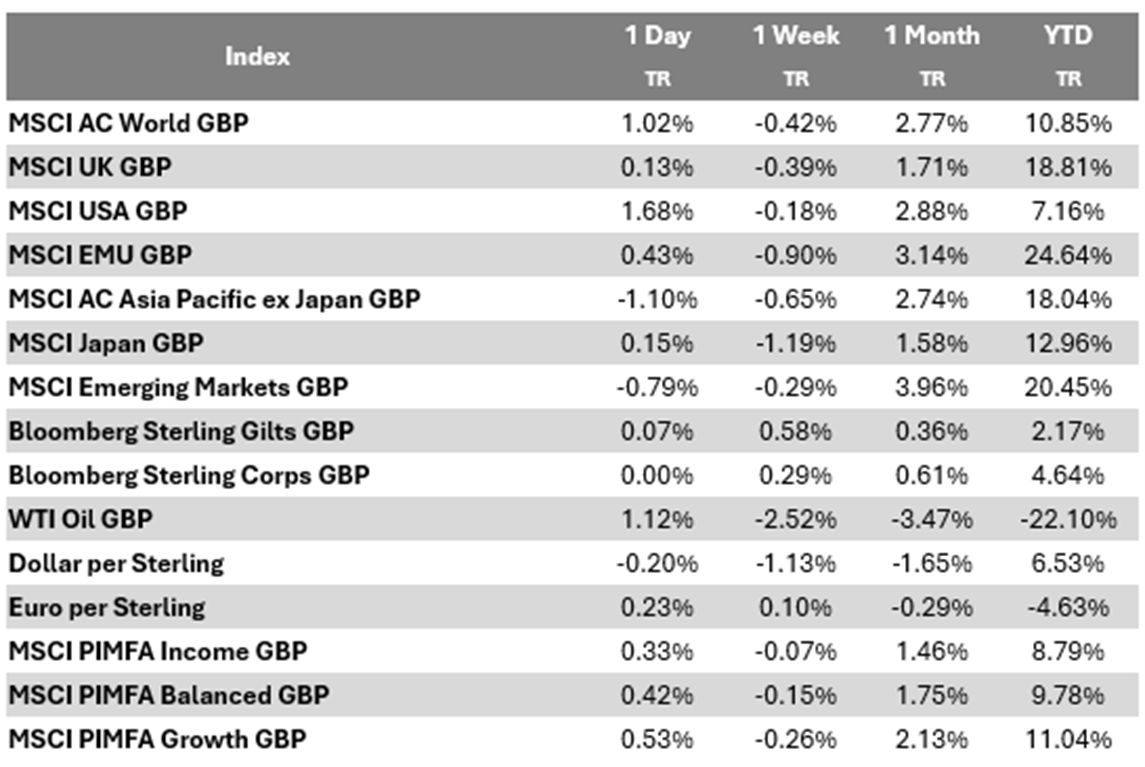

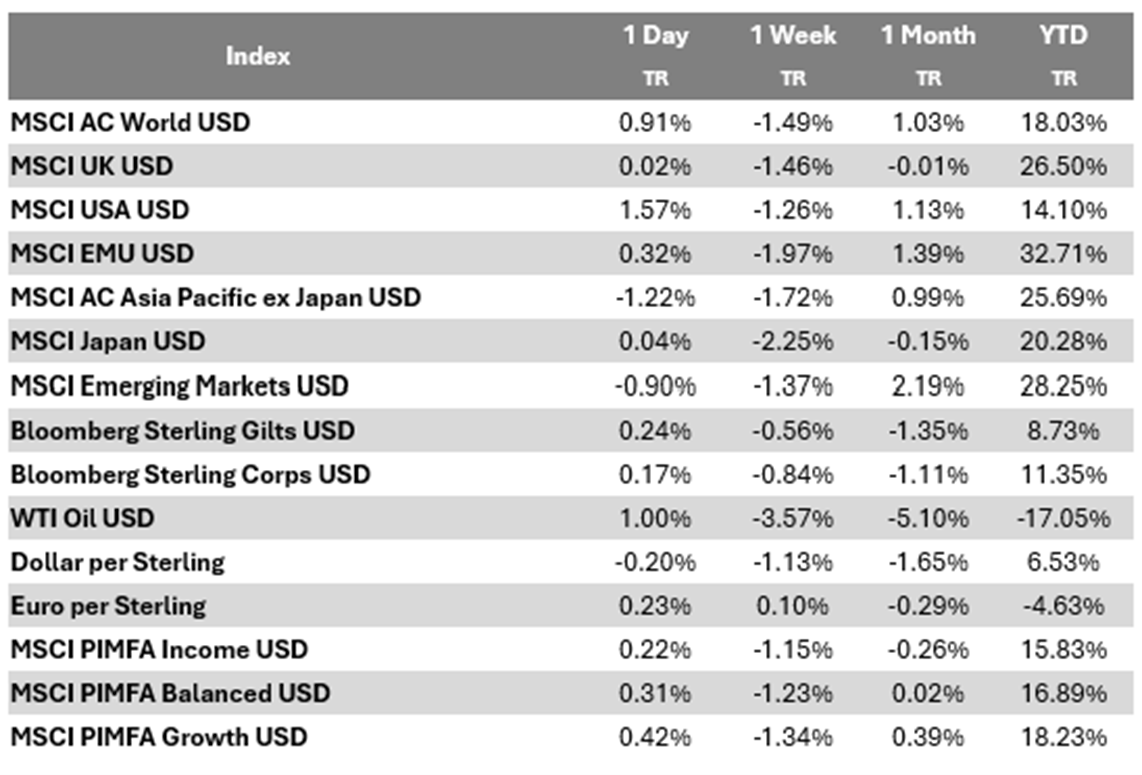

Please see below the daily update article from EPIC Investment Partners, received this morning – 17/10/2025:

EPIC Fixed Income philosophy: breaking free from debt-driven returns

The EPIC Fixed Income Strategy is designed to provide investors diversification beyond the confines of a traditional benchmark. Cognisant of the limitations of fixed income indices, which leads to larger exposure to highly indebted nations, the strategy prefers a rigorous, global search for mispriced sovereign and quasi-sovereign debt issued by wealthy nations, as defined by our Net Foreign Analysis (NFA). Our active approach is built on discipline and deep fundamental insight, creating value across the portfolio.

Active management in practice: the Pemex rally

This active approach is exemplified by our position in Petróleos Mexicanos (Pemex) bonds, a primary contributor to our outperformance. Despite persistent operational and financial challenges, Mexican state-owned Pemex has been one of the major outperformers across the strategy.

For instance, the 7.69% bond maturing in 2050 has seen a remarkable rally of approximately 28% year-to-date*. The true catalysts were the explicit government backing and undervaluation of the bond. The strategic selection of undervalued bonds enables us to bypass the limitations inherent in an index.

Outperformance versus the JP Morgan EMBI Global Index

* Source Bloomberg LP and EPIC Calculations. As at end September 2025.

The Sheinbaum administration – a new chapter for PEMEX

The election of President Claudia Sheinbaum signalled a decisive shift in approach, committing to addressing the company’s deep-seated financial issues. This renewed government support is the single most important factor for bond investors. The explicit commitment underscores the quasi-sovereign character of Pemex’s debt, effectively positioning the Mexican government’s creditworthiness as the ultimate backstop.

The administration’s proactive steps, which underscore their commitment to stabilise Pemex and other-state owned companies, include:

- A comprehensive 10-year plan (2025–2035): This strategic roadmap aims to transform Pemex into a more efficient and sustainable entity through debt reduction, production stabilisation, and the revival of key operations.

- Fiscal relief: A new tax reform is designed to significantly reduce Pemex’s historically high tax burden, freeing up capital for productive investment.

- Direct financial lifelines: The government has provided, and committed to providing, substantial financial support, including a large investment fund to finance projects and ensure timely payments to suppliers.

The market’s confidence has been formally validated by credit rating agencies. In a matter of weeks:

- S&P Global Ratings affirmed its BBB rating in September, a benchmark that has remained in place since March 2020. This consistency is key: unlike other agencies whose recent upgrades were a direct reaction to immediate government action, S&P’s investment-grade rating is the clearest reflection of its belief that the Mexican sovereign link is the fundamental driver of value.

- Moody’s upgraded Pemex by two notches (from B3 to B1) in September, citing a “very high” government support assumption for the company.

- Fitch Ratings followed suit with a further upgrade to BB+ in October, specifically noting that the successful execution of a large government-funded tender offer indicated an “increased linkage between Pemex and the sovereign.”

This wave of upgrades confirms that the government’s financial strategy, centred on improving stability and sustainability, has dramatically improved the credit profile of the Pemex bonds.

The value of vision

The success of the Pemex position validates our core philosophy. By focusing on fundamental analysis and identifying the true drivers of value, such as explicit government support, we capitalise on opportunities consistently overlooked by passive strategies.

Our unconstrained approach allows us to look past headline risk and conventional metrics, enabling us to target value across three distinct areas:

- Political and structural catalysts – identifying sovereign actions that fundamentally alter credit risk.

- Mispriced technical dynamics – exploiting situations where index constraints force others to sell.

- Deep fundamental dislocation – uncovering value where a market’s negative perception ignores strong underlying economic realities.

Our unconstrained process actively creates value for our clients. We move decisively beyond the limitations inherent in index structures, applying deep insight and rigorous selection to generate performance. Our focus remains squarely on value, discipline, and delivering robust returns for your portfolio.

Please continue to check our blog content for advice, planning issues and the latest investment market and economic updates from leading investment houses.

Andrew Lloyd

17/10/2025