Please see below a Weekly Market Commentary, received from Brooks Macdonald, yesterday evening – 10/05/2022

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Pensions, particularly Workplace Pensions, are quite often considered to be confusing. Please see Tom Selby of A J Bell’s article below explaining a little about Auto-Enrolment contributions.

A reader wants to know why the sums don’t add up with retirement savings

Thursday 05 May 2022 Author: Tom Selby

I’m being automatically enrolled into a workplace pension scheme and was told this would be 8% of my salary. However, I’ve just done the sums and my contribution works out less than this – can this possibly be right? I also have a friend who hasn’t been auto-enrolled at all. Are we being shafted by our employer?

Spencer

Tom Selby, AJ Bell Head of Retirement Policy says:

Under auto-enrolment rules, all employers, regardless of size, are required to enrol staff in a pension scheme and pay a minimum level of contributions.

The reason for the reforms was simple – millions of people weren’t saving for retirement. While lots of organisations had a pension scheme, this wasn’t a legal requirement. Even where there was a scheme, plenty of employees simply didn’t join.

Auto-enrolment was first introduced in 2012 for the UK’s largest employers, with medium and smaller employers brought in and contributions scaled up until 2019.

AM I BEING SHAFTED?

While I cannot rule out the possibility your employer isn’t playing by the rules, the answer is likely a lot simpler.

Under auto-enrolment legislation, employees are required to contribute a minimum of 4% and employers 3%, with a further 1% coming via basic-rate tax relief – taking the total to 8%. Employees have the option to opt out of the scheme if they want to, although they miss out on the employer contribution if they do.

However, the minimum requirement is 8% of ‘band earnings’ rather than 8% of total earnings. For 2022/23, the earnings that qualify for minimum auto-enrolment contributions are those between £6,240 (the lower earnings limit for National Insurance contributions) and £50,270 (the upper earnings limit).

Take, for example, someone earning £20,000 a year. If their 8% contribution was based on their total earnings, they would expect £1,600 in total to go into their pension during the 2022/23 tax year.

But if the contribution is based on band earnings, then it will be 8% of (£20,000 – £6,240), which is £1,100.80.

WHAT ABOUT MY FRIEND?

There are various legitimate reasons your friend might not have been auto-enrolled.

If they are under 22 years old or over state pension age (66) then they will not qualify for auto-enrolment, although they have the option to opt-in.

If they have earnings below £10,000 (the auto-enrolment earnings ‘trigger’) they also will not qualify for auto-enrolment, although again they have the option to opt-in if they want to.

Furthermore, employers have the option of not auto-enrolling new joiners for the first three months of their employment.

As an IFA & Employee Benefit Consultant, and an employer, I understand both the value of pensions and how we need to clearly communicate with staff about pensions and employee benefits. Pension contribution rates can make a significant difference over time to the value of your total pension funds on retirement. And whether or not you can afford to retire early!

Communication can be key. Employees need to know what pension provision they have got, what they might need to retire, forecast how it may grow, and how they can make up any potential pension fund shortfall.

Please find below, an update on markets, received this morning from Blackfinch – 03/05/2022

Personal insolvencies have reached a three-year high, as the cost-of-living crisis has left more people unable to repay their debts. There were 32,305 individual insolvencies in England and Wales in the first quarter of 2022, according to the Insolvency Service, which was a 17% increase on insolvencies in the previous quarter.

April’s Industrial Trends Survey from the Confederation of British Industry, the first quarterly survey since Russia’s invasion of Ukraine, suggested a sharp fall in confidence from UK manufacturers. Business optimism fell to a net balance of -34% in April, from -9% in January.

The US Federal Reserve’s preferred measure of consumer inflation – the Personal Consumption Expenditures (PCE) price index – hit a 40-year high. It increased 6.6% in the year to March, with energy prices up 33.9% and food up 9.2%.

The US economy shrank unexpectedly for the first time since the initial COVID-19 outbreak. According to the US Bureau of Economic Analysis. US gross domestic product (GDP) in the first quarter of 2022 fell 0.35%, or at an annualised rate of 1.4%.

US consumer sentiment improved in April, according to a University of Michigan survey. Its index of consumer sentiment increased from 59.4 in March to 65 in April, but was still significantly below the 88.3 reported in April 2021. Most of the improvement came from gains of 21.6% in the year-ahead outlook for the US economy and an 18.3% jump in personal financial expectations.

The number of Americans filing new claims for unemployment support fell last week, according to the US Labor Department. There were 180,000 ‘initial claims’ filed, down from 185,000 the previous week, suggesting the jobs market remains solid.

The Eurozone faces stagflation (slowing economic growth and high inflation) after statistics agency Eurostat reported growth slowed to 0.2% in the first quarter of 2022 while inflation hit a record level of 7.5%.

Natural gas prices jumped as much as 20% as Russia’s energy company Gazprom cut gas supplies to Poland and Bulgaria, after both countries refused to pay for gas in roubles.

Consumer confidence in Germany has reached an all-time low, according to analytics firm GfK. Its confidence index, based on a poll of 2,000 Germans, fell from -15.7 in April to -26.5 in May, far worse than expected.

Russia’s central bank lowered interest rates from 17% to 14%. Economists had expected a smaller cut to 15%, but borrowing costs are still much higher than before the Ukraine war.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses

Please see below a positive article received from AJ Bell this afternoon, which reminds us of several things that have improved when it comes to managing our finances.

Whether it’s been tax hikes, the cost of living crisis, or the war in Ukraine, doom and gloom hasn’t exactly been hard to find in April. The downbeat mood around household finances is palpable, and understandably so, with the price of essential items rising so rapidly.

At tough times like these, we find it natural to focus on the problem at hand, and batten down the hatches. But it might also help to cheer ourselves up a bit by remembering the positive developments we have seen in the personal finance arena in recent times.

STRONG STOCKS

Let’s start with the stock market. It’s been a decent period for investors, with £10,000 invested in the average global fund 10 years ago being worth £28,230 today. Even an investment in the spluttering UK stock market would have more than doubled your money, turning £10,000 into £20,360, if you had purchased a typical UK equity fund.

Right now, there are quite legitimate concerns around the valuation of the US tech sector, and the potentially damaging effect interest rate rises and inflation may have on global economic growth.

These issues raise the question of whether a stock market correction is waiting in the wings. This is actually always a possibility, and simply part and parcel of stock market investing. But the good news is that even if share prices take a big tumble, many investors would still be sitting on a healthy profit, thanks to the returns made by the global stock market over the last decade.

FALLING COSTS

The cost of investing has also fallen significantly over the years. 1% used to be a fairly competitive dealing commission for stockbrokers to charge twenty years ago. So on a £10,000 trade, you might pay £100 in dealing fees. Now you’re more likely to pay a flat fee somewhere in the region of £10.

Indeed, some platforms don’t charge any commission for share deals. Annual fund charges have come down significantly over the years too. It’s now possible to invest in a plain vanilla index tracker fund for as little as 0.2% a year, including platform charges.

By way of contrast, consider that when the government introduced stakeholder pensions as a ‘cheap’ option for savers in 2001, the annual charges were capped at what was then a competitive 1% a year, and the funds on offer were largely passive.

PENSION FREEDOMS

Pensions themselves have also made great progress. The pension freedoms introduced in 2015 mean that savers have much more control over how they draw on their pensions, rather than being shunted into an annuity.

As interest rates have tracked lower, and taken annuity rates with them, the pension freedoms have undoubtedly helped many people avoid locking into a low income stream for life. It’s also almost ten years since automatic enrolment was introduced, which requires employers to set up, and pay into a pension for their staff.

Since the reforms were introduced in 2012, the proportion of private sector workers saving in a workplace pension scheme has more than doubled from 32% to 75%.

Critics will say that the 8% total contribution rate doesn’t go far enough to replace the final salary schemes of yesteryear. That may be so, but the cost of final salary schemes simply became unaffordable as life expectancy shot up. That was a good thing of course, but with financial consequences.

Detractors can also point to the fact that automatic enrolment doesn’t do anything for the self-employed, who have to fend for themselves on the pensions front. Again, that’s true, but the numbers show that automatic enrolment has still been a success story, and offers a good foundation from which it can be expanded.

That’s particularly the case when you consider that at the launch of the scheme, naysayers predicted automatic enrolment would simply flop, because workers would just opt out in their droves.

A MENTION FOR ISAS

The humble ISA is also worthy of an honourable mention. It’s a tax shelter that can all too easily be taken for granted. The £20,000 allowance is now extremely generous, and is supplemented by a £9,000 allowance for Junior ISAs too.

That compares to an annual allowance of £7,000 when ISAs were introduced in 1999. We often expect tax allowances to be uprated in line with inflation. Well, if that had been the case for ISAs, the annual allowance would now be just £11,350.

None of this is to whitewash the genuine financial pain that is being felt by people up and down the country, but if you want to read about that you have plenty of options right now. Hopefully some of the positive developments listed above might make you feel a bit more upbeat about the current state of personal finances, if only for a while.

Please check in again with us shortly for further relevant content and market news.

Please find below, an update on markets, received this afternoon from Blackfinch – 25/04/2022

Retail sales fell 1.4% in March, following a 0.5% drop in February, according to the Office for National Statistics, as people cut back on fuel and food spending amid soaring prices. Overall, sales volumes were 2.2% above pre-pandemic levels in February 2020.

2,114 UK businesses became insolvent in March, more than double the figure in March 2021 (999), and 34% higher than the pre-pandemic figure of 1,582 in March 2019.

In April, the Purchasing Managers’ Index (PMI) for the UK services sector dropped materially from March’s 10-month high, while the new orders index plunged to 54.6, down from 60.4 in February. The slowdown also caused firms to slow their pace of hiring; the employment index fell to 55.8 – its lowest level since April 2021 – from 58.4 in March.

The UK government set out 26 new sanctions against Russia over its invasion of Ukraine, including sanctions on military figures and defence companies.

The European Commission’s confidence indicator rose by 1.8 points to -16.9 in the eurozone, and by two points to -17.6 in the wider European Union (EU).

Consumer prices rose at an annual rate of 7.4% in March, rather than 7.5% as previously estimated, according to the EU’s statistics office Eurostat. Energy prices surged 44.4% in March, while unprocessed food cost 7.8% more. Even after stripping out these volatile components, annual inflation reached 3.2% in March, well above the European Central Bank’s 2% target.

Production in the 19 eurozone countries rose 0.7% in February from January, according to Eurostat. The biggest monthly increases were in Italy (up 4%), Croatia (up 2.7%) and Ireland (up 2.4%).

The International Monetary Fund (IMF) downgraded global growth forecasts with 2022 gross domestic product (GDP) growth revised to 3.6%, down from January’s prediction of 4.4%.

The IMF said UK economic growth was expected to match growth in US during 2022, but will slump in 2023, taking the UK to the bottom of the league table of comparable economies in the G7 group of countries. The UK is also expected to face the highest inflation.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses

Please see below ‘Markets in a Minute’ article received from Brewin Dolphin yesterday afternoon, which provides current market updates on a global scale.

The release last week of the first major US corporate earnings reports of 2022 was accompanied by a lacklustre few days for global equities.

In Europe, the STOXX 600 and the Dax ended their holiday-shortened trading week down 0.3% and 0.8%, respectively, as data from the US and UK showed a further spike in inflation. The FTSE 100 fell 0.7% as energy stocks declined and the pound strengthened against the dollar.

The S&P 500 tumbled 2.1% as disappointing retail sales figures and concerns about inflation weighed on investor sentiment. The financials sector underperformed after first quarter results from banking giant JPMorgan Chase missed analysts’ estimates.

In Asia, Japan’s Nikkei 225 added 0.4% after Bank of Japan governor Haruhiko Kuroda said the economy would continue to recover despite surging commodity prices. China’s Shanghai Composite declined 1.3% as cases of Covid-19 continued to climb in Shanghai, fuelling concerns about supply chain disruptions.

IMF cuts global growth forecast

Stocks were mixed on Tuesday (19 April) as traders returned from the Easter long weekend. The FTSE 100 ended the trading session down 0.2% after the International Monetary Fund (IMF) slashed its forecasts for global gross domestic product (GDP) growth to 3.6% for 2022 and 2023, down from 4.4% and 3.8% previously. The IMF said global economic prospects had been severely set back, largely because of Russia’s invasion of Ukraine. The UK is set to be the worst performing G7 economy year, with GDP increasing by just 1.2% amid the rising cost of living and tax increases.

The STOXX 600 also declined on Tuesday, whereas Wall Street stocks made solid gains as investors digested a slew of corporate earnings. The FTSE 100 took its cue from Wall Street to start Wednesday’s trading session up 0.1%.

US retail sales miss forecasts

Last week saw the release of the latest US retail sales figures, which revealed sales in March rose by just 0.5% month-on-month. This was the slowest pace in 2022 so far and lower than the 0.6% increase forecast in a Reuters poll.

The bulk of the increase was driven by sales at service stations, which surged by 8.9%. This came after prices at the pump soared to an all-time high amid Russia’s war against Ukraine (US retail sales are not adjusted for inflation). Excluding gasoline, retail sales fell by 0.3%.

The report from the Commerce Department also showed online store sales fell by 6.4% after declining 3.5% in February, the first back-to-back fall since the last two months of 2020.

US import prices accelerate

US import prices rose by the most in over a decade in March as the Russia-Ukraine war increased petroleum prices. Import prices rose by 2.6% from the previous month, the largest rise since April 2011, according to the Labor Department. On an annual basis, prices surged by 12.5% after advancing 11.3% in February.

This came after data showed consumer prices rose at their fastest rate for 41 years in March, increasing by 8.5% year-on-year. Meanwhile, producer prices rose by 1.0% in March from the previous month, roughly double estimates, and by a record 9.2% year-on-year.

With inflationary pressures persisting, investors will be keeping a close eye on this week’s speeches from Federal Reserve officials for any further guidance on how aggressively policymakers will raise interest rates this year.

UK inflation hits 7%

Here in the UK, inflation hit a fresh 30-year high in March as fuel prices surged. Consumer prices rose by 7.0% year-on-year, up from 6.2% in February and ten times the 0.7% increase seen in March 2021, according to the Office for National Statistics. Transport fuel prices surged by 30.7% from a year ago, and prices of other items such as furniture, cooking oil, clothing, second-hand cars and hotels all rose at a double-digit annual rate. Core inflation, which excludes energy, food, alcohol and tobacco, rose by 5.7% year-on-year.

The figures could add further pressure on the Bank of England to accelerate the pace of interest rate increases. The Bank has increased the base rate three times since December from 0.1% to 0.75%. Its next monetary policy decision is scheduled for 5 May.

China’s economy slows in March

China’s economy slowed in March after a strong start to 2022. Data from the National Bureau of Statistics revealed GDP grew by 4.8% in the first quarter from a year ago, beating expectations for a 4.4% gain and above the 4.0% growth seen in the fourth quarter of 2021. However, figures for March showed annual retail sales fell by the most since April 2020, down 3.5%, as coronavirus restrictions were imposed across the country. The jobless rate rose to 5.8%, the highest since May 2020.

The Chinese government is sticking to its zero-Covid policy despite growing fears about the hit to the economy. Fu Linghui, a spokesperson for the National Bureau of Statistics, warned of “frequent outbreaks” of Covid-19 in China and an “increasingly grave and complex international environment”. On Monday, China’s central bank said the country would step up financial support for industries, firms and people affected by coronavirus outbreaks. It has published a list of 23 measures that include lending guidance for banks, general pledges for more credit or other financial support, and making it easier for companies to expand the crossborder use of the yuan.

Please check in again with us shortly for further relevant content and news.

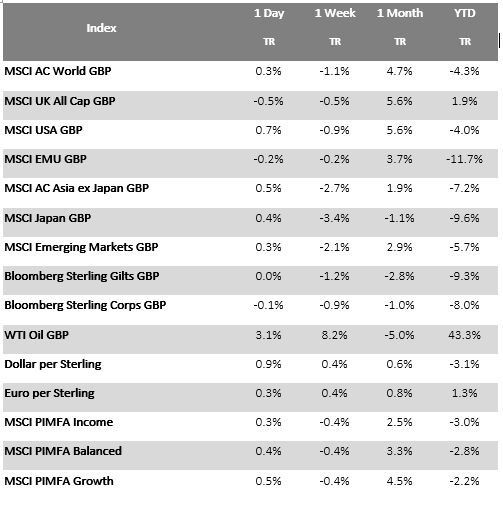

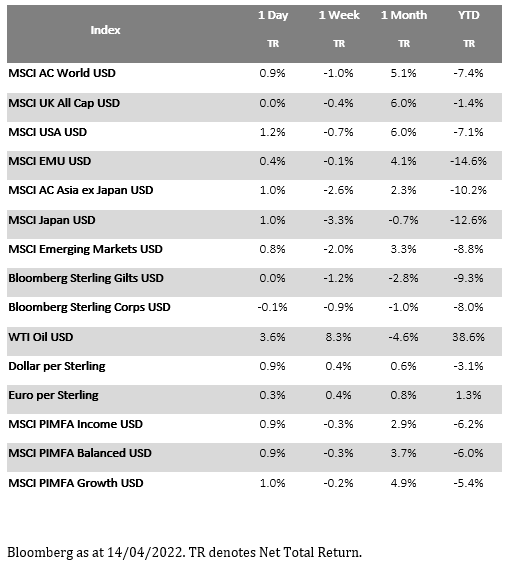

Please see article below from AJ Bell received on Thursday afternoon – 14/04/2022.

How much will I get from the state pension?

A reader in their 60s also wants to know about pension credit

Thursday 14 Apr 2022 Author: Daniel Coatsworth

I’m 62 and have worked all my life, what am I likely to receive from the state from age 66 and how does pension credit work?

Sonia

Tom Selby, AJ Bell Head of Retirement Policy says:

The full flat-rate state pension is worth £185.15 in 2022/23 and you will qualify for it when you turn 66. In order to qualify for the full amount, you need a 35-year National Insurance contribution record.

You need at least a 10-year NI record to qualify for any state pension, with a deduction made for every year of missing NI you have. Once you have a 35-year NI record you cannot build up any more state pension entitlement.

The state pension system was reformed in 2016, meaning millions of people built up rights under a combination of the old system and the new system.

Anyone who built up state pension entitlements under the old system and hadn’t reached state pension age before 6 April 2016 has a ‘foundation amount’ calculated.

Anyone with a foundation amount equal to the full flat-rate state pension at 5 April 2016 would not have been able to build up any extra state pension – even if they added more qualifying years to their National Insurance contributions record.

Those with a foundation amount below the full flat-rate state pension could continue to build up qualifying years via NI contributions and boost their state pension entitlement.

People with a foundation amount worth more than the flat-rate state pension would receive the full flat-rate amount plus a ‘protected payment’ to reflect the extra entitlement built up under the old system. They would not gain any extra pension for further qualifying years they accrue.

Use this link to check your state pension entitlement.

Crucially, it is up to you to claim your state pension from the DWP.

Note that the state pension age is scheduled to increase to 67 by 2028 and 68 by 2046 – although a review of the state pension age is underway and due to be completed in 2023.

PENSION CREDIT

Pension credit is another key benefit provided by the state which tends to go unclaimed by lower income retirees.

In 2022/23, if you are over state pension age (66), single and your income is less than less than £182.60 a week then pension credit will top you up to that amount. For a couple, the combined income figure is £287.70.

In relation to pension credit your income includes your state pension, other pensions, employment or self-employment earnings and most social security benefits. As with the state pension, it is up to you to claim pension credit.

Please continue to check back for our latest blog posts and updates.

Please find below, a daily update on markets, received this morning from Brooks Macdonald – 14/04/2022

What has happened?

US bond prices continued the recent rally on Wednesday as markets pared back expectations for an aggressive series of interest rate rises from the US Federal Reserve. Following the latest US Consumer Price Index data for March published on Tuesday, which showed a weaker than expected core month-on-month rise in prices, hopes have risen that the near-term inflationary pressures might be at or near a peak. US 2 year bonds, which are more sensitive to monetary policy decisions, have seen yields fall more than 10 year yields this week, with the 10 year-less-2 year yield curve having risen around 40bps since the nadir at the start of the month. In equity markets, the principle of regional proximity to the Ukraine conflict weighed again on Wednesday; while equities were mixed in Europe, US equities were stronger, while across sectors, technology shares outperformed wider equity benchmarks. Overnight, Asia equity markets are broadly higher on reports that China’s policy makers may look to make further cuts in banks’ reserve requirement ratios alongside other policy tools to support the economy. Looking ahead to today the European Central Bank (ECB) holds its latest monetary policy meeting decision, though markets are not expecting much change to the ECB’s recently more hawkish messaging.

US calendar Q1 2022 company results season gets underway

The US bank JP Morgan kicked off the latest calendar Q1 2022 company results season on Wednesday. Seen as a bellwether for the broader US economy, JP Morgan reported profits which fell 42% in Q1 2022 compared to the same quarter period a year ago, and missing analyst EPS estimates amid a more cautious outlook generally. Aside the market impact from Russia’s invasion of Ukraine, investment banking revenue was lower as companies looked to have delayed deal activity in recent months. The US bank also increased reserves saying the possibility of an economic downturn had moved from ‘low’ to ‘slightly less low’. JP Morgan CEO Dimon warned of twin economic uncertainties arising from Ukraine as well as near-term inflationary headwinds. Putting pressure on policy makers, Dimon said “we remain optimistic on the economy, at least for the short term … consumer and business balance sheets as well as consumer spending remain at healthy levels … but see significant geopolitical and economic challenges ahead”. He added that “the Fed needs to try to manage this economy and try to get to a soft landing, if possible.” Asked whether the US could face a recession, Dimon said that “I am not predicting a recession. Is it possible? Absolutely.”

Brooks Macdonald’s Asset Allocation Committee weighs up the investment outlook

Brooks Macdonald’s Asset Allocation Committee held its latest monthly meeting on Wednesday, and as part of discussions, weighed up the latest investment outlook in terms of the twin market drivers of economic growth and inflation. While the broader economic growth outlook remains constructive and above longer-term trend rates of growth, the Committee are mindful that there has been a downward revision of estimates in aggregate. The Committee views a lower economic growth backdrop as likely given the impact that near-term inflationary pressures may have on the cost-of-living squeeze and corporate margins. Whilst it is too early to say whether inflation will slow meaningfully by the end of the year, the base effects mean that headline inflation is likely to slow even if inflationary pressures remain a theme into 2023.

What does Brooks Macdonald think?

Our Asset Allocation Committee is, in aggregate, presently somewhere between a so-called ‘Soft-Landing’ scenario (describing a low inflation, low economic growth outlook) and a ‘Stagflation’ scenario (high inflation, low growth). Whilst both of these scenarios might favour more growth/defensive investment styles, the Committee is maintaining its equity barbell balance at the current time. There is likely to be continued volatility in markets in the near-term as central banks in particular look to try to thread the policy needle against post-pandemic distortions and the war in Ukraine, and as such, we are keen not to be drawn prematurely in favour of either a growth/defensive or value/cyclical narrative.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses

Please find below, a market update received from Blackfinch Group this morning – 11/04/2022

UK gross domestic product (GDP) rose just 0.1% in February, 0.2% less than economists expected. The UK economy is now around 1.5% larger than just before the UK’s first lockdowns two years ago, according to the Office for National Statistics.

The three storms, Dudley, Eunice and Franklin, which hit the UK in mid-February weighed on the construction sector, leading to a 0.1% drop in output.

UK house prices continued to surge in March, lifting the average house price to a new record high of more than £282,000. Since the first pandemic lockdown began two years ago, the average UK house price has jumped 18%, or £43,577.

UK households and businesses were hit by the biggest monthly jump in motor fuel prices in at least two decades. Average UK petrol and diesel pump prices increased by 11p and 22p per litre respectively in March, according to the RAC’s Fuel Watch.

The number of Americans filing for unemployment benefits fell to just 166,000, the lowest figure since 1968, according to the US Labor Department.

In the US, the total volume of mortgage applications fell another 6% last week, according to the Mortgage Bankers Association’s seasonally-adjusted index. This left mortgage applications 41% lower than one year ago.

In the Republic of Ireland, inflation as measured by the Consumer Price Index (CPI) jumped 6.7% in the year to March 2022, the highest annual inflation rate since November 2000.

German manufacturing orders fell by an unexpected 2.2% in February, in the run-up to Russia’s invasion of Ukraine. The decline, which was led by a drop in overseas orders, was much worse than economist forecasts of a 0.3% fall.

In Turkey, inflation soared to 61.1% in March, its highest reading since 2002 as rising energy and commodity costs intensified Turkey’s cost-of-living crisis.

As the UK Foreign Office joined the US in announcing sanctions on Vladimir Putin’s two adult daughters, it said it expects Russia’s GDP this year to contract by between 8.5% and 15%. Around £275bn, or 60% of Russian foreign currency reserves, are currently frozen, which has hampered Moscow’s ability to support its economy.

Russian consumer prices jumped 7.61% in March alone, the fastest monthly increase in inflation since 1999. Annual CPI inflation rose 16.69% in year-on-year terms in March, sharply up on February’s 9.15%.

The United Nations’ Food and Agriculture Organization (FAO) reported that world food prices reached record highs in March as the war in Ukraine drove up prices. The FAO’s food prices index rose nearly 13% in March, adding to global inflationary pressures.

Global trade fell 2.8% between February and March as Russia’s invasion of Ukraine hit imports and exports, according to the Kiel Institute of the World Economy.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses

Please find below an article on the increase in student loan repayments, received from AJ Bell, yesterday evening – 07/04/2022

Chancellor Rishi Sunak has announced a shake up of the student loan system, which will make it more expensive for people to go to university and mean graduates are paying off their loans for up to 40 years after they leave university.

Graduates and potentially their parents may be left wondering if there’s a case for taking action to pay off borrowings as early as possible in light of these changes.

The modified rules extend the period until your loan is wiped out from the current 30 years up to 40 years. It means someone who graduates when they are 21 could be paying off their loan until they are 61.

The next big change is that the threshold at which you start repaying your loan has reduced from the current £27,295 down to £25,000. However, one help for graduates is that the interest on the loan will be simplified to be just the current rate of RPI inflation, where currently it’s charged at RPI plus up to 3%, varying by your income.

REPAYMENTS GOING UP

However, the combined impact of these changes mean that many graduates will repay more than double what they currently do. For example, someone who graduates with £45,000 of debt on a starting salary of £30,000 a year will currently pay back £30,900 in total, assuming their salary increases by 3% a year. Under the new system they will repay £71,518 – so almost £27,000 more than they borrowed thanks to the impact of interest over the 40-year term of the loan.

Someone who starts on a lower graduate salary of £20,000 will pay back £7,207 under the new system, whereas previously they wouldn’t have repaid any of the loan as they would never have earned enough to get over the income repayment threshold.

However, the changes do benefit higher earners, who will pay off their loan faster and so incur less interest over the term of the loan, but also benefit from the lower, flat-rate interest under the new system. For example, someone on a starting salary of £50,000 (on the same debt and salary increase basis as above) would pay off almost £117,000 under the current system, but only £62,000 under the new system. Of course, few graduates will start on such a high salary.

SO IS IT BETTER TO PAY OFF THE LOAN STRAIGHT AWAY?

Parents who have a lump sum they could use to pay off the debt will now be wondering whether it’s better to pay off the loan as soon as their child graduates (or just not take out the loan in the first place and use that pot of money to pay for their child’s university education) or whether they leave their child to pay off the loan through their salary. However, it’s not an easy calculation and relies on some big assumptions about your child’s future earning potential.

The first thing to note is that student loan debt is not the same as other debt – you don’t have to pay it if you have no income, or your income falls below the new £25,000 a year threshold. So, if you take time out, a career break or work part-time on a lower salary, you wouldn’t be liable to pay it. It also doesn’t count on your credit file as debt like that volume of credit card debt would, for example.

Regardless, many graduates won’t want their university debt following them around for 40 years if they can help it. And, as you repay your debt at a rate of 9% of any income over the £25,000 threshold it means that graduates have a 42.25% effective tax rate over this income level (20% basic rate tax, 13.25% National Insurance and 9% student loan repayments). That could significantly impact their ability to save money for a house deposit, for example, or to live the lifestyle they want.

However, whether it’s worth paying off the loan hinges on what your child is likely to earn. Someone with £45,000 of debt on a starting salary of £25,000 who sees a steady 3% a year increase in their salary will repay just over £36,000 in total over the 40 years. That’s obviously much less than the amount they initially borrowed and so means it wouldn’t be worth paying off the debt when they graduate. However, a small increase in their starting salary to £30,000 changes the figures entirely, as they would pay off just over £71,500, far more than the initial debt.

ACCOUNTING FOR PERSONAL CIRCUMSTANCES

These scenarios don’t account for any career breaks, due to having children, going back into education or travelling, where the graduate would make no repayments. And nor do they account for big increases in salary, due to promotions or switching jobs. And both these factors can dramatically impact the sums.

Let’s take that person starting on £30,000, with £45,000 of debt and a gradually rising salary. If they took a five-year career break early on in their career and then resumed work on their previous salary their repayments will reduce to just more than £40,000.

Now take that same individual starting on £30,000 with no career break but instead they get three pay rises of £5,000 each in years five, 10 and 15 of their career – now their repayments rocket to almost £104,000 – meaning that it would have made financial sense to pay off the loan when they graduated.

As these figures highlight, there’s no easy answer. Some of it will come down to the career your child picks and their likely future choices around career breaks, and some may come down to whether that’s the best use of the lump sum you have sitting around.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses