Please see the market update below received this morning from Brooks Macdonald – 19/05/2022

What has happened

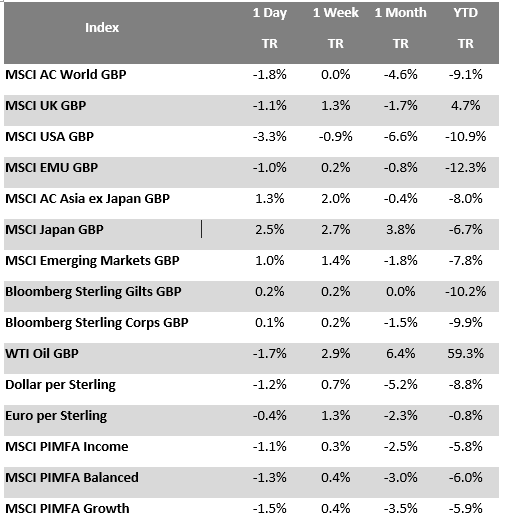

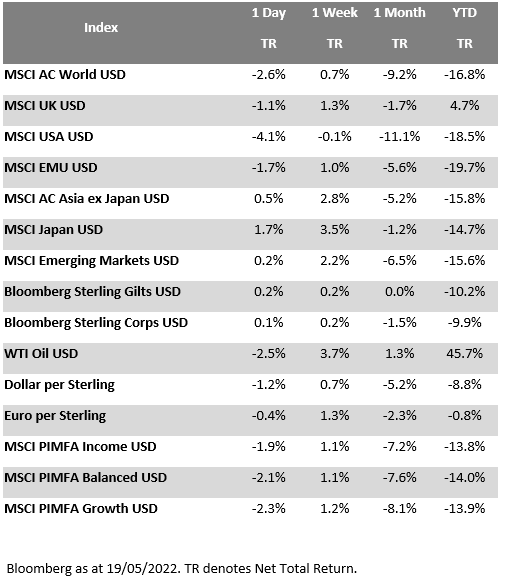

The bounce in global equities that had buoyed sentiment on Tuesday, faded fast on Wednesday. Selling the previous day’s rally, investors seemed to focus back on concerns around near-term inflation pressures in particular. In company news, US general merchandise retailer Target missed estimates and the shares fell around 25%, but rather than a read on the health of the US consumer in aggregate, it looked more about the impact of a consumer shifting away from pandemic-driven elevated goods spend, which hit Target’s sales of goods outside of its grocery lines, such as TVs and kitchen appliances. Also on Wednesday, UK CPI data showed inflation rose to 9% Year on Year in April, slightly below a consensus estimate of 9.1%. Boosted by the 1st April rise in the energy price cap, the headline inflation rate reached a 40 year high. In currency markets, Sterling fell versus the Dollar on concerns that the Bank of England might have to tread more carefully around near-term inflation pressures, in order to guard against longer-term economic growth risks.

US retailer Target delivers an off-target negative surprise

US general merchandise retailer Target reported 1Q earnings on Wednesday, but missing estimates the stock fell around 25%. While the retailer was impacted by higher costs (including fuel costs), and supply chain troubles, the dominant impact seemed to be the company caught by a bigger than expected consumer shift out of goods (especially durable goods) such as TVs and kitchen appliances, that had done well during the pandemic, leaving the company overstocked and forced to mark down prices. Without stimulus cheques fuelling spending, combined with a return to more normal consumption patterns as consumers move back towards services, this was seen as a factor the company. As the Target CEO Cornell said on Wednesday, “three core merchandise categories, apparel, home and hardlines, we saw a rapid slowdown … while we anticipated a post-stimulus slowdown and we expected consumers to continue refocusing spending away from goods and into services, we didn’t anticipate the magnitude of that shift.”

Markets caught in an investor sentiment tug-of-war

Markets are caught in an investor sentiment tug-of-war battle at the moment, but relatively high levels of market volatility are likely to be with us for a while yet. For central banks, the challenge is getting the balance right between taming near-term inflation pressures while not impacting longer-term economic growth, but it’s a challenge that’s fraught with difficulty. With US Fed Chair Powell hoping for a “softish landing” and UK BoE Governor Bailey seeing a “narrow path” between the risks of inflation and growth, the question as to whether central banks can successfully thread-the-needle on policy unfortunately has no short-term answer.

How is the inflation picture shaping up?

The inflation picture is rightly dominating investors’ attention, but it can be unpacked into a number of different drivers currently. COVID has created price ‘disruption’ as a result of the post-pandemic restart and the imbalance in supply chains between both goods and services as well as demand and supply. War in Ukraine this year has complicated the inflation picture, adding significant price ‘shocks’ to energy and food in particular. But price ‘disruption’ and price ‘shocks’ are not enough by themselves to kick-start a multi-year inflation process. For that a necessary component would be a significant and sustained rise in inflation expectations (including wage expectations). However, analysis last week from the Peterson Institute for International Economics suggests that the big news in the US April jobs report published earlier this month was a potentially slowing wage growth picture. Looking at US average hourly earnings, the annualized rate of growth (once adjusted for compositional changes in the labour force), was 3.8% over the past three months, a pace considerably slower than in 2021, which saw peaks around 7%.

What does Brooks Macdonald think?

At Brooks Macdonald, we recognise that the current inflation picture is complex and multifaceted. On balance, we expect the current high inflation rates to start to ease over the remainder of this year and into 2023 – but how quickly (and how far) inflation drops back (as well as the impact to economic growth further out from interest rate hikes in the interim), remain difficult to gauge. Ultimately, it’s one of the reasons why, within equities, we continue to hold to our barbell balance between growth/defensive and value/cyclical investment styles at the current time.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

David Purcell

19th May 2022