Please see the below summary of last weeks Mini Budget from Brewin Dolphin and their thoughts:

Chancellor Kwasi Kwarteng has delivered his mini-budget, in which he unveiled measures that aim to drive UK economic growth.

The fiscal event came against a backdrop of high inflation and one of the steepest falls in real wages on record. With consumer prices up 9.9% in August from a year ago, and expected to near 11% when energy bills rise in October, Kwarteng confirmed that many of the tax cuts promised by prime minister Liz Truss during the Conservative Party leadership race would be enacted.

Kwarteng, who took on the position of chancellor less than three weeks ago, announced the scrapping of additional-rate income tax, the reversal of April’s increase in the rates of National Insurance (NI) and dividend tax, and a reform of stamp duty land tax.

Here, we summarise the main announcements, before giving Guy Foster’s view on what they could mean for investors and the economy.

The Economy

Unlike the full budget, this mini-budget did not include detailed economic and fiscal projections from the Office for Budget Responsibility (OBR). Instead, the chancellor published a ‘growth plan’, which sets a target of 2.5% average growth in UK gross domestic product (GDP) over the medium term. GDP fell by 0.1% in the second quarter and it is expected to fall by another 0.1% in the third quarter, meaning the UK would be in a technical recession.

Kwarteng said the 2.5% growth target would be supported through tax cuts and reforms to the supply side of the economy. The latter will include measures to speed up infrastructure projects, the creation of new investment zones, increasing private sector investment, and encouraging more people into work through reforms to universal credit and support for the over-50s.

The cost of the government’s tax-cutting measures will be published in a forecast by the OBR later this year. Measures to alleviate the pressure from rising energy bills alone will see borrowing for 2022/23 rise from £161.7bn to £234.1bn. Kwarteng said the government will provide an update on its fiscal rules alongside the OBR’s forecast.

‘With a lot of the measures in the minibudget boosting demand, the risk is that interest rates will have to rise further to offset this. The chancellor seems to be pressing the accelerator, while the Bank of England’s Monetary Policy Committee is pushing on the brakes’ – Guy Foster, Chief Strategist

Additional-rate income tax abolished

In a surprise move, Kwarteng revealed that additional rate income tax will be abolished. From 6 April 2023, those living in England, Wales and Northern Ireland will no longer pay 45% tax on annual income exceeding £150,000. Instead, all annual income above £50,270 will be taxed at 40%, the current higher rate of income tax.

Basic-rate income tax lowered

In another reform to income tax, Kwarteng confirmed that the planned reduction in the basic rate of income tax for those living in England, Wales and Northern Ireland will take place sooner than expected. The rate was due to be lowered from 20% to 19% from April 2024, but this reduction will now come into effect from April 2023. This will bring a tax saving of around £124 a year for someone on a £25,000 salary, or £374 a year for someone on £50,000. Kwarteng did not make any changes to the personal allowance (the amount you can earn each year before you start paying income tax) or the higher-rate tax threshold. These will remain at £12,570 and £50,270, respectively, after being frozen in April 2021 for five years.

Dividend tax increase reversed

Investors will benefit from lower dividend tax after Kwarteng announced April’s 1.25 percentage point rate hike will be reversed. As of 6 April 2023, the rate of dividend tax will revert to 7.5% for basic-rate taxpayers and 32.5% for higher-rate taxpayers. Additional-rate dividend tax will be scrapped to align with the removal of additional-rate income tax.

The annual dividend allowance – the amount of dividend income you do not have to pay tax on – will remain at £2,000.

National Insurance rate hike reversed

The day before the mini-budget, Kwarteng confirmed that April’s increase in the rate of National Insurance will be reversed. The 1.25 percentage point rate hike was part of previous chancellor Rishi Sunak’s plan to fund the NHS and social care. It was due to last for one year, after which the extra 1.25p in the pound would be collected as a new health and social care levy.

From 6 November, however, the rate of NI will fall from 13.25% to 12% on earnings between the primary threshold (£12,570) and the upper earnings limit (£50,270) and from 3.25% to 2% on earnings above this. The move will save around £155 a year for workers on a salary of £25,000, £468 a year for those on £50,000, or £1,093 a year for workers on £100,000, according to calculations by Brewin Dolphin. Next year’s levy will be cancelled, with funding for health and social care instead coming from existing taxes.

Stamp duty cut

Stamp duty land tax in England and Northern Ireland has been immediately reformed. The level at which homebuyers start paying stamp duty has doubled from £125,000 to £250,000. First-time buyers will start paying stamp duty if their first home costs £425,000 or more, up from £300,000 previously. The value of the property on which first-time buyers can claim stamp duty relief has also risen to £625,000 from £500,000.

According to the government, these measures will reduce stamp duty bills for all movers by up to £2,500, with firsttime buyers able to access up to £11,250 in relief.

Energy bills capped

The above tax cuts come on top of the government’s recently announced energy price guarantee, which aims to reduce some of the pressure from soaring energy bills. The guarantee replaces the Ofgem price cap and will see a typical household’s energy bill capped at £2,500 a year for two years from 1 October. This is expected to save the average household around £1,000 a year based on current energy prices from October. This is on top of the £400 energy bill discount that each household will receive over winter.

Businesses, charities and schools will be given equivalent support via a new ‘supported wholesale price’ for six months, with further help offered to companies in vulnerable industries after that.

Corporation tax frozen

In a welcome move for businesses, Kwarteng announced that the planned increase in corporation tax will no longer go ahead. The main rate of corporation tax was due to rise to 25% in April 2023, but it will now remain at 19%. For businesses in the pub and hospitality sectors, alcohol duty will be frozen from February 2023 rather than rise in line with the retail price index (RPI).

Businesses in some areas could also benefit from a new network of low-tax, low-regulation investment zones. Focusing on England in the first instance, regulations and planning rules will be eased in these new zones, and businesses operating in the zones will be able to access time-limited tax incentives over ten years.

Cap on bankers’ bonuses lifted

Kwarteng also confirmed that the hotly debated cap on bankers’ bonuses will be removed, suggesting this would help to make London a more attractive place for global banks to do business. The cap was introduced by the EU in 2014, when the UK was still a member, and limits bonuses to twice an employee’s salary. Once the cap is removed, banks will be free to award whatever level of bonus they choose.

With such a wide range of measures being introduced, Guy Foster, our Chief Strategist, shares his views on how they could affect investors and the economy.

The new prime minister and chancellor have been outspoken about their very ambitious growth target of an average of 2.5% over the medium term. The most common route to increasing growth comes from boosting demand and drawing people into employment, but with unemployment historically low that poses a major challenge. That’s the reason the Bank of England is raising interest rates – to slow demand and reduce inflation.

With a lot of the measures in the mini-budget boosting demand, the risk is that interest rates will have to rise further to offset this. The chancellor seems to be pressing the accelerator, while the Bank’s Monetary Policy Committee (MPC) is pushing on the brakes.

The energy bill cap, reversing the NI increase, bringing forward the income tax cut, and abolishing additional-rate tax are all policies that will boost demand.

The growth target depends much more on the UK’s ability to boost the economy’s potential capacity. That is what the government will hope to achieve through changes to universal credit in order to try and reduce labour inactivity. Other supply side measures include cancelling the planned increase in corporation tax, low tax investment zones and greasing the approval process for infrastructure investment. These kinds of policies have potential but they take a long time to take effect and will prompt public resistance, making them difficult to implement.

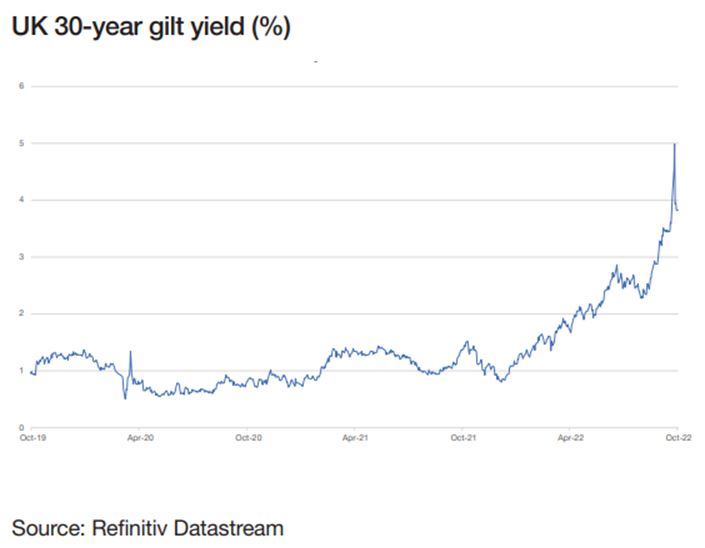

The net result of the chancellor’s statement was that government bond yields rose sharply. This was in anticipation of higher interest rates over the coming years, and the deluge of new bonds that will be issued so that the government can borrow more money to meet its extra spending and reduced tax revenue.

Markets moved to reflect a much steeper interest rate trajectory. Rates were volatile but at times implied that interest rates could go up by more than 0.75 percentage points at each of the remaining MPC meetings this year, eventually peaking at well over 5%.

With many of the details pre-released, the biggest surprise was that there was so little done to raise new funds or cut other spending to pay for the headline measures. Despite the prospect of higher interest rates, the pound eventually fell reflecting investors’ concerns about the deteriorating public finances and scepticism that the increase in debt will translate into higher growth.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Andrew Lloyd DipPFS

26/09/2022