Please see below the weekly market commentary from Brooks Macdonald – received 17/08/2020

Weekly Market Commentary | US focus shifts to presidential race as tensions with China ease

17 August 2020

Read detailed economic and market news from our in-house research team.

Weekly Market Commentary

COVID-19 updates

By Edward Park

US indices stop just short of all-time highs

Fiscal stimulus in the US is delayed as Congress’s focus moves to the presidential race

US/China Phase One talks postponed, easing fears of an imminent escalation

US indices stop just short of all-time highs

US indices have stubbornly stayed below their all-time high as delays to the US stimulus package dampened a more buoyant mood. Last week saw a steepening of bond curves globally which implies expectations of stronger inflation, and therefore higher rates, down the line.

Fiscal stimulus in the US is delayed as Congress’s focus moves to the presidential race

With the Democratic and Republican nominating conventions taking place over the next two weeks, markets will need to push back their hopes for a US fiscal stimulus package. This delay means unemployed Americans now see a significant fall in the federal support they receive as part of the COVID-19 relief measures. Given this is around 10% of the US workforce1, this may have a sizeable impact on consumer confidence and demand. This delay will likely put even greater focus on monetary policy in the short term. This week we have the publication of The Federal Open Market Committee (FOMC) minutes for July, where markets will be looking for any discussion on average inflation targeting by the US Federal Reserve. If inflation was taken as an average (rather than a single target), this would allow the central bank to let the economy inflate in the short term without immediately needing to curb monetary policy. However, if fiscal policy is delayed, the market will start to expect further proactive monetary stimulus from the US in lieu of targeted fiscal measures such as unemployment relief.

US/China Phase One talks postponed, easing fears of an imminent escalation

Investors were expecting a call between US and Chinese officials to discuss the Phase One trade deal this weekend. This did not transpire which has helped reduce fears of an imminent escalation between the two sides. This week however will focus on the US election, with the Democratic convention starting today. The main event will be Joe Biden’s speech on Thursday which is of major importance given his current lead over President Trump. Any specific comments around minimum wages, fiscal stimulus, healthcare reform and taxation will be closely watched.

With earnings season slowing, this week is likely to be predominantly driven by US politics as the presidential race increases in pace and US/China tensions remain in the background. US viral cases continue to slow but European countries have stepped up restrictions as governments seek to curb the spread across the continent.

The weekly market commentary articles are useful in providing a quick update regarding recent events from around the world.

Please continue to check back for our regular blog posts and updates.

Please see article below from Legal & General’s asset allocation team – received 10/08/2020.

Legal & General Asset Allocation team’s key beliefs

American Express

This week, we take a tour of the United States – taking in the election, the economy, and the risk outlook for markets.

As with all Key Beliefs emails, this email represents solely the investment views of LGIM’s Asset Allocation team.

Biden: his time?

US presidential elections rarely lack drama, but it’s hard to recall one being carried out in such unusual circumstances as this year’s campaign. A few weeks ago it looked as good as it gets for Democratic candidate Joe Biden following months of terrible headlines for President Donald Trump, with polls and betting odds shifting in Biden’s favour. But then the polls stabilised and it seemed Trump was at his polling floor, making it difficult for Biden to gain more voters. With the potential for the news flow to normalise as new virus cases peak, the risks are skewed towards a tightening race.

The betting odds have barely moved, with the market average still giving Biden a 60% chance of winning. But polls have seen more movement, with Biden’s lead falling from an average of nine points to six over the past month. A few more polls in this direction and the narrative could escalate, pricing out some of the risk of a Democratic sweep.

The next major development is likely to be Biden’s pick for vice president. Betting markets suggest the contest is between Senator Kamala Harris and former national security advisor Susan Rice, with Senator Elizabeth Warren the only potentially market-moving – but low probability – option.

The focus then turns to party conventions over the second half of August. It remains to be seen how these translate as virtual events, how the press will cover them, and how voters will respond. Historically, a convention has given candidates a bump in the polls; they are likely to have a smaller effect than normal this time, but remain a wildcard, nonetheless.

Loan Concern

The US Senior Loan Officer (SLO) survey released last Monday night showed aggressive tightening across all categories, and by almost as much as during the financial crisis. The SLO survey has historically been a key metric for our economists in tracking bank lending standards, but how relevant is it this time round?

Lending standards tightened 2.8 standard deviations, not far away from the peak tightening of 3.4 standard deviations in October 2008. The tightening was broad based across all categories, with demand also weak for all loan types except mortgages.

But comparisons with 2008 are perhaps unfounded. Thanks to unprecedented support for corporate borrowers, strong bond sales have so far more than offset weak issuance of rated bank loans, meaning we are unlikely to see similar levels of bankruptcy, in our view – at least among companies with access to bond markets.

The key question is whether this tightening is bad news for the future or merely reflects a terrible second quarter. On the optimistic side, auto sales were not far from normal in July despite a huge apparent tightening in auto credit and very weak demand in this survey, while forward-looking housing market indicators look strong despite the tightening in mortgage credit availability in the second quarter.

The tightening nevertheless raises the risk that, without further large fiscal support, there will be economic scarring from bankruptcies as borrowers are not able to roll over loans. At a minimum, it is inconsistent with our most optimistic scenario which now will require some reversal of this tightening for the economy to return to trend growth by the end of next year. Employment data have also been mixed, with Friday’s non-farm payrolls just beating expectations following weaker PMI and ADP prints.

Risk Waiting

Last week saw us close out two of our more defensive tactical positions – long US Treasuries and short equities – following a cluster of near-term risks that appear not to have played out. New virus cases have slowed both in states that re-imposed harsh restrictions and those that did not, making further shutdowns less likely in the short term. Although we are seeing potential second waves in a number of other countries, nothing is spinning dramatically out of control, and vaccine news has added to a more positive tone of late.

In addition, incoming economic data last week had the potential to change the market’s assessment of what’s possible for growth over the next year, but have not proved to be a catalyst. And finally, concerns about US/China relations have so far failed to ignite. The South China Sea announcement came and went, while the forced sale of TikTok also seems unlikely to escalate tensions further.

This is not to say that all is rosy. Donald Trump may yet choose to fan the flames of Chinese resentment as an election tactic, while vaccine hopes and virus containment measures may not live up to the hype. As mentioned in previous editions of Key Beliefs, we now prefer to express our caution via selling investment-grade credit given the more stretched market positioning in that asset class.

A useful article from Legal & General’s Asset Allocation team on the United States election, the economy and the risk outlook for markets.

Please continue to check back for our latest updates and blog posts.

In the ever changing world that we live in, we recognise the importance of regular and current communication. This weekly news update provides you with a short summary of events around the world which we hope you will find useful.

UK COMMENTARY

The UK Manufacturing Purchasing Managers’ Index (PMI) for July was revised down slightly to 53.3 from initial estimates, with numbers supported by an increasing domestic demand. The survey of members also showed increasing confidence, with 62% expecting production to be higher in 12 months’ time, whilst only 12% forecast a contraction.

The latest Services PMI number came in strongly at 56.5, up from 47.1 in June, moving back in to expansion territory.

The Bank of England keep interest rates on hold at 0.1%, commenting that they expect the economy will shrink by a fifth and unemployment will double by the end of the year as the furlough scheme unwinds.

US COMMENTARY

Tensions between the US and China continue to escalate as President Trump announces a US ban on video-sharing, social networking service TikTok and multi-purpose messaging service WeChat.

The US jobs market appears to stall, with private payrolls adding only 167,000 jobs in July, against expectations of 1mln new jobs.

Weekly jobless numbers are, however, stronger than expected with first-time jobless claims falling by 249,000 to 1.2mln, ahead of expectations of over 1.4mln. Overall unemployment numbers also fell to 10.2% from 11.1% in June.

ASIA COMMENTARY

China PMI is reported at 52.8, ahead of consensus and further support for the existence of a strong economic recovery.

China’s exports were up 7.2% year-on-year after rising just 0.5% in June, with support from the textiles and electronics industries, not simply medical supplies which had dominated export numbers recently.

COVID-19 COMMENTARY

A rapid saliva-based COVID-19 antigen test in development by Avacta Group and Cytiva will receive clinical validation testing by the Liverpool School of Tropical Medicine.

Another useful article from Blackfinch Asset Management highlighting key events from around the world.

Please continue to check back for our latest blog posts and updates.

Please see Active Minds article below from Jupiter Asset Management – received 06/08/2020

Summer warmth turns chilly for UK equities

In contrast to the warm, sunny weather in the UK at the moment, the UK equity market feels quite chilly and unloved in a global context, said Dan Nickols, Head of Strategy, UK Small & Mid Cap. The S&P 500 Index in the US is now up year-to date, while FTSE All-Share Index is down over 20% and the Numis Smaller Companies Plus AIM ex Investment Companies Index of UK small and mid-caps is down almost 18%.1

The reason why the UK has been so weak compared to other markets is partly compositional, as it contains fewer technology names, more financials, and more discretionary consumer stocks. Dan believes there is another layer too: the ongoing Brexit drama means that, for overseas investors, the UK can simply be filed under ‘too difficult’ and ignored for now in favour of other equity markets.

With an eye on the future, Dan is looking at real-time data around things such as credit card transactions, which indicate there was a good recovery until the end of June that then showed signs of slowing in July. Dan also highlighted a risk off unemployment picking up in the coming months, as the furlough scheme tapers off into a weak economy, bringing the importance of judicious stock and sector selection into sharp relief.

All of the above creates a challenging environment for UK equity investors. Dan highlighted that, in the UK small and mid-cap world, leadership in the market from a style perspective is very stark, as value continues to struggle badly while momentum, growth and revision factors remain relatively strong. Dan and the team are trying to navigate this by being purposefully overweight structural growth names, while tempering that with some exposure to what they believe are well-managed, conservatively financed stocks that are more geared into economic growth – although they have pared these back over the last few weeks, while retaining exposure to the stocks in which the team have highest conviction.

Large-cap tech stocks drive emerging markets

Emerging markets had a pretty good July, with the MSCI Emerging Markets Index finishing the month up around 3% (in sterling terms), noted Colin Croft, Fund Manager, Emerging Markets. Year to date, the index is almost flat, which is quite remarkable given the state of the global economy, said Colin.2 However, gains have been concentrated in a fairly narrow set of large-cap tech stocks, which now represent significant weightings in the index. These stocks are up significantly year to date, almost entirely driven by re-ratings, rather than seeing much in the way of earnings upgrades.

It is impossible to predict what the trigger could be for a change in the relative rating of these kinds of stocks. However, Colin suspects that as soon as there’s some sort of light at the end of the tunnel in terms of the pandemic, investors will want to take profits in these kinds of ‘haven’ stocks that have become so expensive, and could instead choose to move into stocks with more leverage to the recovery. It’s likely to be a bumpy road to get there though – for example, sentiment for recovery-dependent sectors such as financials and travel has been badly affected by a pickup in cases in countries that were previously looking much more encouraging, such as Spain and Australia. Elsewhere, the outbreak in Latin America shows no signs of abating – instead, it is plateauing at high levels.

Fortunately, there are some structural themes playing out that are more or less independent of the pandemic, highlighted Colin. One of these is the likely positive impact of the 5G rollout; another is the gas pipe reform we’re seeing in China. The latter has been under discussion for years, but finally some progress was made over the past month or so. Pipelines there were owned by the big three majors, which were also producers; however, now China is injecting all the pipe assets into a national company, which will then allocate the capacity in a strategic manner. Colin noted that this is happening on terms that have been surprisingly favourable to investors: they’re being injected at 1.2x or 1.4x book value; they’re also getting 40% cash payments for it, not just shares; and there’s talk about paying special dividends too.

Tech in the time of coronavirus

The significant impact of technology across various sectors has been one key positive theme accelerated by the pandemic, says Makeem Asif, Fund Manager, Multi-Asset. Whether it is working from home, educating children online, retailers’ pivoting to online distribution or the need for more cybersecurity, the pandemic has led to a step change in the use of tech.

But, for Makeem and the global convertibles team, the biggest issue has been the valuation of some software companies where it is not unusual to see shares trade on 25x-40x revenues. In the semiconductor space, despite some initial supply chain disruptions, production in most factories in Asia is back on track. Earlier this week the semiconductor industry association published its monthly report which tracks sales and average selling prices of units. This highlighted how robust the semiconductor industry has been during the pandemic: in the twelve months to June, sales grew 7%, up from the 3% annual growth seen in May. The team expects chip sales to continue to rise driven by demand from data centres, autos, electric vehicles and other devices. In addition, says Makeem, such companies tend to have more reasonable valuations with good cashflow metrics.

In the fintech space, the hygiene requirements arising from the pandemic have acted as a catalyst to accelerate the uptake of digital payments with their clear advantage over cash. One of the dominant US card payment companies said it expected to reissue around 70% of its cards in the next 12-18 months. Although the switch to digital payments is not new, Makeem says there is still a significant amount of growth to come as some economies have been slow to adapt. Furthermore, there are still around 1.7 billion people worldwide who do not have a bank account.

1Source: FE, index returns in GBP to 31.07.2020 2Source: FE, index returns in GBP to 31.07.2020

Articles like this are useful for getting an insight to the market from market experts within their specified field.

The Coronavirus Pandemic has affected our lives in many different ways but as noted above a key positive theme has been the boost of the technology sector within the markets.

Please continue to check back for our latest blog posts and updates.

Please see below the latest market update article from Brewin Dolphin – received 04/08/2020.

Brewin Dolphin – Markets in a Minute – Equity markets mixed, gold and silver continue to rise

Global share markets were mixed last week, with China outperforming the rest of the world as its economic recovery continues. US indices were flat or marginally up thanks to some extraordinary results from the US tech giants, but equities in the UK and Europe have fallen on poor economic data, rising coronavirus cases and a “wall of worry” about the economic outlook later this year.

Bond yields broadly fell again with yields on US Treasuries hitting record lows, while gold and silver prices rose as investors looked for safe havens. Meanwhile, the US dollar suffered its worst month in 10 years against a basket of currencies.

A positive start to the week…

Markets started the new week with a rebound. Equities in the UK, Europe, US and Asia all pushed higher on Monday, as surveys of manufacturing businesses in the US, UK and Europe suggested that factory activity was increasing. The FTSE100 saw the largest daily increase, jumping by 2.3% on Monday, pushing back up through the 6,000 level to 6,032.85.

Virus developments

New cases appear to be slowing in the US, suggesting the pausing of re-openings and the mandated use of masks in many states may be working. It also saw a reduction in hospitalisations, and the fatality rate is now around 1.5% compared to 7% in April. This is probably because more young people are getting the virus while older people are taking more care to protect themselves, while treatments are also improving. All this helps reduce the chance of another national lockdown.

Unfortunately, after a period of falling cases, Europe is now seeing infection rates rise again, driven heavily, but not exclusively, by Spain (about 50%).

Japan has also seen a big rise and even China has seen a pick-up in new cases, albeit from a very low base. It demonstrates just how hard the virus is to completely suppress, but China is an example of how an economy can recover while managing localised outbreaks.

The news of two revolutionary new coronavirus testing kits that give results in 90 minutes will no doubt be a great help in containment efforts. Previous tests took two days.

What’s eating the dollar?

Even after falling so far last month, we suspect the trend remains weaker for the dollar. Despite the recent reduction in coronavirus cases it still seems as if Europe will do a better job of containment than the US, with governments generally prepared to impose local lockdown measures before things get out of hand.

Both regions have produced stimulus packages that are supporting growth, primarily consumption at the moment, which you might expect to be positive for the dollar. But it comes at the cost of an increased budget deficit (where government spending exceeds its revenues), and this will likely result in an increased current account deficit (where the value of its imports exceed the value of its exports). Both of these can weigh on the dollar.

Time is tight for US stimulus deal

The extra $600-a-week in unemployment payments announced as part of the original stimulus package in March, came to an end last week. Politicians are still deadlocked in negotiations about the details of a new stimulus bill, with Republicans wanting to cut the payments to $200 a week and Democrats wanting to keep payments unchanged.

All this while the employment crisis burns (as evidenced by another week of higher jobless claims). Even given the tight timeframe, with the Senate due to go into summer recess on 7 August, we still think a deal will be passed, even if it means having to push back the summer break. The alternative would be delaying until September which is an outcome that both parties would be keen to avoid.

Corporate news

Earnings season in the US has been producing the right kind of headlines. Around halfway through and nearly 85% of companies have beaten EPS estimates, ahead of the more usual 80%. Exactly two thirds of companies have reported better-than-expected sales levels. That is an improvement on most other years, when an average of 50% of firms exceeded sales expectations.

Last week saw updates from some of the big tech names. After announcing stellar results as beneficiaries of the new work and play at home environment, the combined market value of Facebook, Amazon, Apple and Google soared by $230bn in after-hours trading on Thursday, taking their total value to more than £5trn for the first time and lifting the S&P500 into positive territory for the week.

All that glitters…

The best play on a weaker dollar has been precious metals, and while the focus has centred on the gold price hitting record highs, silver has actually been the better performer of late, rising nearly 25% in July alone. We still think there is more upside because silver’s rebound has not yet fully reversed the historic divergence in the ratio between the price of the two metals, plus silver has additional demand for industrial uses.

Another good overview of the markets from Brewin Dolphin. Although markets started with a rebound this week, we are still experiencing high levels of volatility.

Please continue to check back for our latest blog posts and updates.

Please see article below from AJ Bell Youinvest received 30/07/2020

The growth of China’s consumer economy

The country could stoke domestic demand to become more self-reliant

Thursday 30 Jul 2020 Author: Tom Sieber

In the last decade or more the Chinese economy has undergone a significant transition as it moves away from an infrastructure-driven and export-reliant economy to one fired by domestic consumption.

This change can be tracked by looking at how the country’s current account surplus has moved to a deficit. Broadly speaking a current account surplus means an economy is exporting a greater value of goods and services than it is importing.

Having peaked in 2008 when China truly lived up to its reputation as ‘The World’s Factory’ the surplus has declined significantly.

There are several factors underpinning the growth of the consumer economy, one being a natural offshoot of the maturation of the Chinese economy. A larger Chinese middle class is more likely to have disposable income to spend on products and services at home.

In the short term at least, exports have been hit by the coronavirus crisis as demand has dried up and trade routes have been affected by lockdown restrictions. Chinese tourists who might have taken their renminbi overseas are also shopping domestically instead.

There are signs China wants to move further in this direction as it looks to become more self-reliant. This may reflect pressure on the country and its businesses from other countries concerned about its growing global influence, and about its recent actions in Hong Kong and in the immediate aftermath of the Covid-19 outbreak.

A report by the Chinese Academy of Social Sciences, a think tank closely affiliated to the state, suggests the next five-year policy plan – due for 2021 – should prioritise home-grown innovation and look to tap into a substantial domestic market.

Please continue to check back for our latest blog posts and updates.

Please see below the latest market update article from Brewin Dolphin – received 28/07/2020.

Markets in a Minute: Equity markets lose ground as investors seek safe havens28 . 07 . 2020

Global share markets struggled to hold on to recent gains over the past week as tensions between the US and China escalated, with tit-for-tat consulate closures in Houston and Chengdu. There were also signs that the rebound in the US economy was waning, with initial jobless claims rising for the first time since March. Increasing coronavirus cases in numerous countries added to worries.

Bond yields fell, the gold price hit a record high as investors looked for safe havens and the US dollar fell to its lowest level for two years when compared to a basket of other currencies.

Last week’s markets performance*

FTSE100: -2.64%

Dow Jones: -0.75%

S&P500: -0.3%

Dax: -0.63%

Hang Seng: -1.5%

Shanghai Composite: -0.54%

*Data for the week to close of business on Friday 24 July.

Holiday chaos

Markets started the week cautiously yesterday. Asian shares were mixed, the US rose, but equities in the UK and Europe lost ground. The FTSE100 closed down by 0.3%, and the Eurostoxx600 index also fell by 0.3%. Travel stocks shouldered the worst of the losses on the back of the government decision to impose a two-week quarantine on travellers returning from Spain. It had a knock-on effect as many travellers to other destinations cancelled their holidays fearing a similar last-minute change to the rules. But the UK was not alone; France also warned against citizens travelling to Catalonia, and said those returning from a list of 16 countries outside the EU would be subject to mandatory testing at the border on arrival.

Dollar woes

We have been calling a decline in the dollar for some time now and it has fallen against virtually everything over the past week, especially when compared to the euro which is continuing its strong run. Recent data suggests that the European economy is performing better than the US, and given European interest rates are negative, while they are still (just) in positive territory in America, investors perceive US rates have further to fall, putting downwards pressure on the dollar. The euro gained 0.95c yesterday to $1.17.81, above the $1.17 level for the first time since late 2018. The pound also strengthened 0.7% to $1.29.01.

Dollar exchange rates

Virus news

While global case numbers continue to rise, driven largely by emerging economies, there have been renewed spikes in numerous locations including Japan, Hong Kong, France, Canada, Germany and, of course, Spain. However, it is the progress of the virus and policy response in the US that will have the greatest impact on the global economy.

In that sense at least, there were hopeful signs in the US that new infections were peaking, and there are several factors which suggest that the economic impact of the virus in the coming months won’t be as severe as it has been in the past.

Firstly, the rise in cases is partly explained by the increase in testing. That means the headline case number is less worrying and it also means more people who know they are infected can self-isolate and be treated.

Hospitalisation rates have been lower and are falling. That means more minor cases are being identified and people are self-isolating, and it also suggests that high-risk groups are isolating to keep out of harm’s way. Additionally, those who are hospitalised are getting better faster. Treatments have improved and the ICU mortality rate has declined. All these factors suggest that repeating the total lockdowns seen earlier in the year is not a viable option.

Stimulus deadlock

While the EU eventually approved its €750bn recovery package after a marathon summit early last week, US Congress is still debating how to proceed. The Democrats approved a bill for $3trn in additional stimulus two months ago, including a proposal to keep paying the $600-a-week in extra unemployment benefits until the end of the year. The payments are due to expire this week.

Yesterday, however, the Republican-controlled Senate unveiled a $1trn plan that involves cutting the $600-a-week benefits to $200 in September, then setting unemployment benefits at a maximum of 70% of the claimants’ most recent salary. The idea is to make sure that nobody earns more for staying at home than they would going to work.

However, the Democrats said the plan fell far short of what was needed to ensure the US recovery stayed on track, and said the cut to benefits was a “slap in the face” for the 30m Americans relying on unemployment payments. The two parties are now negotiating a compromise.

Road to recovery

While recent economic data has generally been better than expected, that trend has been less pronounced in the UK than other regions. Although the initial purchasing managers’ indices for July show activity is improving, the data is only relative to the previous month and so does not really tell us a great deal other than things aren’t quite as bad as they were in June.

While the direction of travel is welcome, there’s every reason to expect the UK recovery to be slow as the job retention scheme is unwound over the coming months.

We compared the Office of Budgetary Responsibility (OBR) and US Congressional Budget Office (CBO) forecasts for UK and US GDP respectively. They anticipated that the US will reach its pre-COVID level of activity in 2021, a year ahead of the UK.

Brexit and trade deals

The current state of Brexit negotiations also implies a slower trajectory for the UK. Whilst opinions differ, the market views any frictions between the UK and EU as inhibiting UK economic activity. Last week the Telegraph reported that government insiders are resigned to the fact that they may be trading with the EU on WTO terms in 2021. The FT reported that the government are equally resigned to the fact that a trade deal with the US will not happen ahead of the US elections this year (and therefore will be pushed back to the next congressional session starting in the new year). The first of these stories is presumably part of the bargaining strategy and doesn’t necessarily change our view that a thin trade deal can be achieved later in the year, but will likely still mean some economic disruption. The second weakens the UK hand in further negotiations but is not a surprise given that the US has typically been a tough partner for smaller countries to negotiate with. Both scenarios present some headwinds which could add to volatility.

A good overview of the current market situation from Brewin Dolphin. High levels of volatility continue in the markets and the impacts of the virus are still being felt globally.

Please continue to check back for our latest blog posts and updates.

Please see article below from AJ Bell Youinvest on the potential capital gains tax hike – received 23/07/2020.

How to beat the potential capital gains tax hike

The tax system could soon change to help the Government raise money to cover some of its Covid-19 support efforts

Thursday 23 Jul 2020 Author: Laura Suter

Chancellor Rishi Sunak has signalled he is looking to shake up how capital gains tax (CGT) is paid, which could leave taxpayers with a higher tax bill.

Sunak has asked the Office for Tax Simplification to look at how CGT is structured, whether the tax can be simplified and if more help can be given to individuals in the administration of the tax.

While he doesn’t explicitly say so, many people assume that the timing of the review indicates the Chancellor could be looking at changing the tax as one way to raise money in order to pay for the Government’s cost of the current Covid-19 pandemic.

The Government has spent a large amount of money on helping the country to stay afloat during the current crisis and everyone expects this year’s Autumn Statement to reveal how it plans to pay for this support. While additional Government borrowing is one solution, tax hikes may also be on the agenda.

The review will look at the differences between the CGT system and the income tax system, how private residence relief works and the reliefs and exemptions on offer.

PUBLIC OPINION

The move might not be entirely unpopular with the British public. Research from AJ Bell showed that two thirds of people think we have a responsibility to contribute towards the cost of the recent measures.

When questioned, the most popular tax to increase was either dividend taxes or CGT, with 37% of respondents thinking it was acceptable to raise those taxes. This was followed by a third of people who said income tax and 22% who said inheritance tax.

WHAT COULD CHANGE?

Changing tax rates: One area that may change is the rates charged on CGT (see below for current rates). There is a big difference between the rates charged for income tax and CGT.

An additional rate taxpayer, for example, would pay 45% tax on any income they make over their personal allowance, but only 20% on their investment gains. One thing the Government could do is bring these rates in line with each other.

Cutting allowances: In a similar vein to above, individuals have a tax-free rate for their income and for their capital gains – currently £12,500 before income tax kicks in and £12,300 for CGT.

These allowances could be brought together, so someone only has one lot of £12,500, for example, before they incur tax. This would bring lots more people into the bracket of having to pay CGT.

Scrapping main home relief: At the moment you pay no CGT on the gains you make on your main home – in part this is offset by the fact that you have to pay stamp duty tax when you buy a new home.

However, one suggestion has been that the Government could remove or limit this relief. This would mean lots of people who had made a gain on their property would face a large tax bill, but in turn could raise a lot of money for the Government. It would be an odd move to make just as the Government has put in other measures to try to get the housing market moving.

HOW CAN YOU BEAT THE HIKE?

If you’re worried about any rise in the tax rates or cuts to allowances, you could think about locking in gains now. Remember, anything in an ISA or SIPP is exempt from CGT, so you don’t need to worry about those gains. But outside of these tax wrappers your investments could face CGT.

You can choose to cash in gains up to your annual allowance this year, in order to lock in some gains and make use of that allowance. If your gains are higher than your allowance, you could transfer assets to your spouse so they can use their allowance.

Transfers to spouses are exempt from CGT, but if they then sell the assets they’ll face CGT on any profit between the price you bought the investment and the price at which they are selling. If you transfer assets to them, they can then cash in the gains and use their annual allowance to avoid a large tax bill.

For example, let’s assume Mrs Smith has investments that have a £25,000 gain on them, and she is a higher-rate taxpayer. If she sold those investments in one tax year, she’d use her £12,300 allowance but still pay tax at 20% on the remaining £12,700 gain – which would equal a £2,540 tax bill.

However, if she transferred the investments with the remaining £12,700 gain on them to her husband, who is a basic-rate taxpayer, he could use his £12,300 tax free allowance – leaving just £400 of gains to pay tax on. At his lower 10% CGT rate this would mean a tax bill of just £40 – saving £2,500.

Another option is cashing in the gain and rebuying the asset in your ISA, assuming you have some of your annual ISA allowance remaining. This is called ‘bed and ISA’ and means you can use your annual allowance, keep hold of the investment and future gains will be exempt from CGT.

HOW DOES CAPITAL GAINS TAX WORK?

You pay capital gains tax on any profit you make when you sell an asset that has risen in value.

Some assets are tax free, including your main home. Everyone gets a tax-free allowance each year, which is currently £12,300 per person.

Beyond this level any gains are taxed depending on your income tax rate, so basic-rate taxpayers pay 10% (or 18% on property) while higher and additional-rate payers pay 20% (or 28% on property).

If you give money to your spouse you don’t have to pay CGT, nor on assets including land, property or shares you gift to charity. If you make a loss on an asset you can offset that against any gains you make on other assets in order to reduce your tax bill – and you can carry forward losses into future years.

A useful article covering the potential changes to capital gains tax and a breakdown of how capital gains tax works. The Government has spent a large amount of money on helping the country during the Coronavirus Pandemic and it will be interesting to see how the Government plans to pay for this support and what changes will be made.

Please continue to check back for our latest blog posts and updates.

Please see article below from Close Brothers Asset Management received 17/07/2020.

Looking at the path to recovery

SUMMARY

•Covid-19 has already dented global growth in 2020 • Having fallen initially, equity markets have recovered as investors take a long term view • Sovereign bond yields remain at or near historic lows across most developed markets • The efficacy of health policy will be key in determining how long the pandemic lasts – the effects of the pandemic on the economy are likely to be long lasting • The global economy may be less interconnected in years to come, due to changing supply chains, a larger role for fiscal and health policy and geopolitical tensions • Changes already underway have been accelerated by the pandemic – investors must identify the winners and losers in the post-pandemic world

INTRODUCTION

In the first quarter of 2020, the spread of Covid-19 around the world precipitated an unprecedented health emergency, forcing countries worldwide to respond quickly with dramatic measures to limit the spread of the virus. Stock markets initially plunged, as investors reacted to this sudden new threat to the global economy, while bond yields reached new lows, reflecting investor caution and the expectation of central bank monetary stimulus. At one point, the price of a barrel of oil turned negative, as low demand and a supply glut exhausted North American storage capacity. The world had seemingly been turned on its head in a matter of weeks.

In time, markets have recovered much ground, comforted by both governments and central banks stepping in to ease the immediate impact of the pandemic on consumers and businesses. The MSCI World Index, having fallen over 30% in February and March, was less than 10% below the pre-pandemic level at the end of June. Given the backdrop of an immediate global recession, and an uncertain path to recovery in 2021, such strong performance is hard to reconcile. Within bond markets, sovereign yields remain anchored, with the yield on a 10Y US treasury still well below 1%, suggesting a more pessimistic view of growth.

While investors have learned to stomach the immediate economic implications of Covid-19, what lies ahead is still somewhat unclear. Nonetheless, even in a time of such uncertainty, there are some conclusions investors could draw with a degree of confidence, many of which have clear and important implications for businesses.

LASTING SIDE-EFFECTS

The disruption caused by the pandemic may be with us for some time. The pandemic is not yet over. While the initial surge of the pandemic is behind us here in the UK and restrictions are easing, in parts of the US, Russia, India, Latin America and Africa, the spread of the virus is still accelerating (see figure 1). What is more, there are some signs of a “second wave” of the virus in some countries that have eased restrictions, resulting in social distancing being reintroduced.

Epidemiologists and health professions in general know much more about Covid-19 than they did at the start of 2020, but much is still unknown. Research into the virus is focussed on three key areas which will determine how long the pandemic lasts.

1. VACCINE The first focus for research is to find an effective vaccine – until an effective vaccine is found, Covid-19 will remain a health risk. The global health community has already started a coordinated research effort, with a number of potential avenues being explored. There are also funding programmes and agreements in place designed to ensure that access to a vaccine is fair, so as to avoid poorer countries being deprived of important health resources. However, developing, testing and distributing a vaccine will take time. Unlike medication that is given to those who are ill, a vaccine is given to someone who is well. An effective vaccine also needs to protect a person for a reasonably long time, not just a few weeks. All of this means that vaccine testing takes longer than other kinds of medication. With these facts in mind, and despite all the resources being committed, it is unlikely that a vaccine will be available in 2020.

2. TREATMENT A second area of research is that into treatments for people already suffering with Covid-19 symptoms. These treatments either seek to limit the virus’ ability to attack the body, or to limit the complications caused by the body’s own response to the virus. Such therapies may limit the severity of the illness the virus causes, saving lives and reducing strain on health services. So far, only limited progress has been made in this research area, mostly in terms of repurposing existing drugs that have been found to have some positive impact on Covid-19 patients. This means that, for now at least, the disease caused by the virus remains a serious concern.

3. TRANSMISSION The third research area is concerned with the transmission of the virus. What factors determine how easily the virus is spread? Which social distancing measures are most important in order to limit contagion?

How do we know who has the virus? While our understanding of how the virus spreads is improving, research in the area remains nascent. For now, policy makers have limited access to data assessing the effectiveness of various social distancing measures, though over time this will improve. As a result of this, it is possible that governments will have to test different policy measures before they are able to establish which are most effective. On the virus detection front, scientists are making some progress towards quicker and more accurate tests for the virus, which may help policy makers control the spread.

Given that a vaccine is unlikely to be available in 2020, the limited progress made in finding a therapy, and the limited data available to policy makers when evaluating social distancing programmes, it seems likely that the economic disruption caused by the pandemic will be long-lasting.

DESYNCHRONISATION IS COMING

The global economy may become less coordinated as a result of thepandemic The prevailing trend of the global economy over the last two decades has been one of globalisation – increasingly sophisticated and interconnected supply chains have allowed businesses to source materials and labour worldwide, and just-in-time production technology has eliminated the requirement for businesses to hold a large inventory. As a result of this, the global economy also became increasingly synchronised – monetary stimulus in China would ripple across the globe, impacting copper prices in Chile and hotel rates in Cherbourg.

The pandemic may cause a partial desynchronisation in the global economy for a number of reasons. Firstly, the experience of the pandemic has revealed the importance of supply chains being not only efficient, but also resilient. For strategically important goods, this is likely to lead to a partial re-shoring of production, reducing the supply chain’s vulnerability to shocks along the line. For other goods, it seems possible that nations may also shift some off-shore production from distant manufacturing hubs to a neighbouring country with appropriate manufacturing capacity. While this does not signal the end of globalisation, we may see some fragmentation in global trade and a period of disruption while supply chains are re-orientated.

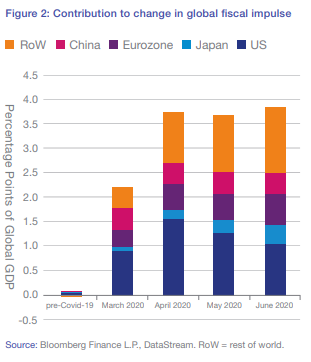

The second driver of desynchronisation is the greater importance of health and fiscal policies versus monetary policies. In the years since the financial crisis, monetary policy has been the dominant policy tool used to control the global economy, with governments in the world’s developed markets unenthusiastic, for the most part, about accommodative fiscal policy in the wake of a crisis. While monetary policy remains an important and powerful policy tool with a strong influence over the global economy, attitudes to fiscal policy have changed and government spending is likely to be higher in those economies that can afford it and those prepared to borrow further to fund it. While monetary policy has mostly washed through the global economy, especially that enacted by the US and China, the effect of fiscal policies may be more localised and heterogeneous, as the results will depend on the efficacy of the measures introduced, the scale of spending, and the sphere of focus (see figure 2 below).

Lastly, the stresses caused by the pandemic appear to have further stroked nationalist feeling in some of the world’s economies, exacerbating geopolitical tensions that were already simmering away. We see this especially in global relations with China, where tensions are rising on a number of fronts.

While we do not expect the age of globalisation to end altogether, it does seem possible that desynchronisation may cause greater dispersion in asset performance across geographical regions.

ACCELERATED CHANGE

The pandemic has accelerated a number of structural changes that were already in train. In the words of Vladimir Lenin, “There are decades where nothing happens; and there are weeks where decades happen.” For many of us, life has changed a lot since the beginning of the pandemic, in both large ways and small. These changes have knock-on implications for the economy and businesses. One such example of a trend accelerated by the pandemic is the wider adoption of working from home. The pandemic has forced many businesses to adjust working practices and put in place the necessary technology and procedures to allow employees to be as productive from home as they would be in the workplace. This makes remote working for some not only possible, but an attractive option. This is supportive for the industries that facilitate this approach to working. However, it is likely to cause disruption to other sectors of the economy – remote working is likely to weigh on the airline sector, especially those carriers more exposed to business travel, if companies do not adjust. Demand for housing may also change – space for a study may be more important than proximity to a railway line. For those sectors where remote working is not an option, the extra costs associated with providing a virus-safe working environment may shift the scales in favour of the wider adoption of automation.

While few of these trends are new, the pace of adoption appears to have been spurred by Covid-19. Businesses themselves may also be transformed for better or worse. New business practices may add costs for some companies, but may provide opportunities to increase efficiency for others. Indeed, some listed firms will emerge from the crisis slimmed down and more profitable than when they went in to lockdown.

POSITIONING PORTFOLIOS

Given what we know about the pandemic, what is the likely impact on asset prices? As we have discussed, we expect global growth to be much lower than usual this year, and this in turn will weigh on corporate earnings growth – with some companies already cutting dividend payments (earnings paid out to investors). Given the pace of research progress into a vaccine, treatments and limiting transmission, some of the effects of the pandemic will be long lasting, making it likely that the economic recovery takes longer.

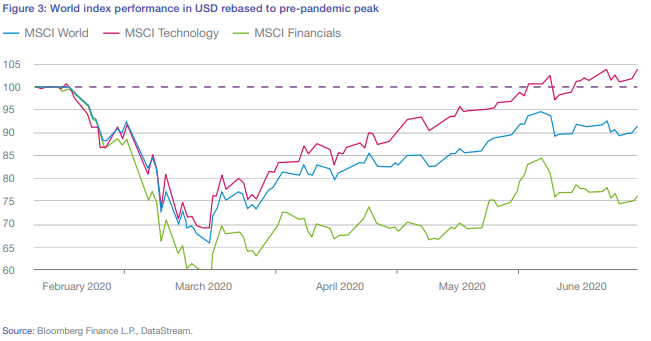

While growth may be depressed near term, shares are long term investments and current prices should theoretically reflect the present value of all future earnings, not just those in the next twelve months. On this basis, it is the structural changes accelerated by the pandemic that will likely have a more meaningful impact on asset prices. Asset prices certainly reflect this in some areas, with the global technology index outpacing the broader global index, and currently sitting above pre-pandemic levels (see figure 3 below).

In this environment, we believe that active management will be even more important. Investors must consider which health and fiscal policies are likely to be more favourable, and as a result, which regions will experience better outcomes. We must also consider which industries are best positioned and which businesses are best adapting to the realities of the post-pandemic world.

Within the bond market, the new outlook for global growth makes it likely that interest rates will remain at new lows for longer, which is generally supportive for bonds. However, the marked increase in government bond issuance is a potential source of concern. While central banks have committed to bond buying programmes, this appetite may not be unlimited. With government bond yields so low, further monetary accommodation may be required in order to eke out further price performance from these richly priced assets. Nonetheless, given the scope for shocks to the economy, bonds play an important role within multi-asset portfolios.

Across shares and corporate bonds, our research focus remains on businesses with ample working capital, as it is these businesses which we believe will be able to survive and thrive once immediate emergency support measures are withdrawn. At some point, social distancing measures will be lifted and growth will recover. Our priority now is establishing the right price for assets that will survive the here and now and will be attractive to hold in the longer term.

CONCLUSION

With the initial turmoil of this unprecedented health and economic emergency behind us, we are focussing on the longer term implications of Covid-19. We continue to closely monitor the evolution of the health data in order to better gauge the likely duration of this period of weak growth, and to analyse individual securities so that we may identify those with the greatest near term resilience and long term prospects.

A good insight from Close Brothers Asset Management.

The disruption cause by COVID-19 could be with us for some time yet. Whilst the initial surge of the pandemic is behind us here in the UK and some restrictions are easing, in parts of the US, Russia, India, Latin American and Africa, the spread of the virus is still accelerating with some signs of a ‘second wave’ of the virus in some of the countries that have eased restrictions. What lies ahead still remains somewhat unclear.

Please keep checking back for regular updates and blog posts.

Please see article below from J.P.Morgan’s weekly market update – received 13/07/2020.

The US presidential election will take place on 3 November 2020. The result will have important implications for investors, as the combination of policies employed by the next administration could have a significant influence on whether the US stock market can continue the outperformance that it has recorded for much of the last decade. Our regularly updated election insights provide investors with all they need to know as the election story evolves.

US election insight – July 2020

The race for the White House is heating up. Joe Biden and the Democrats have seen a surge in the polls in recent weeks, as the US experiences a wave of Covid-19 cases and against a backdrop of widespread protest against racial inequality and social justice issues. The Democrats are also making strong headway in the battle for the Senate, increasing the odds of a “blue wave” in November. The next key event will be the selection of Joe Biden’s running mate – a decision that takes on more significance this year than in a normal election campaign.

What will be voted on in November?

The race for the White House is the main focus, but a president’s ability to achieve their policy goals is influenced by who controls Congress.

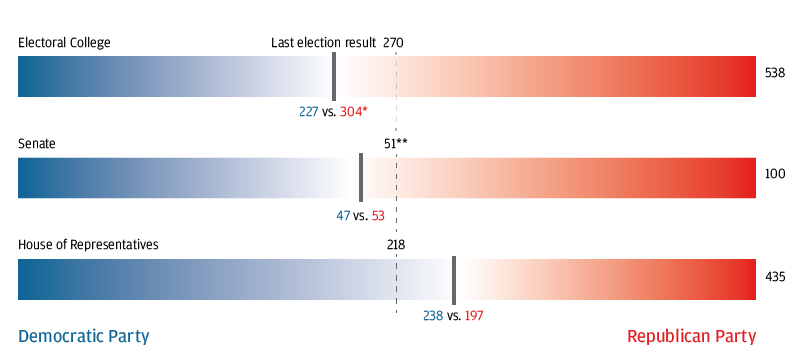

American voters will be asked to make three key decisions on 3 November. The main focus will clearly be on who wins the keys to the White House, but a president’s ability to achieve their policy goals is influenced by which parties control the two arms of Congress: the House of Representatives and the Senate. If Congress remains divided between the Democrats and the Republicans as it is today, the winner of November’s contest will rely heavily on unilateral action taken via executive orders and rulemakings through the federal government via the department and agencies that have significant power. Enacting larger policy proposals requires approval by Congress and the winner of the election will have a much tougher time enacting that part of their agenda. Exhibit 1 shows the numbers needed to win each race.

The electoral college

The presidential candidate that wins the most number of votes (or wins “the popular vote”) does not automatically become president. Instead, the US employs an electoral college system. Votes are tallied at a state level, and the winner in each state earns the “electoral votes” that belong to that state (with the number of electoral votes in each state determined by population size). A candidate needs to win at least 270 of the 538 electoral votes in order to win the presidency.

The Senate

US senators serve six-year terms, which means that roughly a third of the 100 Senate seats are up for grabs at each federal or mid-term election. Currently the Republicans control the Senate. There are 35 seats up for election this year – 23 currently held by Republicans and 12 currently held by Democrats. To win control of the Senate, the Democrats would need to keep all of their existing seats and flip three seats if they win the presidency, or four if they do not, as the vice president casts tie-breaking votes.

The House of Representatives

Each of the 435 seats in the House are up for election in November, with the winners serving a two-year term. Currently the Democrats control the House. For the Republicans to win back control, they would need to win 21 additional seats and hold on to two vacant seats that were previously held by Republicans.

Members of both the House and the Senate serve on a wide range of committees. The Senate has the authority to approve presidential nominations – such as Supreme Court justices and members of the Federal Reserve Board. Betting odds at the start of July put a Democratic sweep of the House and the Senate as the most likely by a significant margin.

Exhibit 1: Votes or seats in the Electoral College, the Senate and the House of Representatives

Source: 270 to Win, The Cook Political Report, J.P. Morgan Asset Management. *In 2016 Trump earned 306 pledged electors, Clinton 232. They lost, respectively, two and five votes to faithless electors in the official tally. **51 seats are needed for a simple majority if the dominant party in the Senate is not represented in the White House. If the president and majority party are the same, only 50 seats are needed for a majority because the vice president casts the tie-breaking vote. 2016 numbers include two independents that vote with the Democrats. Data as of 30 June 2020.

How might Covid-19 change the election timeline?

While Covid-19 has upended the usual schedule, election day itself is unlikely to shift given the need for Congress to approve any change.

The coronavirus outbreak has already had a significant impact on the primary season – the process by which Democratic and Republican presidential candidates are formally nominated. After state lockdowns began in earnest in mid-March, 16 states and one territory either postponed, cancelled or switched their primaries to vote-by-mail with extended deadlines. The Democratic National Convention, at which the Democratic candidate is officially nominated to represent the party in the presidential election, has been delayed by a month to 17-20 August, a week before the Republican National Convention.

While election day may well look very different to any other seen before in the US, the 3 November date is not likely to move. Presidential elections are set in federal law to take place on the Tuesday after the first Monday in November, and for this to be changed, approval from the Democrat-controlled House of Representatives would be required.

It appears that social distancing is highly likely to be required in some form and may threaten voter turnout, which is particularly important for the Democrats’ prospects given the distribution of the electoral college. Non-traditional voting methods have been rising in availability and popularity in recent years (see Exhibit 3), but Democratic proposals for further expansions in 2020 have so far been met with strong opposition by the Republicans.

Exhibit 3: States permitting different methods of alternative voting

Number of states

What are the investment implications?

Election years are on average characterised by lower returns and higher volatility, but market dynamics in 2020 will be dominated by the prevailing economic environment

Typically, returns are lower and volatility is higher in election years than in non-election years (see Exhibit 6), although these averages are significantly skewed by major recessions and market events in recent election years. Returns and volatility in 2020 will almost certainly be attributable to Covid-19, not the political campaigns quietly existing alongside it. While the election is still a few months away, there are three areas of focus that could materially impact investor sentiment over the summer.

1. Roadmap for the rebound Top priority for whoever leads the next US administration will be to manage the economy as it restarts in earnest in 2021. Government finances have been stretched by the vast fiscal packages approved so far and tough choices will need to be made about whether to push ahead with further stimulus, or to try to tighten the belt as the recovery gets underway. The Federal Reserve (the Fed) may come under increasing pressure to keep yields low, although if this pressure is so strong as to cause investors to question the Fed’s independence, there is a risk that longer-dated yields could be pushed higher.

2. US-China relations The US-China relationship is now back on a worrying path. The hit to both business confidence and investment intentions across the globe in 2019 highlighted the economic damage that was caused by the trade war. Actions from either country that ratchet up tensions further ahead of the November election are a clear catalyst for market volatility. While so far it has been a Republican administration in charge of the negotiations, further information from the Democrats about how they would propose to manage this relationship may also impact market sentiment.

3. Progressive policy proposals The most progressive policies moved out of the picture as the most progressive Democratic candidates exited the race. Yet it is still evident that Joe Biden’s vision for corporate America is clearly different to President Trump’s. Democratic proposals for the use of anti-trust legislation to clamp down on “Big Tech”, plans for corporate tax changes and how to shore up the healthcare system are all matters that warrant close attention.

The combination of policies employed by the next administration will be an important factor in determining whether the US stock market’s leadership over much of the past decade will continue. An environment of escalating trade tensions has favoured the higher-quality US stock market relative to other regions historically, although we recognise that an increase in regulatory pressure on the tech titans could pose risks to US market leadership given the high weights to technology and communication services sectors in US indices. We will be tracking developments closely as 3 November approaches.

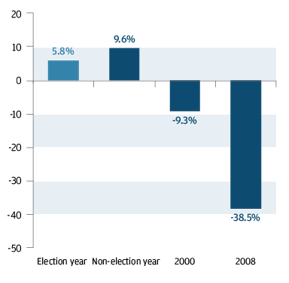

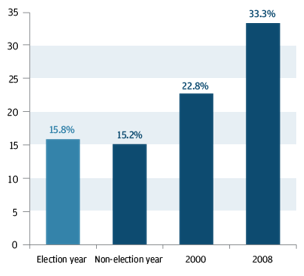

Exhibit 6: S&P 500 price returns Percent, average return from 1932 – 2019

S&P 500 realised volatility Percent, 52-week standard deviation of price returns, 1932-2019

As the US is one of the largest most influential markets globally, what happens next from a political point of view is important to the global economy.

Please keep checking back for regular updates and blog posts.