Please see below an article from Brewin Dolphin which was published and received yesterday (20/01/2023), which details their views on the reopening of China and how this could impact markets:

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below today’s Daily Investment Bulletin from Brooks Macdonald, with a look ahead at Inflation data coming out of the US today. Received this morning – 12/01/2023:

What has happened

As markets eagerly await the US CPI release later today, there was growing optimism that inflation would quickly fade in 2023, buoying equity and bond markets. US 10-year Treasury yields fell with the benchmark yields sitting at 3.53% at the time of writing. Short-dated Treasury yields remained more robust with the Fed still expected to continue with tight monetary policy in the short term, even if we see a downside surprise to inflation today.

EU green subsidies

Risk appetite was also helped yesterday by reports suggesting that the German Chancellor was supportive of a fresh joint EU financing scheme which would provide a counter-balance to the US’s green subsidies which have been instigated by the recent blockbuster Biden bills. The optimism also extended to a broader hope that the EU was more likely to provide bloc wide measures looking forward, in good times and bad. The difference between Italian and German 10-year yields was a direct beneficiary of this with the spread narrowing by almost 0.3% since the start of the year, as investors imply that Germany would ultimately be warmer towards fiscal burden sharing.

US Inflation

With the European inflation numbers pointing to a possible global retrenchment in inflation pressures, hopes have been riding high that we will see a third downside miss to the US CPI release today. Lower inflation now will open up far more options for global central banks to respond to the downturn in economic growth expected in 2023 therefore inflation remains critical to the outcome for US and European GDP this year. As a reminder, the economist consensus expects US headline CPI to fall to 6.5% and for the core figure, which excludes food and energy, to fall to 5.7%. While the initial reaction will be to these primary figures, bond markets will also be studying the sub-components to see if there are signs of slowing inflationary pressures amongst some of the stickier items in the CPI basket.

What does Brooks Macdonald think

As ever, it is hard to overstate the importance of today’s CPI figures. The current rally we have seen in risk assets, while moderate against the context of 2022’s falls, is predicated on an easing inflation backdrop. With inflation appearing to fall, markets are more confident that monetary policy can ease when economic growth recedes, avoiding a harsh recession. A large upside beat to the numbers today would call this into question making 13:30 today a vitally important time for markets.

Please continue to check our Blog content for advice, planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below, an article from Brewin Dolphin looking ahead to what may be in store for investors over the next 12 months. Received yesterday afternoon – 09/12/2022.

After a challenging year for financial markets, Janet Mui, our Head of Market Analysis, looks at what the next 12 months could have in store for investors.

2022 proved to be a challenging year for investors. The war in Ukraine, high inflation, rising interest rates and the growing risk of a global recession meant there were many sources of anxiety for financial markets.

A mild recession ahead

While a recession in major developed economies looks inevitable, the length and depth of the recession is likely to be mild. Labour markets in developed economies remain in good shape, with job openings in abundance. Financial institutions are well capitalised and are unlikely to experience the kind of liquidity crunch that we saw in the 2008 financial crisis. Governments around the world are shielding the most vulnerable from the surge in energy costs, and there are still plenty of pandemic household savings to cushion the blow of the cost-of-living crisis.

That said, the cost of borrowing has risen significantly. 2022 saw the fastest cycle of interest rate hikes in US history, and this is something that will reverberate more visibly in 2023. There will be inevitable adjustments to the years of excesses and imbalances built up in the economy. That could mean a downturn in the housing market, a reduction in borrowing by households, de-leveraging by corporates, and more fiscal prudence by governments in 2023.

Inflation to ease

The biggest challenge for financial markets in 2022 was arguably the persistence of eye-watering inflation, which had a knock-on effect on monetary policy and economic activity. The good news is that inflation is likely to slow sharply in 2023 for a number of reasons.

Commodity prices, including wholesale oil and gas, have fallen markedly. Inventories of goods are building up and shipping costs are declining rapidly, which are good indications that price pressures will fall.

Historically, interest rate rises impact the real economy and inflation with a lag of 12 to 18 months. Inflation of goods and services typically eases as demand falters in a recession. So, once inflation comes down, we can anticipate better times ahead.

Interest rates to peak and pause

We think that most of the large and rapid interest rate increases are behind us in major developed economies. The Fed funds rate is likely to peak at around 5% in the second quarter, while the UK bank rate will likely peak at between 4% and 4.5% in the third quarter.

The hawkish tone from Federal Reserve officials has softened a bit recently, as they acknowledged there is a time lag between monetary policy and the impact on the real economy. Meanwhile, the Bank of England’s governor Andrew Bailey has decisively pushed back against previously elevated market interest rate expectations.

These suggest to us that while central bankers are determined to fight inflation, they know they have already done a lot in a short time span, and they don’t want to overtighten and crash the economy as a result. Whether interest rates will be cut in 2023 depends on how quickly inflation comes down. It seems more likely that interest rates will plateau and stay high in 2023, and that cuts are a 2024 story.

China to gradually reopen

There are more concrete signs that the Chinese government is softening its stance towards Covid restrictions after widespread protests. We think the overall direction remains constructive and that the worst of zero-Covid restrictions are behind us. The normalisation of Chinese activity will be incrementally positive for global demand, at a time when recession looms in 2023.

Investors and, indeed, the market will remain very sensitive to Covid developments in China. There is a general sense of FOMO – fear of missing out – in case there is a big rally, which could help Chinese stocks gather momentum.

While the markets may have got ahead of themselves, and before we get overly excited, we should recognise the challenges and complexities involved in the reopening process. Over the longer term, investors are likely to remain concerned about the political, geopolitical, and regulatory implications of the cabinet reshuffle by president Xi Jinping at the National Party Congress.

Long-term investment opportunities

Despite this year’s economic uncertainty and market volatility, we believe opportunities for long-term investors are emerging. We think there are pockets of attractive opportunities in bonds after the surge in yields and spreads this year. Investors are now able to lock in decent yields while taking little to no credit risk, with the potential for attractive price returns when interest rates eventually fall.

The outlook for equities is less clear. Weak growth and earnings could drag stock markets lower before a decisive fall in interest rates helps equities reach a bottom. Throughout history, equities tend to deliver superior long-term returns. Timing the market is difficult, but the declines in prices we have seen this year give investors the ability to buy good companies at more attractive valuations. Our preference remains on quality companies with strong balance sheets, pricing power, and sustainable business models.

To conclude, while 2023 is likely to be a year of recession, it could be a better year for market sentiment as central banks slow and then pause interest rate hikes, and inflation eases more meaningfully.

Please continue to check our Blog for advice, planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below, an article from Brewin Dolphin providing a summary of the latest news from global markets. Received yesterday afternoon – 06/12/2022.

Eurozone inflation slows for first time since 2021

Shares in Europe rose for the seventh consecutive week last week as a slight easing of inflation raised hopes of slower interest rate hikes.

The STOXX 600 ended the week up 0.6%, with signs of improving economic confidence also helping to boost investor sentiment. The FTSE 100 gained 0.9% despite a sharp slowdown in the UK housing market.

In the US, the S&P 500, Nasdaq and Dow rose 1.1%, 2.1% and 0.2%, respectively, after Federal Reserve chair Jerome Powell signalled smaller interest rate hikes.

In Asia, the Shanghai Composite added 1.8% and the Hang Seng surged 6.3% amid signs that China is moving away its zero-Covid policy. Japan’s Nikkei 225 underperformed, falling 1.8% as data showed a decline in industrial production and consumer confidence.

Asia shares rally as China eases testing rules

Stock markets in Asia rose on Monday (5 December) after authorities in China relaxed some of their strict Covid testing rules over the weekend. It followed a wave of nationwide discontent the previous week. The Shanghai Composite added 1.8% and the Hang Seng soared 4.5%, with travel and technology stocks among the top performers.

The positive news was somewhat marred by the latest Caixin / S&P Global purchasing managers’ index (PMI), which showed service sector activity in China contracted at its fastest pace in six months in November. The index dropped to 46.7, well below the 50.0 mark that separates growth from contraction.

The easing of restrictions in China helped to boost the FTSE 100, which rose 0.2% on Monday, led by the mining sector. Gains were held back by a warning from the Confederation of British Industry that the UK faces a “lost decade of growth” if action isn’t taken to address falling business investment and worker shortages. In Europe, the Dax lost 0.6% and France’s CAC 40 fell 0.7% after S&P Global’s composite PMI for the eurozone showed economic activity contracted for the fifth month in a row in November, marking the longest downturn since the recession of 2011 to 2013.

Eurozone inflation eases to 10.0%

Last week, figures from the EU’s statistics agency showed inflation in the eurozone fell for the first time in 17 months, raising hopes the European Central Bank (ECB) will announce smaller interest rate rises this month. Consumer prices rose by 10.0% year-on-year in November, down from a record high of 10.6% in October and below the 10.4% forecast by economists in a Reuters poll.

Energy price inflation eased to 34.9% from 41.5% in October, which outweighed a slight rise in food, alcohol and tobacco inflation to 13.6% from 13.1%. Services inflation also slowed slightly to 4.2% from 4.3%.

Further positive news came from the European Commission’s economic sentiment survey, which registered its first increase since February. The index rose to 93.7 in November from 92.7 in October, driven by a rebound in consumer confidence. This more than outweighed a further deterioration in industry confidence. Consumers were more positive about their household’s financial situation, both over the past 12 months and especially for the next 12 months. Consumers’ expectations about the general economic situation were also more upbeat.

UK house price growth slows

Here in the UK, the latest research from Nationwide showed a sharp slowdown in annual house price growth to 4.4% in November from 7.2% in October, as the fallout from the mini-budget continued to impact the market. Prices fell by 1.4% month-on-month, the largest fall since June 2020.

Robert Gardner, Nationwide’s chief economist, said that while financial market conditions have now stabilised, interest rates for new mortgages remain elevated and the market has lost a significant degree of momentum. “Housing affordability for potential buyers and home movers has become much more stretched at a time when household finances are already under pressure from high inflation,” he said.

Separate figures from the Bank of England showed UK mortgage approvals dropped to 59,000 in October, down from 66,000 the previous month and the lowest level since the June 2020 lockdown. The ‘effective’ interest rate – the actual interest rate paid – on newly drawn mortgages increased by 25 basis points to 3.09% in October, the highest since 2014.

Fed signals smaller rate hikes

US Federal Reserve chair Jerome Powell said in a speech last week that the central bank could slow the pace of interest rate increases as soon as the mid-December policy meeting. Many commentators are now anticipating a 0.5 percentage point rate hike at the December meeting, as opposed to the four consecutive 0.75 percentage point rate hikes that preceded it. However, Powell also warned against relaxing monetary policy too soon and said the peak interest rate could be higher than previously forecast.

Powell said that in order to bring inflation back down, the labour market would need to soften. However, Friday’s nonfarm payrolls report showed the economy added 263,000 jobs in November, exceeding consensus estimates, while the unemployment rate stayed at 3.7%. Average hourly earnings were up by 0.6% month-onmonth, pushing the annual rate of increase to 5.1% from 4.7% the previous month.

Japan industrial production declines

Over in Japan, industrial production declined by 2.6% month-on-month in October, worse than forecasts of a 1.5% fall, according to flash data from the Ministry of Economy, Trade and Industry (METI). It came as elevated raw material costs and slowing overseas demand resulted in industries scaling back output. Production was up by 3.7% on an annual basis, but this was below expectations for a rise of 5.0% and represented a slowdown from 9.6% growth the previous month. METI’s forecast of industrial production was more positive, with output rising by 3.3% month-on-month in November and 2.4% in December.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see the below article from Tatton Investment Management which was received this morning (05/12/2022) detailing their thoughts on last week’s events and their impact on markets:

Overview: December begins in almost good cheer

December has begun on a positive footing for investors, with market participants choosing to focus on the positives rather than the negatives, and most equity markets now trading above bear market territory again. The release of Federal Open Markets Committee (FOMC) meeting minutes at the end of November gave investors enough reasons to buy risk assets. The minutes were in line with previous statement from Powell, but inflation data had turned less scary in the meantime. With news headlines full of stories of tech firm staff layoffs, signalling an easing of tight labour conditions, markets began to see an end to endless rate rises. Current interest rate futures have US interest rates peaking below 5% and with that peak brought forward to April next year (rather than above 5% in May/June). In other words, it is no longer premature to contemplate the Fed going easier or at least less aggressive at slowing the US economy.

The release of above-forecast US non-farm payroll data might have dealt a blow to the dovish narrative. While surrounding labour market data has shown reasonable signs of a slowdown, it is not yet feeding through to the most important US national labour market surveys. The US picked up another 263,000 employees in November, another outsized month of job growth. Meanwhile, the unemployment rate stayed the same at 3.7%. Lots of jobs being filled while the unemployment rate stays the same ought to mean more people returning to the labour market. Yet the number of people in work or seeking work went down from 62.2% to 62.1% of the working age population. Even worse, they worked fewer hours and the rate of growth of average hourly pay went up slightly to 5.1% year-on-year. So, it’s all very confusing, and markets were skittish as a result. But despite Friday’s volatility, markets have been experiencing more stability over the past couple of weeks, with investors less fearful to invest into risk assets. This seems like a better test of household inflation expectations than just asking people what they expect the rate of inflation to be next year: they are putting their money where their views are.

The release of above-forecast US non-farm payroll data might have dealt a blow to the dovish narrative. While surrounding labour market data has shown reasonable signs of a slowdown, it is not yet feeding through to the most important US national labour market surveys. The US picked up another 263,000 employees in November, another outsized month of job growth. Meanwhile, the unemployment rate stayed the same at 3.7%. Lots of jobs being filled while the unemployment rate stays the same ought to mean more people returning to the labour market. Yet the number of people in work or seeking work went down from 62.2% to 62.1% of the working age population. Even worse, they worked fewer hours and the rate of growth of average hourly pay went up slightly to 5.1% year-on-year. So, it’s all very confusing, and markets were skittish as a result. But despite Friday’s volatility, markets have been experiencing more stability over the past couple of weeks, with investors less fearful to invest into risk assets. This seems like a better test of household inflation expectations than just asking people what they expect the rate of inflation to be next year: they are putting their money where their views are.

It is still not all plain sailing though, particularly with geopolitical risks lingering in the background. While China has not been the largest buyer of cheap Russian oil and gas supplies (the honours belong to India and Turkey), last week President Xi Jinping said China was willing to expand energy trade links with Russia in the future. So even if the markets present good opportunities, the political risks of investing in China will remain apparent while the Xi regime remains in place. The recent sentiment shift has been encouraging. However, it also means that market levels remain vulnerable to a whole host of factors that are fiendishly difficult to forecast – from central bank agendas and desire to reassert their credibility, to the geopolitics of China and Russia, to the level of consumer demand destruction from higher (energy) prices and interest rates that will eventually hurt corporate profits. Last week felt calm, and although we hope things stay that way, we would not bet on it.

Emerging markets still defying gravity

Emerging markets (EMs) are usually highly sensitive to the ebbs and flows of global growth. Investors see EM assets as high risk but potentially high reward, meaning buyers are plentiful when the going is good, and harder to find when things look bleak. In that respect, 2022 looked like an arduous task for EMs: global growth has stalled, interest rates are rising at the quickest pace in a generation, and the US dollar has been exceptionally strong. Many of the larger EM companies have substantial dollar-denominated debts, so this can prove a toxic mix for developing nations. And yet, in many respects, EM assets have held up surprisingly well. This may sound strange, considering MSCI’s EM index has lost around 20% of its value this year, but context is key. The S&P 500 has fallen by a similar amount in local currency terms, while the technology-heavy Nasdaq index has fallen by nearly a third. The comparison to US tech stocks is particularly significant, since both are considered long-term growth assets that are highly sensitive to financial conditions. Tech stocks have taken the hit, but EMs have got off much easier.

Everyone except China has done very well and generated positive returns. Brazil in particular has seen a lot of positivity, despite investor concerns about the return of left-wing President Lula. Strong commodity demand certainly helped as well. At the EM headline level though, all of these have been outweighed by negativity towards China. The world’s second-largest economy has been crippled by Beijing’s zero-Covid policy, along with a severe liquidity crunch in its property sector, and questions over the strongman leadership style of President Xi. With all this in the background – not to mention Russia’s war on Ukraine – EMs could have seen a dramatic fall this year, significantly underperforming developed market counterparts. That most EMs have not is testament to their resilience. Central banks frontloaded their monetary tightening last year, allowing them much more leeway in 2022. Commodity exporters were also helped by rallying energy prices earlier in the year, but even EM nations without these exports have held up well. Underlying this has been a sustained improvement in economic fundamentals. Even though risk appetite has sunk this year, there is a sense that EM risks (excluding Russia and China) are themselves lower, at least compared to previous global downturns.

There is an oddity to this though. For half a decade, analysts have talked about the growing trend of ‘deglobalisation’: the fading or reversal of international trade, which had been marching forward since the 1980s. COVID exposed fragilities in global supply chains, particularly around medical supplies, which increased the incentive to ‘onshore’ production or development in key industries. Onshoring by western countries and the removal of trade links should be bad news for EMs, forcing a structural decline in exports. China’s meteoric rise in recent decades was initially down to its comparatively cheap labour and production costs. As the world’s second-largest economy has matured, those costs have caught up with the developed world. If Chinese production is no longer cheap – and the geopolitical risks are higher – there is little incentive for companies to move there, other than tapping into the enormous Chinese market to sell their products.

Of course, moving out of China does not necessarily mean moving back home – and companies might just as well look for cheaper production sites around the world. This has happened to an extent; India and Vietnam have seen massive production growth. But this process takes time. The trade flows between the US and China, while lower than they were a few years ago, are still huge, and that capacity cannot be easily replaced. These are the key question that investors and policymakers must grapple with in the years ahead. Building trade links takes time, and there is a lot of political pressure to move production back onshore, rather than finding somewhere else. The good performance of EMs outside of China this year suggests globalisation is far from over, but whether the decline is permanent or temporary will depend on politics.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below market insight received this morning from J.P. Morgan, which re-caps 2022 and provides an outlook for 2023.

Developed world growth to slow with housing activity bearing the brunt As we look to 2023 the most important question is actually quite straightforward: will inflation start to behave as economic activity slows? If so, central banks will stop raising rates, and recessions, where they occur, will likely be modest. If inflation does not start to slow, we are looking at an uglier scenario.

Fortunately, we believe there are already convincing signs that inflationary pressures are moderating and will continue to do so in 2023.

Housing markets are, as usual, the first to react to central banks touching the monetary brake. Materially higher new mortgage rates are crimping new housing demand and we think the ripples of weaker housing activity will permeate through the global economy in 2023. Construction will weaken, spending on furniture and other household durables will fall and falling house prices could weigh on consumer spending for the next few quarters. The decline in activity should have the intended effect of taming inflation.

Thankfully, the risks of a deep, housing-led recession of the type experienced in 2008 are low. First, housing construction was relatively subdued for much of the last decade, which means we are unlikely to see a glut of oversupply driving house prices materially lower (Exhibit 1). Second, those that have recently bought at higher prices were still constrained by the banks’ more stringent loan-to-value and loan-to-income ratios.

Finally, the impact of higher rates on mortgage holders is likely to be less severe. In the US, households did a good job of locking in the low rates experienced a couple of years ago. Only about 5% of US mortgages are on adjustable rates today, compared with over 20% in 2007. In 2020 the 30-year mortgage rate in the US hit just 2.8%, prompting a flurry of refinancing activity. Unless those individuals seek to move, their disposable income won’t be impacted by the recent increase in interest rates.

In the UK, some households have similarly done a good job of protecting themselves from the near-term hike in rates. In 2005 – the start of the last significant tightening cycle – 70% of mortgages were variable rate. Today, variable rate mortgages account for only 14%. However, a further 25% of mortgages were fixed for only two years. This makes the UK more vulnerable than the US, albeit with a bit of a delay.

It’s also worth remembering that not everyone has a mortgage, while individuals that have cash savings will see their disposable income rise as interest rates increase. This factor is particularly important when thinking about the larger countries in continental Europe, where fewer households have a mortgage, and household savings as a percentage of GDP are higher than in the US and UK (Exhibit 2). The European Central Bank (ECB) was often warned that zero interest rates would be counterproductive because of the degree of savings in the region.

Europe is weathering the energy crisis well

For Europe, the key risk is less about a housing bust and more about energy supply, given that Russia – the former supplier of 40% of Europe’s gas – stopped the bulk of its supplies this summer.

For the coming winter, at least, the risk to gas supplies is in fact diminishing due to a combination of good judgment and good luck. Europe managed to fill its gas tanks over the summer, largely replacing Russian gas with liquefied natural gas from the US.

Since then, Europe has had the good fortune of a very mild autumn and, as a result, enters the three key winter months with storage tanks that are almost full (Exhibit 3). Unless temperatures turn and we face bitterly cold weather in the first months of 2023, Europe looks increasingly likely to make it through this winter without having to resort to energy rationing.

The gas in storage was, of course, obtained at a very high price. However, governments are to a large extent shielding consumers from the bulk of higher energy prices. We will have to wait to the spring to see whether the cost to the public purse is proving too great for support to continue.

China to open up post Covid, easing global supply chain pressures

The Chinese economy has been faced with an entirely different set of challenges to the developed world with widespread lockdowns still in place to contain the spread of Covid-19. Low levels of vaccination, particularly among the elderly, coupled with a less comprehensive hospital network than in the west, have left the Chinese authorities reluctant to move towards a ‘living with Covid’ policy. However, a prolonged period of lockdown also appears untenable and we expect China to experience an acceleration in activity as pent-up demand is released. While the timing of policy changes remains uncertain, the market’s performance has highlighted how sensitive investors are to any signs of a shift in approach.

Importantly, normalisation of the Chinese economy could significantly ease the supply chain disruptions that have contributed to rapidly rising goods inflation. Although a rebound in growth in China could also boost demand for global commodities, our assessment is that on balance this is another driver of lower inflation in 2023.

Inflation panic subsides, central banks pause

Signs of slowing activity in the west, and a return to full production in China, should ease inflation through the course of 2023, with the shrinking contributions from energy and goods sectors in particular helping price pressures to moderate in the months ahead.

However, to be sure that we’re out of the inflationary woods, wage pressures also need to ease. This is where the central banks went wrong in assuming inflation would prove “transitory”, as they underestimated the extent to which labour market tightness would result in workers asking for more pay (Exhibit 4).

Job vacancies – which in all major regions still exceed the number of unemployed – will be a key indicator to watch in the next couple of months (Exhibit 5). Job hiring and quits are already rolling over and, given higher pay is one of the most common reasons for people moving jobs, we see this as a sign that wage growth should ease.

Assuming headline inflation and wage inflation are easing, we see US interest rates rising to around 4.5%- 5.0% in the first quarter of 2023 and stopping there. The ECB is similarly expected to pause at 2.5%-3.0% in the first quarter. The Bank of England may take slightly longer to reach a peak, given that inflation is likely to prove stickier in the UK. We see a peak UK interest rate of 4.0%-4.5% in the second quarter.

Central banks also have ambitions to reduce the size of their balance sheets by engaging in quantitative tightening, but we do not expect a particularly concerted effort, nor any significant disruption. Quantitative easing was designed to give central banks extra control and leverage over long-term interest rates, helping the market to absorb large scale government issuance. We expect quantitative tightening to operate under the same principle and, given bond supply is still expected to be meaningful in size in 2023 – and borrowing costs have already risen meaningfully – we expect central banks to be modest in their ambitions to reduce their balance sheets.

Recessions to be modest

Ultimately, our key judgment is that signs will emerge in the coming months that inflation is responding to weakening activity. Inflation may not be heading back quickly to 2%, but we suspect that the central banks will be happy to pause, so long as inflation is headed in the right direction.

Against this view, there are two types of bearish forecasters. Some still believe we have returned to a 1970s inflation problem, which will require a much deeper recession and much larger rise in unemployment than we expect to drive inflation away.

Others argue that moderate recessions are difficult to engineer because slowdowns take on a life of their own, with a tendency to spiral. This situation has been true in the past, when deep recessions were busts that followed a boom. Following excessive growth in one area of the economy – most commonly business investment or housing – it has often taken a long time for the economy to adjust and find alternative sources of growth. However, this time round, investment and housing growth has been more modest (Exhibit 6).

In addition, bouts of excess enthusiasm have usually been fuelled by excessive bank lending, which has historically led to a period of weak credit growth, further compounding the downturn. This time round, however, more than a decade of regulation since the global financial crisis means that the commercial banks come into the current slowdown extremely well capitalised, and they have been thoroughly stress-tested to ensure they can absorb losses without triggering a credit crunch (Exhibit 7).

In short, busts follow booms. But booms were notably absent in the last decade where activity across sectors was, if anything, too sluggish. Although economic activity does need to weaken to be sure inflation moderates, we do not expect a lengthy, or deep, period of contraction. Given the decline already seen in the price of both stocks and bonds, we believe that while 2023 will be a difficult year for economies, the worst of the market volatility is behind us and both stocks and bonds look increasingly attractive.

The fixed income reset

Allocating to fixed income has been a never-ending source of headaches for multi-asset investors in recent times. After a long bull market, yields had reached the point where government bonds could no longer offer either of the key characteristics that they are typically expected to deliver: 1) income, and 2) diversification against risky assets. At one point, a staggering 90% of the global government bond universe was offering a yield of less than 1%, forcing investors to take on ever greater risk in extended credit sectors that had much higher correlations to equities. Low starting yields had also diminished the ability of government bonds to deliver positive returns that could offset losses during equity bear markets (Exhibit 8).

This year’s record-breaking drawdown has added to fixed income investors’ woes. Surging inflation, central banks desperately trying to play catch-up and governments that had seemingly lost their fear of debt, have all combined to trigger a brutal repricing. Markets have had to totally rethink the outlook for monetary policy rates and the risk premium that should exist in a world in which central banks cannot backstop the market. The drawdown in the Bloomberg Barclays Global Bond Aggregate in the first 10 months of 2022 was around -20%, four times as bad as the previous worst year since records began in 1992.

Crucially, while the correction in global bond markets has been incredibly painful, we believe that it is nearing completion. Further hikes from the central banks are likely in 2023 as policymakers continue to battle inflation. Yet with the market now pricing a terminal rate close to 5% in the US, around 4.5% in the UK and near 3% in the eurozone, the scope for further upside surprises is significantly diminished provided that inflation starts to cool. This is a key difference versus the start of 2022: this year’s problem has not only been that the central banks have been hiking rates aggressively, but that they have been hiking by far more than the market expected.

Looking forward, it is clear that the income on offer from bonds is now far more enticing. The global government bond benchmark has seen yields rise by roughly 200 basis points (bps) since the start of the year, while high yield (HY) bonds are again worthy of such a title with yields approaching double digits. Valuations in inflationadjusted terms also look more attractive – while the roughly 1% real yield on global government bonds may not sound particularly exciting, it is back to the highest level since the financial crisis and around long-term averages.

What about the correlation between stocks and bonds? What has been so punishing for investors this year has been the fact that bond prices have fallen alongside stock prices. This could continue if stagflation remains a key theme through 2023. While our base case sees stocks and bonds staying positively correlated in 2023, we think this time both asset classes’ prices will rise together. If inflation dissipates quickly, we could see central banks pause their tightening earlier than forecast or even ease policy, supporting both stock and bond prices.

The potential for bonds to meaningfully support a portfolio in the most extreme negative scenarios – such as a much deeper recession than we envisage, or in the event of geopolitical tensions – is perhaps most important for multi-asset investors. For example, if 10- year US Treasury bond yields fell from 4% to 2% between November 2022 and the end of 2023, that would represent a return of c.20% which should meaningfully cushion any downside in stocks (Exhibit 9). Such diversification properties simply weren’t available for much of the past decade when yields were so low.

Given this uncertainty about inflation and growth, and the chunky yields available in short-dated government bonds, investors might want to spread their allocation along the fixed income curve, taking more duration than we would have advised for much of the year.

Within credit markets, we believe that an “up-in-quality” approach is warranted. The yields now available on lower quality credit are certainly eye-catching, yet a large part of the repricing year to date has been driven by the increase in government bond yields. Take US HY credit as an example, where yields increased by around 500bps in the first 10 months of 2022, but wider spreads only accounted for around 40% of that move. HY credit spreads still sit at or below long-term averages both in the US and Europe. It is possible that spreads widen moderately further as the economic backdrop weakens over the course of 2023.

The reset in fixed income this year has been brutal, but it was necessary. After the pain of 2022, the ability for investors to build diversified portfolios is now the strongest in over a decade. Fixed income deserves its place in the multi-asset toolkit once again.

The bull case for equities

Our 2023 base case of positive returns for developed market equities rests on a key view: a moderate recession has already largely been priced into many stocks.

By the end of September 2022, the S&P 500 had declined 25% from its peak. Historically, following this level of decline, the stock market has tended to be higher a year later. There have been two exceptions since 1950: the 2008 financial crisis and the bursting of the dot-com bubble in 2000.

We don’t see macroeconomic parallels with 2008, but what about valuation similarities with 2000? One risk to our bullish base case scenario for stocks would be if valuations still need to fall considerably further from here.

S&P 500 valuations started 2022 not far off those seen during the dot-com bubble. However, high valuations could largely be attributed to growth stocks (Exhibit 10). Despite underperforming in 2022, these stocks are still not particularly cheap by historical standards.

Value stocks, however, are now quite reasonably priced compared with history. We have stronger conviction that value stocks will be higher by the end of 2023 than we do for those growth stocks that still look expensive. However, a peak in government bond yields could provide some support to growth stock valuations in 2023.

Another risk to equities is that consensus 12-month forward earnings expectations currently look too high, having only declined by about 5% from their recent peak. A recession is likely to lead to further reductions in earnings expectations. We believe that in a moderate recession, 12-month forward earnings estimates are likely to decline somewhere around 10% to 20% from the peak, as they did in the 1990s or early 2000s.

While some might argue that when these earnings downgrades materialise, they will lead the stock market lower, we believe that the market has already priced in some further downgrades to consensus forecasts (Exhibit 11). For example, at the beginning of 2022, US bank stocks were reasonably valued at 12x earnings and consensus 12-month forward earnings forecasts rose about 10% over the course of the year – yet bank stocks fell about 35% from peak to trough. This supports our view that the market is already factoring in worse news than consensus earnings forecasts suggest.

We also note that the interaction between consensus earnings forecasts and markets has been inconsistent over time. In the early 2000s and in the 2008 financial crisis, reductions in earnings forecasts led to further stock market declines; but in the early 1990s, stocks rallied as 12-month forward earnings expectations declined (Exhibit 12).

While falling earnings forecasts could lead stocks lower, if the magnitude of the decline in earnings is moderate – as we expect – then it would likely only lead to limited further downside for reasonably valued stocks, relative to the declines already seen in 2022.

We acknowledge that it would be unusual for the stock market to have bottomed already—that does not tend to occur before the unemployment rate has started to rise and the Federal Reserve (Fed) has started to cut interest rates. However, the market has already declined much more than usual before jobs have started to be lost. Given this is probably the best predicted recession in the last 50 years, we believe there is a chance that equity markets could have priced it in sooner than they normally do.

Overall, while we are not calling the bottom for equity markets, we do think that the risk vs. reward for equities in 2023 has improved, given the declines in 2022. With quite a lot of bad news already factored in, we think that the potential for further downside is more limited than at the start of 2022. Importantly, the probability that stocks will be higher by the end of next year has increased sufficiently to make it our base case.

Defend with dividends

Our base case sees a moderate recession in most major developed economies in 2023. We believe that equity markets have already priced in a lot of the bad news in 2022, but stocks which provide an attractive income appear more reasonably valued than those with little or no income (Exhibit 13). Investors who are more cautious than us about the outlook may want to focus on this cheaper segment of the market to hopefully limit further downside.

Of course, the income stream from dependable dividend payers can also help buffer returns. Strong, dividend paying companies often go to great lengths to maintain dividends, even when earnings are under pressure. With payout ratios relatively modest at present, maintaining current dividends looks more feasible than in some prior recessions (Exhibit 14).

Another factor worth considering is that the universe of companies currently paying healthy dividends is fairly diverse, spanning a wide range of sectors. Some of the usual suspects like utilities remain in the pool but we believe sectors such as financials, healthcare, industrials and even some parts of tech contain a number of dependable dividend payers that can also grow their dividends over time. As a result, should the macro backdrop not improve, and stagflationary pressures persist into 2023, we would expect income paying stocks to prove relatively resilient.

In conclusion, even though we expect a challenging macroeconomic environment in 2023 and downward corporate earnings revisions, we think income stocks could have a good year with dividends proving more resilient than earnings. For investors that are tentatively looking to increase their equity exposure, an income tilt could prove relatively resilient in the worstcase scenario, while also providing the potential for outperformance in our more optimistic scenario for markets given attractive valuations.

Catalysts for a recovery in emerging market assets

Emerging market equities had another very challenging year and disappointed investors’ expectations for this promising high growth asset class. By the end of October, the MSCI Emerging Markets Index had lost 29% in 2022, underperforming developed market equities by 10%.

Emerging markets were hit by multiple headwinds, including a sharply slowing global economy, escalating political risks, China’s zero-Covid policy and the fastest Federal Reserve (Fed) tightening cycle in more than three decades.

Due to the sharp drop in share prices, equity valuations have fallen across the board. As a result, emerging market equities now look increasingly attractive from a valuation perspective. Our proprietary valuation composite for emerging markets, which includes price-to-earnings, price-to-book and price-to-cash flow ratios, as well as dividend yield, is currently significantly below its long-term average and is also cheap relative to global equities (Exhibit 15).

What are the potential catalysts to watch that could help to close this valuation discount in 2023?

The Fed pausing

The Fed, and the other large central banks in Europe, are determined to slow growth to ease inflationary pressures. Rising interest rates, increasing energy and input costs, and changing consumer patterns (from goods to services) are already slowing down demand for goods and hampering global manufacturing. North-east Asian markets, with their high export dependency, have been hit hard in the past couple of quarters as manufacturing purchasing managers’ indices have fallen and earnings expectations have been revised down. In Taiwan and Korea, the highly significant semiconductor industry was at the centre of the storm as a combination of weakening demand, higher capacity and US restrictions on Chinese exports added to the overall economic headwinds.

Given our base case macro outlook of a modest recession in the US and Europe, and retreating inflation in 2023, we expect the Fed to stop increasing rates early in 2023. In such a scenario, cyclical stocks, such as those in the technology sector, and cyclical markets, such as Korea and Taiwan (which have also derated), would find a much more favourable environment, since equity markets are usually forward-looking and look ahead to price in an economic recovery.

2. The end of the zero-Covid policy in China

Beijing has stuck to a restrictive lockdown policy through much of 2022, with serious consequences for economic growth. Consumption growth remains subdued, weighing particularly on the services sector. Meanwhile the struggling property sector has limited room to improve as home buyer sentiment remains depressed by uncertainty over future incomes.

However, policymakers introduced an easing of Covid control measures in November which re-ignited confidence that China is moving incrementally towards an ending of its zero-Covid policy. While an announcement of a complete end to Covid measures does not look imminent, even a roadmap for gradual easing could provide the catalyst for a strong recovery in Chinese demand, which would be beneficial for not only for China but also for all its major trading partners in the region.

3. Abating political risk

Emerging markets were also hit hard by an escalation of political risk in 2022. Russian equities (3.6% of the MSCI Emerging Markets Index at the beginning of 2022) became un-investable following the Russia-Ukraine war and the subsequent international sanctions imposed on Russia. In addition, a tightening of regulations in China and growing Sino-American tensions contributed to the decline in Chinese equities.

While political outcomes are hard to predict, investors need to acknowledge that abating political risks are a possible outcome in 2023. The Chinese economy is highly dependent on global demand, and global consumers are highly dependent on Chinese production (Exhibit 16). As a result, there are significant economic incentives for both sides to remain on good terms.

For attractively valued emerging markets to shine in 2023, at least one of these three featured catalysts need to occur. We strongly believe that central banks will be less restrictive in 2023, but certain political outcomes, such as the end of China’s zero-Covid policy, or a cessation of hostilities in Ukraine, remain very uncertain.

Therefore, while the significant valuation contraction in the past year has made emerging markets an attractive choice for cyclical exposure in portfolios, investors should continue to acknowledge that some risks are likely to linger.

Sticking with sustainability

2022 has been a very challenging year for all investors, but there have arguably been additional headwinds for those with a sustainable tilt. The strong performance of oil and gas companies has led many sustainably tilted strategies – particularly those that apply blanket exclusion policies – to underperform benchmarks, while the growth tilt of renewable technology stocks has also been problematic in a year where surging bond yields prompted a broad-based growth sell off.

A closer look under the surface of the equity market helps to track how sentiment has ebbed and flowed. Fossil fuel companies have been the major beneficiary of high commodity prices, outperforming global stocks by more than 50% in the first 10 months of 2022. Sustainably focused strategies that tilt away from the traditional energy sector are therefore likely laggards. Performance across the broader renewable energy sector has been more nuanced, with a sharp sell-off at the start of the year as bond yields rose followed by a turnaround that began with the RussiaUkraine war. Strategies linked to hydrogen stocks have suffered much more, with several of the most popular funds down more than 40% from January to October 2022 given their acute sensitivity to rising bond yields (Exhibit 17).

Despite these near-term difficulties, we see many reasons why it would be a mistake for investors to shy away from reflecting sustainability considerations in portfolios.

In Europe, the energy crisis has forced governments to prioritise energy security in the short term, with coal demand set to reach new record highs in 2022, and oil and gas companies delivering strong profits growth as prices surged. Yet these events must not obscure the bigger picture. To reduce dependency on Russian fuel while also meeting climate objectives, Europe needs to reshape how it sources and uses energy, and fast.

An accelerated rollout of lower priced renewable projects is the only medium-term solution, with associated earnings tailwinds for energy companies that can scale up their renewable capacity. Clean energy investment is accelerating in response, with the International Energy Agency expecting at least USD 1.4 trillion in new investment in 2022 and the sector now accounting for almost three quarters of the growth in overall energy investment. The European Union’s (EU’s) REPowerEU plan allocates nearly EUR 300 billion in investment by 2030 to help reduce the bloc’s dependence on Russian fossil fuels. The US is also joining the party, with the Inflation Reduction Act including tax credits and other financial incentives aimed at making clean energy more accessible.

Fears around windfall taxes – not just for energy companies but also for electricity providers – may be one reason why this earnings optimism has not been fully reflected in prices so far. Clearly it is not socially acceptable to allow utility companies to reap large windfall profits from surging electricity prices in the midst of a cost-of-living crisis. Yet given the need for governments to encourage investment as part of the energy transition, we would expect any impact of windfall taxes on renewable providers to be far less than for traditional energy companies. If the marginal cost of electricity is eventually de-linked from the natural gas price – as the EU and UK are examining – then renewables providers would probably fall out of scope of such taxes too.

Changes in the broader macro environment could also be more conducive for sustainable equity strategies in 2023. After a historic sell-off in the bond market, our base case sees moderating inflation leading to more stable bond yields next year. This should help to reduce the pressure on companies pushing for technological breakthroughs who have a much greater proportion of their earnings assumed to be further in the future (and are therefore much more sensitive to changes in discount rates).

Sustainably minded investors should not only look to equity markets next year – we also expect green bond markets to see significant development. With governments and corporates across Europe looking to raise capital to tackle environmental challenges, there is no shortage of projects that could be financed via greater green bond issuance. Issuers in these markets benefit not only from strong demand that can help to drive down yields (Exhibit 18) relative to traditional bond counterparts, but also an investor base that is tilted towards more stable lenders of capital than conventional syndications.

While the prospect of greater issuance is rarely something to cheer for bond investors, this activity should go a long way to addressing one of the green bond market’s key deficiencies: the lack of a “green yield curve” that makes manoeuvring portfolios in this universe more challenging. As the green bond market matures, an expanded opportunity set that offers greater flexibility will be a major requirement. The key for investors will be to scrutinise covenants for measurable and specific targets, and ensure that proceeds make a material difference to the ability of the issuer to deliver their green, social or sustainable project.

In sum, many investors will end 2022 feeling battered and bruised and, unlike in recent years, a sustainable tilt is unlikely to have helped to boost portfolio resilience. Yet we believe it would be short-sighted to shun the sustainable agenda as a result. Policy tailwinds look set to combine with improved valuations and a more conducive macro backdrop, creating investment opportunities that are too exciting to ignore.

Central projections and risks

Our core scenario sees developed markets falling into a mild recession in 2023 on the back of tighter financial conditions, less supportive fiscal policy in the US, geopolitical uncertainties and the loss of purchasing power for households. Despite remaining above central banks’ targets, inflation should start to moderate as the economy slows, the labour market weakens, supply chain pressures continue to ease and Europe manages to diversify its energy supply. However, we remain in an unusual environment, and it’s as important as ever to keep an eye on the risks to our central view, as they are skewed to the downside.

Please check in again with us shortly for further relevant content and news.

Please see below, an article from Brewin Dolphin regarding the performance of global stock markets over the past week. Received late yesterday afternoon – 22/11/2022.

Stocks mixed as UK chancellor hikes taxes

Stock markets gave a mixed performance last week as investors digested a slew of tax hikes in the UK and signs of an economic slowdown in the US.

The FTSE 100 ended the week up 0.9% after data showed UK retail sales bounced back in October. Germany’s Dax gained 1.5% as a survey showed investors became less pessimistic for a second month in row in November.

In contrast, US stocks fell last week following mixed economic data. Whereas US retail sales were above forecasts, a gauge of manufacturing fell to its lowest level since May 2020. The S&P 500 lost 0.7% and the Nasdaq declined 1.6%.

In Asia, Japan’s Nikkei 225 slid 1.3% as core consumer price inflation rose to a 40-year high and gross domestic product (GDP) unexpectedly contracted in the third quarter. China’s Shanghai Composite added 0.3% after a meeting between Chinese president Xi Jinping and US president Joe Biden helped to boost sentiment despite a rise in Covid-19 cases.

Last week’s market performance*

• FTSE 100: +0.92%

• S&P 500: -0.69%

• Dow: -0.01%

• Nasdaq: -1.57%

• Dax: +1.46%

• Hang Seng: +3.85%

• Shanghai Composite: +0.32%

• Nikkei: -1.29%

* Data from close on Friday 11 November to close of business on Friday 18 November.

China reports first Covid deaths since April

Stocks started this week in the red on concerns China could implement further lockdowns after reporting its first Covid-related deaths since April. In Beijing, where cases have hit a fresh record high, business and schools in the most affected districts have been shut and there are tighter rules for entering the city. The FTSE 100 slipped 0.1% on Monday (21 November) while the S&P 500, Shanghai Composite and Dax all lost 0.4%. Oil prices also declined as analysts warned lockdowns could dampen demand.

The FTSE 100 was up 0.7% at the start of trading on Tuesday after Saudi Arabia denied reports that OPEC was considering an increase in oil production.

Hunt confirms tax increases

Last Thursday saw UK chancellor Jeremy Hunt deliver his autumn statement, in which he confirmed a range of tax increases and spending cuts to help narrow the gap between the government’s income and outgoings and demonstrate fiscal responsibility to the markets.

The raft of tax hikes included slashing the capital gains tax exemption, dividend allowance and additional-rate income tax threshold, and extending the freeze on the personal allowance, higher-rate income tax threshold and inheritance tax nil-rate band. Hunt also announced that public spending would rise by just 1% a year in real terms in the next parliament. The energy price cap will increase from April 2023, meaning the average household will see their bills rise from £2,500 to £3,000 a year.

The autumn statement was accompanied by the Office for Budget Responsibility’s economic and fiscal outlook, which warned that a squeeze on real incomes, rise in interest rates and fall in house prices would see the economy fall into a year-long recession from the third quarter of 2022. GDP is forecast to contract by 1.4% in 2023 before rising by 1.3% in 2024 as energy prices and inflation fall.

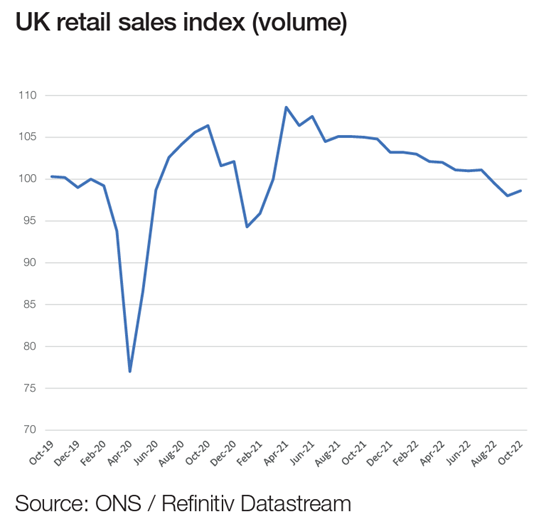

UK retail sales rise in October

More positively, data published on Friday showed UK retail sales bounced back in October, with volumes up 0.6% from the previous month, according to the Office for National Statistics (ONS). This was double the 0.3% increase forecast by economists in a Reuters poll. It followed a 1.5% decline in September, when sales were impacted by the bank holiday for the funeral of HM Queen Elizabeth II.

Sales in the three months to October were 2.4% lower than the previous quarter, suggesting the rising cost of living is resulting in consumers reining in their spending. Sales were also 0.6% below their pre-pandemic February 2020 level, yet shoppers spent 14.2% more as a result of high inflation.

Earlier in the week, the ONS’s consumer price index (CPI) report showed UK inflation rose to a 41-year high of 11.1% in October, up from 10.1% in September, mainly due to increases in energy bills and food prices.

US economic data mixed

US retail sales figures were also published last week and were well above consensus expectations. Sales rose by 1.3% in October from the previous month, the biggest gain since May. The increase was led by car sales and higher petrol prices (US retail sales are based on receipts as opposed to volume). Even when volatile car sales and petrol prices were excluded, sales were up 0.9% on the previous month.

Conversely, industrial production in the US decreased by 0.1% in October, as a slight gain in manufacturing output was offset by weaker mining and utilities production. A gauge of manufacturing in the mid-Atlantic region also worsened. The Federal Reserve Bank of Philadelphia’s current activity index dropped from -8.7 in October to -19.4 in November, the lowest reading since the early months of the pandemic.

Japan core inflation hits 40-year high

Over in Japan, core inflation (excluding fresh food prices) hit a 40-year high in October as a weak yen pushed up the cost of imported commodities. Prices rose at an annual rate of 3.6% in October, up from 3.0% in September. Unlike other central banks, the Bank of Japan (BoJ) is sticking with its policy of ultra-low interest rates. The BoJ’s governor, Haruhiko Kuroda, reiterated the bank’s pledge to maintaining monetary stimulus to achieve wage growth and sustainable and stable inflation.

Separate figures from the Cabinet Office showed Japan’s GDP fell by an annualised 1.2% in the three months to the end of September. Again, this was largely due to external factors. Imports grew by 5.2% from the previous quarter as higher energy costs and the weak yen drove up the prices of products coming to Japan, whereas exports grew by just 1.9%. The steep rise in imports meant net exports declined, which dragged GDP lower.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below the daily investment bulletin from Brooks Macdonald, which looks at the US Midterm Elections and expectations regarding today’s (10/11/2022) US CPI report. Received this morning – 10/11/2022.

What has happened

US equities struggled yesterday after a solid run of gains, with the headline US index down over 2% on the day. European equities posted small losses with sentiment boosted by news that Russian troops were withdrawing from the Ukrainian city of Kherson.

Midterm elections

With the midterm elections significantly closer than many commentators had expected, the last remaining states will determine the victors in the House of Representatives and the Senate. Electoral models still suggest that the Republicans will take the House but by a far smaller margin than previously expected. Within the Senate, one of the remaining seats is Georgia, where no candidate received the 50% needed to avoid a run-off race which will now take place on 6th December. Should the other remaining two Senate seats be split between the two parties, the Georgia race will determine control of the Senate, as it did in 2020. With Republican Ron DeSantis one of the strong performers of the midterms, speculation is building that he will announce shortly that he will run for President in 2024.

US CPI

Later today will see the release of the US CPI report which remains the most important of the monthly data releases. The report last month catalysed a broad sell-off in risk assets as core CPI surpassed economist expectations. This month the market is expecting a 0.6% month-on-month gain in the headline CPI report which would bring the year-on-year number down to 8% from 8.2%. The core month-on-month number is expected to ease slightly, coming in at 0.5%, which would bring the year-on-year figure to 6.5% rather than 6.6%.

What does Brooks Macdonald think

The importance of today’s CPI report is clear, with bond investors looking for signals as to whether US inflation has peaked and is starting to plateau. Before the next Federal Reserve meeting we have today’s release and one in December, therefore today’s report will have less of a direct follow through to Fed policy than previous months. That said, market pricing will rapidly incorporate the latest change in US price pressures, although investors should be cautious of extrapolating today’s datapoint too far into the future given the uncertainty and volatility of US inflation in 2022 so far.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below, an article from Brewin Dolphin regarding global trends in interest rates and their current and potential impact on economic growth and the markets. Received late yesterday afternoon – 01/11/2022.

Hopes rise of more moderate rate hikes

North American and European markets rose last week amid prospects that interest rate rises to tackle inflation may not be as steep as previously predicted, but a different story emerged from Asia.

Reports that the Fed may moderate its rate rises buoyed US markets, with some encouragement north of the border from Canada. The Bank of Canada increased its rates by a less-than-expected 50 basis points to 3.75%.

This was seen as a sign that central banks are stepping back from overly aggressive rate rises, increasing expectations that the Fed would follow suit or at least signal a slowdown when it meets this week. Markets are predicting a 75 basis points rise.

In the UK, gilt markets and Sterling reacted positively to the appointment of Rishi Sunak as prime minister and the FTSE 100 broke back through the 7,000 barrier, ending the week up 1.12% at 7,047.67.

Even the STOXX Europe 600 seems to have got a Sunak boost, rising 3.65% last week.

In contrast, Asian markets have lagged over the week, both in terms of performance and monetary policy.

Last week’s market performance*

• FTSE 100: 1.12%

• S&P 500: 3.95%

• Dow: 5.72%

• NASDAQ: 2.24%

• Dax: 4.03%

• Hang Seng: -8.32%

• Shanghai Composite: -4.05%

• Nikkei 225: 0.80%

• STOXX Europe: 3.65%

US markets rise off back of mixed data

US consumer confidence in the country dipped during October to 102.5, from 107.8 in September after two months of gains. Jobless claims rose from 214,000 to 217,000 while pending home sales of single-family homes plunged by more than 10% in September and mortgage rates rose to a two-decade high of 7.16%.

On the positive side, US GDP rose 2.6% annually during the third quarter, ahead of expectations for a 2.4% increase. It was the first boost to GDP for six months.

However, durable goods orders – seen as a proxy for investment activity – contracted in September and the latest US purchasing managers’ index (PMI) points to weaker private sector demand.

US markets lifted off the back of the mixed data. The S&P 500 ended the week up 3.95% and the Dow Jones was up 5.72%. Meanwhile, the Nasdaq managed to overcome poor technology earnings to finish last week up 2.24%.

Alphabet and Microsoft reported lower than expected third-quarter earnings, while Facebook owner Meta signalled that it would lose more cash next year as it continues to invest in creating the metaverse.

UK and European markets get ready for Rishi

The UK’s blue-chip index received a boost last week as the appointment of former chancellor Rishi Sunak as prime minister – replacing Liz Truss – suggested a return to greater political and economic stability in the country.

Mortgage rates – which rose to average highs of 6% off the back of Truss and ex-chancellor Kwasi Kwarteng’s much-maligned mini-budget – fell during the week, while markets are now expecting the Bank of England’s next interest rate hike to be 75 basis points or less.

At one point recently it looked as though that the increase may need to be around 150 basis points to curb rising inflation. However, UK interest rates are now expected to peak at below 5% in 2023, down from as high as 6.3% just after the mini-budget.

The much-anticipated Autumn Statement, originally scheduled for 31 October, was delayed until 17 November. That doesn’t necessarily bring an end to the UK’s corporate and economic woes though.

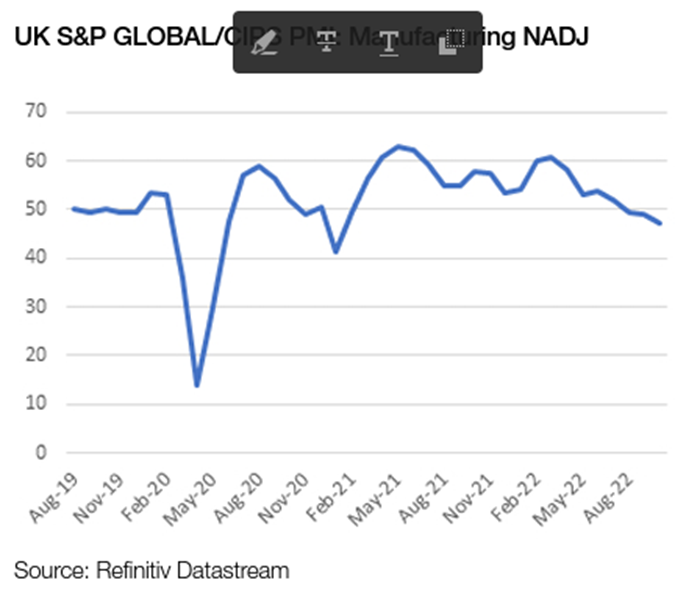

Data from the S&P Global/CIPS UK Composite PMI showed activity in the services and manufacturing sectors fell from 49.1 in September to 47.2 in October, below analyst expectations of a 48 reading. Manufacturing PMI hit a 29-month low of 45.8, while the services sector was also at a new low of 47.5.

The CBI’s latest quarterly survey found business sentiment has reached the lowest level since April 2020 at -48. The monthly net balance of manufacturers that expected prices to rise over the next three months fell from +59 to +46 between September and October – the lowest reading since September 2021.

ECB raises rates as expected

The European Central Bank increased interest rates as expected by 75 basis points to 1.5% – the highest since 2009. ECB President Christine Lagarde told reporters that “we will have further increases in the future,” adding that it might well be the case at “several meetings.”

Despite this, business activity still declined across the Eurozone in October. Its services purchasing managers’ index fell to 48.2 in October, down from 48.8 in September, hitting a 20-month low. The manufacturing PMI also fell to a 29-month low from 48.4 in September to 46.6 in October.

European natural gas prices also fell, helped by warmer weather and traders reducing reliance of supplies from Russia amid its invasion of Ukraine.

Bucking the trend

Unlike other financial policymakers, the Bank of Japan last week held interest rates at record low levels of -0.10. The central bank said it would continue to purchase as many Japanese government bonds as necessary, at a fixed rate, to keep 10-year bond yields at its 0% target.

While its manufacturing and services PMI data remained above the positive 50 reading, suggesting that growth continues, both consumer prices and the unemployment rate were up – at 3.5% and 2.6% respectively – above analyst expectations. The Nikkei 225 ended the week almost flat at 0.80%.

The economic growth news coming out of China was better than expected, with gross domestic product (GDP) data showing 3.9% annualised growth during the third quarter, up from just 0.4% in the previous period.

The next three months may be more uncertain though, as rising Covid-19 cases in the People’s Republic have led to lockdowns in several areas of the country.

Corporate data was already looking precarious with retail sales coming in at 2.5%, missing forecasts of a 3.3% rise.

China’s National Bureau of Statistics also reported a 2.3% annual fall in industrial profits for the first nine months of 2022, with manufacturing companies down 13.2%.

Amid these declines and new Covid-19 uncertainty, the Shanghai Composite closed the week down 4.05%. There was also a big outflow from Chinese equities amid the latest Communist Party Congress, which contributed to Hong Kong’s Hang Seng index falling 8.32% last week.

President Xi further cemented power by removing his premier Li Keqiang, historically a supporter of economic reforms. The next premier will not be announced until the National People’s Congress in March but it is expected to be Li Qiang, chief of the Chinese Communist Party (CCP) in Shanghai.

This may further hit market confidence as he doesn’t have any central government experience and was criticised for his management of a two-month lockdown in Shanghai earlier this year.

However, Chinese stocks rallied on Tuesday amid social media speculation that a committee is being formed to reduce stringent lockdowns and exit the country’s zero Covid strategy. The yuan strengthened and the Hang Seng Tech Index jumped as much as 9.3%.

* Data from close on Friday 21 October to close of business on Friday 28 October

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see the below article from Brewin Dolphin, highlighting the economic impact of the government U-turn on freezing corporation tax, and the effect this is having on markets. Received late Friday afternoon – 14/10/2022.

Prime minister Liz Truss has reversed the decision to scrap the planned rise in corporation tax. Guy Foster, our Chief Strategist, discusses the impact this could have on financial markets.

Prime minister Liz Truss has announced a second major mini-budget U-turn and the departure of chancellor Kwasi Kwarteng following weeks of market and economic turmoil.

Plans to scrap next year’s increase in corporation tax will no longer go ahead and the role of chancellor has now been filled by former health secretary Jeremy Hunt. Chris Philp is no longer chief secretary to the Treasury and has been replaced by Edward Argar, former paymaster general.

Background

Today’s statement comes after the mini-budget on 23 September resulted in a steep decline in UK government bonds (gilts) and the pound, widespread stock market volatility, and lenders pulling mortgage deals from the market. The mini-budget included a much bigger package of tax cuts than had been expected, raising concerns about a surge in government borrowing and more aggressive interest rate hikes. According to the Institute for Fiscal Studies (IFS), the tax cuts would have cost the Treasury almost £45bn a year1 , contributing towards an £80bn increase in borrowing by 2026/27.

One of the biggest measures in the mini-budget was scrapping the planned increase in corporation tax from 19% to 25%. Today’s U-turn means the increase will now go ahead in April 2023, saving the government around £18bn a year, Truss said.

The government had already announced on 3 October that it was scrapping plans to axe additional-rate income tax. Removing the 45% tax rate would have cost about £2bn a year according to the government, or £6bn a year according to IFS estimates.

How are markets reacting?

Bond and share prices rose ahead of Truss’s statement as speculation about the corporation tax U-turn mounted. There were large swings in the value of the pound as traders digested the sacking and replacement of the UK chancellor.

The market’s reaction was somewhat tempered by the fact that a tax cut U-turn had been widely anticipated. Borrowing costs have, however, fallen this week as speculation continued to mount.

Today’s stock market rally came in the context of markets which were higher globally as the news was announced. This largely reflected a strong performance on Wall Street following the latest US inflation figures. Speculation about the return of the corporation tax hike did cause some volatility among companies with particularly significant UK operations, such as banks, housebuilders and some retailers, who are now facing higher tax bills.

What is the longer-term outlook?

Speculation about the U-turn had already seen UK borrowing costs fall and the new chancellor will be aware of the need to emphasise fiscal sustainability as many of his predecessors were too. It would not be surprising to see the return of self-imposed fiscal rules, which serve as guard rails to keep policy on track, and which give investors a sense of how policy will develop. These form part of the economic orthodoxy that had been shunned by this government, despite being seen as an essential policy signal by previous governments.

The latest period of turbulence could worry investors that one benign economic strategy can quickly be replaced by another they find more alarming. However, it should also reassure them that it demonstrates how the government of the day is accountable to its party, the electorate, and the Office for Budget Responsibility. An independent Bank of England will support the financial system without interfering with policy. And these institutional protections mean that change can be forced to retain the confidence of the markets. That is not true of all countries and should enable the UK to quickly regain investors’ confidence.

This is a turbulent time for the government, and we expect further changes to be announced today by our new chancellor.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.