Please see below, an article from Brooks Macdonald which discusses the key factors currently affecting global investment markets. Received today – 16/01/2026

What has happened?

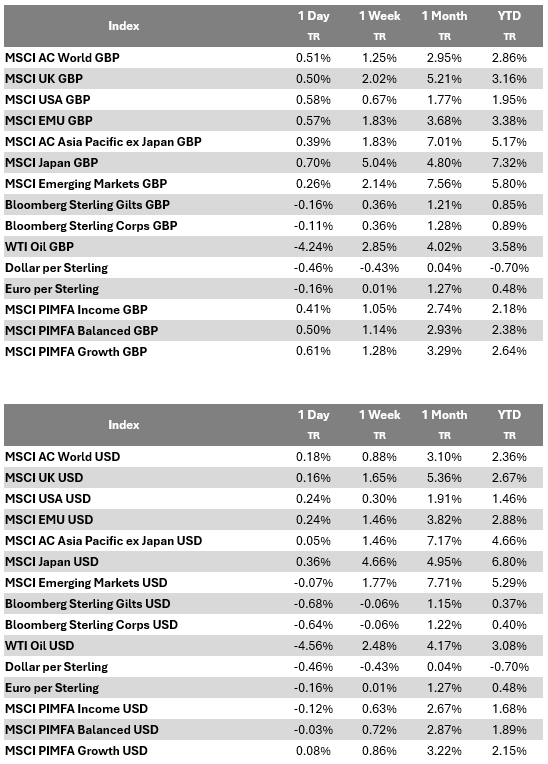

Markets strengthened yesterday as geopolitical concerns eased and supportive US data lifted sentiment. A more conciliatory tone from the US helped oil prices break a five day winning streak, easing some of the recent risk premium embedded in energy markets. Brent crude saw its sharpest decline since June, falling -2.18% to $63.76/bbl, while gold and silver both edged back from Wednesday’s highs. The S&P 500 gained +0.26%, led by semiconductor stocks after TSMC’s upbeat results, with the Philadelphia Semiconductor Index up +1.76% and Nvidia rising +2.13%. Banks also outperformed, helped by strong earnings from Morgan Stanley and Goldman Sachs. Meanwhile, expectations of fewer Fed rate cuts pushed the 10 year US Treasury yield up to 4.17%. In Europe, the STOXX 600 and FTSE 100 both closed at record highs, supported in the UK by stronger than expected November GDP (+0.3%).

US data keeps the expansion narrative alive

Momentum was reinforced by a series of strong US economic indicators. Initial jobless claims fell to 198k (vs. 215k expected), pulling the four week average to a near two year low. Though seasonal effects may be at play, the data added to the impression of a resilient labour market. Two regional Fed surveys echoed that message: the New York Fed’s Empire State manufacturing index rose to 7.7 (vs. 1.0 expected), while the Philadelphia Fed survey climbed to 12.6 (vs. -1.4 expected). Both showed easing cost pressures, with prices paid components at multi month lows. This mix of firm growth and moderating inflation led investors to scale back rate cut expectations in 2026. Markets now price just 48bps of cuts by year-end. Treasury yields moved higher across the curve, helped by comments from several Fed officials emphasising that inflation remains above target and that policy should stay restrictive for the time being. Today is the last chance to hear from Fed speakers before the blackout period begins.

What does Brooks Macdonald think?

The continued leadership from cyclical and small cap equities stands out, with the Russell 2000 outperforming the S&P 500 for the tenth consecutive session, which is the longest streak since 1990. This suggests investors are becoming more comfortable with the durability of the US expansion, even as policy expectations move toward fewer cuts. A good balance between solid growth and gradually easing inflation would support risk assets, but geopolitical developments and new data releases could shift sentiment quickly.

Please continue to check our blog content for the latest advice and planning issues from leading investment management firms.

Alex Kitteringham

16th January 2026