Please see today’s Brooks Macdonald Daily Investment Bulletin received earlier this morning (20/10/2022):

What has happened?

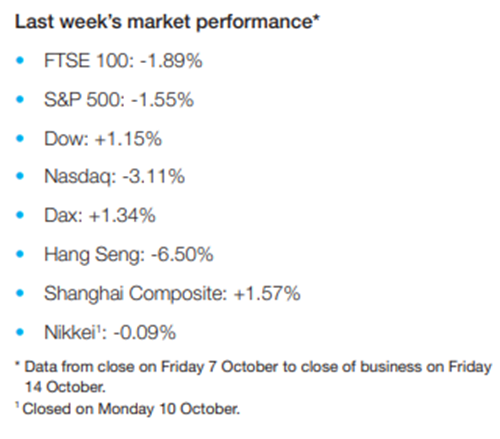

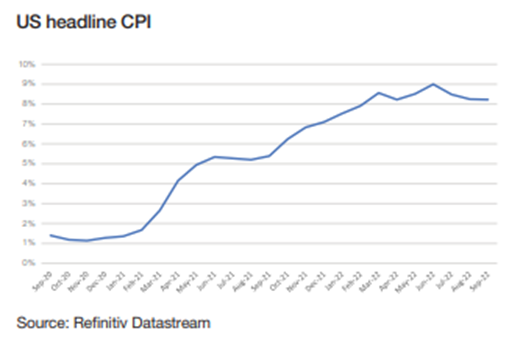

After a good start to the week, equity markets ran out of steam on Wednesday with US government bond yields moving higher, as worries surfaced again over inflation and the expected next round of central bank interest rate hikes. The US Federal Reserve meeting on 2 November is now less than 2 weeks away, and markets have priced in a 75bp hike, which if it happens would be the fourth 75bp-sized hike in a row. Elsewhere, of interest was a Bloomberg news report that China is considering cutting quarantine for arrivals from abroad from 10 days (with 7 days in a hotel followed by 3 at home), to 7 days (with 2 days in a hotel followed by 5 at home), giving oxygen to hopes that China’s zero-Covid policy might be loosening a bit.

Dare markets hope again for a Fed monetary policy pivot?

Federal Reserve Bank of Minneapolis President Neel Kashkari said on Wednesday that the US central bank could potentially pause its interest-rate increases at some point next year if policymakers see clear evidence that core inflation is slowing. “My best guess right now is yes, do I think inflation is going to level out over the next few months, the services, the core inflation, and then that would position us some time next year to potentially pause,” For balance however, Kashkari did make it clear that he saw no evidence yet to give him “comfort” that core prices were moderating, and that was something he was “quite concerned about”. Also supporting the idea of an easing in Fed interest rate ‘tempo’ at least, Federal Reserve Bank of St. Louis President James Bullard, said on Wednesday that he expects the US central bank to end its front-loading of aggressive interest-rate hikes by early next year and shift to keeping policy sufficiently restrictive with small adjustments as inflation cools. “You do have to think about what the reasonable level is” Bullard said.

Mounting pressure for the UK Truss government

Over the course of yet another dramatic day in Westminster, the Home Secretary Suella Braverman resigned over what was described as a national security breach, reportedly sending sensitive documents from a personal email. However, adding to the sense of a volatile political climate, in her resignation letter Braverman said “Pretending we haven’t made mistakes, carrying on as if everyone can’t see that we have made them, and hoping that things will magically come right is not serious politics”, and adding that “I have concerns about the direction of this government. Not only have we broken key pledges that were promised to our voters, but I have had serious concerns about this Government’s commitment to honouring manifesto commitments”.

What does Brooks Macdonald think

While the UK is dominating the political headlines for now, it is not the only country facing the risk of political upheaval. Over in the US, crucial mid-term elections are due to take place on 8 November (with some states having already started early-voting). According to the latest financial betting odds from PredictIt, Democrats are expected to cede control of the House of Representatives, and lately in recent days, possibly also the Senate, to the Republicans. While the risk of impending political gridlock sounds unwelcome, for markets it can often be a least-worst option – as it stymies the chance of any more radical political policy ambitions becoming law, and supporting a political status-quo. Simply then, for markets, political risk can become one less thing to worry about.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Carl Mitchell – Dip PFS

Independent Financial Adviser

20/10/2022