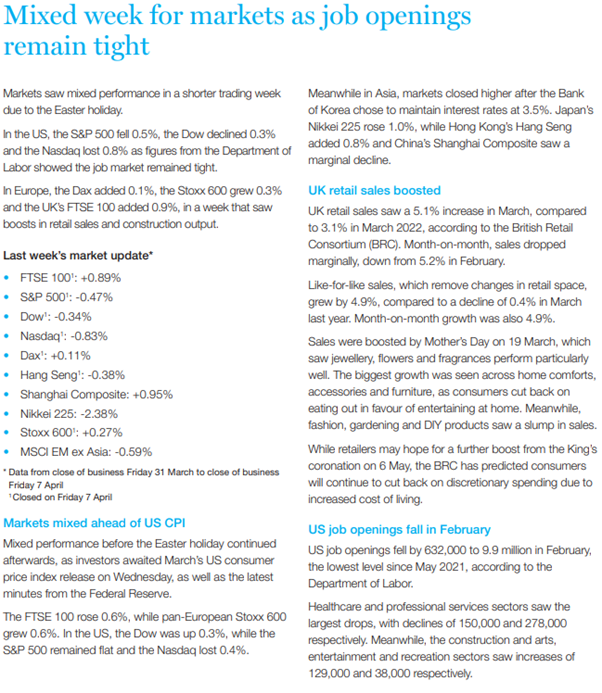

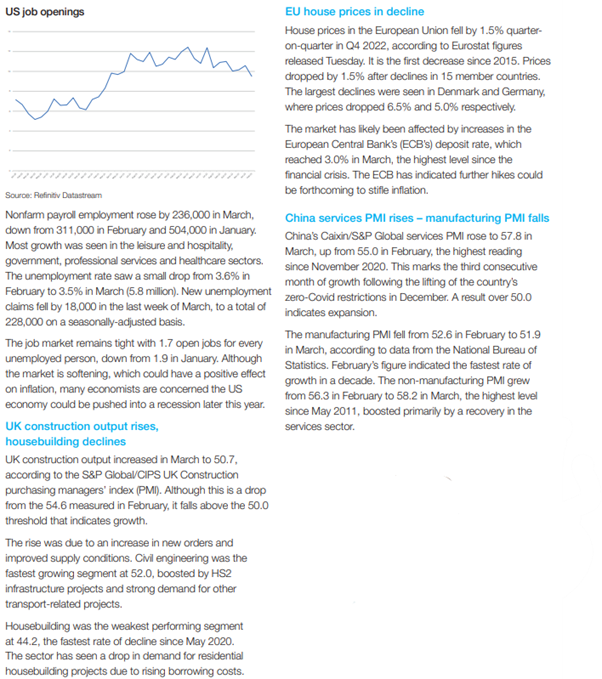

Please see the below article from Invesco received over the weekend:

I’ve just returned from my first trip to Asia since the pandemic, where I was honored to be asked to present at a conference. I’d forgotten how long the flights are, and how the onboard movies are critical to passing the time. On one leg of my journey, I counted 12 superhero movies offered on one flight. Thanks to my insomnia, I wound up watching five of them. A pervasive theme, which I never really paid attention to before when I watched these movies with my kids, was the idea that superheroes have enormous power, but sometimes they can make mistakes in using that power — with very significant repercussions. Another theme is that reasonable, well-intentioned superheroes can have strong differences of opinion, and it’s much easier to believe you are right than to actually be right.

Maybe these themes really struck me now because I think central bankers see themselves as modern-day superheroes, or as close to superheroes as economies can find. And to be fair, they have resolved major threats to economies in recent years, from the Global Financial Crisis to the pandemic to the UK gilt yield crisis last fall. But as institutions with powerful policy tools, there is a built-in risk that they might make mistakes that are far-reaching and very consequential. We saw that first-hand when US Federal Reserve (Fed) Chair Jay Powell insisted that inflation was transitory and chose not to start hiking rates until March of 2022.

From there, of course, the Fed embarked on an aggressive tightening policy. And while we wait to see the full impact of that policy on the economy, I think the risks are increasing that the Fed could make a mistake in where it goes from here.

Inflation is cooling, but the hawks remain wary

It’s clear that the US economy is cooling, and so is inflation. Maybe not all forms of inflation are easing as quickly as the Fed would like, but they have been moving in the right direction. Even core services ex-shelter inflation, the focus of the Fed’s inflationary concerns, is showing signs of progress: the 3-month annualized run rate is at 4% after peaking at 9.2% last year. And we got a very encouraging March US Producer Price Index (PPI) report, suggesting we will likely see further easing of the US Consumer Price Index (CPI), as the CPI tends to follow the PPI with a lag.

What is not clear is how much damage the Fed has already done to the economy because of its aggressive tightening thus far, much of which has arguably not yet shown up in the data because of the lagged effects of monetary policy. And yet, we’re still getting hawkish Fedspeak:

- Last week Fed governor Christopher Waller said there has been minimal progress on inflation in the last year and more rate hikes are needed to get inflation under control. He said inflation “is still much too high and so my job is not done.”

- San Francisco Fed president Mary Daly said, “While the full impact of this policy tightening is still making its way through the system, the strength of the economy and the elevated readings on inflation suggest that there is more work to do … How much more depends on several factors, all with considerable uncertainty attached to their evaluation.”

- Perhaps more concerning was what we got from the minutes of the Fed’s March meeting: Federal Open Market Committee (FOMC) participants observed that “inflation remained much too high” and that “the labor market remained too tight.” It seems the Fed would likely have hiked 50 basis points had the banking sector mini-crisis not occurred in March.

Luckily, there are some cooler heads that will hopefully have an impact on Fed deliberations. Chicago Fed President Austan Goolsbee said the Fed should proceed cautiously with any more rate hikes given the stress in the banking system, “At moments like this of financial stress, the right monetary approach calls for prudence and patience.”

Other central banks are taking a hawkish tone

The Fed isn’t the only central bank talking hawkishly:

- European Central Bank (ECB) President Christine Lagarde continues to share her concerns about inflation. Last week she warned that she expects price pressures to remain high for some time. And now the ECB is considering another “jumbo” rate hike at its next meeting. Don’t forget the ECB is also busy working to rapidly reduce the size of its balance sheet.

- Last week Bank of England Governor Andrew Bailey assured that the mini-banking crisis would not have an impact on the path of rate hikes: “What we have not done — and should not do — is in any sense aim off our preferred setting of monetary policy because of financial instability. That has not happened.”

I think the Fed poses the most danger to the US economy given how much tightening it has done and given the significant economic weakening that has already occurred, as we have seen in falling Purchasing Managers’ Indexes. But other central banks that continue to tighten in this environment also pose a risk to their respective economies. We just don’t know how much damage has already been done. This adds to the uncertainty around what central banks will do next. As San Francisco Fed President Mary Daly made clear, “… there are good reasons to think that policy may have to tighten more to bring inflation down…But there are also good reasons to think that the economy may continue to slow, even without additional policy adjustments….” Or as Christine Lagarde said in an interview on Sunday, “… we are faced with high uncertainty because of multiple factors, you know, from all corners of the world.”

The impact of aggressive tightening

Besides the contributions it has made to the mini banking crisis, the Fed is causing other problems too as a result of its aggressive tightening. For example, net interest on public debt has risen 41% thus far in fiscal year 2023 versus fiscal year 2022 largely because of the increase in interest rates. Discussion of this topic might not be found in the FOMC minutes, but it’s an important one since money spent servicing debt is money not available to be spent in other, more productive ways. I can’t help but wonder that, with superheroes like this, who needs supervillains?

Then there is the uncertainty around the debt ceiling. We have to worry that if an agreement is not reached expeditiously, we may have a repeat of the summer of 2011 — or worse. I hope that’s not the case, but in this politically charged environment, it could be.

Implications for investors

As I conclude this commentary, it occurs to me that it’s been another week in which I’m writing about central banks. I realize my central bank commentary series is starting to rival the number of superhero movies I’ve seen — but unfortunately, the reality is that central banks are still largely controlling the narrative when it comes to both economies and markets.

In my view, the current environment with central banks argues for defensive positioning in the very near term, especially in the US, for those who are tactical allocators. However, for those who are strategic allocators, I believe it’s time to start looking for opportunities to selectively add to one’s portfolio.

Whether you are a tactical or strategic allocator, there are two asset classes I believe may perform well in the near term and the longer term:

- Within equities, I’m most positive on the technology sector. Many tech companies are reducing costs, which should help take pressure off profit margins. In addition, many tech stocks offer secular growth at a time when growth is scarce, which should make them more popular with investors.

- Within fixed income, I’m most positive on investment grade credit. High quality debt with relatively high yields makes sense to me in this environment.

With both these views, the main short-term risk, especially for tactical investors, is that continued hawkishness by the Fed in excess of what markets already expect could lead to some renewed upward pressure on long-term interest rates, which in turn could drive longer-duration assets like tech equity or investment grade credit prices somewhat lower. But with inflation cooling and the economy slowing, the Fed should be at or near the end of the tightening cycle, which should limit these risks.

In general, though, I favor being diversified across and within the three major asset classes: equities, fixed income and alternatives.

I believe it also makes sense to be globally diversified across asset classes. Western Europe is further behind in its rate hiking phase than the Fed, which suggests that US fixed income and longer-duration sectors of US equities (like technology) are probably better positioned than European fixed income or growth/tech equities.

China is in a much earlier stage of its reopening and recovery, with much less inflation risk (since its government didn’t do major job protection programs, fiscal transfers, or monetary easing in the way the West did, accounting for a less aggressive reopening rebound). The People’s Bank of China can therefore afford to be much more dovish, pointing to a better overall financial environment than in the West. This environment suggests “risk on” positioning may perform better.

Emerging markets as a whole are in a more advanced phase, but with major differences, calling for diversification and active country selection and risk management: Some are arguably at or near in the end of tightening in many cases (such as India), though there are others where more hiking may be needed (South Africa for example, and perhaps parts of Central/Eastern Europe, which still have very high inflation and are probably likely to keep leading the ECB in hiking) or where policy and political uncertainty point to sustained ultra-high rates (like Brazil).

The key for investors is to understand where the risks are, both upside and downside. Right now, many of those risks are coming from central banks. While well intentioned, central bankers don’t often merit superhero status. Don’t forget that central bankers are only human, and they can often be driven by the same emotions that can hobble investors from achieving their goals, such as pride and fear. Central bankers only carry briefcases and financial calculators, not magic lassos and sabers. And while they might wear Canali suits, they don’t wear capes.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Andrew Lloyd DipPFS

24th April 2023