Please find below, a Daily Investment Bulletin received from Brooks Macdonald this morning – 19/08/2022

What has happened

Amidst a quieter day for equities and bonds, European and US equity markets managed to hold on to small gains as bond yields remained steady despite a large volume of central bank speak.

Ukraine war

There were some progress around peace negotiations between Russia and Ukraine yesterday with Turkey playing the role of intermediary between the two parties. Alongside President Zelenskiy and President Erdogan, UN Secretary General Guterres joined the talks in Lviv. Turkey are now set to consider launching talks with President Putin as reports suggested that both sides were open to establishing diplomatic channels albeit via the proxy of Turkey for the time being.

Central banks

The ECB started the day with some more hawkish speakers setting the tone. ECB board member Schnabel began, suggesting that inflation may continue to rise in the short term and that the ECB’s view of inflation risks is yet to change as ‘I do not think this outlook has changed fundamentally’. It was a similar tone from the ECB’s Kazaks who said that the ECB will ‘continue to increase interest rates’ to bring inflation expectations under control. The market is pricing in 50bps of ECB rate rises at the next meeting in September. Over in the US, there was a range of opinions on the next steps for Fed interest rates at the September meeting. President Daly backed a 50bp move whilst President Bullard supported 75bps and President George spoke more of the risks of inflation complacency. President Kashkari discussed the possibility of a soft landing, admitting that he didn’t have a high level of confidence that the Fed would be able to achieve that nirvana.

What does Brooks Macdonald think?

The tone from both the ECB and Fed were similar yesterday, a reiteration of the need to bring inflation under control and a willingness to hike rates to achieve that outcome. Of course, their domestic inflation and economic paths are likely to be very different therefore the Fed’s desire is probably more focused on convincing the market that future inflation expectations should be close to target. The next major central bank event will be the Jackson Hole symposium next week with Fed Chair Powell speaking on Friday.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see the below article from Brooks Macdonald highlighting the key factors influencing markets around the world, as well as offering their take regarding the effect on future investments. Received late this morning – 18/08/2022

What has happened?

An upside beat to UK CPI and some hawkish central bank messaging from the central bank of New Zealand led risk appetite to reverse yesterday with European equities falling by almost 1% and the German index falling by over 2%. Over in the US, longer duration equities underperformed with the US technology index giving back some of the strong gains of the last week.

UK CPI

The UK inflation release was the early catalyst for the more sombre mood in equities yesterday. UK CPI rose to 10.1% in July versus market expectations of 9.8%. This release prompted two conclusions within bond markets, a confirmation that the path of European and US inflation is likely to diverge and secondly that the Bank of England will need to become even more aggressive on rate rises. The market now expects 50bps of rate rises at each of the three remaining meetings in 2022, aggregating to a total rise of 1.55% from the current base rate. UK government gilts also saw their yields climb as a stickier inflation backdrop and tighter monetary policy was priced into the market. Double digit inflation in the UK may prove a psychological threshold for consumers but makes it difficult for the Bank of England to focus on the rising economic growth risks.

FOMC Minutes

Whilst the tone yesterday was very much risk-off, the Federal Reserve meeting minutes were viewed more constructively by investors. The minutes showed that the committee was aware of the risk that they will over tighten policy given the time lag that interest rate hikes and quantitative tightening have in feeding through to the real economy. This risk of monetary policy overshoot would be particularly acute if the August CPI release shows a further slowing in headline CPI after the July miss. The minutes also reiterated the message from the Fed that ‘it likely would become appropriate at some point to slow the pace of policy rate increases’.

What does Brooks Macdonald think?

Given the August Fed break, we have another round of economic data, including CPI and the US jobs report, before the next Fed meeting in September so plenty could change however the US does look in a very different place to Europe. It was the realisation that a US CPI miss was not a global panacea that led to yesterday’s retrenchment and it could mean that equity gains from here are more regionally selective.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below ‘Markets in a Minute’ article received from Brewin Dolphin yesterday evening, which provides a global market update with reference to the current economic position in the US and China.

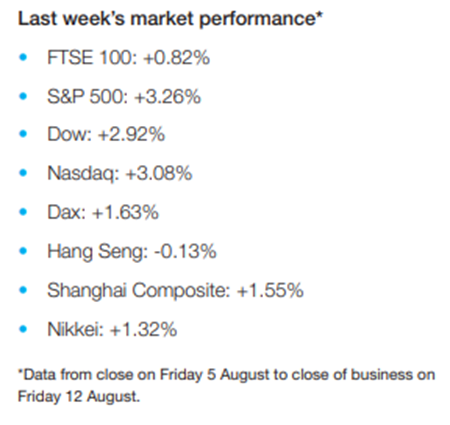

Most major stock markets rose last week as data suggested the rise in US consumer prices may have peaked.

The S&P 500, Dow and Nasdaq surged 3.3%, 2.9% and 3.1%, respectively, as lower-than-projected inflation figures led to renewed optimism that the Federal Reserve will raise interest rates at a less aggressive pace.

Stocks in Europe rallied as industrial production in the eurozone rose by more than expected. Germany’s Dax added 1.6% and France’s CAC 40 gained 1.3%. The FTSE 100 climbed 0.8% as data showed UK gross domestic product (GDP) fell by less than feared in June.

Investor sentiment was also strong in Japan, where the Nikkei added 1.3%. The reshuffling of Japan’s Cabinet signalled policy continuity, with top figures retained in key posts. The Shanghai Composite advanced 1.6% on news China’s trade surplus rose to a new record of $101.3bn for the month July, surpassing the $100bn threshold for the first time ever.

China’s economic data disappoints

Stocks started this week in the green, with the FTSE 100 and S&P 500 edging up 0.1% and 0.4%, respectively, on Monday (15 August). Gains were held back by disappointing manufacturing and retail sales data from China. Industrial production rose 3.8% year-on-year in July, below the 3.9% expansion in June and a 4.6% increase forecast by analysts in a Reuters poll. Retail sales rose 2.7% year-on-year, below the 3.1% growth in June and forecasts for 5.0% growth. China’s central bank responded by lowering interest rates on key lending facilities for the second time this year.

The FTSE 100 rose 0.4% at the start of trading on Tuesday as investors digested the latest UK jobs data. According to the Office for National Statistics (ONS), the real value of workers’ pay dropped by 3.0% in the three months to June, the fastest rate since comparable records began in 2001, as wage increases were outstripped by inflation. Unemployment rose by 0.1 percentage points to 3.8% and the number of new job openings fell for the first time since summer 2020.

US inflation moderates slightly

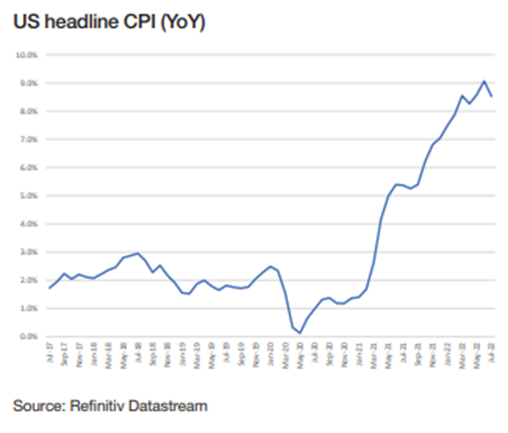

Figures released last week raised hopes that inflation in the US has peaked and started to decelerate. On a monthly basis, the US consumer price index (CPI) was unchanged in July as a fall in gasoline prices offset increases in shelter and food. Food prices rose by 1.1% over the month, whereas gasoline prices declined by 7.7%. On annual basis, CPI eased to 8.5% in July from 9.1% in June, below economists’ expectations of 8.7%. Core CPI – which excludes volatile food and energy prices – was unchanged at 5.9% year-on-year.

Nevertheless, San Francisco Federal Reserve Bank president Mary Daly said it was too early for the US central bank to declare victory in its fight against inflation. In an interview with the Financial Times, she did not rule out a third consecutive 0.75 percentage point rate rise at the next policy meeting in September, although she signalled support for the Fed to slow the pace of its interest rate increases.

“There’s good news on the month-to-month data that consumers and business are getting some relief, but inflation remains far too high and not near our price stability goal,” she stated.

Rising prices hit retail sales and confidence

Here in the UK, figures from the ONS showed the UK economy contracted by 0.1% in the second quarter, led by a large reduction in coronavirus activities, such as NHS Test and Trace and lateral flow orders. Real household expenditure also declined by 0.2%, driven by falls in net tourism, clothing and footwear, food and nonalcoholic beverages, and restaurants and hotels.

The decline in GDP was sharper at the end of the quarter, falling by 0.6% in June. However, this was better than the 1.3% contraction forecast by economists and partly reflected the fact that June saw two fewer working days as a result of the Queen’s Platinum Jubilee.

The Bank of England has forecast that the UK will enter into a recession in the fourth quarter of this year, with output falling in each quarter until the end of 2023.

Eurozone industrial production up 0.7%

Industrial production in the eurozone rose by 0.7% in June from the previous month, following an upwardly revised 2.1% increase in May. This was well above consensus expectations for a 0.2% rise. On an annual basis, production expanded by 2.4%, above the 0.8% increase expected by economists. The rise was driven by an expansion in capital goods and energy output, which more than offset declines in consumer goods output, according to Eurostat.

Elsewhere, however, it was reported that droughts in Europe were hindering energy production, agriculture and river transport. According to Sky News, water levels in reservoirs for hydropower are down in nine countries, including Italy, Serbia, Montenegro and Norway. Water levels in Germany’s Rhine River fell to a new low on Friday, further restricting the distribution of coal, petrol, wheat and other commodities.

Please check in again with us shortly for more relevant content and market news.

Please see today’s Brooks Macdonald Daily Investment Bulletin received earlier this morning (16/08/2022):

What has happened

A gloomier economic mood has impacted sovereign bond yields this week with yields falling in both the US and Europe. Against this lower yield backdrop, and despite the poorer economic data, equities rose yesterday in both the US and Europe, building on previous gains.

Economic data

Early on Monday the release of China’s July economic data disappointed the market, showing less momentum than investors had hoped. Industrial production and retail sales both expanded, but by less than expected, and this catalysed another central bank rate cut to help support the economy and financial markets. Over in the US, the Empire State manufacturing survey for August also showed weakness but instead of a positive reading the gauge plunged into negative territory for its worst reading since the financial crisis. The Empire State survey measures business activity in New York State with new orders and shipments both plummeting. Prices paid did fall, and given the fall in new orders, price cutting and discounts are likely to be needed to reduce inventories.

Energy

With lower prices paid set to provide some US inflation relief over the coming months, energy remains a key swing variable. At a headline level, oil prices continue their retreat with WTI below $90 a barrel and Brent falling to levels seen before Russia’s invasion of Ukraine. A fall in demand due to a possible recession is the larger story here however recent moves will also be impacted by the possible return of Iran to global oil supply. The latest developments on the Iran nuclear deal appear to show progress and negotiations between Iran and the EU appear to be gathering momentum. European energy prices remain a standout with prices continuing to rise as heatwaves created issues with fuel transportation and air-conditioning increased energy demand. Should US energy prices continue to decouple from European prices, there could be a very different set of paths for the two economic blocs.

What does Brooks Macdonald think

Financial markets, having been emboldened by the recent weaker-than-expected inflation releases have had a far more risk-on tone in recent weeks. The strong US jobs report also helped sentiment as it raised the prospect that inflation could slow sufficiently to allow central banks to engineer a soft landing from a strong economic starting point. The US jobs report appears to be an exception for the time being however and the weight of poorer economic data is playing through into the bond markets and driving outperformance of growth equity sectors.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below Tatton Investment’s Monday Digest with some interesting analysis of current global market positions. This digest was received this morning (15/08/2022):

Investor FOMO returns

Investors are feeling FOMO: the “fear of missing out” once again. Last week brought a continuation of the trend since early July, with boosts to both bond and equity markets. Curiously, the good feeling among investors seems unaffected by the bad news all around. Inflation is roaring ahead and consumers are struggling to keep up, central banks are intent on crushing price pressures with aggressive monetary policy, and talk of a global recession abounds. The growth slowdown is already being felt by companies. This year’s second quarter earnings showed a downgrade in forward-looking estimates for the next 12 months. And yet, stock markets continue to rally.

Naturally, falling earnings and rising stock prices mean equity valuations – on a price-to-earnings ratio – have climbed higher. This is a reflection of increased risk appetite. Equally important has been the fall in real yields. At the start of August, inflation-adjusted yields on 10-year US Treasuries once again sank to almost zero, and they are still well below their mid-June peak. This is largely down to shifting impressions of US Federal Reserve (Fed) policy. But it also shows investors are confident in the stability of financial assets, and in the Fed’s ability to promote a healthy US economy.

The key question is whether the medium-term macroeconomic backdrop has improved enough to justify this view. Markets are certainly betting it has, but we are not yet convinced, and the fact that markets are so confident is itself a cause for concern. Perfect landings are incredibly hard to achieve, and there are still significant risks to the outlook. Oil prices have fallen back, but any further reduction will be hard to achieve in the short term. China might be weak currently, but is likely to improve towards the end of this year. That will increase global demand for crude oil, which could hit US households just as they are starting to gain confidence. That would force the Fed to continue on its tightening path, dampening hopes of a monetary reversal. Such a situation could cause serious problems in the next couple of months, particularly for businesses required to refinance during that period.

The problem is not that the Fed is unlikely to get things right, but that markets have priced in such a high probability of success that any deviation could be devastating. The summer lull has probably helped prop up market sentiment somewhat. With many traders on holiday, it is much easier for markets to convince themselves everything is rosy. This lull coincides with a two-month break in Fed meetings, with the next one scheduled for the end of September. When that does come around, we should expect the Fed to have a renewed zeal for taming prices, which could provide a wake-up call for markets. We have never agreed with the doomsayers, and we still do not think that a global recession is inevitable (though recessions in the UK and Europe are all but certain). At the same time, we are slightly uncomfortable with the level of optimism implied by current equity values. We should enjoy the sunshine while it lasts, but future market improvements will need to be based on more than just the summer breeze.

Fiscal firepower in UK’s inflation fight

The increasingly bitter race to replace Boris Johnson has seen a host of promises from candidates on taxes, energy bills and welfare payments. But rampant inflation will be the main problem facing whoever wins the Tory leadership election. The stakes are high, and so far, the debate has focused on whether tax cuts or government spending are the best means of supporting people. In a recent article, senior figures from the Institute for Fiscal Studies describe how frontrunner Liz Truss’ promised tax cuts are ultimately unsustainable without a reduction in public spending somewhere down the line. All Tory leadership candidates emphasised the need for strong growth and the supposed ‘fiscal headroom’ of £30 billion, but there are serious flaws in these points.

For starters, that £30 billion would be easily eaten up by either a fall in tax revenues or a modest rise in unemployment payments. Considering the UK is set for a lengthy recession, both of those are likely. More generally, promoting short-term growth right now is at odds with taming inflation. The two forces generally keep each other in check, but Britain is now bracing for a recession coupled with persistently high inflation. This essentially means supply is so constrained that even economic contraction – and hence falling demand – is not quite enough to get short-term prices under control.

Faced with these intense pressures, what can any government do? Again, the fundamental problem comes down to the lack of supply. Right now, we are seeing this in energy markets, but the issue is a general one for the UK and has a longer-term characteristic. As both Tory leadership candidates are keen to point out, low productivity has held Britain’s economy back for well over a decade. This is down to a lack of investment, as well as deep-rooted problems in the labour market. Britain’s sluggish labour participation rate has gained attention in this regard, but equally problematic is the shortage of skilled workers.

This is not a short-term issue, though the effects of it are very much being felt now. A simple solution would be to increase immigration, but that seems unlikely in the political environment. Over the longer-term, investment in better education is another solution, but that is at odds with the government’s (even Rishi Sunak’s) desire to cut taxes as soon as practical. Or alternatively, other areas would need cutbacks. One way or another, supply and demand will have to be brought into balance. If that does not mean investing in more supply (particularly of skilled workers) it will have to mean crushing demand. The more the government shies away from this, the more aggressive the Bank of England will have to get.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

It’s a common misconception that inheritance tax only affects the extremely wealthy. However, if you’ve been looking into inheritance tax you may have read about a threshold of £325,000 before tax applies. Anything you own above that value, could be subject to 40% tax.

To understand how this relates to you and whether you’re going to be liable for inheritance tax, you’ll want to look at a few things. The following information is based on our current understanding of taxation law and practice in the UK which may change. The amount of tax you pay and relief you receive depends on your own personal circumstances which may also change in the future.

Figuring out the size of your estate is the first step

To judge whether inheritance tax is due, the first thing to do is calculate the value of everything you own.

We don’t often tot up the value of everything we own and it’s maybe why people often get caught out with inheritance tax. In fact, according to HMRC statistics, the average inheritance tax bill was a massive £209,000 in 2018/19. So, it’s really important to do this now.

It can also be surprising what is included in your estate for inheritance tax purposes and what’s not. For example, did you know that any gifts to your loved ones you’ve made in the last seven years could be included? Whereas the value of your pension might not be.

To start you should add up the value of your property, savings, investments and cars. Then, imagine you turned your house upside down. Anything that falls out should be included, like your TVs, laptops, furniture, antiques, jewellery and any valuable collections. You can see how quickly it would all add up. But does that mean inheritance tax would apply to all of it?

There are allowances that you need to be aware of

That threshold of £325,000 is an important figure because it’s a tax-free allowance that everyone is entitled to, no matter what your circumstances are or who you plan to leave your money to. You may have heard it being called the nil-rate band – but let’s call it a tax-free allowance just now to keep things simple.

There’s another big allowance, but it has some rules around it. The tax-free property allowance of £175,000 – or residence nil-rate band to give it its technical name – applies if you leave your home to your children or grandchildren.

So, if you add the two allowances together (£325,000 and £175,000) you can potentially leave £500,000 tax-free, as long as you leave your home to your children or grandchildren. The property allowance does reduce if your estate is worth a certain amount, but we won’t go into too much detail just now.

You can double your allowances to leave even more tax-free

Did you know if you’re married or in a civil partnership you can leave everything to your partner completely free from inheritance tax? However, this doesn’t mean you can ignore inheritance tax.

For example if you die first, everything would pass to your partner tax-free. But when they die, there could be inheritance tax due.

The good news is your partner can use your unused allowances. So, if you leave everything to them they can use your tax-free allowances of up to £500,000 plus their own £500,000. This means they can potentially leave £1m tax-free to children or grandchildren.

What if I do have an inheritance tax bill?

Inheritance tax is sometimes referred to as a voluntary tax. This is because there are many planning opportunities to reduce or prevent it.

Of course, with tax it’s never simple. There are a lot of complicated rules about inheritance tax. And there are a lot of potential pitfalls that could cost your loved ones a fortune. The good news is I am here to help and can advise what the best ways are for you to reduce inheritance tax.

Please find below, the Daily Investment Bulletin received from Brooks Macdonald this morning – 11/08/2022

What has happened

Risk appetite was emboldened by one of the largest downside misses to headline CPI in recent history. The equity gains were broad-based with cyclical sectors and technology shares leading the charge as investors wagered that the Fed would need to be less aggressive on monetary policy.

US CPI Report

US headline CPI came in at 8.5% year-on-year against expectations of a 8.7% increase and a 9.1% reading for June. If you zoom into the detail, the monthly change was actually negative at -0.02% which is the first monthly fall in over 2 years. As expected, the main driver of this was decline in energy prices and specifically gasoline which was -7.7% lower over the month alone. Core inflation was expected to rise on a year-on-year basis but actually stayed flat at 5.9%, further helping to boost sentiment. Whilst some of the more volatile components of the CPI readings are showing signs of peaking, broad inflationary pressures undoubtedly remain and will take time to filter through to lower median CPI. The Atlanta Fed divides up CPI into ‘flexible’ and ‘sticky’ elements and whilst the flexible reading fell sharply last month, the sticky reading actually saw gains. Words of slight caution but this is unlikely to deter the market which is very much in risk on mode.

Fed reaction

Bond markets moved quickly to reduce the probability of a 75bp rate hike at the September Fed meeting, with the futures market pricing in a coin toss between that and a 50bp hike. 10-year Treasury yields also fell initially however more hawkish Fed speak ultimately led to the benchmark yield broadly flat for the day. Chicago Fed President Evans said that inflation remained ‘unacceptably high’ and forecast that ‘we will be increasing rates the rest of this year and into next year’. President Kashkari said that he expected a 4.4% Fed interest rate at the end of next year and stressed the commitment of the Fed to bringing down inflation.

What does Brooks Macdonald think?

The Fed reaction, warning against inflation complacency, makes absolute sense. The Fed cannot afford for market or consumer inflation expectations to start to rise again after the recent falls. For the time being, investors are happy to look through the more hawkish messaging, expecting this to reversed as we enter 2023 and recessionary risks rear their heads. With central bank forward guidance seemingly dead for the rest of 2022 at the very least, inflation data remains the key determinant of market sentiment, on that basis yesterday is undoubtedly a strong positive for risk assets.

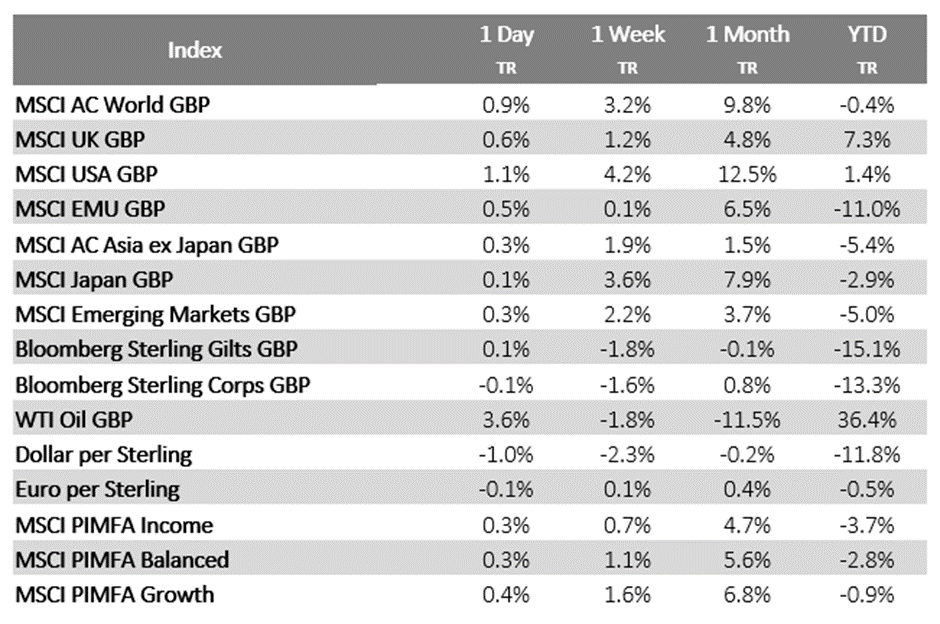

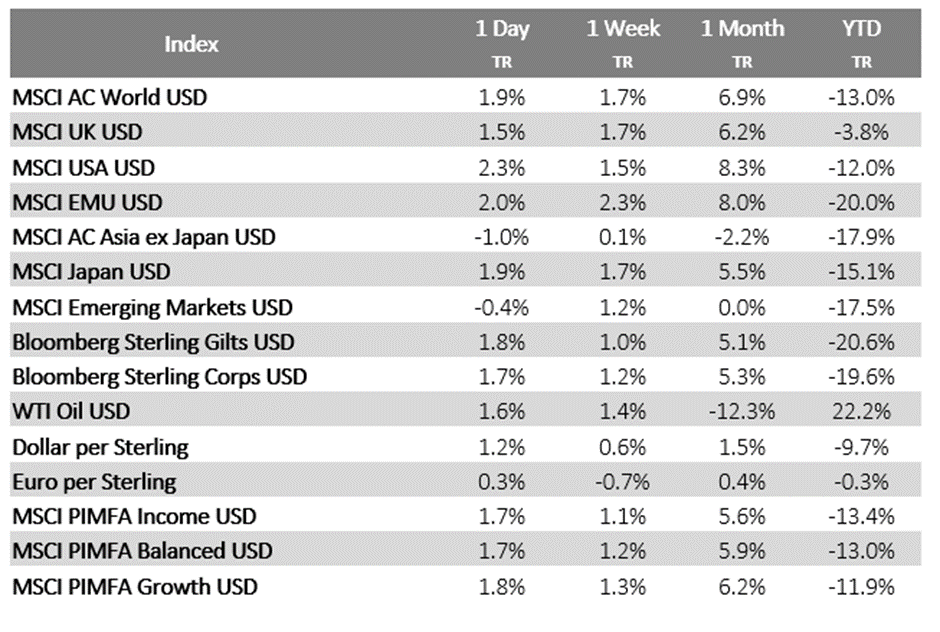

Bloomberg as at 11/08/2022. TR denotes Net Total Return

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see the below article from Brooks Macdonald, providing a detailed summary of the week’s economic and market news. Received late yesterday evening – 08/08/2022

The market lost confidence that the Federal Reserve (Fed) was set to pivot its focus from inflation to recessionary risks

The market’s confidence in the Fed’s ‘pivot’ from an inflationary focus to a recessionary focus was questioned last week, leading to bond market volatility. The market had already begun to conclude that the Fed had not in fact pivoted after a series of more hawkish Fed speakers, however it was the US employment report on Friday that firmed this view. As a result bond yields rose substantially, with the US 2-year yield rising by 34bps and the 10-year yield by 18bps. This left the yield curve even more inverted as investors took a lack of Fed pivot as making a US recession even more likely.

A strong US employment report suggests that the US labour market remains hot

The US employment report saw a significant beat in the number of new jobs created in July, with 528,000 jobs created versus 260,000 expected. Not only did this suggest a far hotter labour market than expected, but the June reading was also revised up higher. US average hourly earnings rose more than the market was expecting, hitting 5.2% year-on-year, suggesting that the inflationary pressures from wage rises are likely to continue to play a part in the inflation readings.

This week’s focus will be on the US Consumer Price Inflation (CPI) report with headline CPI expected to fall and core CPI rise

This week’s main planned macroeconomic event will be US CPI on Wednesday which is expected to see headline CPI fall from 9.1% to 8.7% but for core CPI to move from 5.9% to 6.1% year-on-year. What the market will make of falling headline CPI but rising core CPI may have as much to do with sentiment as economic reality. Core CPI is far more important to central bankers however headline CPI is arguably more politically charged. If there was a political element to the Fed’s hawkishness, driven by the Biden administration keen to get the cost-of-living squeeze under control, then a headline fall would be an important win. The release of US producer price inflation will also garner attention with the cost of healthcare expected to become an increasingly important sub-component.

Markets arguably read far too much into Fed Chair Powell’s comments at the post committee meeting press conference. Ultimately, a fall in the CPI readings are the only sustainable exit ramp for the current hawkish policy. Should a recession occur this may come through a hit to demand, in the interim markets will be hoping for signs of softening pressures this week.

Please continue to check our blog content for advice and planning issues from us and leading investment houses.

Please see below article received from Tatton this morning, which reports a surprisingly positive outlook on markets despite high inflation rates, global energy supply struggles and a rising tension between the US and China in relation to Taiwan.

Bad news filled the airwaves last week. Faltering global growth, higher inflation forecasts and rising interest rates set a dour tone – capped off by a geopolitical crisis in Taiwan. UK investors were struck by the Bank of England’s dire warnings: a 13% inflation peak and a protracted recession are now in store for Britons, according to Governor Andrew Bailey. Predicted to last for five quarters, the looming UK recession is set to outlast the one following the global financial crisis in 2008/09.

Yet despite all that gloom, capital markets have been in surprisingly good spirits. Equities have rallied since the start of July, and bond yields have fallen. As a result, markets have more or less recovered all of their June losses. So, why are investors so unfazed by the current bad news? Judging from bond markets, the feeling is that we have reached peak global inflation. Oil prices have started falling and the actions of oil producers themselves point to a belief that current prices are unsustainable. Supply chain bottlenecks clogged by the pandemic are also improving, while consumer demand has clearly taken a hit from the cost-of-living crisis. The thought is that this will cause a reversal of central bank policy sooner than previously expected, with implied US rates peaking by the end of this year. Investors have essentially given central banks – particularly the US Federal Reserve (Fed) – a vote of confidence. Its policies are expected to prevent a dangerous wage-price spiral while maintaining the economy at a decent level. What’s more, middle-class consumers still have savings to fall back on, while jobs remain plentiful and businesses are more financially sound than in previous downturns. Recessions in most regions are expected to be shallow and brief, while the US might avoid one altogether.

Monetary policy works on a very long lag, meaning that tweaks to interest rates now will only have an effect a year or so down the line. But if bond markets are to be believed, inflation will already be largely under control by then – meaning further tightening would be overkill. Central bankers want to tame inflation right now, and the only way they can think to do that is by affecting consumer and business behaviour. They will hope that pessimism will stop employees pushing for higher wages, bringing down cost pressures. That is the best-case scenario, and the one markets are currently betting on. Such optimism in bond markets was the main reason for July’s uptick in equity prices – as falling yields made stocks comparatively more attractive. But that positivity is itself a little concerning, as it makes asset prices vulnerable to worse-than-expected news.

There are still many risks to the overall outlook, which are arguably not properly priced-in. Europe is particularly at risk, facing energy shortages and sharply higher costs this winter. This should bring consumer demand down further and eventually cool inflation, but that could take some time. The main source of Europe’s woes is gas supplies, which are very hard to adjust in the short-term, and are highly susceptible to Russia’s war in Ukraine. European businesses could be the hardest hit, as they have less sway over electoral outcomes and are therefore lower down on politician priority lists.

Markets nevertheless seem to think the inflation battle is already won, and there is a clear path to economic recovery. But none of that is certain, and there are many political obstacles that could get in the way. Governmental paralysis in Britain and Italy could prevent decisive policy action (Conservative MPs have already questioned the Bank of England’s independence in response to its dire forecasts), while US-China tensions over Taiwan are a serious and perhaps under-appreciated risk to global growth. Negative news flow, particularly around energy supplies, could severely dampen market sentiment from here.

Energy profits: here for a good time, not a long time

Oil and gas prices, buoyed by pandemic supply issues and then catapulted skyward by Russia’s invasion of Ukraine, have generated truly astonishing results for the world’s biggest energy companies. Centrica, the owner of British Gas, recently reported profit growth of 500% year-on-year for the first half of 2022. Meanwhile, Shell posted its best ever quarterly profits for Q2 and BP its highest profits in 14 years for the same period. All of this comes while Britons face eye-watering rises in energy and fuel costs. Naturally, the disparity has led to a great deal of negative media coverage.

These profits have naturally benefitted share prices. On a net total return basis, unsurprisingly, Energy is the best performing sector over the last year, by some distance. Bloomberg’s energy index is 28.4% up from a year ago. Utilities, the only other sector to post positive growth over that time, are up just 5.3% by comparison. These moves are made all the more impressive by the negative equity market backdrop in that time. The rise in ‘risk-free’ rates has dampened equity valuations across virtually all industries, and energy is no exception. In fact, on a forward price-to-earnings ratio, energy company valuations have come down more than any other sector. The fact that energy companies have posted the best returns while dropping to the lowest valuations is astonishing, and shows how sharp the recent energy price shock has been. But it also shows investors are much less optimistic about the long-term prospects for energy companies than current results might suggest. Some of this is down to the likely political response: the UK government has already announced a windfall tax on oil and gas companies, and the sharper the contrast between struggling households and booming energy giants gets, the more likely we are to see further taxes – and not just in the UK.

The deeper reason for falling energy valuations, though, are likely to be structural. Russia’s war and the ensuing sanctions delivered the biggest price shock to global energy markets since the 1970s OPEC embargo. Oil and gas supply lines between Russia and the West have been battered and may not ever recover, leading to a sharp squeeze in prices. But over the longer-term, prices are less about what goes where and more about the balance of aggregate supply and demand. That balance has not been fundamentally changed by Russia’s invasion. Russia has a short-term interest in squeezing its European customers – particularly Germany, which has been one of the hardest hit by constrained gas supplies – but has no interest in reducing its oil and gas production over the long term. It has already found many willing buyers in Asia, and will inevitably want to get back to full production and export volumes when it can. Then there is the demand side. The pandemic recovery saw a sharp burst of pent-up energy demand, but this has since cooled off significantly. With looming recession fears, this trend is set to continue. What’s more, the incredible rise in energy prices is already destroying end demand. Come winter, this is likely to mean intense energy saving efforts – with communal heating and power-cuts already being discussed in Germany.

The current price shock will also have implications for the future. Fossil fuel investment measures have been drawn up for the UK and US – which will increase supply some years into the future. More importantly, there is a clear political drive toward increasing renewable or even nuclear energy production. This is part of a much longer-term move away from oil and gas, and the cost-of-living crisis that is rooted in our fossil fuel dependency goes back, has significantly heightened the sense of urgency that already existed from the global warming CO2 side of things. Inevitably, this dampens the long-term outlook for oil and gas demand.

Fossil fuel producers are well aware of this. At their most recent meeting, OPEC+ countries agreed a minimal increase in production despite a seemingly huge price incentive to pump more. This suggests a recognition that current price levels are unsustainable in the face of rising interest rates and a slowing global economy. On the current trajectory, oil supply is likely to outstrip demand within the next four years. As producers see it, increasing production now will just make them more vulnerable to lower prices in the future. With this in mind, lowly valuations for booming energy companies are to be expected. Record oil and gas profits are here for a good time, but not a long time.

Please check in again with us shortly for further updates and relevant content.

Please see below the latest daily investment bulletin from Brooks Macdonald, which was published and received this morning (05/08/2022):

What has happened

Equity and bond markets were generally quieter at a headline level yesterday, however with oil prices continuing to fall, WTI oil below $90 per barrel and Brent below $95 per barrel, the energy sector saw stark underperformance.

Bank of England

The Bank of England presented a gloomy picture for the UK economy as it announced a 50bp rate rise, the largest since 1995. Whilst forward guidance for central banks is, at best, on hold for this cycle, further rate hikes seem likely given the Bank’s focus on inflation and its lofty predictions of where year-on-year inflation rates could end up. The BoE predicted a prolonged contraction in economic activity, starting in Q4 of this year then lasting until the start of 2024. Alongside this, the Bank forecast that inflation would reach 13% this year before falling in coming quarters. These numbers are quite spectacular changes from previous guidance and paint a very downbeat outlook for the UK economy. One of the big question marks at the moment is how UK government fiscal policy will play out, and for that we will need to know the next Conservative Party leader.

US Employment Report

The initial jobless claims in the US have been a recent area of weakness for the US labour market outlook, showing a worsening picture even as the non-farm payroll reports showed a more upbeat picture. Yesterday’s claims came in line with expectations however the number of ongoing claims rose more than expected, suggesting that those claiming are struggling to find roles as quickly. Given the importance of the employment outlook to the US Fed, today’s employment report will be critical to whether the US central bank begins to more formally pivot to concerns around economic growth and inflation rather than inflation alone. The market expects 250,000 new jobs to have been created in July and for unemployment rate to stay steady at 3.6%.

What does Brooks Macdonald think

Recent Fed speakers have used the strong labour market backdrop as the crux of their argument as to why Fed interest rates still need to rise to tackle inflation. A weaker employment report will question this narrative and lead the Fed to consider a more balanced view of future interest rates. Recent corporate earnings have painted a more positive picture of the economy in the near term however the initial jobless claims suggest that there are now signs the US economy is losing some of its momentum.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.