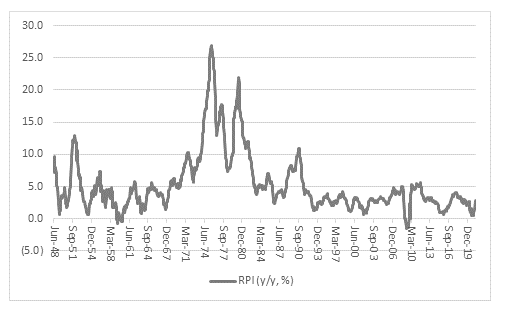

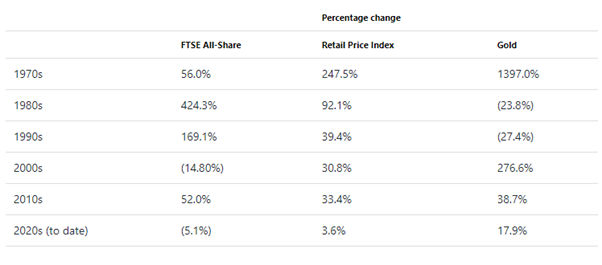

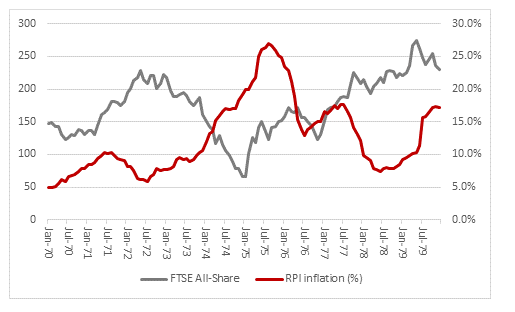

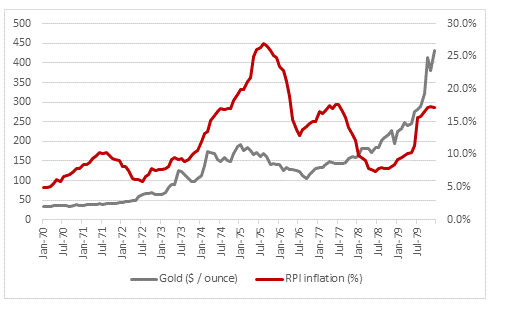

Please see below article received from Legal & General yesterday afternoon, which offers insightful analogies relating to inflation and current global market performance.

When two people jump on a trampoline simultaneously, their gravitational potential energy (what goes up must come down) is converted into elastic potential energy in the trampoline (what goes down must come up). If one of the participants (the bouncer) lifts up their legs at the point of maximum trampoline stretch, all the energy is transferred to the other participant (the bouncee). This launches the bouncee into the air much more emphatically than a single person could achieve by themselves. If the bouncer is a lot heavier than the bouncee, then the results can be spectacular. This phenomenon makes us think of inflation today.

Trampolines and inflation

In this analogy, the pandemic is the bouncer and prices are the bouncee. Historically, prices that fall hard have had little tendency to revert. As former Crystal Palace manager Iain Dowie might have put it, there normally isn’t much “bouncebackability”.

But prices have been emphatically “double bounced” in recent months: the pandemic exerted incredibly unusual downward pressures as demands for hotels, restaurants and airlines collapsed. That stretched the trampoline elastic to its limits. Suddenly removing the pressure has catapulted prices higher, with a slew of indicators pointing to near-term inflation taking off.

Having been double bounced, the question is whether inflation will stay high. It is tempting to believe high prices will stay high forever, but financial markets seem to be buying into the Crystal Palace prognosis. Dowie’s comments were triggered by the team bouncing back into the Premier League in the 2003-04 season from a seemingly dire position in mid-November. However, they were relegated again the following season.

Similarly, the US inflation curve is inverted: after a bout of higher inflation over the next few years, markets are priced for a return to something more normal thereafter. Sinkbackability is the flipside of bouncebackability.

The post-recession equity playbook

If you were worried about equity valuations before, are you a little less worried now? Since mid-April, the S&P 500’s forward price-to-earnings (P/E) ratio is down by over a point. At 21.3x we can’t exactly call it cheap, but it reflects an encouraging trend and one we expect to continue for some time. Put another way, the forward earnings yield has increased by around 0.2%.

In a benign de-rating, share prices are up, but by less than earnings; P/E ratios decline as a result. Since mid-April, the S&P 500 is up marginally, but the next 12 months’ forecast earnings are up by 7%.

We’re not just seeing this picture in the US, either. Estimates of forward earnings are upby 5.5% in Europe, and 8% for the DAX; even the less-cyclical FTSE 100 has seen forward earnings estimates rise by 3.5%.

This is a normal pattern after recessions, so not entirely unexpected. But it’s noteworthy that it has started, because until now it had been missing from this cycle.

In Phase 1 after a recession, prices typically go up a lot more than earnings, in anticipation of the earnings rebound. That would be the P/E expansion we had last year. In Phase 2, that picture reverses and earnings go up by more than prices, so P/E ratios contract. That’s what we’re seeing now.

The S&P 500 grinding higher with headline valuations drifting lower is the general pattern we expect to see over the next year. We are therefore relatively relaxed about high P/E ratios today, with a lot of earnings growth likely to be ahead. If we were to be at these same multiples this time next year, we would be a lot more worried.

A tinker, not a taper

Have US interest rates been rising or falling recently? It seems like a straightforward question with a straightforward answer. The first quarter was the fifth-worst quarter for US Treasuries in the past three decades, as 10-year yields rose by nearly 90 basis points. Every market commentator under the sun is now talking about a “rising interest rate environment” and what that means for other asset prices. But, did you know that US money-market rates have just fallen to all-time lows?

That seems a symptom of a superabundance of cash looking for a home in short-dated securities. The Federal Reserve is hosing the financial system with money and there simply isn’t enough short-dated government debt to go around.

Does any of this matter for assets outside the money-market space? We can think of two implications.

First, the dollar’s been weak at the same time as the short end of the yield curve has been collapsing since March this year. The Bank of England’s Jan Vlieghe has signalled a possible rate hike in the UK as early as May next year, we had a similar nod from New Zealand last week, and the rates payable on emerging currencies have started to drift higher. As long as the Federal Reserve refuses to even “think about thinking about” raising rates, it’s hard to see the dollar trend turn around.

Second, we’ve seen general collateral and triparty repo rates nailed to the floor in recent months, down from +10 basis points at the end of last year. That’s not a huge change, but it makes it that little bit cheaper to fund long-duration positions or more expensive to fund short-duration positions. We are tactically short duration, but the emphasis is on ‘tactically’, given the carry costs (which are getting steadily worse) and positioning.

To ‘fix’ the problem, we expect the Federal Reserve to push up its administered rates at the next opportunity in June. Precedent for tinkering with the Interest On Excess Reserves (IOER) can be found in both June 2018 and January 2020. The trick this time will be to persuade the markets that this adjustment is not a tightening of monetary policy. A tinker, not a taper, will be the order of the day.

We will continue to publish relevant content as we edge towards ‘Freedom Day’ on the 21st of June.

Stay safe.

Chloe

02/06/2021