Please see this week’s Markets in a Minute update below from Brewin Dolphin, received yesterday afternoon – 27/01/2026.

How are U.S. tariff threats impacting markets?

We examine the market’s reaction to President Trump’s threats to impose tariffs on Europe over Greenland.

Key highlights

- Davos and the debt markets: Equities struggled as President Trump threatened tariffs against NATO members for their stance on Greenland.

- All that glitters is gold: Gold benefitted from the news, exceeding the financial landmark of $5,000 per troy ounce.

- UK retail sales boost: Retail sales expanded on a seasonally-adjusted basis and consumer sentiment improved.

Davos and the debt markets

Equity markets struggled last week, rocked by a news flow that at times had somewhat ominous overtones – even if the fundamental and tangible drivers of equity performance still seem to be in place.

The ominous news flow predictably came from U.S. President Donald Trump. As he prepared to attend the World Economic Forum in Davos, his rhetoric over Greenland suggested little room for compromise and a determination to take sovereignty over the region from NATO ally Denmark.

In response, some NATO members planned exercises in the region. This prompted the president to declare that they would be punished by tariffs beginning in February, increasing in June and staying in place until America’s acquisition of Greenland has been completed.

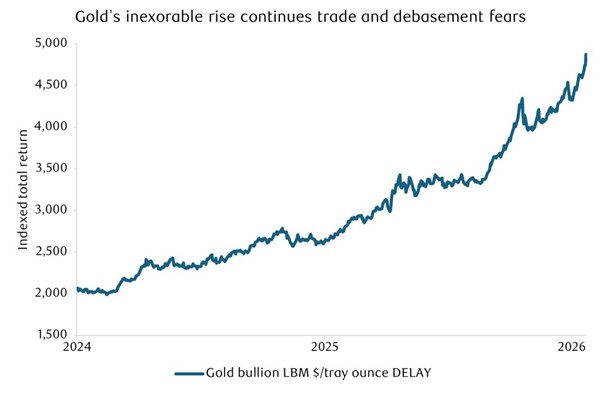

With their usual dispassionate approach to foreign affairs, markets were little moved by threats to Greenland’s sovereignty, but they were concerned about the possibility of tariffs. Equities were weaker, the dollar fell, and bond yields rose. Gold remains one of the few asset classes to benefit from this news.

Source: LSEG Datastream

Following the ‘Liberation Day’ tariffs, countries have generally been reluctant to impose retaliatory tariffs on the U.S., partly because those with balance of payments surpluses with the U.S. would appear to have more to lose from a trade war. This latest tariff threat created an additional challenge – U.S. tariffs were only imposed on eight countries participating in NATO exercises, but retaliation would need to come from the European Union as a whole. Dragging a lot of countries into a trade war that has the scope to escalate further would test the unity of the Eurozone.

Could an alternative be for Europeans to sell their holdings of U.S. treasuries? Europe as a region is believed to hold around 12% of U.S. treasuries, the sale of which would put upward pressure on U.S. borrowing costs.

The complication is that many of those bonds are private sector holdings and are therefore outside the control of the state. Mobilising them to sell would be nearly impossible. Many may be beneficially owned by stakeholders outside Europe anyway. And for most, the decision to hold them reflects the liquidity that only the treasury market can offer – or a need to hold U.S. assets to avoid losing currency competitiveness against the U.S. The desire to hold less treasuries is powerful and explains part of the rise in gold as an alternative home.

Returning to the topic of Davos, this has typically been a forum in which countries and business leaders find ways to help each other. President Trump’s involvement has been to shift the narrative to one of greater self-sufficiency and self-interest. It’s a uncomfortable message for those who aren’t part of the world’s largest economy, but it’s one that was taken head on by Canadian Prime Minister Mark Carney. He talked about the need for middle countries to accept that the old global rules-based order is no more, and that middle power countries like Canada, the UK and the EU states finding flexible alliances will be the way to avoid subordination to the global superpowers.

It’s a stark but compelling reality, which RBC Chief Executive Officer Dave McKay was asked to expand upon at the Forum.

As the week progressed, a tentative de-escalation was brokered by NATO Secretary Mark Rutte. It sounded as if President Trump would be willing to drop his demand for Greenland’s sovereignty in exchange for military access. It’s understood that some access to Greenland’s mineral wealth would also be afforded. Greenland holds significant deposits of rare earth elements. However, Helima Croft, RBC’s Head of Commodity Strategy, believes they’re remote, ice-covered and expensive to access.

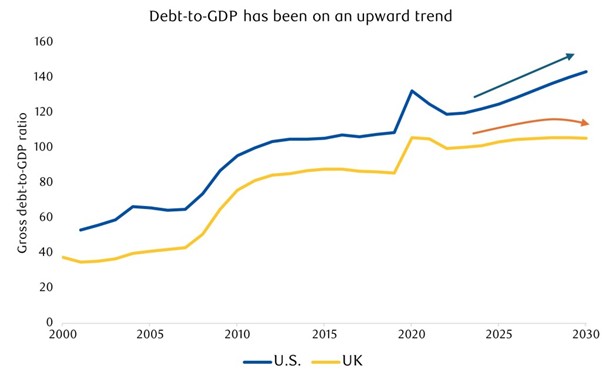

The debate over Greenland forms a further evolution of the ‘Worlds Apart’ theme, which RBC Wealth Management identified three years ago. What began as a rupture in trade seems to be becoming broader and more fundamental with each month that passes. It discourages investors from holding U.S. assets, even if only at the margin, and has contributed towards the weakness of the dollar and the rise in the gold price. As such, it contributes to an overlapping theme of debasement, which is more substantially represented by the U.S.’s reluctance to address its unrepentant government borrowing.

Source: LSEG Datastream

Rising government debt has been a concern for many industrialised countries, but the U.S. is certainly a stand-out because under both the Republicans and Democrats, the forecast public finances have been allowed to worsen.

UK sees retail sales boost

In the UK, by contrast, last week saw some good news on the public finances.

The fiscal position is stretched in the UK. However, governments do take tough actions based on recommendations by the independent fiscal watchdog and will take some comfort that borrowing has increased more slowly than expected.

In other UK news, retail sales expanded on a seasonally-adjusted basis and some aspects of consumer sentiment improved. It does seem as if UK consumers held back spending due to concerns over the prospect of tax hikes in the Autumn Budget, but they may now feel confident to indulge a little more. Recent interest rate cuts will also help.

Please continue to check our blog content for advice, planning issues and the latest investment market and economic updates from leading investment houses.

Charlotte Clarke

28/01/2026