Please see below article received from Brooks Macdonald this morning, which provides a market update and reflects on global economic developments.

What has happened

Despite some initial optimism after the release of the Federal Reserve statement, Fed Chair Powell’s press conference lead to concern that the Fed’s terminal rate could be higher than previously guided and that rates may stay at that level for some time. Against this backdrop equities and bonds both repriced in US trading with the US dollar seeing a fresh bout of strength.

Bank of England

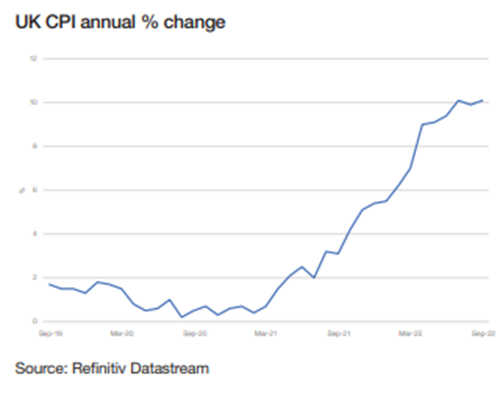

Before we turn to the Fed, today’s Bank of England meeting will be the next milestone for central bank watchers to ponder. The Bank of England has seen a remarkable turn of events since its last meeting in September which has seen the mini-budget, quantitative easing, policy reversal and a change in Prime Minister. The net effect of all of this is that, despite a very volatile round trip, markets still expect the Bank to raise interest rates by 75bps at this meeting. In some ways the central bank is flying blind yet again, as the November Autumn Statement by the government may have very different inflationary impacts depending on how the government chooses to fill the fiscal hole. Despite the political backdrop being far more stable than a month ago, the UK still has a significant inflation problem and that will need to be addressed by the Bank today.

Federal Reserve

The market initially rallied after the Fed raised interest rates by 75bps and inserted the following in the statement, saying that the ‘Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation’. The bond market interpreted this as a dovish pivot and a sign that the pace of interest rate hikes would slow. Powell was at pains to stress during his press conference that whilst the pace of hikes may slow, the terminal rate may need to be higher than the Fed had guided in September and policy may need to stay in restrictive territory for some time to keep inflation under control.

What does Brooks Macdonald think

Powell was consistent in stressing that the rises of under-tightening were greater than over-tightening, continuing to stress the Fed’s role in quashing inflation. There was very little new news in Powell’s statement, but his words pushed back against the market’s, perhaps naïve, belief that the Fed would pivot quickly from rapid tightening to rapid loosening. Now markets are beginning to price in interest rates plateauing at the terminal rate for several meetings, bond yields need to readjust.

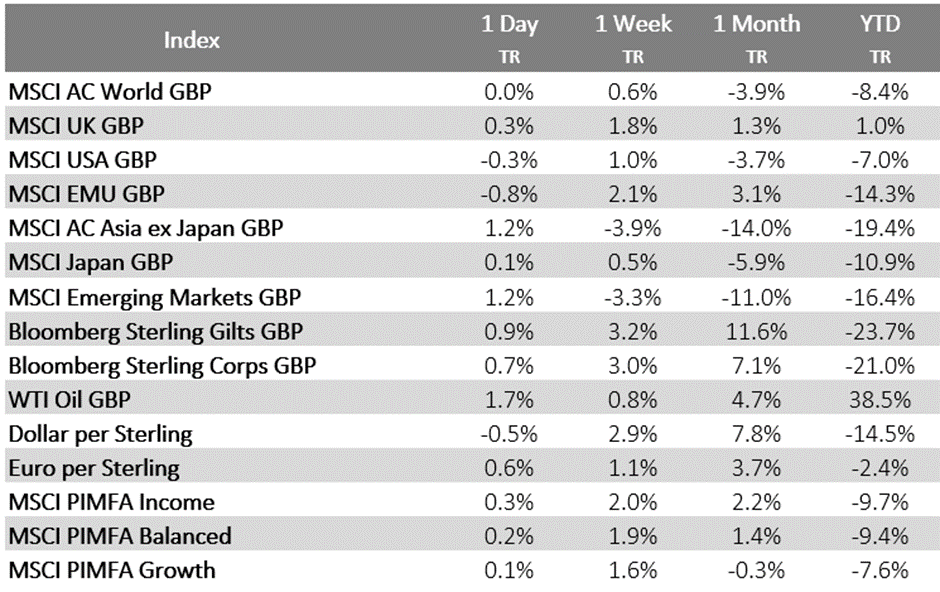

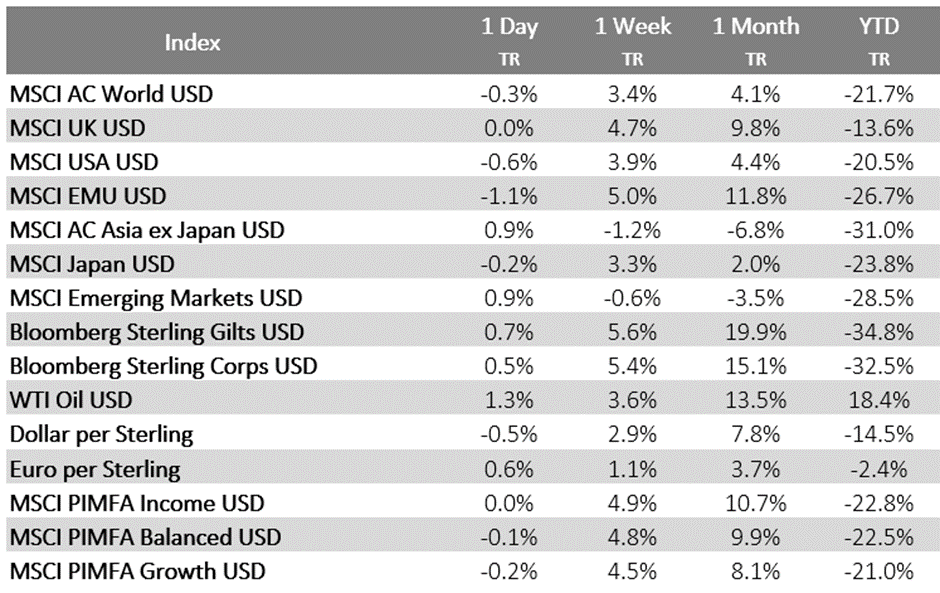

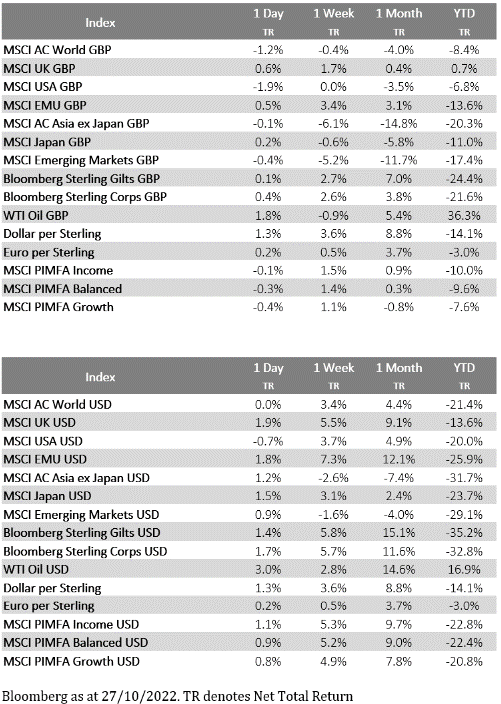

| Index | 1 Day | 1 Week | 1 Month | YTD | |

| TR | TR | TR | TR | ||

| MSCI AC World GBP | -1.5% | 0.2% | 1.4% | -8.3% | |

| MSCI UK GBP | -0.6% | 1.3% | 3.5% | 2.1% | |

| MSCI USA GBP | -2.5% | -0.7% | 1.6% | -7.4% | |

| MSCI EMU GBP | -0.7% | -0.8% | 5.6% | -14.2% | |

| MSCI AC Asia ex Japan GBP | 1.0% | 4.0% | -5.6% | -17.2% | |

| MSCI Japan GBP | 0.9% | 2.2% | 1.6% | -9.1% | |

| MSCI Emerging Markets GBP | 0.7% | 3.7% | -3.2% | -14.3% | |

| Bloomberg Sterling Gilts GBP | 0.1% | 1.5% | 4.2% | -23.3% | |

| Bloomberg Sterling Corps GBP | 0.3% | 1.5% | 5.3% | -20.4% | |

| WTI Oil GBP | 2.0% | 3.6% | 9.8% | 41.2% | |

| Dollar per Sterling | -0.1% | -1.2% | 2.7% | -15.2% | |

| Euro per Sterling | -0.1% | 0.7% | 1.9% | -2.4% | |

| MSCI PIMFA Income | -0.6% | 0.8% | 3.3% | -9.2% | |

| MSCI PIMFA Balanced | -0.8% | 0.7% | 3.0% | -8.9% | |

| MSCI PIMFA Growth | -1.0% | 0.6% | 2.8% | -7.1% | |

| Index | 1 Day | 1 Week | 1 Month | YTD | |

| TR | TR | TR | TR | ||

| MSCI AC World USD | -1.6% | -1.0% | 4.6% | -22.2% | |

| MSCI UK USD | -0.7% | 0.1% | 6.7% | -13.5% | |

| MSCI USA USD | -2.6% | -1.9% | 4.7% | -21.5% | |

| MSCI EMU USD | -0.8% | -1.9% | 8.9% | -27.3% | |

| MSCI AC Asia ex Japan USD | 0.9% | 2.7% | -2.7% | -29.8% | |

| MSCI Japan USD | 0.8% | 1.0% | 4.7% | -22.9% | |

| MSCI Emerging Markets USD | 0.6% | 2.5% | -0.3% | -27.3% | |

| Bloomberg Sterling Gilts USD | 0.1% | 0.3% | 7.0% | -35.1% | |

| Bloomberg Sterling Corps USD | 0.3% | 0.2% | 8.2% | -32.7% | |

| WTI Oil USD | 1.8% | 2.4% | 13.2% | 19.7% | |

| Dollar per Sterling | -0.1% | -1.2% | 2.7% | -15.2% | |

| Euro per Sterling | -0.1% | 0.7% | 1.9% | -2.4% | |

| MSCI PIMFA Income USD | -0.7% | -0.4% | 6.4% | -23.1% | |

| MSCI PIMFA Balanced USD | -0.9% | -0.5% | 6.2% | -22.8% | |

| MSCI PIMFA Growth USD | -1.1% | -0.6% | 5.9% | -21.2% |

Bloomberg as at 03/11/2022. TR denotes Net Total Return

Please check in again with us soon for further relevant content and news.

Chloe

03/11/2022