Please see article below from Close Brothers Asset Management received 17/07/2020.

Looking at the path to recovery

SUMMARY

•Covid-19 has already dented global growth in 2020

• Having fallen initially, equity markets have recovered as investors take a long term view

• Sovereign bond yields remain at or near historic lows across most developed markets

• The efficacy of health policy will be key in determining how long the pandemic lasts – the effects of the pandemic on the economy are likely to be long lasting

• The global economy may be less interconnected in years to come, due to changing supply chains, a larger role for fiscal and health policy and geopolitical tensions

• Changes already underway have been accelerated by the pandemic – investors must identify the winners and losers in the post-pandemic world

INTRODUCTION

In the first quarter of 2020, the spread of Covid-19 around the world precipitated an unprecedented health emergency, forcing countries worldwide to respond quickly with dramatic measures to limit the spread of the virus. Stock markets initially plunged, as investors reacted to this sudden new threat to the global economy, while bond yields reached new lows, reflecting investor caution and the expectation of central bank monetary stimulus. At one point, the price of a barrel of oil turned negative, as low demand and a supply glut exhausted North American storage capacity. The world had seemingly been turned on its head in a matter of weeks.

In time, markets have recovered much ground, comforted by both governments and central banks stepping in to ease the immediate impact of the pandemic on consumers and businesses. The MSCI World Index, having fallen over 30% in February and March, was less than 10% below the pre-pandemic level at the end of June. Given the backdrop of an immediate global recession, and an uncertain path to recovery in 2021, such strong performance is hard to reconcile. Within bond markets, sovereign yields remain anchored, with the yield on a 10Y US treasury still well below 1%, suggesting a more pessimistic view of growth.

While investors have learned to stomach the immediate economic implications of Covid-19, what lies ahead is still somewhat unclear. Nonetheless, even in a time of such uncertainty, there are some conclusions investors could draw with a degree of confidence, many of which have clear and important implications for businesses.

LASTING SIDE-EFFECTS

The disruption caused by the pandemic may be with us for some time.

The pandemic is not yet over. While the initial surge of the pandemic is behind us here in the UK and restrictions are easing, in parts of the US, Russia, India, Latin America and Africa, the spread of the virus is still accelerating (see figure 1). What is more, there are some signs of a “second wave” of the virus in some countries that have eased restrictions, resulting in social distancing being reintroduced.

Epidemiologists and health professions in general know much more about Covid-19 than they did at the start of 2020, but much is still unknown. Research into the virus is focussed on three key areas which will determine how long the pandemic lasts.

1. VACCINE

The first focus for research is to find an effective vaccine – until an effective vaccine is found, Covid-19 will remain a health risk. The global health community has already started a coordinated research effort, with a number of potential avenues being explored. There are also funding programmes and agreements in place designed to ensure that access to a vaccine is fair, so as to avoid poorer countries being deprived of important health resources. However, developing, testing and distributing a vaccine will take time. Unlike medication that is given to those who are ill, a vaccine is given to someone who is well. An effective vaccine also needs to protect a person for a reasonably long time, not just a few weeks. All of this means that vaccine testing takes longer than other kinds of medication. With these facts in mind, and despite all the resources being committed, it is unlikely that a vaccine will be available in 2020.

2. TREATMENT

A second area of research is that into treatments for people already suffering with Covid-19 symptoms. These treatments either seek to limit the virus’ ability to attack the body, or to limit the complications caused by the body’s own response to the virus. Such therapies may limit the severity of the illness the virus causes, saving lives and reducing strain on health services. So far, only limited progress has been made in this research area, mostly in terms of repurposing existing drugs that have been found to have some positive impact on Covid-19 patients. This means that, for now at least, the disease caused by the virus remains a serious concern.

3. TRANSMISSION

The third research area is concerned with the transmission of the virus. What factors determine how easily the virus is spread? Which social distancing measures are most important in order to limit contagion?

How do we know who has the virus? While our understanding of how the virus spreads is improving, research in the area remains nascent. For now, policy makers have limited access to data assessing the effectiveness of various social distancing measures, though over time this will improve. As a result of this, it is possible that governments will have to test different policy measures before they are able to establish which are most effective. On the virus detection front, scientists are making some progress towards quicker and more accurate tests for the virus, which may help policy makers control the spread.

Given that a vaccine is unlikely to be available in 2020, the limited progress made in finding a therapy, and the limited data available to policy makers when evaluating social distancing programmes, it seems likely that the economic disruption caused by the pandemic will be long-lasting.

DESYNCHRONISATION IS COMING

The global economy may become less coordinated as a result of the pandemic

The prevailing trend of the global economy over the last two decades has been one of globalisation – increasingly sophisticated and interconnected supply chains have allowed businesses to source materials and labour worldwide, and just-in-time production technology has eliminated the requirement for businesses to hold a large inventory. As a result of this, the global economy also became increasingly synchronised – monetary stimulus in China would ripple across the globe, impacting copper prices in Chile and hotel rates in Cherbourg.

The pandemic may cause a partial desynchronisation in the global economy for a number of reasons. Firstly, the experience of the pandemic has revealed the importance of supply chains being not only efficient, but also resilient. For strategically important goods, this is likely to lead to a partial re-shoring of production, reducing the supply chain’s vulnerability to shocks along the line. For other goods, it seems possible that nations may also shift some off-shore production from distant manufacturing hubs to a neighbouring country with appropriate manufacturing capacity. While this does not signal the end of globalisation, we may see some fragmentation in global trade and a period of disruption while supply chains are re-orientated.

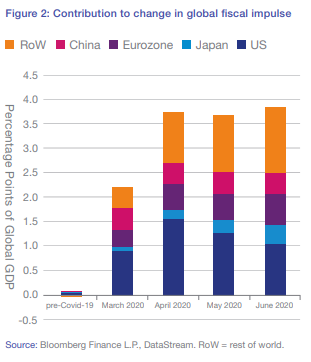

The second driver of desynchronisation is the greater importance of health and fiscal policies versus monetary policies. In the years since the financial crisis, monetary policy has been the dominant policy tool used to control the global economy, with governments in the world’s developed markets unenthusiastic, for the most part, about accommodative fiscal policy in the wake of a crisis. While monetary policy remains an important and powerful policy tool with a strong influence over the global economy, attitudes to fiscal policy have changed and government spending is likely to be higher in those economies that can afford it and those prepared to borrow further to fund it. While monetary policy has mostly washed through the global economy, especially that enacted by the US and China, the effect of fiscal policies may be more localised and heterogeneous, as the results will depend on the efficacy of the measures introduced, the scale of spending, and the sphere of focus (see figure 2 below).

Lastly, the stresses caused by the pandemic appear to have further stroked nationalist feeling in some of the world’s economies, exacerbating geopolitical tensions that were already simmering away. We see this especially in global relations with China, where tensions are rising on a number of fronts.

While we do not expect the age of globalisation to end altogether, it does seem possible that desynchronisation may cause greater dispersion in asset performance across geographical regions.

ACCELERATED CHANGE

The pandemic has accelerated a number of structural changes that were already in train. In the words of Vladimir Lenin, “There are decades where nothing happens; and there are weeks where decades happen.” For many of us, life has changed a lot since the beginning of the pandemic, in both large ways and small. These changes have knock-on implications for the economy and businesses. One such example of a trend accelerated by the pandemic is the wider adoption of working from home. The pandemic has forced many businesses to adjust working practices and put in place the necessary technology and procedures to allow employees to be as productive from home as they would be in the workplace. This makes remote working for some not only possible, but an attractive option. This is supportive for the industries that facilitate this approach to working. However, it is likely to cause disruption to other sectors of the economy – remote working is likely to weigh on the airline sector, especially those carriers more exposed to business travel, if companies do not adjust. Demand for housing may also change – space for a study may be more important than proximity to a railway line. For those sectors where remote working is not an option, the extra costs associated with providing a virus-safe working environment may shift the scales in favour of the wider adoption of automation.

While few of these trends are new, the pace of adoption appears to have been spurred by Covid-19. Businesses themselves may also be transformed for better or worse. New business practices may add costs for some companies, but may provide opportunities to increase efficiency for others. Indeed, some listed firms will emerge from the crisis slimmed down and more profitable than when they went in to lockdown.

POSITIONING PORTFOLIOS

Given what we know about the pandemic, what is the likely impact on asset prices? As we have discussed, we expect global growth to be much lower than usual this year, and this in turn will weigh on corporate earnings growth – with some companies already cutting dividend payments (earnings paid out to investors). Given the pace of research progress into a vaccine, treatments and limiting transmission, some of the effects of the pandemic will be long lasting, making it likely that the economic recovery takes longer.

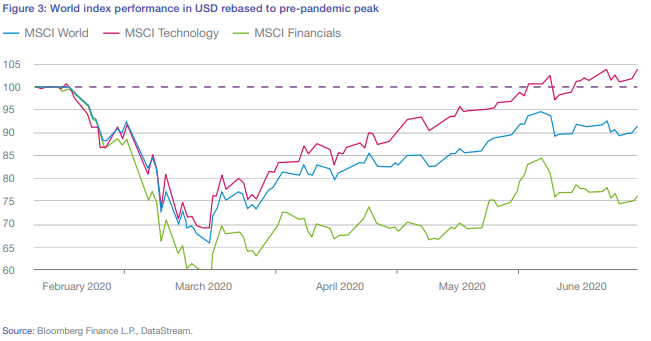

While growth may be depressed near term, shares are long term investments and current prices should theoretically reflect the present value of all future earnings, not just those in the next twelve months. On this basis, it is the structural changes accelerated by the pandemic that will likely have a more meaningful impact on asset prices. Asset prices certainly reflect this in some areas, with the global technology index outpacing the broader global index, and currently sitting above pre-pandemic levels (see figure 3 below).

In this environment, we believe that active management will be even more important. Investors must consider which health and fiscal policies are likely to be more favourable, and as a result, which regions will experience better outcomes. We must also consider which industries are best positioned and which businesses are best adapting to the realities of the post-pandemic world.

Within the bond market, the new outlook for global growth makes it likely that interest rates will remain at new lows for longer, which is generally supportive for bonds. However, the marked increase in government bond issuance is a potential source of concern. While central banks have committed to bond buying programmes, this appetite may not be unlimited. With government bond yields so low, further monetary accommodation may be required in order to eke out further price performance from these richly priced assets. Nonetheless, given the scope for shocks to the economy, bonds play an important role within multi-asset portfolios.

Across shares and corporate bonds, our research focus remains on businesses with ample working capital, as it is these businesses which we believe will be able to survive and thrive once immediate emergency support measures are withdrawn. At some point, social distancing measures will be lifted and growth will recover. Our priority now is establishing the right price for assets that will survive the here and now and will be attractive to hold in the longer term.

CONCLUSION

With the initial turmoil of this unprecedented health and economic emergency behind us, we are focussing on the longer term implications of Covid-19. We continue to closely monitor the evolution of the health data in order to better gauge the likely duration of this period of weak growth, and to analyse individual securities so that we may identify those with the greatest near term resilience and long term prospects.

A good insight from Close Brothers Asset Management.

The disruption cause by COVID-19 could be with us for some time yet. Whilst the initial surge of the pandemic is behind us here in the UK and some restrictions are easing, in parts of the US, Russia, India, Latin American and Africa, the spread of the virus is still accelerating with some signs of a ‘second wave’ of the virus in some of the countries that have eased restrictions. What lies ahead still remains somewhat unclear.

Please keep checking back for regular updates and blog posts.

Charlotte Ennis

17/07/2020