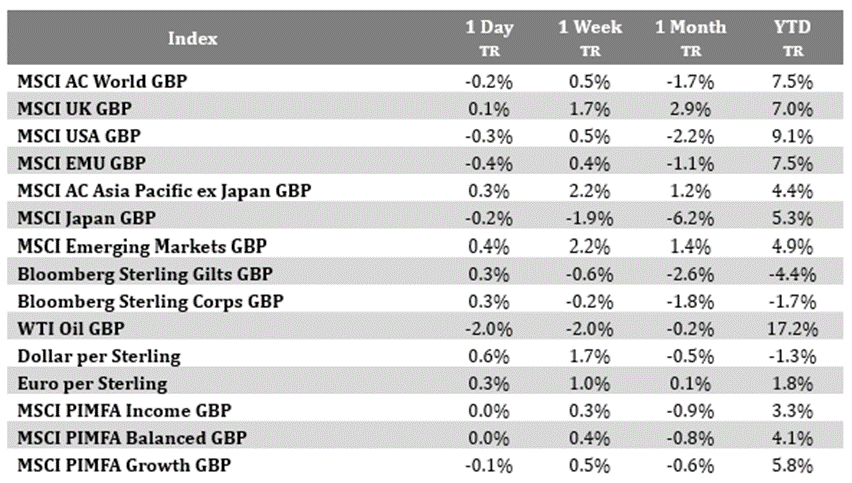

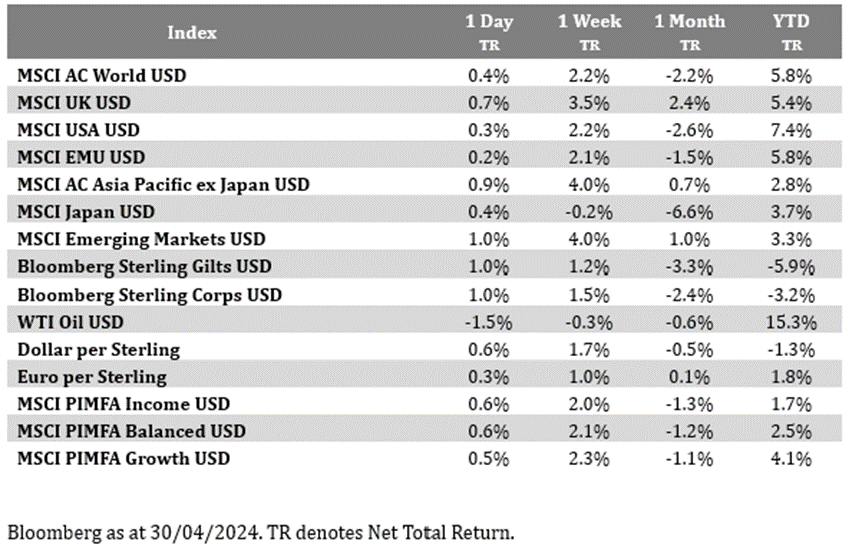

Please see below today’s Daily Investment Bulletin from Brooks Macdonald, which was received this morning (30/04/2024):

What has happened

Equities had a solid-enough start to the week on Monday, with a so-far-respectable Q1 earnings results season edging out concerns that central banks might have to keep interest rates higher for longer in the battle against the risk of still-sticky inflation pressures. In stock news, Tesla, one of the so-called ‘Magnificent 7’ group of US megacap technology companies saw its share price close up +15.3% after news reported by Bloomberg that it had cleared key regulatory hurdles to unlock more autonomous driving technology for its cars in China. Elsewhere, overnight, Samsung Electronics has topped earnings estimates for calendar Q1 after its semiconductor division returned to profitability.

Japanese yen rebounds

The Japanese yen saw some big swings on Monday. After touching its weakest level versus the US dollar in 34 years, the yen staged a decent rebound, with speculation that authorities in Japan had intervened to support the currency. Intraday, after briefly weakening through an exchange rate of 160 to the US dollar, the yen rallied. The day’s trading range of around 160.25 – 154.5 was the widest one-day trading range since late 2022. Japan’s top currency official, Masato Kanda, yesterday declined to comment specifically as to whether or not policy makers had intervened but did add that “we cannot overlook the negative impact that excessive and abnormal foreign exchange fluctuations driven by speculation are having on the nation’s economy … so we will continue to take appropriate measures as necessary.” For context, the Japanese yen is the worst performing G10 currency (group of ten major currencies globally) year-to date, down around -10% against the US dollar.

Oil prices fall as markets weigh up renewed Middle East peace hopes

Brent crude oil prices were down -1.2% to $88.40 per barrel yesterday, as investors weighed up the chances for renewed Middle East peace hopes. The US has been trying to broker a peace deal between Israel and Hamas, with the US Secretary of State, Antony Blinken, visiting the region again on Monday – his seventh visit to the region since the Israel-Hamas war started last October. Blinken boosted peace hopes, saying that Israel had been “extraordinarily generous” in its proposals during talks mediated by Qatar and Egypt, adding that Hamas “have to decide quickly.”

What does Brooks Macdonald think

In commodity markets, the copper price was up +1.7% yesterday, and back up above US$10,000 a ton, at around 2-year highs. The latest copper price rise has come on the back of the recent news in the past week that BHP, the world’s biggest mining group is seeking to acquire Anglo American in an all-share offer. More generally, the rise in the copper price this year (up around 18% year-to-date in US$ terms) is in part reflecting growing concerns around a future where supply constraints are increasingly coupled with structural demand growth. As regards supply, copper production from existing mines globally is forecast to fall sharply in the coming years according to industry research group CRU – they estimate that miners globally in aggregate would need to spend more than US$150 billion between 2025 and 2032 to fulfil the industry’s copper supply needs.

Please continue to check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Carl Mitchell – DipPFS

Independent Financial Adviser

30/04/2024