Please see below article received from Brooks Macdonald this morning, which provides a global market update for your perusal.

What has happened

Global equity indices were up yesterday (in US dollar terms), once again led by mega-cap tech. While the day’s rally did fade a little at the end, Monday still marked fresh record closing highs for both the US S&P500 and tech-focused US Nasdaq equity indices. In contrast, this morning the UK FTSE All-Share equity index is struggling and UK government bond yields are up across the maturity curve, following a dire set of UK public sector deficit numbers – outside of the pandemic, last month was the highest net borrowing for a June month since records began in 1993.

EU trade-talks

With the 1 August tariff-pause deadline next week fast approaching, the lack of progress in European Union (EU)-US trade talks is becoming a concern. While talks are continuing this week, there is speculation that the EU are already planning retaliatory moves in case talks fall apart. Adding to tensions was a veiled threat from US Treasury Secretary Scott Bessent, who said yesterday “it doesn’t have to get ugly”, but “we are the deficit country, so the surplus country will always feel it more. We have a gigantic trade deficit with the EU, and so with the level of tariffs, it will affect them more”.

Middle East

News wires yesterday reported that Iran had agreed to hold talks with the UK, France and Germany to discuss Iran’s nuclear program, expected to take place this Friday in Istanbul, Turkey. However, there are low expectations for any meaningful progress. Ahead of those talks, Iranian officials are due to host a meeting with Russia and China representatives later today, while separately, Iran has yet to formally agree to fresh talks with the US.

What does Brooks Macdonald think

It is hard to argue with recent comments from US bank JP Morgan CEO Jamie Dimon that as regards tariff risks “unfortunately, I think there is complacency in the markets”. It is certainly impressive that global equities (in US dollar terms) are hitting record highs, while at the same time we are still yet to navigate a significant amount of near-term trade tariff uncertainty and risk. Should next week’s 1 August tariff-pause cliff-edge see talks with the EU and other countries unravel, it is not obvious that markets are greatly prepared for such an outcome.

Please check in again soon for further relevant content and market news.

Please see below, an article from Tatton Investment Management, analysing the key factors currently affecting global investment markets. Received this morning – 21/07/2025

Higher and higher

Markets keep rising on incoming liquidity. Growth optimism is improving, helped by strong early Q2 earnings reports. Volatility – both in measured and implied terms – has fallen dramatically, but measured more than implied (the cost of insuring against losses). That means you can profit by selling options and buying the broader market – a recipe for grinding higher.

Chancellor Reeves’ deregulation speech at Mansion House wasn’t well received – but that was more about what she didn’t say (no mention of tax rises) than what she did. Her comments about encouraging risk-taking and getting savers invested in the UK stock market were valid; we’ve argued them before. Follow-through is key, but the City’s pessimism seems a little misplaced. The only thing she did say about fiscal policy was that the fiscal rules are iron-clad. That’s nothing new, but repeating it for bond traders at the back of the room never hurts.

Donald Trump reportedly penned Fed chair Powell’s letter of dismissal – nominally over misconduct but pretty obviously over his refusal to cut rates to the president’s liking. Bond markets were unmoved by this assault on Fed independence (the slight rise in US yields was about stronger growth). We suspect they have faith in the Fed’s institutional strength. Removing the committee chair won’t change the views of the committee – and there’s little suggestion that Trump’s next appointee will follow his rate-cutting orders.

Chinese stocks had a strong week. The media put it down to better growth and nicer Trump – but we think the underlying story is again about liquidity. Chinese households have cash and the government is encouraging them to buy stocks, rather than low-yielding savings or property. That supports stock prices even if company profits are weak. That doesn’t necessarily mean international investors will flock to China (the risk of stranded assets remains), but even if they just move to a “neutral” allocation, it will be strong fuel for Chinese stocks. Like everywhere, liquidity keeps things grinding higher.

Sticky inflation won’t stop UK rate cuts

June’s inflation print – 3.6% year-on-year – was above expectations and the highest in 18 months. Core and services inflation accelerated too, causing markets to slightly dial back their bets for an interest rate cut at the Bank of England’s meeting next month. Markets still see a 0.25 percentage point cut as likely, though. The UK economy is weak and unemployment is rising, as April’s rise in employer national insurance contributions bites. Global input prices are also subdued, largely thanks to Chinese deflation. And while housing inflation looked bad in June’s report, it has decelerated recently.

The fact consumer inflation is high when producer price inflation is subdued tells us companies are moving costs onto customers. They can do so because consumer demand is surprisingly resilient, despite mounting job losses. Pantheon Macroeconomics think the UK economy isn’t as weak as some suggest, with lasting support from last year’s public sector wage rise. Backing that up is the fact that both consumer confidence and retail sales numbers have stabilised in recent months. This could be to do with the fact that total wages aren’t declining, despite layoffs. If that pattern holds, the BoE will have a tough time cutting rates further.

The BoE faces a dilemma. On the one hand, cutting rates while inflation pressures remain undermines the central bank’s credibility (inflation has been above the 2% target for four years). On the other, rising unemployment could quickly spiral into recession if rates stay too restrictive. Last Thursday’s payroll data gave no clarity which way it will go: June’s layoffs were sharper than expected, but May’s job losses were revised down significantly.

June’s inflation won’t stop the BoE from cutting rates next month, but it’s a challenge. Investors can at least take comfort that the challenge is strong consumer demand – ultimately a growth positive.

US inflation: tariffs or growth?

US CPI gained 0.3% month-on-month in June, taking annualised inflation to 2.7%. That’s either in line with or slightly above economists’ expectations, depending who you ask. Core CPI (more important for the inflation trend) came in slightly below expectations at 0.2%. Donald Trump’s tariffs had some inflationary impact – on clothes and furnishings – but it was mild. Tariff effects were subdued by the weakness in global producer prices, coming from Chinese deflation. The most interesting part of June’s inflation report, though, was the New York Fed’s survey showing a fall in consumer inflation expectations.

Markets’ main concern about tariffs has been that they will hurt growth through compressing consumer demand. We worried that this might happen during a weak employment market, but recent employment data has improved. The New York Fed’s survey also suggests that Americans feel more secure in their jobs and finances. It’s early days, but this suggests that tariffs might not hurt demand too much after all. The outlook for real (inflation-adjusted) US growth has improved.

Stronger growth is good for US stocks. For international investors, though, what happens to the dollar is just as important. The currency has weakened greatly year-to-date, dragging down sterling returns on US stocks, but dollar weakness has mellowed recently. We have argued before that the dollar is due a short-term rebound – as low growth was the main downside, and that’s now easing.

But the longer-term case against the dollar remains. The ‘twin deficits’ problem (fiscal and current account) is a drag on the dollar, and it gets worse if US asset returns stop being as exceptional. Trump wants to address one of those deficits (by reducing imports) but his tax cuts are widening the second. The growth and inflation story is dollar positive for now, but that might not last.

Please continue to check our blog content for the latest advice and planning issues from leading investment management firms.

Please see below, The Daily Update from EPIC Investment Partners covering their thoughts on Indonesia’s economic strength following their US Trade Agreement – Received today 18/07/2025:

Indonesia’s Power Play: US Trade Deal Fuels Growth & Ambition

The recently announced US-Indonesia trade agreement is set to significantly reshape bilateral trade dynamics. Under the agreement, Indonesian exports to the US will face a reduced tariff of 19%, down from an initially proposed 32%. Importantly, energy commodities and critical minerals have been exempted from tariffs, aligning closely with Indonesia’s strategic ambitions in industrialisation. In exchange, Indonesia has agreed to substantial purchases from the US, including $15 billion in energy commodities, $4.5 billion in agricultural products, and 50 Boeing 777 jets. These commitments not only support key American industries but also strategically enhance Indonesia’s position in the competitive global market.

Indonesia’s resilience following the devastating Asian Financial Crisis of 1997-1998 highlights its robust economic recovery. That crisis saw severe economic contraction, currency collapse, and substantial capital flight. However, comprehensive macroeconomic reforms, restructuring of the banking sector, and prudent management of foreign reserves have enabled the nation to achieve steady growth, projected by the World Bank to average 4.8% annually between 2025 and 2027.

A key factor underpinning this resilience is Indonesia’s demographic advantage. As the world’s fourth most populous country, with an estimated population of 284.44 million by mid-2025, Indonesia boasts a large workforce and expansive domestic market. Although the annual population growth rate has moderated to around 1.11%, the sheer size of its population continues to fuel domestic consumption and production, underpinning sustained economic activity.

Central to Indonesia’s modern economic strategy is its mineral downstreaming policy, which mandates the domestic processing of minerals like nickel, bauxite, and copper. This policy aims to retain greater economic value within the country, attract foreign direct investment (FDI), facilitate technology transfers, and create employment. The policy has proven successful, attracting record FDI inflows, primarily within the basic metal and non-machinery sectors. The International Monetary Fund (IMF) has endorsed this strategy, acknowledging its positive impact on Indonesia’s external financial stability. The critical minerals exemption included in the US trade agreement further validates this approach, securing crucial markets for Indonesia’s processed minerals.

Despite ongoing challenges related to environmental sustainability and equitable employment, Indonesia’s downstreaming policy exemplifies its ambition to climb the global value chain, reinforcing economic sovereignty and long-term resilience.

A pivotal indicator of Indonesia’s economic transformation is the significant improvement in its Net Foreign Assets (NFA). Following the Asian Financial Crisis, Indonesia’s net foreign liabilities stood alarmingly at -106% of GDP. Through disciplined economic management, sustained current account surpluses, strategic foreign exchange reserve accumulation, and increased FDI, Indonesia has notably improved its NFA position to around -19% recently. This progress, reflected by the country’s upgrade from a one-star to a four-star rating on our net foreign asset analysis, underscores Indonesia’s enhanced capacity to manage financial imbalances and navigate future economic shocks.

In contrast, the US has experienced a stark deterioration in its NFA position. Previously rated four stars in 1998, it is now rated two stars due in part to prolonged budget deficits. With a projected deficit of around $1.9 trillion, or approximately 6% of GDP, the US faces continued reliance on external financing. In contrast to Indonesia’s successful turnaround, the US NFA outlook suggests limited improvement unless significant fiscal adjustments are implemented.

Please continue to check our blog content for the latest advice and planning issues from leading investment management firms.

Please see below, todays Daily Investment Bulletin from Brooks Macdonald covering their thoughts on markets and the ongoing Geopolitical Issues. Received today – 17/07/2025:

What has happened

For the most part, yesterday saw markets continue to digest the latest economic data, including inflation numbers and company calendar-quarter Q2 results that are landing this week. Then, if only for about an hour, investors got a glimpse of how markets might react to a big tail-risk event – namely the risk that the head of the world’s most important central bank, the US Federal Reserve (Fed), might be fired from post. While the rumours were quickly quashed, with conspiracy theories suggesting US President Trump might have been testing markets’ reaction by once-again floating the prospect, there are some important lessons for investors to take away.

A question of central bank independence

Markets reacted quickly yesterday after several news outlets reported Trump was about to fire Fed Chair Jerome Powell. Fears peaked when the New York Times reported that Trump had drafted a letter to fire Powell, with US equity markets and the US dollar down, while US government bonds saw the yield maturity curve steepen sharply. Those moves largely unwound when Trump subsequently said he wasn’t planning to fire Powell, although Trump did caveat saying, “I don’t rule out anything”.

Markets react

With the firing of Powell briefly a serious risk, the US government bond Treasury market saw a huge steepening in the yield curve – at the lows, the US 2-year government bond yield was down -8.2 basis points (bps) on the day at 3.86%, whilst the 30-year bond yield surged by over +10bps in under an hour to an intraday peak of 5.07%. In currency markets, the US dollar index (DXY – an index of the dollar versus a basket of major developed-market currencies globally) slumped down -0.91% at the lows. While the bulk of these moves subsequently unwound as Trump appeared to back-track, the US 30-year over 5-year yield differential was earlier this morning at around 103bps, its steepest level since October 2021.

What does Brooks Macdonald think

In the event of a more Trump-friendly Fed Chair taking charge (Powell’s term as Fed Chair ends anyway in May 2026, though technically he could stay on the Fed board until January 2028), while that could lead to lower policy rates, it isn’t necessarily good news for markets. Sure, lower rates might lower very short-term borrowing costs, but if the markets lost confidence in Fed policy setting, inflation control, and risk premiums more broadly, that could jack up longer-term borrowing costs which the Fed has much less control over. For one, that higher-cost of longer-term borrowing could impact long-term discounted cashflow valuations for megacap tech stocks in particular – and given market concentration risks of tech within US and global equity indices, it is a risk we are alive to.

Please continue to check our blog content for the latest advice and planning issues from leading investment management firms.

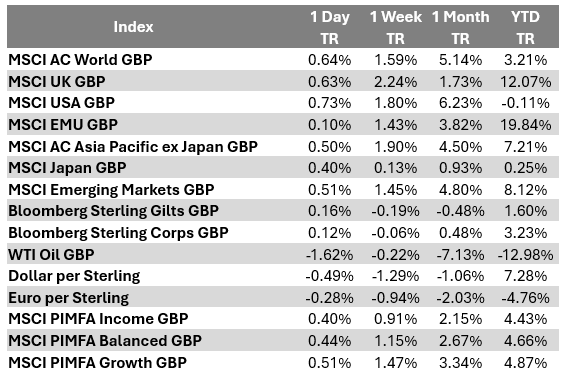

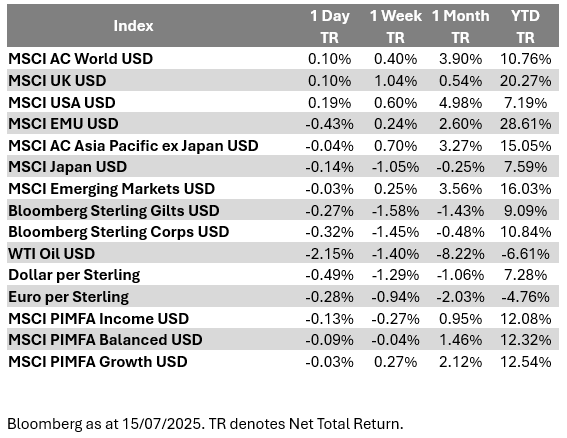

Please see this week’s Markets in a Minute update below from Brewin Dolphin, received yesterday afternoon – 15/07/2025.

Global trade wars and UK growth concerns

U.S. market rallies amid global trade tensions and UK growth concerns.

Key highlights

Breaking new ground: The U.S. stock market has soared over 25% since 8 April, fuelled by President Trump’s tariff deferral, but uncertainty looms with new tariff plans.

Global trade tensions: Tariffs on Brazil, Canada, and copper imports highlight escalating trade tensions, raising costs for key industries and straining international relations.

Economic ripples: Weak UK GDP growth add to the clamour for lower interest rates in the UK, that in turn would be helpful for the public finances.

Market highs amid trade turmoil

The U.S. stock market has risen by over 25% since 8 April, reaching a new all-time high. The rally began when President Trump announced a deferral of the tariffs he had introduced on 2 April. However, the significance of this move seems to have been lost on President Trump, who remarked that he thinks the tariffs have been well received and noted the stock market’s record high.

These comments came in an interview with NBC, during which he floated the idea of imposing 15% or 20% blanket tariffs on “all the remaining countries.” It’s unclear which countries he was referring to. Some media outlets have speculated that he means replacing the baseline 10% rate with a higher rate of 15% to 20%. However, it seems more likely that he means those countries who had deferred tariff rates but haven’t received a letter. The latter explanation seems more plausible, as the Trump administration seems to have reached far fewer trade agreements than it had expected during the 90-day deferral period. Instead, most countries are expected to receive letters, some of which were sent out early last week.

However, by the start of this week, the majority of countries have neither received a letter nor reached a deal, and the 90-day deferral period has now expired.

Last week, additional punitive tariffs were announced on Canada and Mexico, with goods not already covered by the United States-Mexico-Canada Agreement (USMCA) now subject to 35% or 30% tariffs respectively.

Brazil attracted the president’s ire for pursuing a conviction against former President Bolsonaro. President Trump described the charges as a “witch hunt” and responded by imposing a 50% tariff on Brazil. Additionally, several other countries have received individual tariff letters. In most cases, these tariffs are close to the previous individual rates, although those rates were only in effect for a matter of hours before being deferred for 90 days.

The European Union continues to try and find a deal, but if it’s unsuccessful, President Trump announced that it would face a 30% tariff, an unusual 10%-point increase on the ‘Liberation Day’ rate.

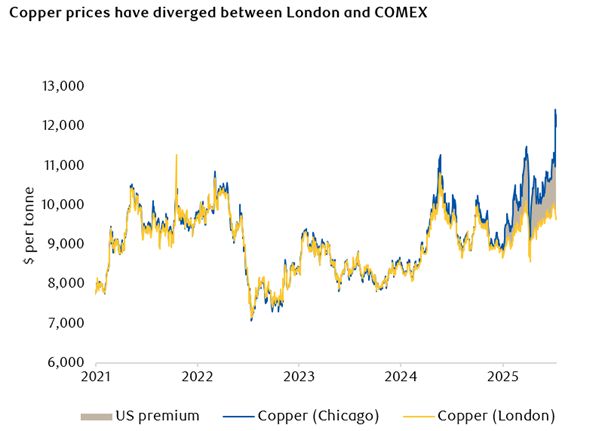

The president has also begun announcing the results of sector-specific tariffs, including a 50% tariff on copper imports. The U.S. currently imports roughly half the copper it needs, as domestic production has been declining. While the tariff could help to reverse that trend, it can take between five and ten years to bring a copper mine from conception to production. In the meantime, the copper import tax is expected to increase costs for U.S. industries such as construction, electronics, automobiles, renewable energy and data centres. The impact of this policy was immediately seen in the diverging price of copper in London and Chicago trading venues. Previously, the two prices were virtually identical, but since President Trump began discussing the possibility of a copper tariff, the two prices have diverged by 25%. While the gap should arguably be 50%, transportation costs for moving copper between markets account for part of the difference.

Copper prices have diverged between London and COMEX

Source: Bloomberg

Whether industry lobbying will be enough for the president to walk back these tariffs, as he has done several times this year, remains to be seen. This is certainly the expectation of the pharmaceutical industry, which has been threatened with a 200% tariff. The tariff is set to be introduced after a grace period of about a year to allow companies to shift their manufacturing to the U.S. However, there’s no way this will result in a meaningful increase in domestic drug manufacturing before it effectively triples drugs prices − an especially contentious issue at a time when the cost of medication is a major concern for voters.

The president, buoyed by calmer markets, appears emboldened to return to the policies which triggered market sell-offs in the first place. He may also have been influenced by criticism of the policies from other billionaires such as JPMorgan Chase CEO Jamie Dimon, who recently expressed concerns about market complacency regarding tariffs during an appearance on Fox News. Obviously, those investors who panicked last time will be wary of doing so again. The risks of getting whipsawed when the market is being driven by the president’s erratic decision making add yet another factor to an already complicated situation.

However, President Trump himself has pushed back against claims of erratic policymaking. Last week, he remarked “We don’t change very much and every time we put out a statement, they say he ‘made a change’… I didn’t make a change, [a] clarification maybe.”

UK starts to feel tax pressures

Source: LSEG

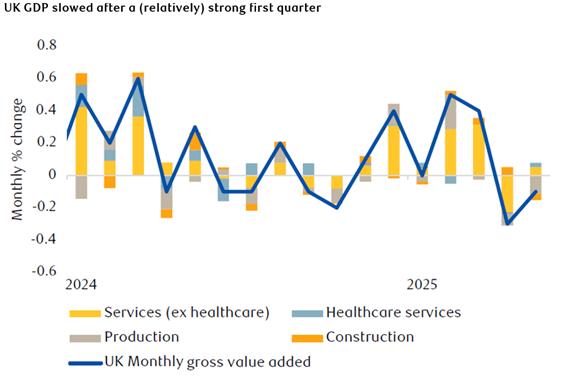

UK gross domestic product (GDP) data released this morning revealed that the economy contracted again in May, defying forecaster expectations of a rebound following April’s decline. UK GDP has been buffeted by a few forces. Tax increases in April, including a rise in National Insurance, contributed to the contraction, and will likely have a lasting impact. An effective increase in stamp duty pulled some housing transactions forward into the first quarter, while exports to the U.S. were also brought forward to get ahead of tariffs.

The UK economy has been slow to recover its momentum. June should be better, though, with positive momentum rebuilding in trade after the earlier shocks this year. Nonetheless, weak growth makes an August interest rate cut increasingly likely. Lower interest rates would be very welcome, as they play a large role in determining whether the public finances stay within the chancellor’s fiscal rules, or whether tax increases are needed this autumn.

Please continue to check our blog content for advice, planning issues and the latest investment market and economic updates from leading investment houses.

Please see below article received from Brooks Macdonald this morning, which provides a global market update for your perusal.

What has happened

Markets yesterday proved once again that they are sensitive to the latest twists and turns in tariff news. With US President Trump late in the day yesterday saying that on tariffs he was “always open to talk”, that proved enough for markets in afternoon trading to edge higher. The US S&P500 equity index finished up +0.14% yesterday to close within 0.2% of last week’s record high, while closer to home the UK FTSE100 equity index gained +0.64% to notch up a fresh record high, all in local currency price return terms.

Mixing tariffs and geopolitics

US President Trump arguably broke new ground yesterday, mixing tariffs with geopolitical deadlines. Trump said yesterday that as well as resuming supplies of US-made Patriot air-defence missiles and other weapons to Ukraine, the US would impose “secondary tariffs” of 100% on countries doing business with Russia unless Russia agreed to a ceasefire within 50 days. While thin on details, it appears that the planned action by Trump would effectively represent additional levies on countries (such as India and China) that buy, amongst other things, oil from Russia.

Gauging Trump’s tariff impact

Today provides another opportunity to gauge what impact Trump’s tariffs are having on both the economy and corporate profits. Later today, we get the most recent monthly Consumer Price Index (CPI) reports from the US and Canada, as well as the calendar Q2 corporate earnings results season kicking off led by the biggest US bank JP Morgan’s results (JPM’s numbers are due out before today’s US market open). On the US inflation front specifically, if the US CPI print is higher than expected (Bloomberg’s consensus estimate is for a US annual all-items CPI rate of +2.6% and a core ex energy and food rate of +2.9%), that could derail US Federal Reserve (Fed) interest rate cut hopes – currently markets (implied from US Fed Funds Futures derivative contracts) are pricing in close to two lots of 25-basis-points of interest rate cuts by December.

What does Brooks Macdonald think

US President Trump yesterday showed that that he is willing to broaden his use of tariffs. Up until now, tariffs have been rationalised by Trump as a means to correct perceived trade unfairness and imbalances. Yesterday saw geopolitics added to the mix, with Trump threatening secondary tariffs on countries that buy from Russia. While this might force Russia to the negotiating table, in doing so it might further cement tariffs as a policy tool that Trump can use across a wide range of other policy ambitions that we have yet to see – as such, tariff policies and tariff uncertainty, even if just a negotiating tactic, could be something of a long-term feature of Trump’s presidency that investors will have to get used to.

Please check in again with us soon for further relevant content and market news.

Please see below, an article from Tatton Investment Management, analysing the key factors currently affecting global investment markets. Received this morning – 14/07/2025

Trump turns nasty; markets turn nice

Markets were on summer holidays last week: volatility dropped and stocks broke all-time highs in local currency terms, thanks to abundant liquidity. However, nasty Trump is back and markets frayed a little as the negotiating tactic of increased tariff pressure played out. As we start this week, Europe and Mexico are under the cosh, as Trump threatens a 30% blanket rate in addition to unchanged sectoral rates. Economic Advisor Hassett told us that the US President sees current EU concessions as insufficient. The EU’s pause in imposing countermeasures may suggest faster progress but the German DAX40 futures were down about 1% as the week’s trading opened. The Euro edged lower against the US dollar by 0.25%.

Last week in the UK, the FTSE 100 broke another all-time high, but the media narrative was about inevitable tax rises. Without underplaying these, some of the rumoured figures (£20bn in hikes) look implausibly high. But a CGT hike is likely, which could cause some pre-emptive asset selling. But the impact on UK stocks will be limited by the fact that Britons don’t own much of their own market. UK bond investors will likely welcome a tax hike, ensuring fiscal discipline, lower growth, and hence lower interest rates (another expected next month). That’s hardly a rosy outlook, but it’s a stable one.

US monetary policy looks less stable, with rumours that Fed chair Powell could be ousted for the more Trump-friendly Kevin Hassett. Those rumours lowered US interest rate expectations, steepening the yield curve, due to both lower near-term rates expectations and higher long-term inflation expectations. Our preferred measure of government ‘credit risk’ moved up – not just for the US but everywhere. That bond move would normally hurt stocks, but investors instead saw it as a growth positive. Optimism was helped by improved US company earnings.

Optimism is also helped by abundant liquidity. CrossBorder Capital point out that the US treasury has injected around $400bn into the financial system in the last six months – via the reduction of its Treasury General Account (TGA). The TGA has fallen even lower than the pre-pandemic trend, partly due to US debt ceiling constraints. But US congress has just raised the ceiling and passed new tax cuts. Compared to the recent months, that will mean a less supportive liquidity flow from the US Treasury.

Investors might therefore be less optimistic. But at the same time, analyst upgrades to company earnings estimates show there is hard data to back up the positivity. We just hope growth signals are enough to support markets when they are less liquid.

Markets doubt copper tariffs

Donald Trump’s surprise 50% copper tariff sent US prices for the metal to record highs last week. The president announced the levy in an off-hand remark, but Treasury Secretary Howard Lutnick reiterated that it would take effect next month – and the episode sent US copper prices 17% higher in a single day. London’s copper futures came down (reflecting a loss of US demand) and the difference between the two rose to an astounding 25%. The fact the premium is less than 50% suggests that markets don’t believe the US – which imports around half of its copper – will totally follow through. The fact other markets didn’t react suggests copper prices could come down even more if and when Trump backs off.

The simple reason markets don’t buy it is because a 50% copper tariff would be extreme self-sabotage. Trump wants to build American industry and win the high-tech race with China – but those things need copper. Ironically, the smelters and refineries needed to expand the US copper industry need the raw metal too. Trump is no stranger to self-sabotage, of course, but the “TACO trade” would suggest that the threat of genuine economic harm will make the president relent.

If that logic doesn’t prevail, things could get nasty. Most tariffs are regarded as one-off cost shocks, but copper demand is structural – and a price hike now could have multiplier effects down the production chain. The threat alone has pushed up US copper prices in the short-term, and adds to the general sense that Trump is back to his disruptive ways, after a period of relative calm for markets.

It will be crucial to watch how this affects other tariffs. The optimistic view is that a blowback on copper weakens Trump’s hand elsewhere; the pessimistic view is that ‘nasty Trump’ is back.

Will China address its overproduction? Chinese producer price inflation (PPI) declined 3.6% year-on-year in June, a stark reminder of China’s deflation problems. Hopes that Beijing will respond with extra demand stimulus buoyed its markets on Friday, but nothing concrete has come through yet.

US tariffs don’t help Chinese deflation, but problems started long before Trump. Chinese companies have little pricing power and have been routinely slashing prices – so much so that the government has told businesses to stop. Consumer demand is weak, hurting company profits and hampering wages, feeding back into weak demand. The housing market never truly recovered from its crash years ago either, further sapping consumer confidence.

Beijing has been pursuing stimulus measures for nearly a year, but the impacts have been underwhelming. Its fundamental problem is that the Communist Party’s main lever for boosting growth – ramping up production – just makes the oversupply issues worse. Official growth numbers still show the economy reaching the 5% target, but that’s largely because of how production – the “P” in GDP – is counted. The factories are firing; people just aren’t buying what they produce. This isn’t to say the official figures are lying, but that the growth targets officials judge the economy against don’t always reflect how the economy feels for most people.

President Xi Jinping has prioritised stability over prosperity in recent years, but there are high-ups in China who are deeply concerned about deflation (as the crackdown on price-cutting shows). Rumours of deflation-busting measures were enough to push Chinese stocks and iron ore prices higher on Friday – as these rumours usually suggest someone is leaking a story.

There are also tentative reports that Xi’s authority might be waning (from total control to near-total control), after the politburo agreed rules on delegating some powers. That’s speculative, but it’s worth remembering that, since 1989, strong growth has been the party’s side of the social contract.

Please continue to check our blog content for the latest advice and planning issues from leading investment management firms.

Please see the below article from EPIC Investment Partners detailing their thoughts on Canada’s response to Trump tariffs and their capability to trade with Asia. Received this morning 11/07/2025.

Canada is embarking on a strategic expansion of its largest port, the Port of Vancouver, aiming to significantly enhance trade with Asian markets, particularly China. The ambitious Roberts Bank Terminal 2 project highlights Canada’s intent to reduce economic dependency on the United States amid rising trade tensions and protectionist policies under President Donald Trump.

Central to this project is the creation of a 100-hectare landmass with a new causeway and wharf on Canada’s Pacific coast. By the mid-2030s, this development is expected to increase the port’s cargo capacity by 70%, handling an additional 2.4 million shipping containers annually. Economically, this will create over 18,000 construction jobs and contribute around C$3 billion annually to Canada’s GDP. Prime Minister Mark Carney’s government has prioritised legislation to expedite approval processes, emphasising the project’s strategic importance for Canada’s long-term economic growth.

The core objective is to significantly expand Canada’s trade capabilities with Asia, particularly China. Increasing west coast port capacity will facilitate direct Asia-bound shipments, reducing reliance on US ports. This move is driven directly by deteriorating US-Canada trade relations, worsened by Trump’s tariffs on Canadian steel and aluminium and his aggressive trade rhetoric, which have unsettled Canadian policymakers.

Trump administration policies, including tariffs justified by national security and rhetoric suggesting potential US absorption of Canada, have eroded longstanding trust. In response, Canada has proactively pursued alternative economic partners to reduce reliance on the increasingly unpredictable US market.

China, already Canada’s second-largest trading partner, stands to gain considerably from the port expansion. Increased Vancouver port facilities will support greater exports to China in agriculture, energy, and minerals. Canada’s existing participation in the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP) and ongoing trade discussions with China further underline this strategic shift.

For the US, the implications are significant. As Canada redirects trade away from its largest export market, American companies, notably in automotive, machinery, and agriculture sectors, could face reduced Canadian demand. This would exacerbate the US trade deficit and negatively impact GDP growth, as net exports significantly influence economic performance.

Additionally, Canada’s diversion of commodities, including oil and critical minerals, to Asian markets means the US may have to source these essential inputs from more distant and expensive providers. Higher production costs could further aggravate the US trade imbalance.

Longer-term US protectionism risks isolating American businesses from advantageous trade agreements increasingly being formed by allies like Canada. This could reduce US competitiveness globally, further impacting economic stability.

Under our net foreign assets scoring model, Canada ranks as a five-star-rated country with net foreign assets just below 50% of GDP. In contrast, the US has fallen to a two-star rating with net foreign liabilities exceeding 70% of GDP. Wealthier countries like Switzerland, Japan, and Canada typically benefit from lower long-term interest rates with Canadian 10-year bond yields currently trading at 100 basis points below the US. If the port expansion is successful, then expect Canada to become a 6-star rated country and the gap between Canadian and US bond yields to widen further.

Please continue to check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Please see below article received from Brooks Macdonald this morning, which offers a global market update for your perusal.

What has happened

Markets had a good session yesterday, shrugging off August 1 tariff concerns. A tech-led rally pushed the S&P 500 (+0.61%) and NASDAQ (+0.94%) higher. The German DAX yesterday and the FTSE 100 this morning hit record highs. Notably, Nvidia (+1.80%) briefly topped a $4tn market cap, closing at $3.974tn. With everything else that is happening, AI remains the greatest hope for US exceptionalism to return. Falling bond yields eased fiscal worries, with the 10-year Treasury yield dropping -6.7 basis points after a strong auction, signalling robust investor confidence despite no clear catalyst.

Trump’s tariff developments

Yes, we have more tariff talks yesterday. President Trump unveiled a 50% tariff on copper imports starting 1 August, a big deal for industries relying on this metal. He also announced a 50% tariff on Brazilian goods, up from 10% on Liberation Day, escalating tensions with BRICS nations and weakening the Brazilian Real by -2.29%, its worst drop since early April. The Philippines got a 20% tariff, and other countries face varied rates, as Trump keeps the trade policy plot twisting.

Federal Reserve insights

The Fed’s June minutes, out yesterday, showed a split on policy and tariffs. A couple of officials hinted at a possible rate cut at the 29-30 July FOMC meeting if data supports it, while some see no cuts at all in 2025, noting the federal funds rate may be close to the neutral level. On inflation, some view tariffs as a one-off price bump, but most worry about longer term effects. This division echoes the ‘dot plot’ published last month: 10 of 19 officials expect two or more rate cuts this year, seven see none, and two predict one.

What does Brooks Macdonald think

The Fed meeting on 29-30 July, just before the 1 August tariff deadline, will see policymakers wrestling with trade levy uncertainties and their economic impact. With inflation’s path still unclear, the Fed is likely to hold steady on rates despite pressure from Trump for more aggressive rate cuts. In addition, oral arguments to the Court of Appeals on whether the International Emergency Economic Powers Act authorises the president to impose tariffs will be heard on 31 July, which adds another layer of complexity.

Please check in again with us soon for further relevant content and market news.

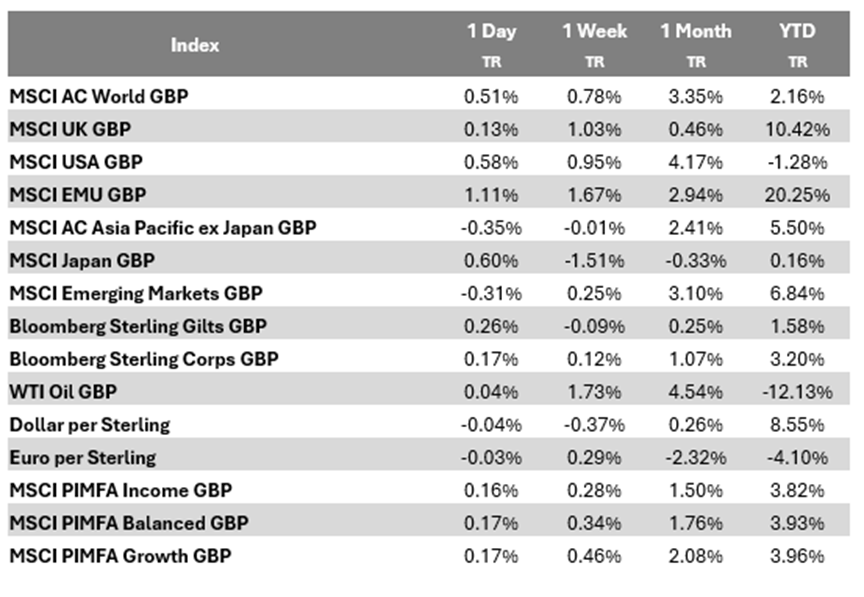

Please see this week’s Markets in a Minute update below from Brewin Dolphin, received yesterday afternoon – 08/07/2025.

Unpacking bond blips, big bills, and labour lulls

We break down the key market moves, policy shifts, and economic signals from the past week.

Key highlights

UK bond market sheds temporary tears: The UK government’s welfare reform U-turn exposed political tensions, briefly unsettled bond markets, and raised questions about leadership and policy direction.

Big bad bill: The U.S. One Big Beautiful Bill was passed by the Senate, extending tax cuts while raising concerns over fiscal sustainability.

U.S. labour market signals: Strong job numbers mask a cooling labour market with slower hiring and wage growth, aligning with the Fed’s ‘wait and see’ approach to interest rate cuts.

Bond vigilantes take on rebels in support of government

Last week, the UK government was forced into yet another humiliating U-turn on its welfare reforms. The objection to this policy is that reform is a euphemism for cuts.

While the government has rightly recognised the need for fiscal restraint, the challenge – as is always the case with politics – lies in reaching consensus on how to achieve deficit reduction.

Many Labour MPs, particularly those in marginal seats, face a difficult balancing act. Cuts to benefits or the desertion of Labour values could cost them at a future election. If spending cuts can’t be made, the chancellor may have no choice but to raise taxes this autumn, given the limited fiscal headroom available.

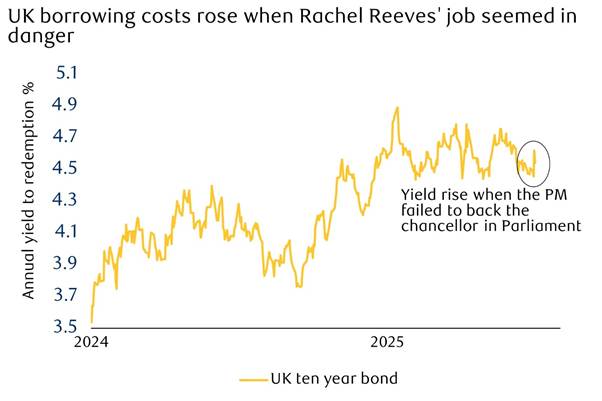

The bond markets remained calm over the welfare cuts, perhaps because the changes themselves are fairly modest. However, bond yields rose when the prime minister missed the opportunity to publicly support his chancellor. Investors will be concerned about the prospect of Rachel Reeves being replaced because it could signal a shift in policy which may place less importance on balancing the books. The bond market’s reaction should serve as a significant boost to the chancellor’s cause.

With the UK holding nearly £3 trillion in government debt, just that one-day rise in yields, triggered by doubts over the chancellor’s position, could theoretically cost around £4 billion if sustained during debt refinancing. Fortunately, a belated endorsement from the prime minister saw yields fall again, minimising the damage. These kind of sell offs are ascribed to so called bond vigilantes because their actions can drive changes in government policy. In this instance, the government should use the action of these bond vigilantes as an endorsement of the governments cost cutting, but whether that brings the rebels back into line remains to be seen.

Big beautiful bill creates bulky bond behemoth

The U.S. budget bill, also known as the One Big Beautiful Bill Act (OBBBA), has now been passed by the Senate and House of Representatives.

The bill extends the original Trump tax cuts that were due to expire at the end of the year. It also includes new tax cuts, such as no taxes on tips and overtime pay, and an increase in the personal tax exemption for retirees. Some of these are due to phase out in future years to make the costs of the bill seem less, but seeing as OBBBA’s primary objective is to make previous temporary tax cuts permanent, it would be naïve to rely upon planned austerity in the future.

In fact, the final version of OBBBA means the boom time budget deficit will remain around 6% of GDP, with a cumulative value projected to reach $3.3 trillion over the coming decade. However, the non-partisan Committee for a Responsible Federal Budget estimates that the cumulative increase in debt could exceed $4 trillion over that decade – or even $5 trillion if temporary measures are made permanent, as history suggests they might be.

Overall, the bill is expected to have a limited impact on the economy, with the deficit remaining close to 6% of GDP over the next few years and the economy currently running close to capacity. However, other recent policies like the clamp down on undocumented migrants restrict capacity growth at a time when demographics limit the natural labour force growth. Furthermore, the trade policy and apparent endorsement of a weaker dollar suggest that the U.S. may increase borrowing while reducing its own earning capacity and discouraging foreign lenders – factors that typically result in higher real interest rates.

The U.S. cannot go bankrupt, as its debts are denominated in a currency which it prints. However, it could default, though this would essentially be a political decision – most likely the result of the brinksmanship between Democrats and Republicans over raising the debt ceiling.

Most plausibly, the sheer volume of bond issuance could gradually push bond yields higher, complicating the effectiveness of monetary policy. While it has been speculated that the Federal Reserve might intervene to suppress those yields, doing so would result in higher inflation. Therefore, although the costs of fiscal largesse may not be intuitive, they are nonetheless very real.

The U.S. bond market sold off last week, driven more by the strong headline employment report than by immediate concerns over the unsustainable path of U.S. government debt. While the headline growth rate suggests that the economy is still strong, it was somewhat inflated –perhaps ironically by a pick-up in public sector hiring.

Trump plans Liberation Day reprise

9 July is approaching, marking the end of the deferral on individual tariff rates announced on Liberation Day. However, the relevance of this date seems to be diminishing.

A trade arrangement has been reached with the UK, a truce has been agreed with China, and Vietnam may have secured a deal too. However, talks with Japan are fractious, negotiations with the Eurozone are logistically challenging, and the Trump administration continues to suggest that a trade deal with India is close.

For the majority of countries, there will be no deal, and the president has begun sending letters outlining their new tariff rates. He had previously suggested that these could rise as high as 60% or 70% but there are no signs of that so far. For example, on Liberation Day, Laos was hit with a tariff of 48%, but in its letter, this has dropped to 40%. For the largest trading partners, the rates are little changed (Japan and South Korea being the most significant examples).

Notable by its absence was the European Union (EU). The bloc has never seemed to be very high on the president’s priority list despite being a significant trading partner. An unnamed source told Politico that the U.S. has offered the EU a 10% baseline tariff with certain key sectors excepted. Depending upon the breadth of, and the rate applied to the excepted sectors, that could be a significant improvement on the 20% rate announced on Liberation Day, but it was not widely reported.

Markets had been expecting a face-saving compromise from the Trump administration. There’s only limited evidence of this in the letters themselves but the new rates will take effect on 1 August, in effect a further deferral, and the president did acknowledge that this leaves more time to reach agreements. Having been chastened by his initial approach of declaring a trade war on all countries simultaneously, the president may opt for a more targeted strategy in this second attempt to raise tariffs.

Please continue to check our blog content for advice, planning issues and the latest investment market and economic updates from leading investment houses.