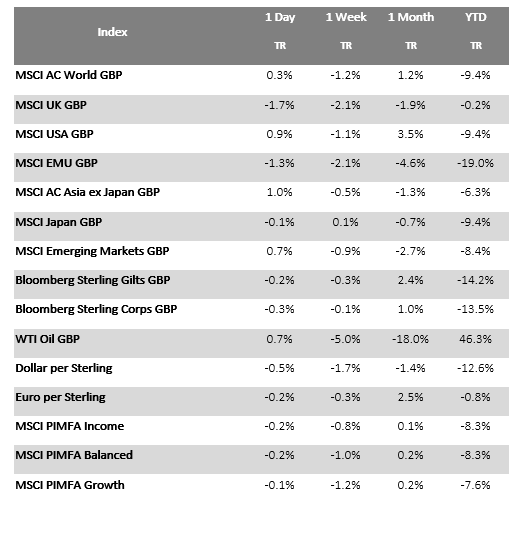

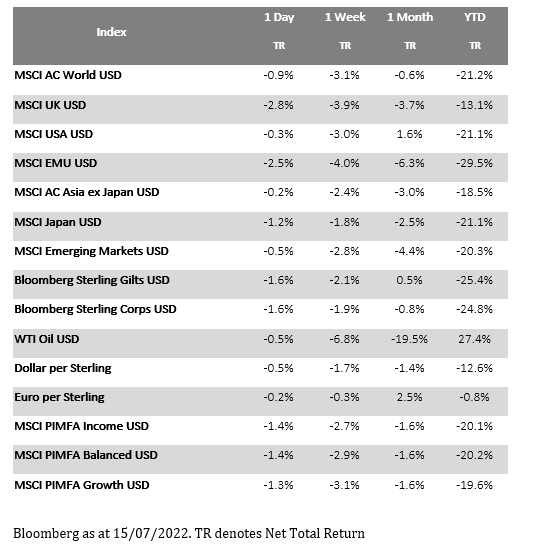

Please find below, a Daily Investment Bulletin received from Brooks Macdonald, this morning – 15/07/2022

What has happened

Risk appetite remained supressed yesterday as bank earnings and recessionary fears combined into another poor day for equity markets. JPMorgan yesterday missed expectations and Morgan Stanley saw investment banking revenue halve compared to the previous year. Q2 earnings will be a key determinant of whether the market concludes that the year-to-date falls adequately compensate for the expected deterioration of margins over the short to medium term.

Federal Reserve

With the US CPI report causing investors to reappraise the near term path for US interest rates, ‘Fed speak’ is being scrutinised to gauge the chances of a 100bp hike. The Fed will enter their communication blackout window on Saturday so yesterday’s comments are one of the last tests of Governor sentiment that the bond market has to work with. Governor Waller yesterday said that the CPI beat earlier in the week justified another 75bp rate hike however he was open to a larger hike if economic data was stronger than expected. President Bullard meanwhile also supported a 75bp hike, with the result that markets reduced their expectations for a 100bp hike. The 2-year US Treasury yield gave back some of its recent rise, trading at 3.11% at the time of writing. US technology stocks were a particular beneficiary of this reduction in rate expectations, managing to secure a small gain yesterday even as the broader US market sold off.

Italy

European political risk returned to the fore yesterday as Prime Minister Mario Draghi attempted to resign after the Five Star Movement refused to back his government in a confidence vote. Draghi said that ‘The loyalty agreement that was the foundation of my government has gone missing.’ With President Mattarella declining the resignation, the Italian political backdrop is uncertain with a fresh round of elections possible. Italy has been facing a large number of economic and political challenges since COVID, as reflected in the spread between German bond yields and Italian yields. Yesterday saw that spread widen to its largest level in over a month.

What does Brooks Macdonald think?

Adding to the concerns of a global slowdown, overnight China released their Q2 GDP data which showed that the economy contracted on a quarter-on-quarter basis. China continues to struggle in applying the zero COVID policy to the latest Omicron led surge and this slowdown may well prompt Beijing to provide further economic support to ensure that the economy does not stall over the summer.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

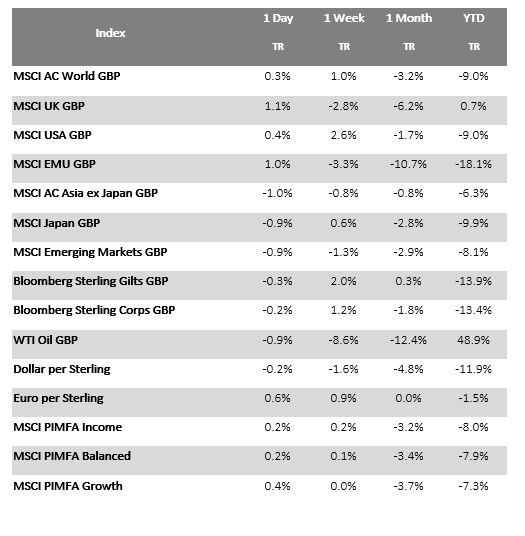

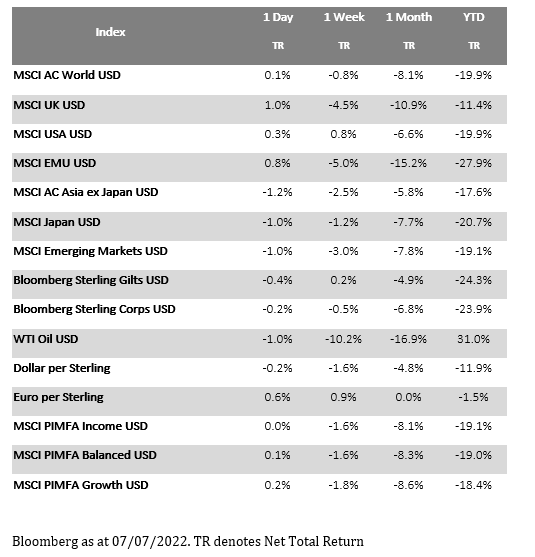

Please find below, a Daily Investment Bulletin received from Brooks Macdonald this morning – 07/07/2022

What has happened

Despite fairly dire economic sentiment, equities made gains yesterday with European equities outperforming as they caught up on the late US rally on Tuesday night. Below the surface, investors continue to rachet up their probabilities of a recession with commodity prices falling and the US 10-year Treasury yield remaining below the 2-year yield, a historical precursor to recessions.

Boris Johnson

This paragraph has needed to be rewritten several times in the last hour but with the announcement that Boris Johnson will step down as Conservative leader, the scene is set for a leadership contest, the winner of which will become Prime Minister. Yesterday saw some fairly extraordinary scenes with a large number of ministers resigning but Boris Johnson remaining resolute that he retained a political mandate to govern after the large majority at the last general election. This morning, Downing Street officials briefed that Boris Johnson would resign as Conservative leader later today whilst remaining caretaker Prime Minister until the election process is concluded in the autumn.

What next

Sterling has seen a small bounce this morning versus the major currency pairs however until a clear leader emerges from the pack of contenders, the true economic and political impact of the change in leader will be hard to price in. At this stage we probably shouldn’t read too much into the bookmakers odds however Penny Mordaunt is leading. Mordaunt has distanced herself from the Prime Minister for several months, which could prove a factor amongst MPs as well as the Conservative membership, and pairs pro-Brexit leanings with liberal Conservatism – potentially appealing to both wings of Tory MPs. Conservative MPs will debate the benefits of each candidate, voting until two candidates remain, with the ultimate winner chosen by Conservative party members.

What does Brooks Macdonald think?

Back in 2019, sterling’s price was closely correlated with the perceived probability of a softer or harder Brexit. In recent weeks, with global central banks opting for differing levels of aggression in tackling inflation, currency pairs have largely been determined by expected differences in interest rate policy. This leadership contest however will undoubtedly draw the attention of currency markets given a) the new leader would have up to 2 years until the next general election b) EU/UK relations remain highly uncertain and c) the cost of living crisis makes fiscal policy even more important.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please find below, a market update received from Brewin Dolphin, yesterday evening – 28/06/2022

Global stock markets rose last week as reports of a slowdown in economic growth helped to calm interest rate fears.

The S&P 500 ended its holiday-shortened trading week up 6.5%, lifting it out of bear market territory, amid signs the Federal Reserve’s monetary tightening was helping to moderate inflation. The Dow and the Nasdaq climbed 5.4% and 7.5%, respectively.

Stocks in Europe broke their three-week losing streak, with the STOXX 600 and FTSE 100 advancing 2.4% and 2.7%, respectively. Weaker-than-expected purchasing managers’ indices (PMIs) helped to alleviate fears of more aggressive interest rate hikes.

In China, the Shanghai Composite gained 1.0% after the country’s president Xi Jinping said it would adopt “more forceful measures to deliver the economic and social development goals for the whole year and minimise the impact of Covid-19”.

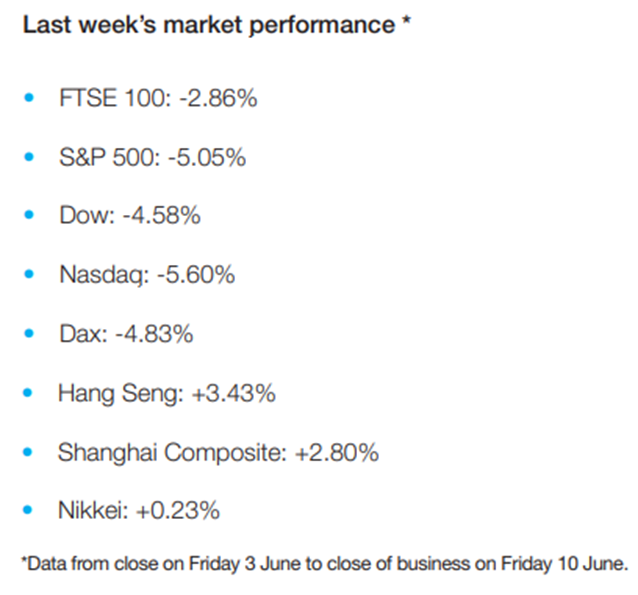

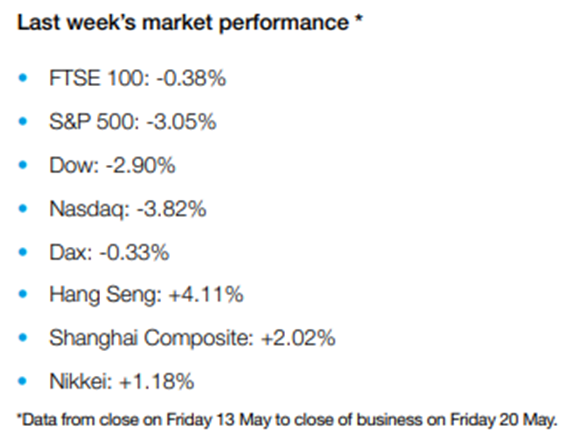

Last week’s market performance*

• FTSE 100: +2.74%

• S&P 5001 : +6.45%

• Dow1 : +5.39% • Nasdaq1 : +7.49%

• Dax: -0.06%

• Hang Seng: +3.06%

• Shanghai Composite: +0.99%

• Nikkei: +2.04%

*Data from close on Friday 17 June to close of business on Friday 24 June. 1 Closed Monday 20 June.

China eases Covid-19 restrictions

UK and European indices started this week in the green as an easing of Covid-19 restrictions in China boosted investor sentiment. The FTSE 100 climbed 0.9% on Monday (27 June) with miners leading gains after G7 leaders pledged a $600bn boost to global infrastructure. In contrast, the Dow, S&P 500 and Nasdaq gave back some of last week’s gains, ending the trading session down 0.2%, 0.3% and 0.7%, respectively.

In economic news, US pending home sales unexpectedly rebounded in May after declining for six consecutive months. Sales rose by 0.7% from the previous month but were down 13.6% on a year-on-year basis.

The FTSE 100 was up 1.1% at the start of trading on Tuesday as hopes of an economic rebound drove commodity prices higher and boosted mining stocks.

UK inflation accelerates to 9.1%

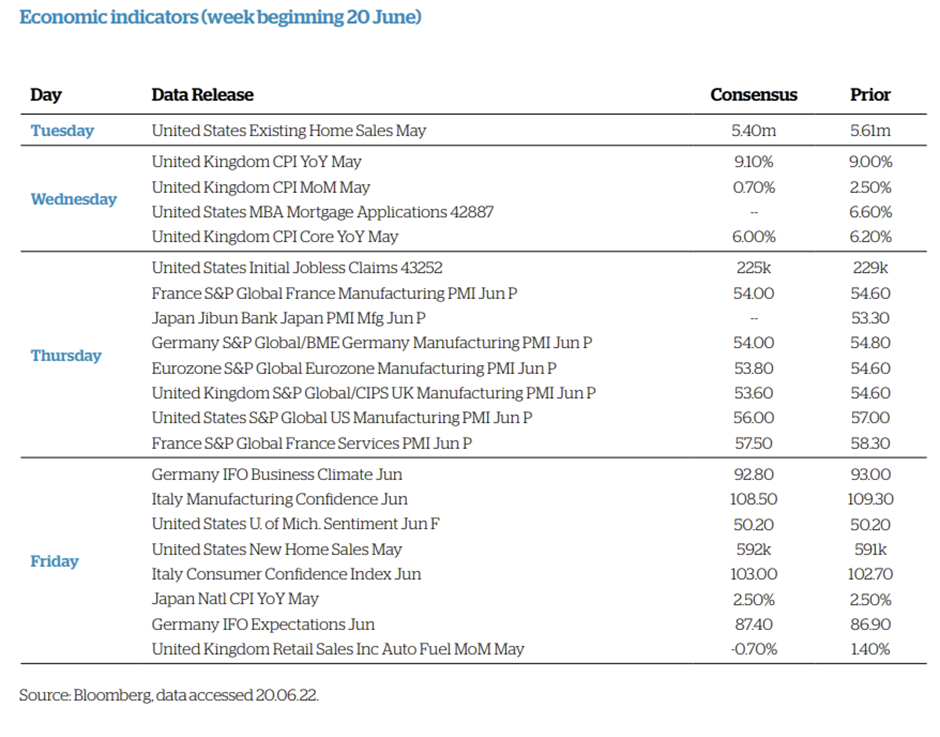

The UK consumer price index, published last Wednesday, showed inflation hit a new 40-year high in May as food and energy prices soared. The Office for National Statistics (ONS) said prices rose by 9.1% in the 12 months to May, slightly higher than the 9.0% increase recorded in April. Prices for food and non-alcoholic drinks rose by 8.7% year-on-year, the biggest jump since March 2009.

Encouragingly, core inflation – which strips out food and energy prices – eased to 5.9% in May from 6.2% in April. On a monthly basis, consumer prices rose by 0.7% in May, much less than the 2.5% monthly increase seen in April.

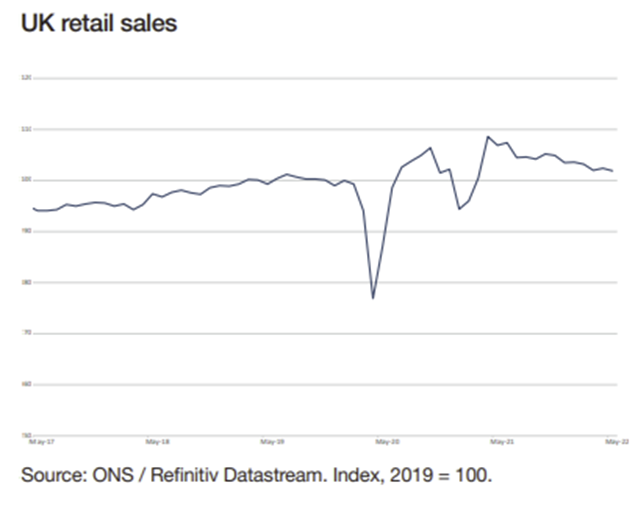

Consumers rein in spending

The latest UK retail sales data suggests rising prices are resulting in consumers reining in their spending. Sales volumes fell by 0.5% between April and May, reversing the expansion seen in the previous month.

The decline was driven by a 1.6% fall in food store sales, which the ONS said seemed to be linked to the impact of rising food prices and the cost of living.

Separate figures showed UK consumer confidence fell to its lowest level since records began. GfK’s consumer confidence index slipped by one point to -41 in June, with a particularly large drop in expectations around personal finances. “With prices rising faster than wages, and the prospect of strikes and spiralling inflation causing a summer of discontent, many will be surprised that the index has not dropped further,” said Joe Staton, client strategy director at GfK.

Eurozone business growth slumps

Last week’s economic data also showed a slowdown in business growth in the eurozone. The S&P Global flash eurozone PMI composite output index fell from 54.8 in May to 51.9 in June, a 16-month low. Manufacturing output contracted for the first time in two years and service sector growth cooled considerably, particularly among consumer-facing services.

Companies also scaled back their business expectations for output over the coming year to the lowest since October 2020. Both the stagnation of demand and worsening outlook were widely blamed on the rising cost of living, tighter financial conditions and concerns over energy and supply chains.

Chris Williamson, chief business economist at S&P Global Market Intelligence, said: “Eurozone economic growth is showing signs of faltering as the tailwind of pent-up demand from the pandemic is already fading, having been offset by the cost-of-living shock and slumping business and consumer confidence. Excluding pandemic lockdown months, June’s slowdown was the most abrupt recorded by the survey since the height of the global financial crisis in November 2008.”

Signs US inflation is moderating

Over in the US, data suggested inflation could be moderating. The University of Michigan’s consumer sentiment survey showed consumers expect inflation to rise at an annualised rate of 5.3% in June, below forecasts and the peak rate of 5.4% recorded in March and April. Meanwhile, S&P Global’s flash PMI data for June showed the pace of input price inflation eased to the lowest for five months, and output charges rose at the softest pace since March 2021.

However, the data also revealed the weakest upturn in US private sector output since January’s Omicron[1]induced slowdown. The rise in activity was the second softest since July 2020, with slower service sector output growth accompanied by the first contraction in manufacturing production in two years. Meanwhile, business confidence slumped to the lowest since September 2020. “Business confidence is now at a level which would typically herald an economic downturn, adding to the risk of recession,” said Williamson.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

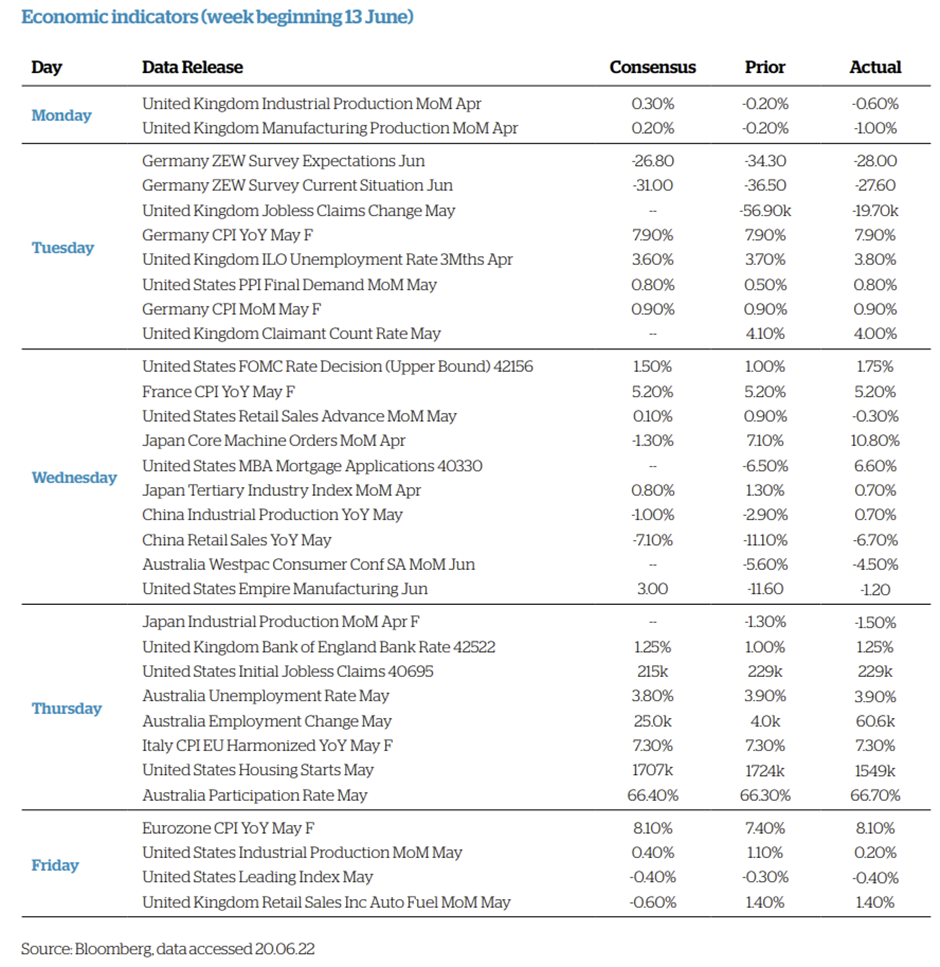

Please find below, a weekly market update received from Brooks Macdonald, yesterday evening – 20/06/2022

US and European equity markets fell heavily last week as the Federal Reserve (Fed) u-turned on its forward guidance

President Macron’s party has lost overall control of the National Assembly, challenging future legislative plans

Fed Chair Powell testifies to Congress this week, keeping central bank policy front and centre

US and European equity markets fell heavily last week as the Fed u-turned on its forward guidance

Last week saw one of the worst weeks for equity markets in recent memory as last minute changes to central bank policy mixed with a poorer economic backdrop. The losses were widespread with few markets and sectors able to avoid the contagion. European peripheral bond markets fared better, as the market gained some comfort from the European Central Bank’s (ECB) emergency meeting to discuss how to tackle any fragmentation between national bond markets.

Whilst last week’s Federal Reserve meeting is out of the way, investors are still reeling from the last minute change in Fed forward guidance which saw a 75bp interest rate hike in June after such a hike had previously been ruled out1 . Forward guidance is extremely difficult at a time when the central bank is data dependent on what happens to inflation and economic growth, however a feeling that the words of Fed Chair Powell should be taken with a pinch of salt will only heighten volatility. This week Chair Powell will testify to both the Senate and House Committees where he is expected to be questioned on what the central bank is doing to control the inflationary spike in the US. Last week Powell said that a 75bp rate hike would not become a typical event however with forward guidance in question, this may not stop markets from pricing in such an outcome.

President Macron’s party has lost overall control of the National Assembly, challenging future legislative plans

The French legislative elections have seen President Macron lose overall control of the National Assembly. Whilst Macron’s party remains the largest overall party, any legislative items will require delicate coalitions to be formed. The elections saw a strong showing for far left and far right parties, splitting the centrist vote. Macron is likely to rely on votes from the fractured centre right parties to pass key items such as pension reforms however such legislation is likely to need to be watered down to pass through a complex web of political priorities.

Fed Chair Powell testifies to Congress this week, keeping central bank policy front and centre

The recent market volatility has been driven by inflation data and the central bank reaction to that data. With the US closed on Monday, no US inflation releases this week, and Powell unlikely to err too much from his statements last week, we may be in for a calmer week. Now we are back to an era of emergency central bank meeting however, the chance of a surprise has greatly increased.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below ‘Markets in a Minute’ article received from Brewin Dolphin yesterday evening, which provides a global update on markets.

US and European indices fell last week as US headline inflation soared and the European Central Bank (ECB) signalled it could increase interest rates at a faster rate than anticipated.

After a positive start to the week, the S&P 500, Dow and Nasdaq slid 5.1%, 4.6% and 5.6%, respectively. The consumer price index (CPI) for May, released on Friday, showed headline inflation rose by 8.6% from a year earlier – higher than consensus estimates.

In Europe, the STOXX 600 dropped 4.0% and Germany’s Dax sank 4.8% after the ECB lowered its outlook for economic growth. The UK’s FTSE 100 fell 2.9%.

Stocks in Asia had a more encouraging week, with the Nikkei 225 edging up 0.2% after figures showed the Japanese economy shrank by less than expected in the first quarter. China’s Shanghai Composite rose 2.8% on news Beijing appeared to be easing its crackdown on the technology sector.

UK GDP unexpectedly shrinks in April

The FTSE 100 slumped 1.5% on Monday (13 June) after data from the Office for National Statistics (ONS) showed UK gross domestic product (GDP) contracted by 0.3% in April after declining by 0.1% in March. Economists had been expecting a slight increase of 0.1%. The ONS said the scaling back of the Covid-19 vaccination programme and pandemic test-and-trace was the biggest contributor to the monthly fall in GDP. Manufacturing also suffered with some companies affected by rising fuel and energy prices.

Stocks in the US and Europe also slid on Monday following speculation the Federal Reserve might decide to raise interest rates by 75 basis points at its next policy meeting on 14-15 June. The S&P 500 and the Nasdaq lost 3.9% and 4.7%, respectively, while the STOXX 600 fell 2.4%. Concerns over a resurgence of Covid-19 cases in China weighed on markets in Asia, with the Shanghai Composite, Hang Seng and Nikkei down 0.9%, 3.4% and 3.0%, respectively.

The FTSE 100 opened in the green on Tuesday as investors mulled the latest UK labour market data. Unemployment edged slightly higher to 3.8% in the three months to April from 3.7% in the three months to March. This was the first increase since the last three months of 2020. The number of job vacancies hit a new record high of 1.3 million, while real wages (adjusted for inflation) fell by 2.2% year-on-year.

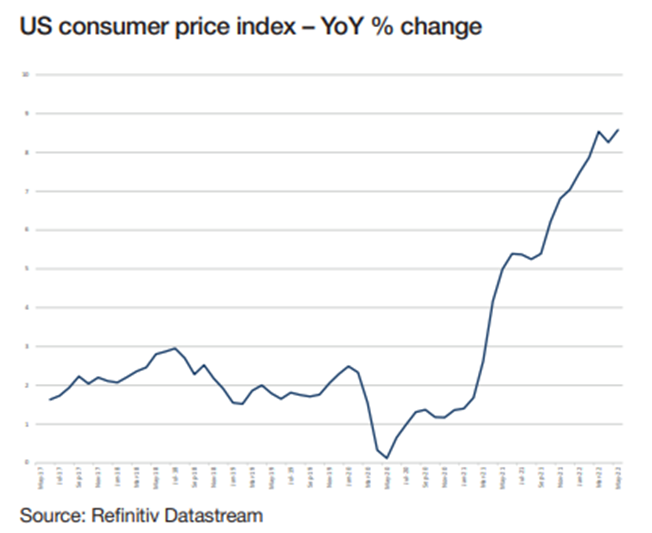

US inflation hits new 40-year high

Inflation in the US accelerated to a new four-decade high in May as the cost of petrol, food and other necessities surged. The headline CPI rose to 8.6% from a year ago, faster than April’s year-on-year increase of 8.3% and the highest level since December 1981.

The increase was driven by a surge in prices for gasoline, food and shelter. Energy costs rose by 34.6% from a year earlier, while groceries jumped by 11.9%. On a monthon-month basis, prices rose by 1.0%, significantly higher than the 0.3% increase in April and above economists’ expectations of a 0.7% rise. Once food and energy prices were stripped out, core inflation rose by 0.6% month-onmonth and by 6.0% from a year ago, according to the Department of Labor.

ECB unveils interest rate plans

Inflation and interest rates also dominated the headlines in Europe last week. The ECB signalled it was likely to raise rates by half a percentage point in September, in addition to a planned quarter-point rise in July. ECB president Christine Lagarde and chief economist Philip Lane had previously said rate rises of 0.25% were the benchmark for its meetings in July and September. On Thursday, however, Lagarde said risks to the inflation outlook were “primarily on the upside”, according to a report in the Financial Times.

The comments came as the ECB raised its inflation projections to an average of 6.8% for this year, well above the 5.1% predicted in March. Inflation is expected to ease to 3.5% in 2023 and 2.1% in 2024. The ECB also cut its outlook for GDP growth to 2.8% for 2022 and 2.1% for 2023, down from 3.7% and 2.8% previously.

“Russia’s war against Ukraine has severely hit confidence, caused energy and food prices to soar further and, together with pandemic-related disruptions in China, compounded existing supply chain pressures,” the ECB said. “These factors pose strong headwinds for the economic recovery in the euro area and come at the same time as a relaxation of pandemic-related restrictions, which is providing a strong boost to the services sector.”

Japan GDP better than expected

The latest economic growth figures for Japan proved to be better than expected. According to the Cabinet Office, GDP declined by an annualised 0.5% in the first quarter of the year, less than the initial estimate of a 1.0% contraction. On a quarter-on-quarter basis, GDP shrank by 0.1%, beating expectations for a 0.3% decline. Private consumption, which makes up more than half of Japan’s GDP, rose by 0.1% from the previous quarter, while inventories also increased. This helped to offset a 0.7% quarterly fall in capital spending.

Please check in again with us shortly for further relevant content and market news.

Please find below, a summary of this week’s Tatton articles, received from Tatton this morning – 13/06/2022

Outlook: new worries, old concerns? After renewed positive sentiment in recent weeks, markets once again are showing signs of fragility. We could characterise this ‘risk off’ mood as growth scepticism or more wariness that inflation needs even stronger and swifter central bank policy tightening before being squeezed out. Last week’s change in emphasis from the European Central Bank (ECB) – while expected – provided the necessary headlines. Interest rates were unchanged, but ECB President Christine Lagarde “committed” that rates will rise by 0.25% at the July meeting, and that bond buying will also end (although there was no mention of actual bond sales). From the current overnight market rate of -0.5%, most economists expect the year-end traded rate to be around +0.75%.

If the ECB is so certain of a rate hike next month, why not start now? If the ECB’s own inflation forecasts keep going up – and all the risks lie towards higher inflation – this is like driving towards a cliff edge with a broken speedometer and promising your passengers you won’t brake too sharply. There may be reasons to think the ECB’s laggardly stance (pun intended) is intentional because most believe the underlying issues are ‘global cost push’, and that the policy that matters comes from the US Federal Reserve (Fed). In which case, policy compression is already underway. US inflation data for May released on Friday worried some investors by being slightly above expectations (with monthly core consumer price index (CPI) inflation still rising at an annualised rate of 7%). US ten-year Treasury yields returned to above 3% last week. Perhaps investors are yet to be convinced inflationary pressures may have peaked.

The current upswing in market risk premia seems to us to be more of a straightforward tale of risk aversion. If energy prices keep rising, or some other external threat emerges, those more anxious investors who headed for the exit might been justified. But resilience levels and activity potential for the global economy have not been in as promising a state for a long time – as has been the resilience of systemically important financial institutions. We suspect last week’s wobble was no more than that.

Monetary and fiscal policy: giving with one hand, taking with the other Boris Johnson’s pyrrhic victory on Monday’s ‘no-confidence’ vote could have big implications for the UK economy. Not that you could tell from the market reaction: the FTSE 100 dropped ever so slightly in midweek, while sterling stayed at the same dollar value. But the Prime Minister’s weakened position makes him much more amenable to the whims of his colleagues, and the pressure to ease the UK’s tax burden is mounting. Backbench MPs are reportedly urging the Prime Minister to override the Treasury on cutting taxes, regardless of the inflationary impact. If this happens, it is unlikely to be matched by spending cuts, which could threaten another rebellion. As such, we should expect that the government will loosen fiscal policy in the coming months.

Let that sink in for a moment. Britain is currently seeing its highest inflation levels in 40 years – higher than any other G7 nation – and unemployment is the lowest it has been since the 1970s. Energy and goods supply is severely constrained, and with an excruciatingly tight labour market, we are on the cusp of a wage-price spiral. And amid all of this, the government is throwing more fuel on the fire by loosening fiscal policy. As politically and socially understandable as this may be, such a move would increase inflationary pressures and put the Bank of England (BoE) in a bind. In this environment, monetary policymakers cannot afford to balance growth prospects against price stability. Instead, they must tighten policy hard, raising interest rates and likely choking off growth potential.

This combination of tight monetary and loose fiscal policy is far from confined to the UK either, as the ECB announcement made clear. More generally, it is a reversal of the policies promoted for more than a decade after the global financial crisis. In that time, we have seen incredibly easy financial conditions while governments have been reluctant to loosen the public purse-strings and in many cases applied outright fiscal austerity. Over the years, many called on politicians to match central banks’ largesse, that it is happening now – while global inflation surges – will no doubt make many uncomfortable.

Rising interest rates and central bank tapering puts upward pressure on yields. But so too does loose fiscal policy, as higher government borrowing increases the bond supply competing for investor’s buying interest. Both happening at the same time could mean dramatic upward pressure on yields – which is unlikely to stop anytime soon. Rising bond yields also push up borrowing costs for consumers and businesses. If these increase too rapidly, widespread defaults become much more likely – the classic harbinger of recession. The silver lining is that increased borrowing costs act as a dampener on demand, pulling down inflation and lessening the need for higher interest rates. Yields are pushing up from extraordinarily low levels, so there could still be some way for bond yields to go before there is a significant risk of triggering a debt default cycle. The BoE will certainly hope that is enough to tame price rises. With the UK economy forecast to be the second-worst performing in the G20 (behind only sanction-ravaged Russia) tighter monetary policy could mean severe pain for businesses and consumers. But with the government apparently pushing ahead with fiscal aid, the central bank has little choice. What the new policy mix means over the longer-term remains to be seen.

A fistful of chips: from supply shortage to glut US technology giant Intel took a beating from investors last week, leading to a 5.3% fall in its share price on Wednesday. This came after projecting disappointing results for the second quarter. Intel reckons its profits will be around 70 cents a share, well below analyst estimates of 82 cents, and follows a disappointing first quarter of 2022, which saw falling revenues for its PC microchips. Intel’s management insists decent growth forecasts for 2022 will be achieved, implying a stronger second half than previously expected. Investors are not so sure that optimism is warranted, unnerved by signs of faltering demand for PCs – Intel’s largest revenue source. Of the other global chip manufacturers, NVIDIA has had a harder time this year whereas Taiwan Semiconductor Manufacturing Co (TSMC), the world’s most valuable chip maker, expects revenues to grow 30% overall this year, a jump from the near 25% growth of last year. TSMC’s projections seem at odds with actual chip price moves, and concerns that demand for computer chips is stalling from global economic and political factors: war in Ukraine, Chinese lockdowns and the cost-of-living crisis across the developed world. Last year, waiting times for games consoles and new cars were unheard of all over the world. TSMC claim these supply shortages continue.

Wait times for semiconductor delivery hit a record high in May, and chipmakers are raising prices due to rising costs, but in other respects, the chip shortage seems much less pronounced. Companies in need of chips are reportedly starting to see relief and, more importantly, demand has plateaued. Apple, one of TSMC’s best customers, is planning to keep its production of iPhones flat in 2022 – capping off a potential route for growth. This comes as global growth is slowing significantly and inflation is eating into consumers’ disposable incomes. Rapid price rises have also forced the hands of central banks, which are now tied into a rate-hiking cycle that will result in higher borrowing costs and less available capital. The smartphone industry has struggled with these headwinds all year, but the pressures are broad-based, hitting demand for goods well beyond consumer electronics.

Therefore, despite manufacturer claims to the contrary, capital markets clearly believe chip demand is weaker than supply. Where once there was extreme undersupply, stock markets indicate there is now oversupply. This looks unlikely to change anytime soon, either. Slowing global growth and a cost-of-living crisis will hold back demand in the short term. And over the medium term, there are signs that supply will be boosted. Beyond the question of how we look at chip manufacturers from an investment perspective, the other takeaway from the easing of chip supply is perhaps this: just as chip shortages were the first sign last year of building supply chain disruptions, the easing of supply issues for ‘commoditised’ semiconductor chips now may well mean that price pressures from the supply shortage of goods might be behind us soon.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please find below, a Weekly Market Commentary, received from Brooks Macdonald yesterday afternoon – 30/05/2022

Equity markets rallied last week, avoiding an 8-week streak of US equity losses

Stronger than expected US retail earnings as well as reduced expectations of US monetary tightening buoyed sentiment

This week’s focus will be on US economic data, European inflation and the commencement of the Federal Reserve’s (Fed) balance sheet run-off

Equity markets rallied last week, avoiding an 8-week streak of US equity losses

US equity markets broke their 7-week losing streak last week, seeing a strong rally which was led by consumer discretionary stocks as discount retailers posted better earnings than expected. Bond markets also shared this rally as investors priced in a less aggressive pace of tightening from the Federal Reserve in the face of declining economic momentum. This week is likely to be quieter with the US on holiday today for Memorial Day and the UK off on Thursday and Friday for the Queen’s Platinum Jubilee.

Stronger than expected US retail earnings as well as reduced expectations of US monetary tightening buoyed sentiment

Despite the week being truncated on both sides of the Atlantic, there are plenty of data releases for markets to interpret. In the US we will see the latest industrial activity metrics as well as the Institute for Supply Management (ISM) manufacturing data which comes after the misses in the Purchasing Manager’s Index (PMI) surveys last week. The Conference Board will also update their consumer confidence survey which will give an insight not only into current consumer confidence but also expectations around the future. The main event however will be the US jobs report which is released on Friday. Last month’s reading came in ahead of market expectations at 428,000 new jobs created, this month the market is predicting a more subdued 320,000 but the unemployment rate is expected to tick down from 3.6% to 3.5%1.

This week’s focus will be on US economic data, European inflation and the commencement of the Fed’s balance sheet run-off

Wednesday will see the beginning of the Federal Reserve’s balance sheet run off as it commences its quantitative tightening programme. The process ramps up in September with the Fed re-investing an even smaller proportion of maturing Treasury and mortgage securities. The Fed’s logic is that by not re-investing a proportion of maturing funds from current holdings, the shrinking of the balance sheet can be open and transparent to market participants, reducing the risk of bond market turmoil. There is undoubtedly a communication and liquidity challenge posed by the combination of rate hikes and balance sheet run-off however and that will keep risk assets on their toes until the process is bedded in.

Equities have edged higher on Monday, buoyed by a fresh round of stimulus in China and the more optimistic tone that ended the US session last week. This week is likely to contain a focus on the European Central Bank (ECB) with the central bank increasingly positioning for a July rate hike. Expect the market to focus on German inflation data as well as the specific wording adopted by ECB speakers.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below ‘Markets in a Minute’ article received from Brewin Dolphin yesterday evening, which provides a global update on markets and economies.

Fears about the impact of inflation on global economic growth led to further stock market losses last week.

In the US, the S&P 500 suffered its biggest daily fall since the early months of the pandemic, closing down 4.0% on Wednesday following poor results from major retailers. On Friday, the index briefly fell into bear market territory, down more than 20% from its January high, as fears of a recession grew. The index finished the week 3.1% lower, while the Dow and the Nasdaq slid 2.9% and 3.8%, respectively.

The FTSE 100 slipped 0.4% as UK inflation soared and consumer confidence fell to its lowest level in nearly 50 years. The pan-European STOXX 600 declined 0.6% after the European Commission cut its growth forecasts for the eurozone.

Over in Asia, China’s decision to cut interest rates to support its ailing property sector helped to boost sentiment in the region. The Shanghai Composite gained 2.0% and the Nikkei 225 added 1.2%

UK house prices hit fresh record high

Most major indices started this week in the green, with the FTSE 100, Dax and S&P 500 up 1.7%, 1.4% and 1.9% at the close of trading on Monday (23 May). Comments from US President Joe Biden that he was considering lowering tariffs on certain products imported from China helped to boost sentiment.

In economic news, figures from Rightmove showed the average asking price of a UK property rose by 2.1% month-on-month in May to £367,501, the highest for the time of year since May 2014. On an annual basis, prices surged by 10.2% as supply failed to keep up with continued buoyant demand.

Stocks slipped back again at the start of trading on Tuesday. The FTSE 100 fell 1.0% as investors mulled the latest UK government borrowing data. According to the Office for National Statistics (ONS), borrowing fell by £5.6bn year-on-year in April to £18.6bn but remained above pre-pandemic levels.

UK inflation hits 40-year high

The latest UK inflation figures showed consumer prices rose at their steepest rate for more than 40 years in April as the cost of food and energy soared. The consumer prices index (CPI) rose by 9.0% compared with a year ago, up from 7.0% in March. On a monthly basis, the CPI increased by 2.5%, up from a rise of 0.6% in the same month a year ago.

The ONS said the increase in the energy price cap was the main reason for the jump in CPI. The annual inflation rate for electricity and gas hit 53.5% and 95.5%, respectively. Average petrol prices rose to a record 161.8p a litre in April from 125.5p a year earlier, pushing the annual inflation rate for motor fuels and lubricants to 31.4%. Elsewhere, the end of a temporary VAT cut for the hospitality industry led to a 1.7% monthly increase in restaurant and hotel prices.

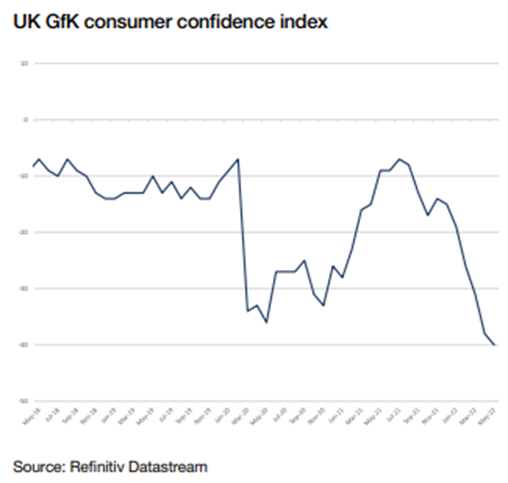

The rising cost of living meant GfK’s consumer confidence barometer fell to -40 in May, the lowest level since records began in 1974. “This means consumer confidence is now weaker than in the darkest days of the global banking crisis, the impact of Brexit on the economy, or the Covid shutdown,” said Joe Staton, client strategy director at GfK. The sub-measures on the general economy sank to -63 for the last 12 months and -56 for the coming year. “The outlook for consumer confidence is gloomy, and nothing on the economic horizon shows a reason for optimism any time soon,” added Staton.

Retail sales jump despite rising prices

Despite the doom and gloom, separate figures from the ONS showed a surprise jump in retail sales in April. Sales volumes rose by 1.4% month-on-month following a fall of 1.2% in March. Economists in a Reuters poll had forecast a decline of 0.2%. The rise was led by strong growth in sales of alcohol and tobacco, which drove food store sales volumes up by 2.8%. Clothing sales were also strong as customers booked weddings and holidays.

On a quarterly basis, sales volumes fell by 0.3% in the three months to April, extending the downward trend in place since summer 2021. “Retail sales picked up in April after last month’s fall,” said Heather Bovill, ONS deputy director for surveys and economic indicators. “However, these figures still show a continued longerterm downward trend.

“April’s rise was driven by an increase in supermarket sales, led by alcohol and tobacco and sweet treats, with off-licences also reporting a boost, possibly due to people staying in more to save money.”

US housing market cools

Over in the US, data suggested the housing market could be slowing as rising mortgage rates make it harder for people to get onto the property ladder. Building permits dropped 3.2% month-on-month in April, led by a 4.6% fall in permits for single-family housing, according to the Commerce Department. Housing starts slipped by 0.2%, with single-family housing starts plunging by 7.3%.

It came after the NAHB/Wells Fargo Housing Market Index, a measure of housing market sentiment, dropped to the lowest level in nearly two years in May. This was blamed on rising prices for building materials and rapidly increasing mortgage rates. The 30-year fixed-rate mortgage averaged 5.3% during the week ended 12 May, the highest since July 2009, according to Freddie Mac data reported by Reuters.

Please check in again with us soon for further relevant content and news.

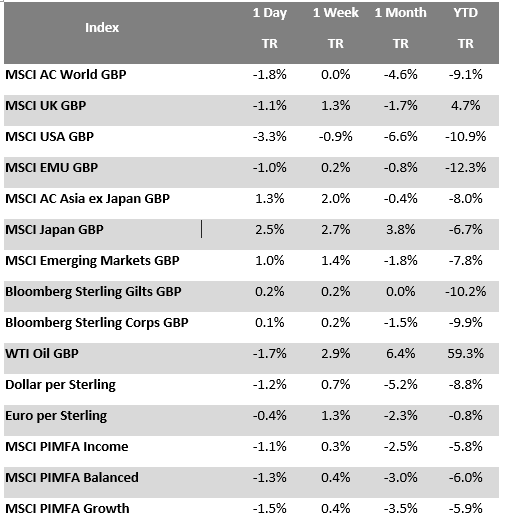

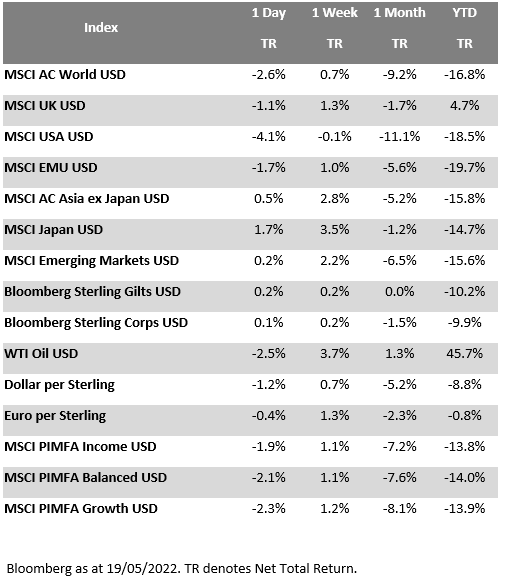

Please see the market update below received this morning from Brooks Macdonald – 19/05/2022

What has happened

The bounce in global equities that had buoyed sentiment on Tuesday, faded fast on Wednesday. Selling the previous day’s rally, investors seemed to focus back on concerns around near-term inflation pressures in particular. In company news, US general merchandise retailer Target missed estimates and the shares fell around 25%, but rather than a read on the health of the US consumer in aggregate, it looked more about the impact of a consumer shifting away from pandemic-driven elevated goods spend, which hit Target’s sales of goods outside of its grocery lines, such as TVs and kitchen appliances. Also on Wednesday, UK CPI data showed inflation rose to 9% Year on Year in April, slightly below a consensus estimate of 9.1%. Boosted by the 1st April rise in the energy price cap, the headline inflation rate reached a 40 year high. In currency markets, Sterling fell versus the Dollar on concerns that the Bank of England might have to tread more carefully around near-term inflation pressures, in order to guard against longer-term economic growth risks.

US retailer Target delivers an off-target negative surprise

US general merchandise retailer Target reported 1Q earnings on Wednesday, but missing estimates the stock fell around 25%. While the retailer was impacted by higher costs (including fuel costs), and supply chain troubles, the dominant impact seemed to be the company caught by a bigger than expected consumer shift out of goods (especially durable goods) such as TVs and kitchen appliances, that had done well during the pandemic, leaving the company overstocked and forced to mark down prices. Without stimulus cheques fuelling spending, combined with a return to more normal consumption patterns as consumers move back towards services, this was seen as a factor the company. As the Target CEO Cornell said on Wednesday, “three core merchandise categories, apparel, home and hardlines, we saw a rapid slowdown … while we anticipated a post-stimulus slowdown and we expected consumers to continue refocusing spending away from goods and into services, we didn’t anticipate the magnitude of that shift.”

Markets caught in an investor sentiment tug-of-war

Markets are caught in an investor sentiment tug-of-war battle at the moment, but relatively high levels of market volatility are likely to be with us for a while yet. For central banks, the challenge is getting the balance right between taming near-term inflation pressures while not impacting longer-term economic growth, but it’s a challenge that’s fraught with difficulty. With US Fed Chair Powell hoping for a “softish landing” and UK BoE Governor Bailey seeing a “narrow path” between the risks of inflation and growth, the question as to whether central banks can successfully thread-the-needle on policy unfortunately has no short-term answer.

How is the inflation picture shaping up?

The inflation picture is rightly dominating investors’ attention, but it can be unpacked into a number of different drivers currently. COVID has created price ‘disruption’ as a result of the post-pandemic restart and the imbalance in supply chains between both goods and services as well as demand and supply. War in Ukraine this year has complicated the inflation picture, adding significant price ‘shocks’ to energy and food in particular. But price ‘disruption’ and price ‘shocks’ are not enough by themselves to kick-start a multi-year inflation process. For that a necessary component would be a significant and sustained rise in inflation expectations (including wage expectations). However, analysis last week from the Peterson Institute for International Economics suggests that the big news in the US April jobs report published earlier this month was a potentially slowing wage growth picture. Looking at US average hourly earnings, the annualized rate of growth (once adjusted for compositional changes in the labour force), was 3.8% over the past three months, a pace considerably slower than in 2021, which saw peaks around 7%.

What does Brooks Macdonald think?

At Brooks Macdonald, we recognise that the current inflation picture is complex and multifaceted. On balance, we expect the current high inflation rates to start to ease over the remainder of this year and into 2023 – but how quickly (and how far) inflation drops back (as well as the impact to economic growth further out from interest rate hikes in the interim), remain difficult to gauge. Ultimately, it’s one of the reasons why, within equities, we continue to hold to our barbell balance between growth/defensive and value/cyclical investment styles at the current time.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below article received from AJ Bell this afternoon, which informs investors of the key factors driving stocks, bonds and other assets in the markets currently.

Many investors are frustrated that a lot of the stocks, funds and bonds in their portfolios have fallen in value this year. It’s been a chaotic time on the markets and negative events keep unfolding.

Inflation is at levels not seen for decades, the first major European war of the 21st century has broken out, and after years of ultra-low interest rates central banks are starting to tighten monetary policy.

Inflation has accelerated over the past year

Investors face a tricky task of determining when things might get better and what they should do with their investments in the meantime. Sitting tight and staying invested is a good strategy, but more active investors might be interested in tweaking their portfolios based on the outlook.

In this article we look at what the experts are forecasting for inflation, economic growth and interest rates and what market observers think has already been priced in. Our aim is to give a picture of how bad life could get or whether things might already be starting to improve.

UKRAINE SHAPES THE OUTLOOK

There is one key source of uncertainty which makes gauging the outlook difficult, namely the progress of the tragic conflict triggered by Russia’s invasion of Ukraine.

As Andrew McCaffery, global chief investment officer for asset manager Fidelity, observes: ‘The war in Ukraine has already caused significant economic damage, and it will continue to shape the near-term outlook for global economies, particularly Europe. Outcomes over the coming quarter will be heavily influenced by the timeline to a resolution and the easing of trade disruptions.

‘In the meantime, any hopes for a moderation in energy prices and supply-chain disruptions have been dashed. Together, these dynamics will continue to dampen growth and put upward pressure on already high inflation.

‘This paints an extremely complex picture, both for policymakers and the markets. We believe the market has yet to reflect the full range of possible outcomes, which span extreme left and right tail risks.’

These ‘tail risks’ refer to more positive or negative outcomes than expected. In this context it’s useful to see what is being anticipated by forecasters and what are the best and worst-case scenarios.

Trying to second guess what happens next in Ukraine is difficult. Chief Europe economist at consultancy Capital Economics, Andrew Kenningham, says: ‘Unfortunately assumptions about the war have steadily got worse over the past two months. We were hoping and assuming the conflict would ease towards the end of the year.

‘Without forecasting exactly what will happen on the ground we are now working on the assumption the conflict will continue with no early resolution but also no major escalation.’

Assuming this reasoning proves correct, companies and countries may be able to adjust to the disruption but if the conflict widens or deepens in any way this could present a new risk for financial markets.

INFLATION

The supply chain issues and high food and energy prices which have contributed to rising prices remain in place. The reintroduction of Covid restrictions in China, the so-called factory of the world, has only added to these inflationary pressures.

UK consumer price inflation forecasts (Q4 2022)

However, there are reasons to think we are close to peak levels of inflation. Investment bank Berenberg expects US inflation to peak at 8.1% and UK inflation to peak at 8.6%, both in the second quarter.

Jennifer McKeown, at the consultancy Capital Economics, says: ‘Globally inflation is going to come down this year thanks to very strong base effects linked to the reopening of economies in the second half of last year.’

Saying that inflation has peaked, for now, is not the same thing as predicting a rapid fall in prices. Berenberg forecasts inflation will remain above 6% in the final quarter of 2022 in the US and the first three months of next year for the UK.

Consensus forecasts on UK inflation may not go far enough. Panmure Gordon chief economist Simon French was already on record as saying UK inflation could hit double digits in 2022 before the Bank of England surprised many observers with a prediction for inflation to peak above 10% at the end of this year.

This would represent the highest level in 40 years but doesn’t seem too extreme given UK inflation data, up to the end of March, is yet to reflect Ofgem’s lifting of the energy price cap by 54% at the beginning of April, with a further big increase expected in October.

The chances of wholesale energy prices easing substantially are limited by attempts on the part of European countries to wean themselves off Russian gas and oil. The US, which is effectively energy independent by comparison, is more insulated on this front.

Tight labour markets, particularly in the developed world, are also contributing to inflation as wages increase.

Eurozone unemployment hit a record low of 6.8% in March and the US reported record job openings for the same month.

GDP

Surging inflation is one of the key reasons economists have been busily revising down growth forecasts this year. In its latest World Economic Outlook, published in April, the International Monetary Fund lowered its global growth forecast to 3.6% in 2022 and 2023. This was 0.8 and 0.2 percentage points lower respectively than in the January report.

UK GDP 2022 forecasts

There is little debate over whether the post-Covid economic recovery has been hit by the Ukrainian conflict. The question is whether it could be derailed entirely. We are already facing stagflation, which is a toxic combination of slowing growth and rising prices.

The yields on two-year and 10-year US government bonds recently inverted, i.e., the longer-dated debt offered a lower yield than the more short-term debt, which is often seen as a signal of recession and US GDP unexpectedly contracted 1.4% in the first quarter.

Nonetheless, non-profit research organisation The Conference Board does not believe a US recession is likely in 2022 – even under its modelling of some extreme scenarios, including oil hitting $200 per barrel.

COVID STILL A PROBLEM

The two main risks to this view are policy mistakes on the part of the US Federal Reserve and mutation or resurgence of Covid-19. Remember the pandemic continues to rage in some parts of the world.

There seems to be a greater risk of recession in Europe. Russia and closely linked emerging European economies look particularly vulnerable to a downturn but developed Europe too could risk slipping into a slowdown.

Capital Economics’ Andrew Kenningham says: ‘For the Eurozone overall we are forecasting almost flat second and third quarters with Italy and Germany at risk of falling into technical recessions; France and Spain should avoid that.’

A technical recession is defined as two consecutive quarters of negative growth and while the Bank of England thinks this fate can be avoided, it is forecasting a 0.25% contraction in UK GDP for 2023.

Outside of the US and Europe, China may be on a different trajectory with the easing of restrictions as Covid cases come down, helping growth to increase through the course of the year. Whether it can hit Beijing’s target of 5.5% is open to question.

INTEREST RATES

The finely balanced outcomes on inflation and economic growth create a tricky backdrop for central banks. It seems certain the Federal Reserve, Bank of England and, even the laggard of the three, the European Central Bank will end the year with higher interest rates.

However, the exact pace and trajectory of those increases remains in question. In its latest update (4 May) the US Federal Reserve lifted rates by 0.5 percentage points for the first time since 2000 but signalled it was not considering a 0.75 percentage point increase in rates for now.

The central bank did nothing to suggest consensus expectations for rates to finish 2022 somewhere around 2.5% were out of whack.

Nick Clay, who runs investment manager Redwheel’s global equity income team, observes: ‘I think the Fed’s been boxed into a corner. It will lead on this, but bond yields particularly in America have already priced a lot of that in.

‘Corporates and governments because of their levels of indebtedness are going to find it difficult to suffer higher interest rates for any length of time. By the time we get to the end of this year we will look back at this period and realise this was the peak in interest rates within the bond yield even if the Fed is still raising rates.’

The negative economic assessment which accompanied the Bank of England’s latest rate hike to 1% (5 May) suggests it may look to avoid hiking rates materially from here. Consensus expectations are for UK rates to reach a high of 2% next year but not everyone agrees with this assessment.

Capital Economics’ chief UK economist Paul Dales says: ‘We think longer-lasting domestic price pressures will mean the MPC (Bank of England’s Monetary Policy Committee) ends up raising rates to a peak of 3% next year, which compares to the peaks of 2.5% priced into the markets and 2% expected by other analysts.’

The European Central Bank may not have moved on rates yet, but it opened to the door to a July rate rise at its meeting in April.

The central bank faces an even more difficult task than the Fed and Bank of England given it needs to balance the needs of economies with very different dynamics. Inflationary pressures are also more acute in the Eurozone given its heavy reliance on Russian energy imports.

Berenberg forecasts two 0.25 percentage point interest rate rises in the third and fourth quarter of this year which would still leave Eurozone rates a long way behind those in the US and UK.

WHERE WILL THE MARKETS END UP?

How much of the increase in rates, reduced growth prospects and higher inflation have been factored in by the markets?

There is no question that investors have reacted to these events. The first quarter saw bond and stock prices fall in tandem for the first time in nearly 30 years.

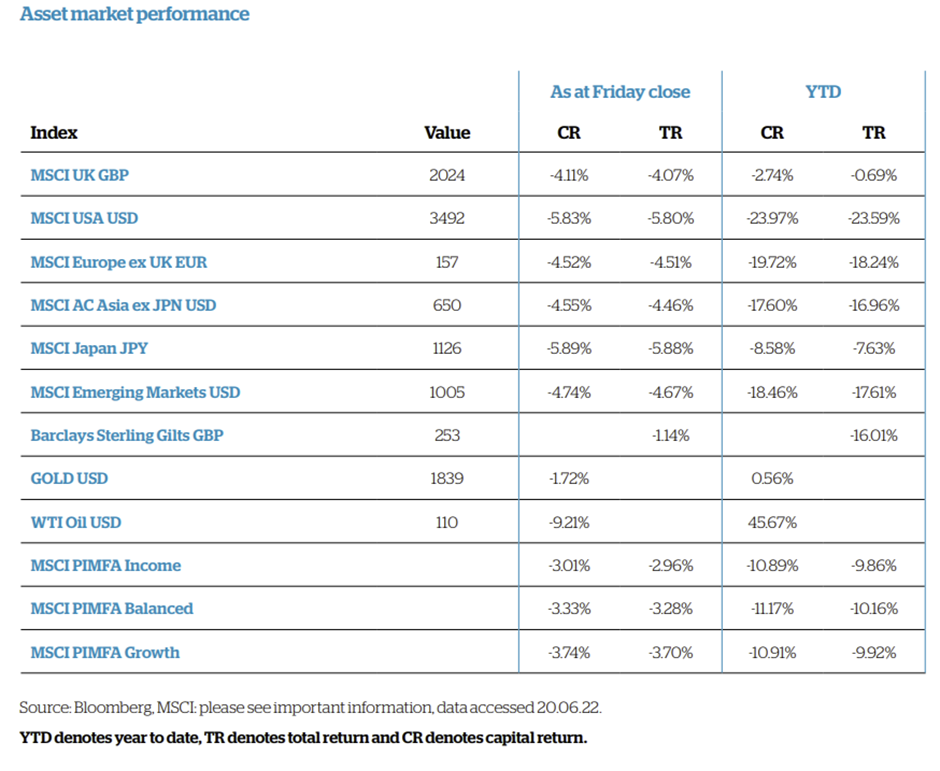

The table shows how global stock markets have performed year-to-date and it paints an ugly picture in most places. The UK’s FTSE 100 index is doing best thanks to its strong commodities exposure. In the US, the Nasdaq receives the wooden spoon as investors turn away from highly rated growth stocks.

Rupert Thompson, investment strategist at asset manager Kingswood, comments: ‘The falls in both bonds and equities have been driven by the move towards stagflation, the unpalatable combination of high inflation and stagnation in economic activity. Worries on this front have been bolstered by recent developments.’

How major stock markets have fared in 2022

Will there be more pain to come for stocks? In early April, investment bank Goldman Sachs updated its year-end forecasts for the S&P 500 index in the US for a closing level at the end of December of 4,700.

This would represent a modest drop versus 2021’s closing level of 4,766 and compares with a current level of 4,125. This represents its best-case scenario. In the event of a recession the bank thinks the index could fall to 3,600.

Bank of America says there have been 19 bear markets in the past 140 years. A bear market is a 20% decline or more from recent highs.

The average price decline in these 19 bear markets was 37.3% and an average duration of 289 days. It says: ‘Past performance is no guide to future performance, but if it were, today’s bear market ends on 19 October 2022 with the S&P 500 at 3,000 and the Nasdaq at 10,000. The good news is many stocks are already there, e.g., 49% of companies in the Nasdaq are more than 50% below their 52-week highs.’

S&P 500

Elsewhere, Morgan Stanley forecasts the S&P 500 to end 2022 at 4,200, JPMorgan predicts 4,900 and Barclays estimates 4,800.

Gains for US stocks have been driven by the big technology companies and as Redwheel’s Nick Clay says, ‘They are very expensive. Even the best company in the world at the wrong valuation becomes the riskiest company. Your expectations are so high they can’t even deliver on those extended expectations.’

Corporate earnings are holding up well. On 29 April Factset said that of the 55% of companies in the S&P 500 which had reported results for first quarter to that point, 80% had reported earnings per share above estimates, which was greater than the five-year average of 77%.

As we write, about half of the STOXX 600 companies in Europe have reported so far and 71% of those have topped analysts’ profit estimates according to Refinitiv IBES data. Typically, one might expect just over half of companies in this index to beat estimates in a quarter.

The question is whether results for the first three months of 2022 reflect the full impact of rising input costs and reduced consumer spending. After all, some businesses are still enjoying a post-pandemic recovery in demand and may also have been able to react to inflation by driving efficiencies.

It will be worth keeping close tabs on the second quarter and first half reporting season to see if earnings can continue to beat forecasts or if mounting inflation and weaker demand start to have a wider negative impact.

Clay at Redwheel says: ‘I think interest rates aren’t going to go up as much as people ultimately fear they might have to, and therefore by the end of this year we’re going to start talking about when they are going to stop raising rates and start cutting them again. The backdrop has plateaued. We’ve had the worst of it.’

WHAT SHOULD INVESTORS DO?

Many readers will be nursing portfolio losses but it is important not to panic. It is worth having a good look at your investments and if any specific holding has performed very poorly, particularly if it has fallen more than the 13.4% year-to-date decline in the MSCI World, then it is worth taking a good look at why.

However, unless anything fundamental has changed on an individual investment then it is worth staying invested and riding out the volatility if you have time on your side. Time in the market is better than trying to time the market.

Asset manager BlackRock found that if you had invested a hypothetical $100,000 in the S&P 500 index of US stocks between 1 January 2001 and 31 December 2020 you would be sitting on $424,760 if you stayed invested but by missing just the best five days that number dropped to $268,277. Often the best days follow some of the very worst.

One way of smoothing out the impact of volatility and remaining invested in the markets is to invest regularly. By doing so you benefit from an effect called pound cost averaging.

When markets rise, a monthly contribution buys fewer shares or units in a fund. When markets fall the same contribution buys more shares or fund units.

In terms of what you should invest in, Fidelity’s Andrew McCaffery says: ‘We believe focusing on high quality companies, rather than sector selection, is the best approach given the rising geopolitical and stagflation risks.

‘Companies with pricing power and the ability to protect margins should perform relatively strongly in this environment. Equities should still provide a robust source of income, now that balance sheets have been repaired following the worst of the pandemic.’

Please check in again with us soon for further relevant content and news.