Please see below, Tatton Investment Management’s ‘Monday Digest’ providing a brief analysis of the key factors currently affecting global markets and economies. Received this morning – 11/03/2024

At least currency markets noticed the budget

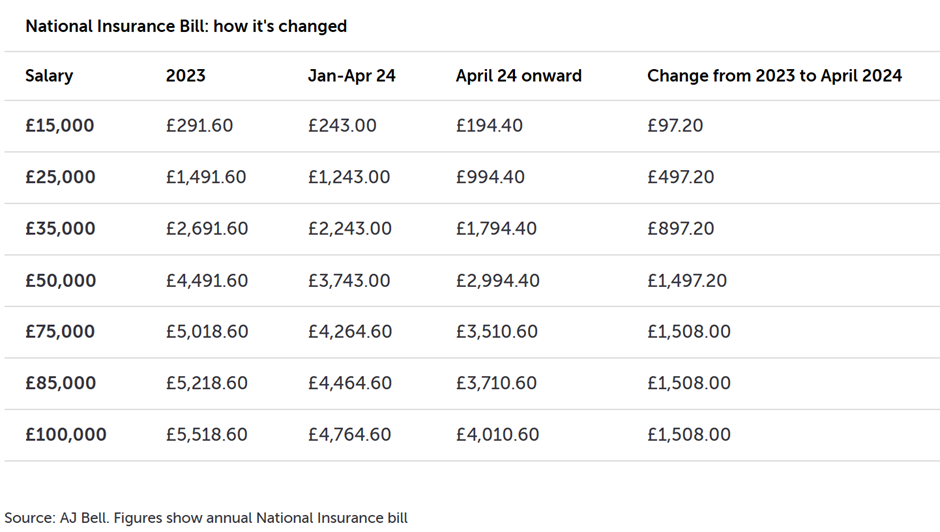

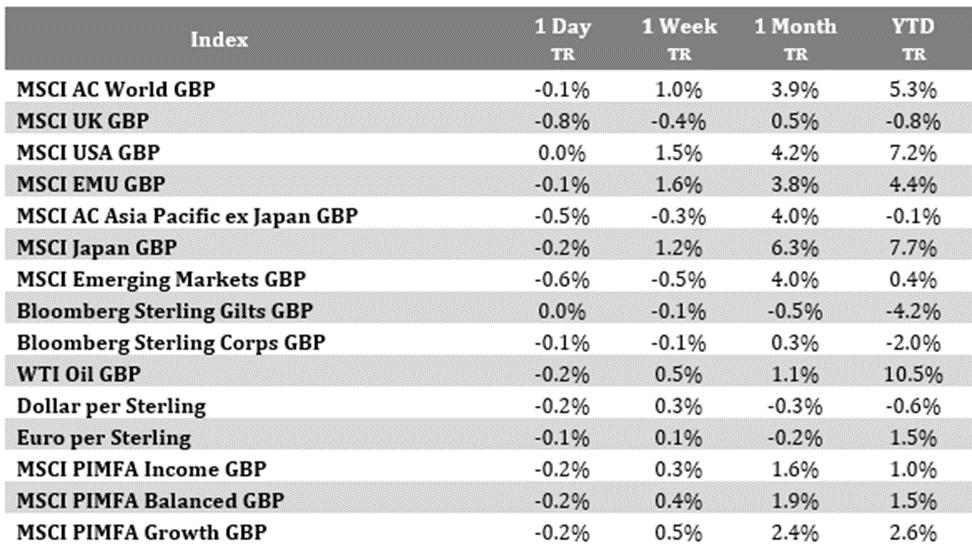

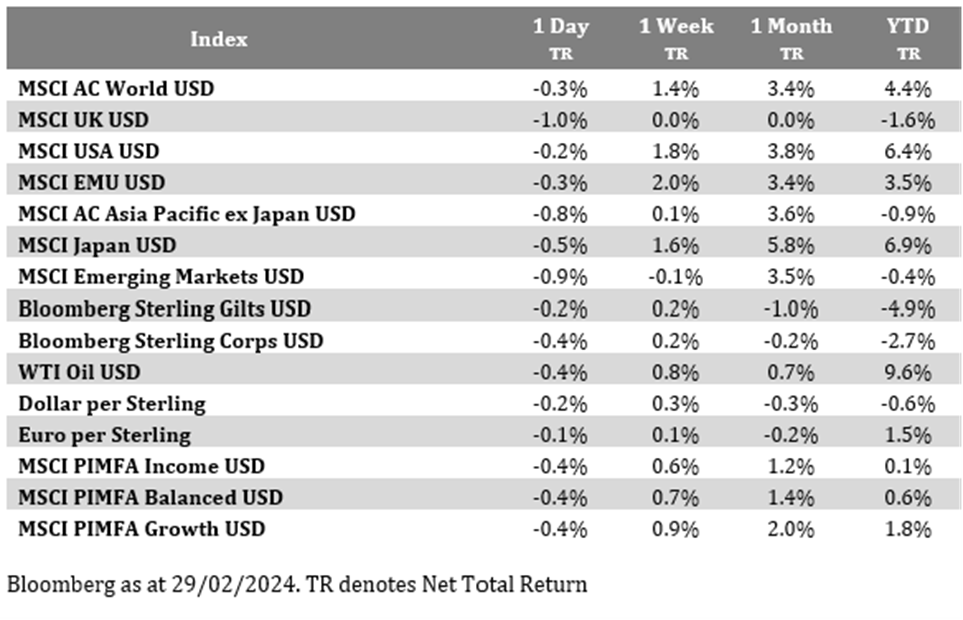

Markets gained again last week, with the S&P 500 hitting another all-time high. But thanks to sterling gaining 1.5% against the US dollar, our table shows negative index returns. Sterling strength may be partly about Jeremy Hunt’s budget, despite the chancellor not giving away so much in the way of fiscal handouts.

The national insurance cut could boost growth, while the freezing of fuel duties will not. The extra ISA allowance seemed more about show; more of a sop than a solution to Britain’s obvious domestic investment problems. Even these small offerings were enough to send our currency higher, though, with foreign investors becoming more optimistic on sterling assets. The outperformance of UK small cap versus large cap was encouraging too.

Rishi Sunak is unlikely to remain Prime Minister for long, but foreign investors are predicting a relatively smooth transition to a new centrist government, and the budget bolstered those perceptions. Mortgage holders will thank him for not raising borrowing costs. So too will the Labour Party, as it means they will more likely be able to borrow to invest.

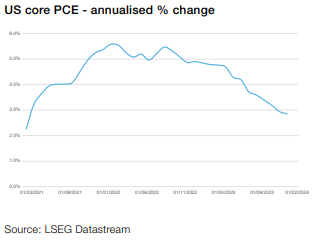

The euro also rose, thanks to the European Central Bank (ECB) leaving interest rates unchanged. The ECB will likely cut by the summer, but President Lagarde seems reluctant to be the first developed market central banker to cut. Federal Reserve chair Jay Powell was similarly mildly hawkish in his testimony to US congress, but investors think a cut is at hand.

Data released on Friday suggests 275,000 US jobs were added in February. That is extremely strong, but the initial data is suspect, as shown by downward revisions to December and January’s initial estimates. Citi Research’s economic surprise indicator shows US economy data is now undershooting economists’ expectations. UK data is starting to beat lowered forecasts while Europe is increasingly beating economist expectations – a great benefit to European equity markets and currency.

What stands out the most, though, is falling volatility across markets – back to or below pre-pandemic levels in most cases. This tends to go in hand with higher equity valuations, as we are seeing now. High valuations also mean that the market has priced in strong future growth. It may be difficult to get more optimistic so that may mean only mild capital gains. We are likely to see more weeks with small gains but little drama.

Tight might soon feel tighter

Balance sheet adjustments – buying or selling assets – are one of the key ways the Federal Reserve (Fed) manages liquidity in the financial system. One of the most impressive things about the Fed’s post-pandemic quantitative tightening (QT – the selling of bonds and mortgage-backed securities) is that it has gotten so little attention. The infamous ‘taper tantrum’ of 2013 caused upsets in markets – and that was just a suggestion that the Fed might not buy as many bonds as it had, not the current outright balance sheet reduction.

Reverse repo operations are one of the key tools the Fed has used to temper the effects of QT. In these, the Fed sells securities for cash now and, at the same time, buys them back at a future settlement date – thereby reducing the current cash in the system. They were crucial in the pandemic for draining excess liquidity that the Fed’s own QE had injected, which was causing short-term “congestion”. Reverse repos have been falling significantly for a while, and this reduction has counteracted the tightening effects of QT. The Fed has been tightening with one hand and loosening with another.

That will likely change, though. The Fed hasn’t told us of any definite plans to taper QT (it is in the ‘talking about talking about it phase’) but the rate of change in reverse repos has already fallen and will level off more the closer operations get to zero. Continuing QT in this phase will probably mean that tight may feel tighter, making markets more volatile.

The key indicator is the gap between interbank lending and the Fed’s reserve rate on repo. When they come closer together it means liquidity levels are at equilibrium.

The Fed could offset any short-term problems by adjusting repos or QT – but we suspect this could become a politically charged topic this election year. Donald Trump might again criticize the Fed for buying up government debt, so the FOMC will want to keep a low profile. But in a sense they might be damned if they do (through allegations of political interference) and damned if they don’t (through market volatility). This poses more risks to stock and credit valuations. QT hasn’t hurt markets yet, but it still can.

Returning M&A returns?

Mergers and acquisitions are trending up. Corporate deals are usually a sign of business confidence, so it makes sense this is happening when markets are buoyant. M&A activity fell dramatically over the last year, thanks to interest rate rises, but Morgan Stanley researchers think we will see a 50% rise this year compared to 2023.

M&A deals need motive and financial opportunity. Activity was massive during the pandemic thanks to extraordinary liquidity, but dramatically shrank through rate rises. Rates are now expected to fall – but rate expectations don’t necessarily set current funding costs. Corporate balance sheets and credit spreads have improved, though, while rallying stock markets have helped companies get more capital. We can see this in Capital One’s all-share buyout of Discover Financial, for example.

There is a huge amount of ‘dry powder’ – capital ready to be invested – held by businesses or private equity funds. Morgan Stanley estimates that global non-financial companies hold $5.6 trillion in cash, while private investors sit on $2.5tn. The US will probably see a lot of activity in private market deals, with less visible partial takeovers or ‘carve-outs’. Regional banks will need to consolidate too, and real estate is primed for M&A.

Researchers also think Europe will lead the way in M&A activity after a relative drought, with consolidations among asset managers and tie ups between telecoms companies. Japan will likely rebound too, thanks to cyclical factors as well as long-term improvements in corporate governance. Globally, Morgan Stanley expects financials to see the most deals, while energy, health and technology could also stand out.

M&A activity could catalyse a rotation from growth to value in markets, since the targets for M&A are usually always undervalued companies. Broadly it should mean more money going into stock markets, but the previous big winners will have less to gain.

Please continue to check our blog content for advice and planning issues from leading investment houses.

Alex Kitteringham

11th March 2024